EU TAXONOMY FOR SUSTAINABLE ACTIVITIES

OUR SEPTEMBER 2020 PUBLICATION (NEW)

SKYDIVING KIT

As of September 2020, there are four months left before the publication by the Commission of the first round of the so-called “Taxonomy Delegated Acts”.

These legally binding acts are long awaited because they will encompass Taxonomy’s technical screening criteria (i.e. metrics, thresholds, etc.) on climate change mitigation and adaptation. This report is a skydiving kit to prepare investors and issuers for the great leap into the “Taxonomy era".

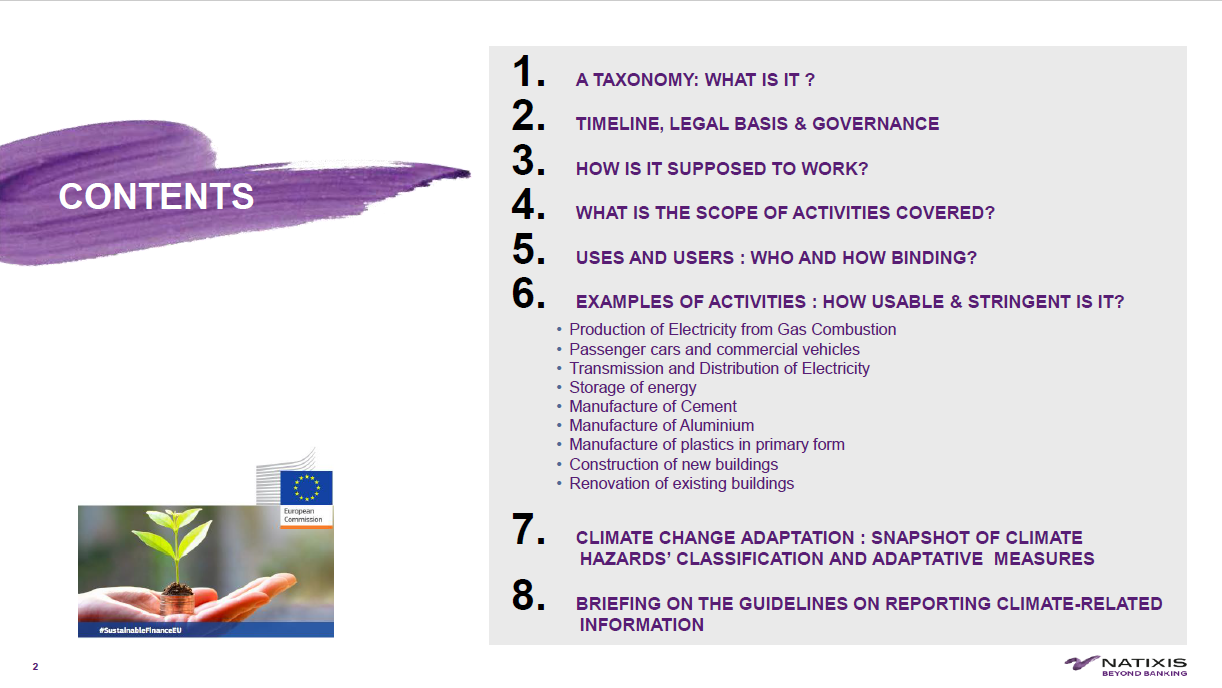

It is structured across 33 questions revolving around legislative process and forthcoming milestones, overall EU's efforts to greening its financial system, key features of the EU Taxonomy, its practical use and requirement per actor categories and key updates from the TEG's final reports.

OUR JULY 2019 PUBLICATION

Vade mecum to digest the 414-page Report from the TEG

Natixis Green & Sustainable Hub’s Center of Expertise is delighted to share with you our EU Taxonomy special report :

“Vade mecum to digest the 414-page Report from the TEG”.

