The European Commission released draft Delegated Act of the Taxonomy criteria

- 5-minute read -

On November 20, 2020 the European Commission published the long-awaited Draft Delegated Act under the Taxonomy Regulation[1], on climate change mitigation and climate change adaptation. This legal text specifies the technical screening criteria under which specific economic activities qualify as contributing substantially to climate change mitigation and adaptation and for determining whether those economic activities cause significant harm to any of the other relevant environmental objectives. The activities and criteria considered to be enshrined in law are based on the recommendations of the Technical Expert Group (TEG) on Sustainable Finance published in March 2020. The Draft Delegated Act for these two objectives is now under a four-week public consultation before approval by the European Parliament and Council of the European Union (EU) by the end of the year (they can only accept or reject the proposal in full and not amend it).

More precisely, the Commission published:

- A draft Delegated Regulation (15 pages)

- An annex for climate change mitigation objective (Annex I - 233 pages)

- An annex for climate change adaptation objective (Annex II - 281 pages)

All the documents released are available here. As a reminder, the technical screening criteria for the four other environmental objectives — sustainable use and protection of water and marine resources; transition to a circular economy, waste prevention and recycling; pollution prevention and control and protection of healthy ecosystems — will be established by the end of 2021.

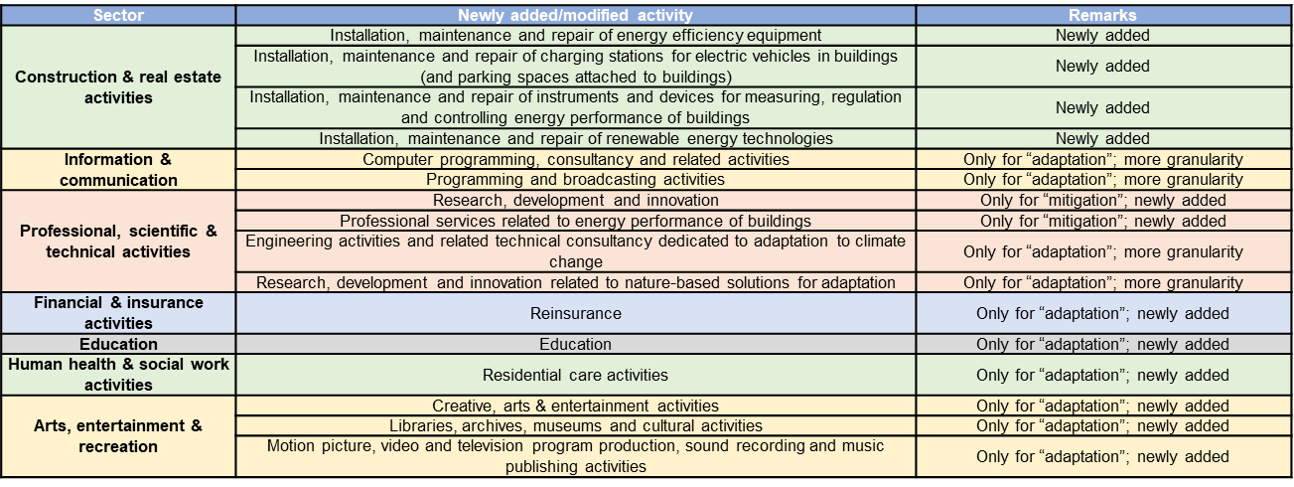

Compared to the TEG’s March 2020 report (see our report “EU Taxonomy Skydiving Kit”), this Draft includes more granularity for the classification of activities in manufacturing, energy, transport and building sector. Sub-categories have been created within existing sectors, in addition to newly created sectors such as “Information & communication”, “Professional, scientific & technical activities”, “Financial & insurance activities”, “Education”, “Human health & social work activities” and “Arts, entertainment & recreation” sectors. Metrics and criteria have been developed for newly assessed activities, reaching a total of 90 activities assessed for mitigation (against 70 in the previous version) and 98 for adaptation (against 69 in the previous version). The table below provides a synthetic view of the changes across the categories of activities assessed. One welcomes the provision of technical screening criteria for “brown activities” that were previously out of the TEG’s review scope, namely sea and coastal freight and passenger water transport or low carbon airport infrastructure.

