France maps green and brown expenses over 2021 budget proposal – auspicious developments for climate change mainstreaming and sustainable finance

As public debate over the ecological transition creates pressure on governments, transparency & availability of information on the environmental impact of public spending are necessary to mainstream environmental finance. In September 2020, the French government released a report mapping positive and harmful impacts of its 2021 State Budget proposal. Green budgeting tools touch upon harmful expenditures and brown taxonomies. The implications and methodological challenges of such an analysis are plentiful. Challenges relate notably to the perimeter of analysis and raise several questions: How to deal with tax and/or budgetary expenses ? How to consider personnel and operating expenses ? Should public spending be delineated between central State and decentralized and independent agencies ? Some areas are difficult to analyze, for instance education or defense. The definition of green or brown in itself is challenging because of the lack of criteria, data shortages and/or glut, and sometimes burdensome data collection & analysis processes. One also wonders what scale of rating and number of notches is adapted. Is it more convenient to use binary criterii or ranges of quantitative thresholds ? Can contradictory environmental objectives compensate each other ? There are numerous potential uses of these green budgeting tools that are hindered by comparability challenges over time and between countries. However, these tools cannot be static because methodological refinements and adjustments are necessary. Lastly, there is a need to take into account social criteria in the review of brown expenses. Overall, a balance between simplicity and sophistication must be found.

Introduction

The Ministry of Economy and Finance of France released on September a report on the environmental impact of the State budget in the annexes of the 2021 Finance law proposal. This first report of this kind in France gives us the opportunity to address the topic of “green budgeting”, a powerful “accounting” tool to identify “brown public expenditures” and monitor, steer and report on green public policies and more importantly on environmental costs and benefits of overall public policies. . These green budgeting tools are moreover to become very useful guidance and materials to structure Green Bonds for Sovereigns. These tools help mainstreaming climate or environmental considerations into ordinary budgetary programs and identifying areas of progress.

Paris Collaborative on Green Budgeting

The “Paris Collaborative on Green Budgeting” is an OECD initiative launched by its Secretary-General Angel Gurría during the 2017 One Planet Summit. The aim of “green budgeting” is to weight how much harm and benefit a public budget creates on the environment, through “pure green” budgetary programs but above all through “mainstream policies”[1]. It aims at breaking silos across policies to track areas of improvement, identify priorities and pinpoint inconsistencies.

Green budgeting consists in tools and methodologies[2] that assess and monitor the impact of public expenses on environmental objectives. These tools contribute to the alignment of budgets within the OECD budgetary governance principles. These principles include designing budgets that identify, assess and manage prudently longer-term sustainability in line with national development needs while ensuring budget documents are transparent and accessible, and provide reliable information for the public, which fosters public debate on budgetary choices. Green budgeting is to be an integral part of these budgetary governance principles[3].

Tools on the top of Finance Ministers’ agenda on Climate Action

This OECD initiative on Green Budgeting was followed by the creation of a “Coalition of Finance Ministers for Climate Action”[4] whose members committed to the application of the Helsinki principles, which consist in:

- Aligning policies with the Paris agreement commitments,

- Sharing best practices within the working group,

- Working towards effective carbon pricing,

- Integrating climate change into macroeconomic, fiscal and budgetary policies,

- Mobilizing private resources of climate finance

- Engaging actively in the elaboration of nationally determined contributions.

The elaboration of green budgeting tools can directly put into practice the first four principles while fostering the others.

Green budgeting guidelines in France

In September 2019, a joint mission between the Auditing Department of public Treasury of France (Inspection générale des finances, “IGF”) and the French General Council on Environment and Sustainable Development (“CGEDD”), released a method for green budgeting[5]. The proposal of this IGF-CGEDD joint-mission paved the way for a report on the environmental impact of the State budget by the French Minister of Economy and Finance. This report accompanied the release of the 2021 Finance law proposal[6].

The IGF-CGEDD joint-mission made the following conclusions on the way a green budgeting analysis should be conducted:

- The perimeter of the analysis should cover the entire budget which includes both fiscal revenues, investment expenses and operating expenses.