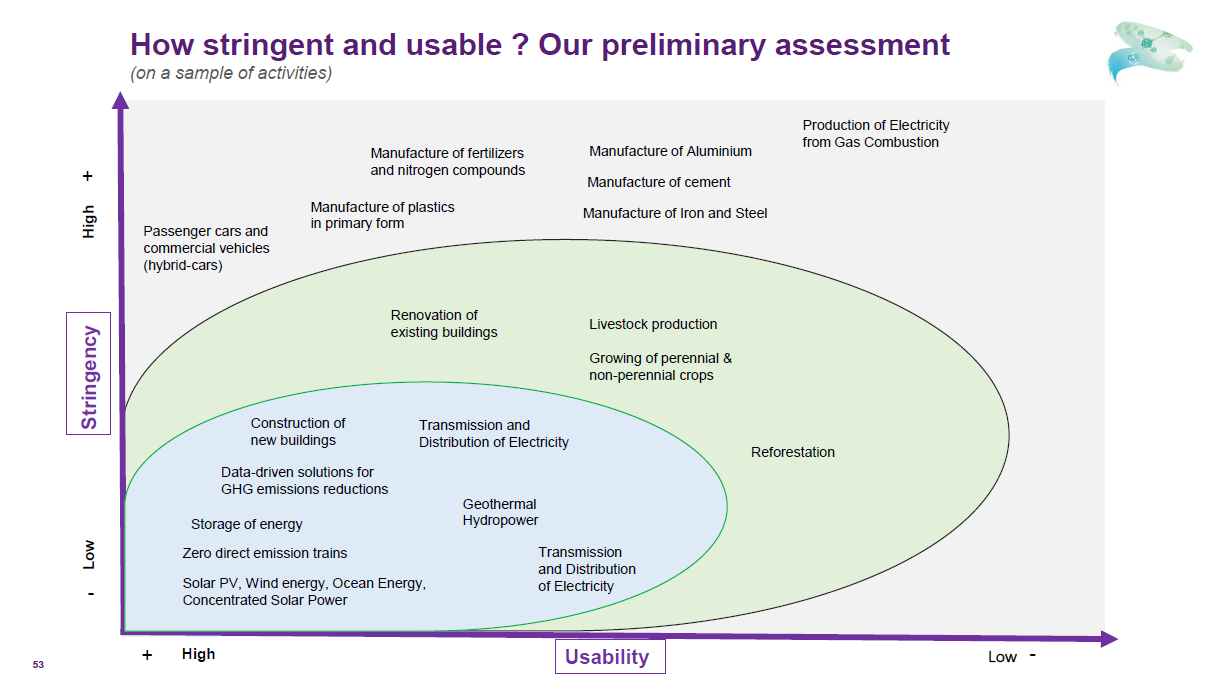

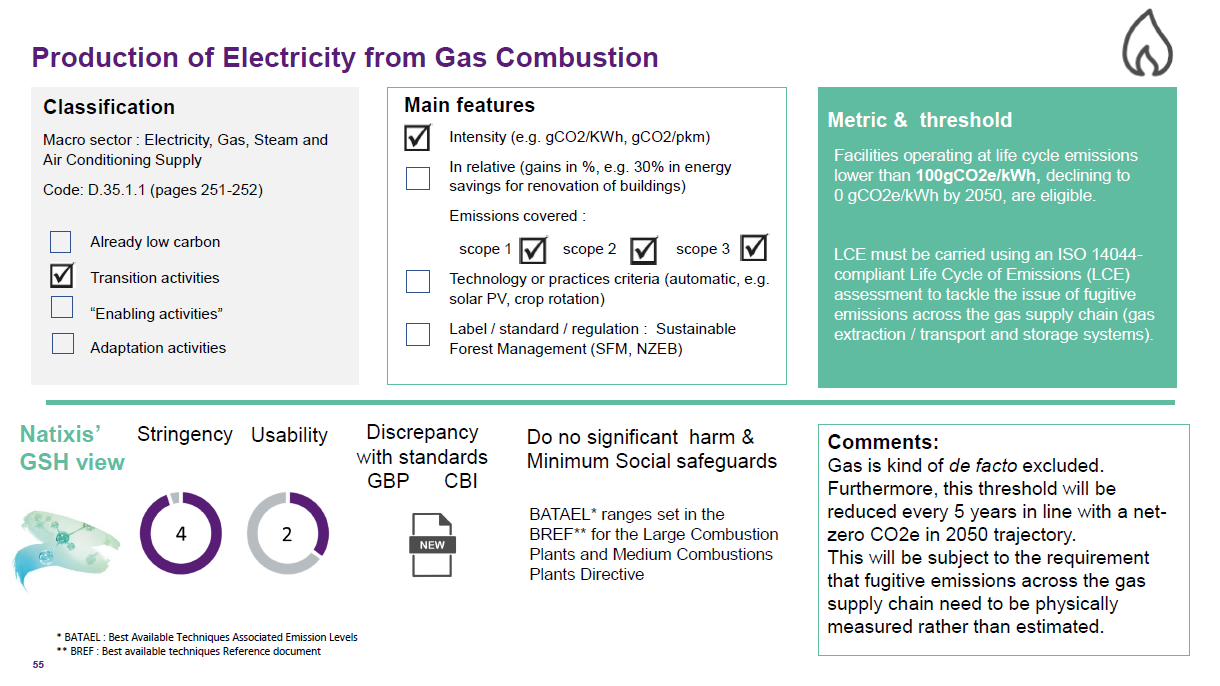

With this publication, Natixis GSH intends to raise awareness and understanding (in particular the Q&A and the stringency and usability activity assessment sheets) on what is at stake, on the tremendous work that has been done by the Technical Expert Group and the one that looms ahead.

This report is a first of series. Coming next our analysis of the EU Green Bond Standard and of on Climate benchmarks and benchmarks’ ESG disclosures.