Table 1: Overview of the activities & sectors changes

Some criteria and thresholds previously proposed by the Technical Expert Group (TEG) have been modified. For instance, the criteria for buildings to be classifieded as energy efficient has been tightened and for construction, life cycle analysis has been added as a requirement for the construction of new large buildings.

Meanwhile, several thresholds still need to be completed with “the average value of the top 10% of installations based on the data collected in the context of establishing the EU ETS industrial benchmarks for the period of 2021-2026 and calculated in accordance with the methodology for setting the benchmarks set out in Directive 2003/87/EC.” (Annex of the Delegated Act, EU Commission, November 2020), notably for the manufacture of cement, aluminum, iron & steel, carbon black, disodium carbonate, organic basic chemicals and of nitric acid. This calibration based on the top 10% of installations is by construction purely relative and quite far from other screening critieria aiming at carbon neutrality alignment through claimed science-based approach. If a sector is well advanced in its decarbonization, there is no reason to set an arbitrary threshold based on a sole BAT or performances. Moreover, as far as we know, the information for the period 2021-2026 is not yet available on such EU-ETS performances, and it is unclear when it will be [2].

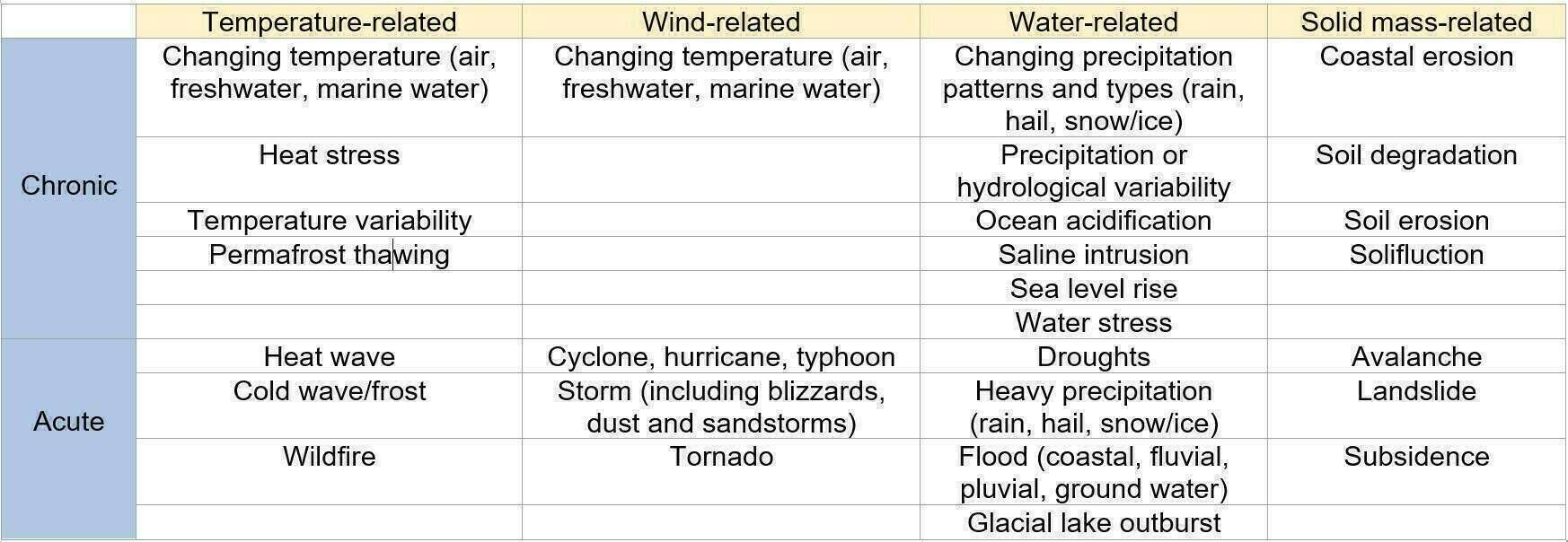

Except for “professional, scientific & technical” and for “financial and insurance” activities, there is a unique technical screening criterion for substantial contribution to climate change adaptation for the 98 activities assessed. It states that the economic activity should implement adaptation solutions that reduce the physical climate risks (see the list in table 2) that are material to that activity. The risk assessment should be proportionate to the scale of the activity and its expected lifespan (for investments into adaptation solutions activities with an expected lifespan greater than 10 years, the risk assessment is performed using high resolution, state-of-the-art climate projections across a range of future scenarios). The climate projections and assessment of impacts are based on best practice, available guidance and take into account the methodologies in accordance with the Intergovernmental Panel on Climate Change reports and scientific peer-reviewed publications. Moreover, the adaptation solutions implemented should not adversely affect the adaptation efforts of other economic activities; favour nature-based solutions or rely on blue or green infrastructure, are consistent with local, sectoral, regional or national adaptation efforts and are measured against pre-defined indicators.

Table 2: Classification of the climate-related hazards

Source: Annex II, “Draft Delegated Acts”, EU Commission (Nov. 2020)

What’s next ?

The draft Delegated Acts for the “adaptation” and “mitigation” climate objective would certainly trigger opposite reactions across different actors affected by those regulations. It is possible, though we believe quite unlikely unless massive controversy, that following the current public consultation, some of the thresholds could be watered down or tighten up. We will carry an assessment of criteria per activity that we will make available upon request (with a two-fold evaluation considering usability and stringency).