- The analysis should assess the impact of the budget on a variety of environmental objectives and not focus only on climate change. These objectives are inspired by the EU Taxonomy Regulation (2020/852)[7] and are:

- Climate change mitigation

- Climate change adaption and prevention of natural risks

- Water management

- Circular economy, waste and technological risks

- Pollution control and reduction

- Biodiversity and protection of natural, agricultural and forest surfaces

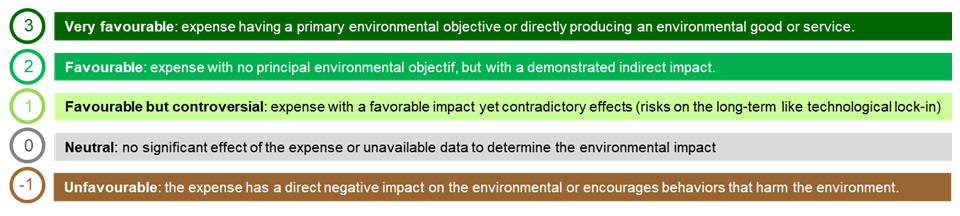

- The report should analyze both positive and negative impacts on the environment, which implies the identification of “brown expenses”. A scale from -1 to +3 is proposed by the mission to rate the environmental impact of the expense in regards with the objectives the following way:

Figure 1 - Rating scale of state budget expenses

Source: Ministry of Economy and Finance of France, Report on the environmental impact of the State budget, Sept. 2020

As we can observe, brown is provided with only one shade or notch. We believe this asymmetry is arguable. To define shades of brown, one could factor in dimensions like the “lack of substitutes or alternatives”, the “end-purpose of the assets or projects financed by the program” (and whether it helps fulfilling vital needs like access to electricity in remote areas), the time horizon, and the “carbon lock-in triggered by the project” (See our article on why we need a shaded taxonomy).

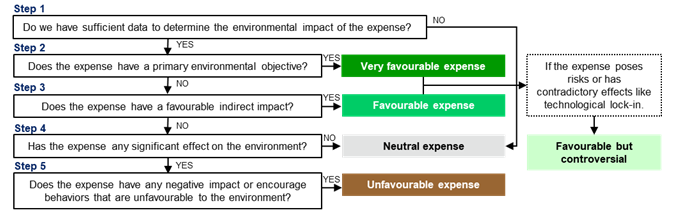

Figure 2 - Decision tree synthesizing the rating process

Source: Natixis GSH

How did France map its green and brown expenses for its 2021 budget?

In the annex of the 2021 Finance law proposal, an environmental report of the State budget is included[8]. It maps green and brown expenses of the State budget[9]. It mentions the IGF-CGEDD joint mission report yet did not follow all the guidelines proposed by the mission.

1. The perimeter of the assessment by the French Ministry of Economy and Finance comprises the entirety of global state expenses, which amount to €488.4 bn in the 2021 budget proposal, as well as 475 fiscal expenses (so-called “niches”) representing €85.9 bn.

- Among fiscal expenses, 107 of them are non-neutral (they either have a positive or negative impact on at least one environmental objective) and represent a total of €11 bn.

- Among this perimeter of global state expenses we can find expenses that are controllable by the State (€290.1 bn), State personnel pensions special accounts (€58.7 bn), State debt relief special accounts (€37.1 bn), levies on receipts to the European Union (€26.9 bn), transfers to local and regional authorities (€48.5 bn), as well as measures from the recovery plan (€22 bn) that will be disbursed in 2021[10].

- Out of these €22 bn, €6.6 bn have been deemed favourable (included in the “Ecology” pillar of the French recovery plan) and partly explains why “green” expenses went up from €29.6 bn in the 2020 Initial Finance Law to the projected €38.1 bn in 2021.

Figure 3 - Scope of the green budgeting evaluation perimeter (in € million)

Source: Ministry of Economy and Finance of France, Report on the environmental impact of the State budget, Sept. 2020

2. France assesses the environmental impact of the budget according to six environmental objectives[11]. A measure can thus be deemed to have a “mixed effect” if it has a positive impact on one of the objectives and a negative impact on another objective: for instance, nuclear energy is low-carbon yet poses technological risks and waste management issues and is thus rated as having a “mixed” effect.

3. Expenses that have “a revenue effect”(like social transfers to households) without any environmental conditionality (see our article about public support conditionality) have been deemed to have a neutral effect. It is the case for instance for transfers to companies (the research & development tax credit could potentially finance harmful or environmentally friendly projects) or to the UE or to regions. The main explanation lies in the difficulty to track their final destination or purpose. This is an improvement axis for future green budgets. In the table below we discuss other methodological conventions and identify potential changes to enlarge the scope of analysis.

Figure 4 – Examples of methodological choices in the environmental analysis of the French State budget

|

Areas |

Choices & methods |

Comments and/or potential changes |

|

Building & digital |

Budget and tax expenditures supporting the construction of new housing are allocated a “brown share” as proposed by the inspection mission. For each expenditure, an “artificializing” part[12] is identified, reflecting the unfavourable impact of expenditures financing new housing on the artificialization of soils. In the absence to date of consensual conclusions on the environmental impact of digital, the expenses associated with the dematerialization of services or processes (ex: deployment of electronic minutes) or the construction of new networks (e.g. the “Very High Speed Internet Plan”) have been neutralized. |

In some cases, the lack of scientific consensus or the unavailability of both comprehensive and up-to-date evaluation data has led to the neutralization of some expenditure. This is the case, for example, of expenditure on digitization of public services, in the very high-speed internet or expenditure on real estate linked to the special allocation account "Management of the State’s real estate assets". One expects future assessment of the life-cycle footprint of such technologies. |

|

Personnel expenses |

By way of exception, the wage bill of the services and administrative authorities with an explicit environmental objective is rated as favorable on the objective concerned. |

Other payroll expenditures for other entities or ministries have been neutralized. |

|

Energy & power |

Potential carbon leakages are taken into account, for instance for reduced electricity tariffs for power-intensive industries. It is rated neutral because it incentivizes industries to electrify their processes (rather than using thermal heat) and still provide an incentive towards efficiency as the level of taxation is not zero[13]. |

By contrast with electricity generation, the risk of carbon leakage has not been taken into account when assessing the impact of reduced tariffs for fossil fuel products in energy-intensive installations. These reduced tariffs are rated as harmful. |

|

Nuclear |

Expenditure on nuclear support, including research, is classified as favourable on the climate mitigation axis but unfavourable to waste management. Targeted research on improving nuclear waste management or decommissioning of nuclear plants has been positively rated on the waste axis[14]. |

On technologies that steer political debates, the involvement of specialized independent agencies would be beneficial for the legitimacy of the green budgeting analysis thanks to a stronger scientific anchorage. In the case of nuclear, one naturally involves the Authority on Nuclear Safety (ASN). |

|

Transport |

The support plans for aeronautics and automobile sectors (which together represent €1.5 bn in the State budget) have been deemed to have a Favourable effect on climate change adaptation and pollution control because there are environmental conditions and objectives associated with these plans, just like a €7 bn plan composed of state grants and state-guaranteed loans has been granted to Air France with the conditions that the airline becomes the “most environmentally friendly carrier in Europe” and cuts emissions per passenger/km by half by 2030 with 2005 as a year reference. |

Out of the €2.6 bn that will be invested in 2021 and in 2022 for aeronautics and automobile support plans, the R&D fund for automobile (€300 m) and the support plan for civil aeronautics R&D (€600m) do not mention any environmental conditionality in the recovery plan documents. Modernization and diversification funds (€1.7 bn to be invested in 2021 and 2022) for aeronautics and automobile managed by Bpifrance will “take into account” environmental considerations: one can criticize the lack of details and specific targets concerning these green expenses. |

|

Defense & security |

Defense is one of the 17 missions of the 2021 Finance Law that has been deemed neutral due to lack of data or due to the implementation of the methodology[15]. However, four programs of the “Defense” mission representing €158 m and €89 m of programs related to domestic security addressed the maintenance of water depollution networks, remediation, waste management, nuclear waste and technological risk management works as presented in a budgetary document for year 2020 related to Defense and Security[16]. |