The European Union great strides in sustainable finance is hailed and encouraged by most of the European market participants. The public consultation launched in May 2020 by the EU on its “Renewed Sustainable Finance Strategy” (RSFS) to which more than 600 actors have participated revealed 58% of respondents believe that “Major additional policy actions are needed to accelerate the systematic sustainability transition of the EU financial sector.” However, there are still mixed positions on a number of topics including the usability of the EU Taxonomy for the public sector or for EU-level public spending frameworks. There is also mixed support for taxonomies of low and negative impact activities (“brown taxonomy”) with 48% of 427 respondents showing support, while 39% disagree. In our view, financial market participants’ main challenge as of today is the lack of robust data and homogenized methodologies that impede the market to gain momentum. Then, the EU’s sustainable finance agenda could better consider and encourage the transition of the European economy. It is key for the success of this task to go beyond a binary approach. The risk is to confine pure ‘green’ activities into a niche market, and to exclude some activities from European sources of financing, missing the mark on the social implications of such abrupt decision.

All that being said, despite several shortcomings in its usability, the EU Taxonomy remains the most sophisticated taxonomy among those developed by other jurisdictions (such as China, Canada, Japan, Russia, Mongolia, South Africa, for which we will publish a dedicated benchmark in the coming weeks).

One notices that the EU is sparing no effort to support transition action towards sustainable growth, balancing social, economic and environmental sustainability. In particular, in order to alleviate the debt burden of several countries, the emergency aid program called “Support to mitigate Unemployment Risks in an Emergency” (SURE) has been deployed by the EU (see our article on EU Social bonds). A dedicated working group has been created on a possible social taxonomy within the Permanent Sustainable Finance Platform. Meanwhile, the future Green Bonds from the EU will reportedly be using the Taxonomy (specifics are unknown) and the EU-Green Bond Standard. The use cases of the Taxonomy are manifold, as exemplified by the French governement, which plans to use the EU classification for its public export climate supporting mechanism (see our article this month).

On climate action, the EU is currently setting climate and energy targets for 2030. A recent draft text for the European Council meeting states that 55% cut to 1990 levels of emissions would be delivered “collectively,” taking “into account national circumstances. This goal reflects a recommendation by the European Commission in September 2020 as part of its proposed EU Climate Law. This text also promotes “common, global standards for green finance” and calls for a legislation for EU Green Bond by June 2021. The EU’s action on sustainable finance is ambitious[3] and the EU Taxonomy is undoubtedly at the core of its strategy.

[1] See the European Commission press release here (Nov. 2020).

[2] Following the collection and submission by Member States of data to determine free allocation at installation level and to update benchmark values, the Commission will assess the data collected and will calculate the updated values for the 54 benchmarks throughout 2020 (European Commission).

[3] Read more about the EU action plan on sustainable finance on the European Commission website here.