I4CE proposes to look into detail at the 2019-2025 Military Programming Law because no document or authority realized a complete assessment of the environmental impact of defense expenses yet[17]. Issues like biodiversity and depollution are mentioned by the Ministry of Armies in a sustainability report made in in 2012, but quantitative analysis of the carbon impact of fuel consumption and heating has not been carried yet. |

Results & analysis: what is the ratio of brown and green expenses?

The Ministry of Economy and Finance has also used the aforementioned methodology to analyze the 2020 budget, making possible the tracking of green and brown spending evolution. In its report, the IGF-CGEDD joint-mission also proposed an analysis of the then 2020 Finance Law proposal. It allowed us to produce the following graph for comparison purposes.

Figure 5 - Green spending and brown spending in 2020 and 2021 (amounts in €bn)

Source: Ministry of Economy and Finance of France, Report on the environmental impact of the State budget, Sept. 2020

IGF-CGEDD, Green Budgeting: proposal of a method for environmental budget analysis, Sept.2019

|

Reminder: • Green expenses have at least one positive impact on one of the mentioned environmental objectives without having any adverse impact. It means that they scored between +1 and +3 on at least one of the six environmental objectives without having scored -1 elsewhere. |

One notices a €6 bn gap between how much has been accounted as green and brown by the IGF-CGEDD joint mission in the analysis of the then 2020 finance law proposal and the analysis made by the Ministry of Economy and Finance. This gap is not solely caused by the difference between amounts allocated to budgetary missions in the initial finance law and the draft of the budget law for the 2020 budgetary year. One indeed observes different methodologies and perimeters of analysis (for 2021, a lot of expenses have been deemed as “neutral” due to lack of data as explained above) yield different results[18]. State ministries and public entities producing the environmental report on their perimeter are naturally poised to minimize brown expenses and to “bulk” green expenses. It raises the question about who is in charge of the assessment and whether it is meant to be challenged at some point by a public independent authority like the “Cour des Comptes” which audits budgetary programs and governance for instance.

While we are far from hard science and at the very beginning of a journey deemed to get more and more systematic, methodic and scientific, the need for consistent perimeters year on year is probably one of the first discipline to establish so that dynamic interpretation is even possible. One could argue that the use of relative ratio of green and brown expenses (% compared to total expenses) would help comparison. See for example the interpretation of the likely rise in green expenses in 2021: result of higher budget allocation or pure arithmetic of COVID-crisis related overall recovery expenditures?

However, one also need to know the actual impact of changes in green and brown expenses throughout years to get a full picture of the progress made in terms of carbon reduction strategies for instance. The use of indicators related to climate impact (GHG avoided emissions could prove useful), water consumption, waste production or impact on ecosystems and biodiversity could make the environmental report of the State budget into a more comprehensive toolkit.

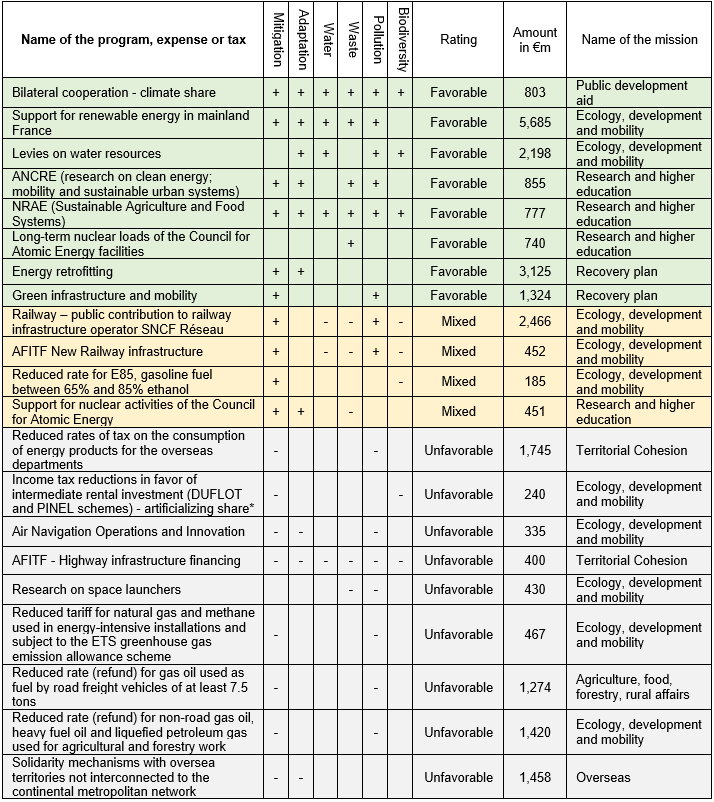

Figure 6 - Summary of major brown, mixed and green expenses and their contribution to environmental objectives, rating, amounts, mission

Remark: a + indicates a positive impact on the environmental objective while a – indicates a negative impact.

As we can see here, it seems any expense or tax that encourages fossil fuel consumption or use is deemed to have an unfavourable impact on the climate change mitigation objective and is thus a “brown” measure. Furthermore, measures that contribue to the increase of soil artificialization, including investment in new railway networks, are deemed unfavourable to the biodiversity objective.

These criterii are thus strict in terms of unfavourable impacts, yet do not provide granularity as to how much good or harm is brought by a spending. For instance, investing in renewable energy in itself does not reduce absolute and relative carbon emissions, yet it is considered green by nature in the green budgeting analysis (for instance, its carbon abatment in France overseas territority where fossil fuels are predominant is much larger than in France mainland)

Reducing "brown” expenses might often have a greater impact in terms of environmental and climate footprint than increasing green expenses. Thus, a voluntary decrease in a brown expense, like a suppression of taxes favoring fossil fuel consumption, could be highlighted in the environmental report of the state budget and presented in a category of “reduced brown spending” for instance and accompanied by specific explanations, including on measures that help to mitigate the social consequences of such reductions (a lot of reduced tariffs on carbon-intensive elecitricity are concentrated in oversea territories and their removal could have negative social impacts). Indeed, if we can prove that the decrease was not contingent but planned and voluntary, then it could be worth to mention it for stakeholders and for the public.

Figure 7 - Distribution of green expenses (on the left), mixed expenses (in the middle) and brown expenses (on the right) by budgetary missions (in € million)

Remark: most brown expenses are included in the “Ecology, development and mobility” budgetary mission, but they mostly include programs of the mobility and solidarity components of the mission carried out by the Ministry of Ecology. Thus, among these €4,883 m, we can find the Solidarity mechanisms with oversea territories not interconnected to the continental metropolitan network (€1,458 m); reduced tariffs on various fossil fuels used for light transport vehicles (€1,274 m); for agricultural purposes (€600 m) or by energy-intensive installations (€467 m); as well as construction of new highway routes (€400 m).

Concerning green expenses, unsurprisingly, almost 45% of green measures identified in this green budgeting assessement are carried out by the Ministry of Ecology within the budgetary mission Ecology, development and mobility. Some measures of the recovery plan which covers multiple sectors (building, rail, circular economy, hydrogen) are separately included and are carried out by the Ministry of Economy, Finance and Recovery. Immaterial assets and expenses can be deemed green (they are also eligible to financing by a sovereign green bond) and represent around 12.5% of the green expenses. It is also worth to note that some public development aids carried out by the Foreign Affairs Ministry are considered favourable to the environment because they include environmental components.

Concerning mixed expenses, railway is the big player here because even though rail transportion emits less greenhouse gas emissions than road, new infrastructure could negatively impact biodiversity by affecting landscapes and physically cutting ecosystems if infrastructure is not built[19] in paralel to ensure ecological continuity. New worksites also generate waste and consume a lot of water.

This assessment shows there is a need to assess the environmental impact of ad hoc projects at project level before consolidating it at ministry level and finally at budget level. One would expect more granularity for future green budget analyses. Artificialization part have been used to assess the harmful impact on biodiversity of the construction of new housing as mentioned in figure 4. In future green budgeting exercices, one could thus expect the French government to implement this same logic to assess the impact on biodiversity or pollution of new physical infrastructure projects like new railway lines with more details.

Fair transition considerations

Concerning brown expenses, most of them are in fact fiscal expenses or tax reductions related to energetic products consumption in overseas, preferred rates for agriculture and solidarity measures for French islands not linked with the metropolitan electricity grid as shown in table 6.

Moreover, the report highlights that it is not because an expense is deemed brown that it has to disappear because they are predominantly related to solidarity measures. A fair transition must take them into account. The adverse environmental rating of an expenditure is not sufficient to conclude that it must be abolished if it meets proven needs for public intervention in favour of another public policy considered to be a priority, for example: the security of populations, balanced land-use planning, equitable access to public services, availability of essential products, etc[20]. The value of the rating is then to highlight these priorities, examine the right tools for public intervention and, if the expenditure whose impact is unfavorable is to be maintained, seek to reduce this impact.

Comparative analysis

This OECD initiative has inspired some analyses made by Mexico, Nepal and Ireland. Mexico[21] for instance proposes a mapping of the impacts of the green budget on GHG emissions reduction for sectors like electricity and heat generation, building, transport, industry, agriculture, forestry and land use, as well as the completion of projects related to each sector (in the transportation sector, the completion of cycling and railway infrastructure in monetary amounts is to be assessed). Benchmarks are thus set for each of the four environmental goals which is meant to allow for international comparisons. Nepal was one of the first country to adopt a climate budget tagging at program level. Adaptation and mitigation were not split yet a short list of thematic areas covering all economic sectors was used. Indonesia[22] is linking climate change targets and SDGs in a national mid-term development plan. A strategic framework has been adopted to integrate environmental policy into the development agenda: the government of Indonesia is working on a transparency framework that would enable the tracking of progress in the implementation of a low carbon development. It is difficult though to compare how green budgeting is done worldwide because there is a variety of methods, of identified environmental objectives and of scopes for the analysis.

Green budgeting prospects

We have identified some areas of improvement for better transparency and monitoring of environmental policies:

- The granularity of the analysis can be progressively improved: entire budget programs and missions are mapped as either green, brown or mixed while they often represent huge masses of money to which coefficients could be applied to capture and segregate between positive and negative aspects within each program.

- One would expect over time to have the ability to gauge the scale of the impact or environmental efficiency of policies: e.g. carbon emissions, avoided emissions, avoided waste or energy consumption per euro spent, etc. In other words, evaluation of the actual consistency of a given policy/program with its ecological transition remit as well as the environmental cost/benefit assessment of public money spending would be welcomed.

In the future, the French government could use stress-tests or shadow prices for carbon to verify if budgets are in line with narrowing windows for decarbonization in order to tackle this challenge[23]. Shadow prices on carbon could help it see if efforts are enough to meet decarbonization rate requirements.

- Budgetary governance frameworks must be reformed to strike a smooth combination of strategic planning, multi-annual envelopes and impact methodologies factoring environmental considerations. Greening these budgetary frameworks can help achieve transpartisan and consistent budgeting analyses throughout years. Policy coherence verification mechanisms are also important to guarantee that the benefits of the decarbonization on a given sector are not outmatched by reforms on others.

- Furthermore, we believe it is increasingly necessary to consider embedded/imported emissions (see the joint report from Ademe, Beyond Ratings and OFCE “Carbon taxation at borders: its redistributive impact on French households’ income”, in French only). This could incentivize governments to implement activity relocating policies[24].

- Within a decade, it is likely that each ministry or administration will produce a green budgeting analysis of their own budget later consolidated in a global state budgeting environmental analysis with increased granularity. The budget mapping analysis can also be carried against the 2030 Agenda and its seventeen sustainable development goals (SDGs), as already undertaken by some local governments (the city of Niort in France, Gironde or Var departments) or national governments (Mexico).

- Lastly, all public policies do not have strict or direct budgetary consequences although having a strong impact on the environment. It is the case of regulation that sets standards or bans some technologies (for instance ban on ICE vehicles sales or plastic bags). Thereby, to have a comprehensive analysis of a government’s action on climate change, the analysis of its budget must be completed with an analysis of regulation or standards. It does not mean that these policies do not have a cost in the end - they could indeed erode tax basis if highly emitting production is outsourced (carbon leakages also involve fiscal revenue leakages) - or require financial support for low-income households or some companies.

In our view, green budgeting tools analyzing embedded emissions and reviewing standards and regulation are among the most instrumental tools for the ecological transition.

Green budgeting tools are of great interest for sustainable finance because they can help identifying eligible expenditures for sovereign green bonds issuances. Furthermore, they touch upon environmentally harmful expenditures, providing preliminary elements on the definition of “brown taxonomies”, a topic of growing interest for which there is little sophisticated definition or classification. There are useful to set transition pathways for governments and contribute to the development of skills, tools and bodies necessary to steer finance towards a greener economy while reducing the share of brown expenses. It finally allows for more transparency, public and political debate and understanding of public priorities. They could prove to become essential pillars of a national sustainable finance architecture both by strengthening public capacities and giving visibility to stakeholders and political institutions.

[1] Green budgeting for instance goes beyond expenses dedicated to renewable energy or clean transportation.

[2] OECD, “Recommendation of the Council on Budgetary Governance, February 2015 - available here.

[3] OECD, “OECD Green Budgeting Framework”, 2020. Further information available here.

[4] Further information available here.

[5] IGF-CGEDD, “Green Budgeting : proposition de méthode pour une budgétisation environnementale »,September 2019 - available here.

[6] Ministry of Economy and Finance, “Environmental report on the state budget”, September 2020 – available here.

[7] Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment - available here.

[8] Ministry of Economy and Finance, “Environmental report on the state budget”, September 2020 – available here.

[9] Ministry of Economy and Finance – R.Mestrius & C.Anselin, presentation video of the “green budget”, October 2020 – available here.

[10] Minister of Economy and Finance, Speech of presentation of the draft finance bill for 2021 by Bruno Le Maire, September, 28th 2020 - available here.

[11] The green budgeting objectives selected by the French Ministry of Economy and Finance are the same as the ones mentioned above by the IGF-CGEDD joint-mission.

[12]The impact on this axis is also mitigated by the better environmental performance of new buildings, especially once Environmental Regulation 2020 is applicable. A different percentage of «artificializing» share is applied depending on the type of housing financed.

[13] In the absence of these measures to reduce the cost of electricity, which is one of the main factors in the competitiveness of electricity-intensive industries, offshoring of production could be outsourced to countries where electricity is low-cost and generally more carbon-intensive, particularly in China. The consideration of indirect effects of the measure explains why it is rated neutral for now.

[14] Grants for decommissioning expenses carried out by the Commission of Atomic Energy and grants to the Institute for Radiation Protection and Nuclear Safety (IRSN) which controls nuclear material and the protection of nuclear installations

[15] Military expenditures might be considered as harmful in the future considering fuel consumption for vehicles for instance.

[16] French Prime Minister services, Cross-cutting policy document on “Defense and national security”, September 2019 - available here.

[17] According to I4CE[1], in 2019, out of €2.1 bn of expenses related to real estate (the Ministry of Armies is the biggest public building occupier in terms of surface), €780 m allocated to energy retrofitting can be deemed as green as €1 bn used to acquire and build new housing. Transportation expenses of the Ministry of Armies represented €800 m, out of which more than €600 m are considered brown expenses (fossil fuel consumption just like €275 m of energy consumption in army buildings. More information available here.

[18] This could be due the following divergence: the IGF-CGEDD counted €15.2 bn of tax exemptions or reduced rates (€12.2 bn of tax exemptions or reduced rates on domestic energetic products, €1.3 bn of reduced tax for electricity from carbon-intensive plants, €1.3 bn of fiscal expenses related to new housing), while as for 2021, the Ministry of Economy counted €7.2bn of brown spending from these same tax exemptions and reductions, one could infer that for 2020, it counted less of these taxes as brown than the IGF-CGEDD mission.

[19] This shows how complex it is to combine and abide by all environmental objectives: if infrastructure like special bridges that one can see above highways are being built in parallel, there is some artificialization being carried out even though it is for the benefit of ecological continuity.

[20] In this case, most brown measures enlisted in the Territorial cohesion, Agriculture and Overseas missions indeed happen to be related to solidarity measures with farmers, for social housing or for areas not connected to the metropolitan grid.

[21] Ministry of Finance and Public Credit of Mexico, “Paris Collaborative on Green Budgeting” – presentation of the green budgeting methodology – available here.

[22] Governance of Climate Change, Bankgok Regional Hub, “Climate budget tagging: experience from Asia”, 2016 - available here.

[23] According to a report of France Stratégie (available at https://www.strategie.gouv.fr/sites/strategie.gouv.fr/files/atoms/files/fs-the-value-for-climate-action-final-web.pdf), if France wants to achieve carbon neutrality by 2050, which is the flagship end goal of the French “Low-Carbon National Strategy”, then the following carbon prices have to be applied or at least modelled into the decisions of all economic actors in France: 54 €/tCO2eq in 2018; 87 €tCO2e in 2020; 250 €/tCO2e in 2030; 500 €/tCO2e in 2040 and 775 €2/tCO2e in 2050. It would be virtually impossible to achieve carbon neutrality by 2050 if we fail to integrate these shadow carbon prices into economic decision and thus into budgetary governance.

[24] The rationale that offshore production is more carbon-intense in some cases can be claimed here to justify a bigger perimeter of non-neutral expenses here.

To go further

- Report by the joint mission between the Auditing Department of public Treasury and the General Council on Environment and Sustainable Development over a green budgeting method:

http://www.igf.finances.gouv.fr/files/live/sites/igf/files/contributed/IGF%20internet/2.RapportsPublics/2019/2019-M-015-03_Green%20Budgeting.pdf

- Report by the French Ministry of Economy and Finance over the environmental impact the 2021 State budget:

https://www.vie-publique.fr/sites/default/files/rapport/pdf/276480.pdf

- Annex on the State green budgeting methodology:

https://www.budget.gouv.fr/documentation/fid-download/5774

- French 2021 budget proposal:

https://www.economie.gouv.fr/files/PLF2021.pdf

- I4CE assessment of the 2020 French budget:

https://www.i4ce.org/wp-core/wp-content/uploads/2019/12/2019-11-28-GreenBudget_VA-web-1.pdf

- Mexican strategy on Green budgeting:

https://www.oecd.org/gov/budgeting/SHCP-Mexico-Jose-Francisco-Perez-De-La-Torre.pdf

- Philippines, Indonesia, Nepal and Bangladesh green budgeting overview:

https://www.climatefinance-developmenteffectiveness.org/sites/default/files/climateBudgetTagging.pdf

- Climate public expenditure and institutional review (CPEIR) methodology:

https://www.asia-pacific.undp.org/content/rbap/en/home/library/democratic_governance/cpeir-methodological-guidebook.html

- France Stratégie (February 2019), Report by the Commission chaired by Alain Quinet –Title in English: The Value for Climate Action - A shadow price of carbon for evaluation of investments and public policies:

https://www.strategie.gouv.fr/sites/strategie.gouv.fr/files/atoms/files/fs-the-value-for-climate-action-final-web.pdf