The clash between sovereignty and sustainability?

16 - minute read

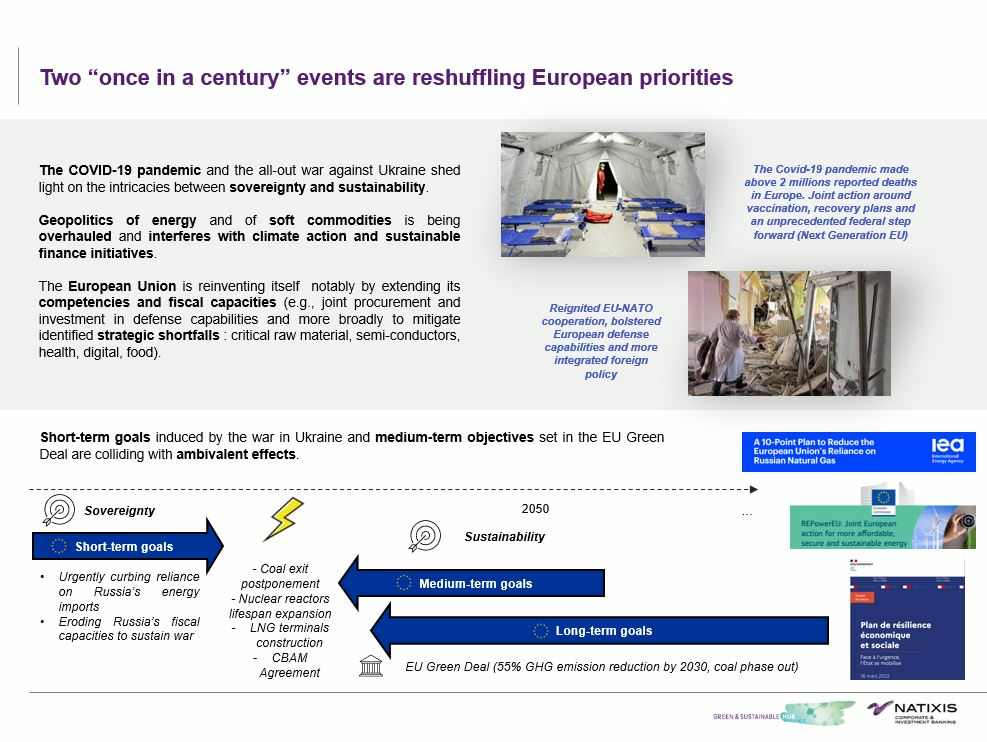

As bombs are falling on Kyiv, Europe’s gas dependency towards Russia could never have felt so pungent. The COVID-19 pandemic and the all-out war against Ukraine shed light on the intricacies between sovereignty and sustainability. These two “once in a century” events epitomize low-probability and high-risk phenomenon. Geopolitics of energy and of soft commodities is being reshuffled and interferes with climate action and sustainable finance initiatives. Short-term goals – curbing reliance on Russia and eroding its fiscal capacities to sustain war – and medium-term objectives set in the EU Green Deal are colliding with ambivalent effects.

Above all, this crisis unveils the untapped ecological potential offered by demand changes. In a nutshell, wearing an extra sweater and lowering the thermostat, or eating less meat, could alleviate gas demand or wheat prices. European political leaders gathered early March in Versailles and committed to “phase out [our] dependency on Russian gas, oil and coal imports as soon as possible”, as well as “to improve its [European Union] food security by reducing its dependencies on key imported agricultural products and inputs, in particular by increasing the EU production of plant-based proteins [1]”.

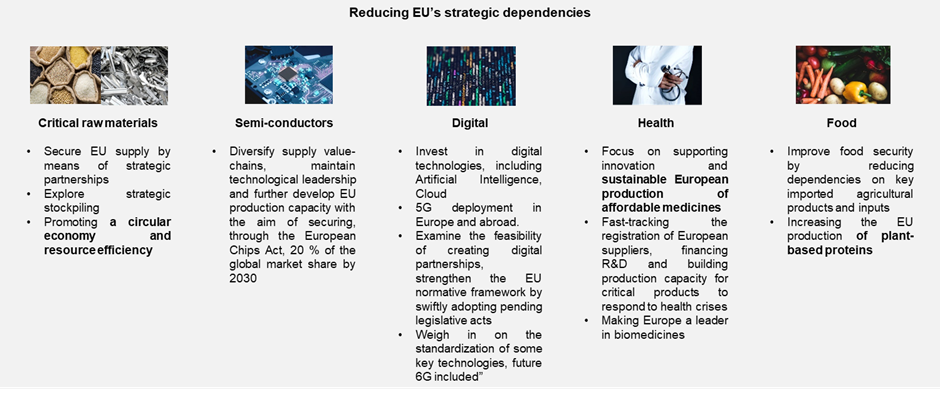

Decision-makers endeavor to drastically reduce reliance from suppliers and/or countries they are at loggerheads with or even enemies. As a reminder, value chains already began to be overhauled following the US-China trade war. A leitmotiv will now guide policies and investments until further notice: achieving strategic control and autonomy on critical sectors like energy, food, health, defense or communication. The two first sectors are among the more material from a climate change mitigation and adaptation standpoint. This article delves into them with the EU Green Deal and “Fit for 55” plan in mind, as well as the inclusion of gas and nuclear in the EU Taxonomy.

***

PART I: Strategic shortfalls around energy & food security

Energy transition: short-term actions & medium-term objectives collide

Russia is sowing the seeds of distress around food security

***

PART II: Taxonomy criteria’s Achilles heel unearthed by the War in Ukraine

Back on the Delegated Act on gas and nuclear activities

A “transitional” role

***

More stringent requirements for nuclear

Nuclear Safety in times of War

***

Gas before the invasion: no one was satisfied

Criteria obsolescence due to the War in Ukraine and LNG extended role

***

PART I: Strategic shortfalls around energy & food security

Key elements

- In 2021, the European Union imported an average of over 380 million cubic metres (mcm) per day of gas by pipeline from Russia, or around 140 billion cubic metres (bcm) for the year as a whole.

- On March 22nd, EU member states had spent ~€17.5bn since the beginning of the Russian invasion on February 24th1 (€6bn in oil, €11bn in gas and €0.5bn in coal)*.

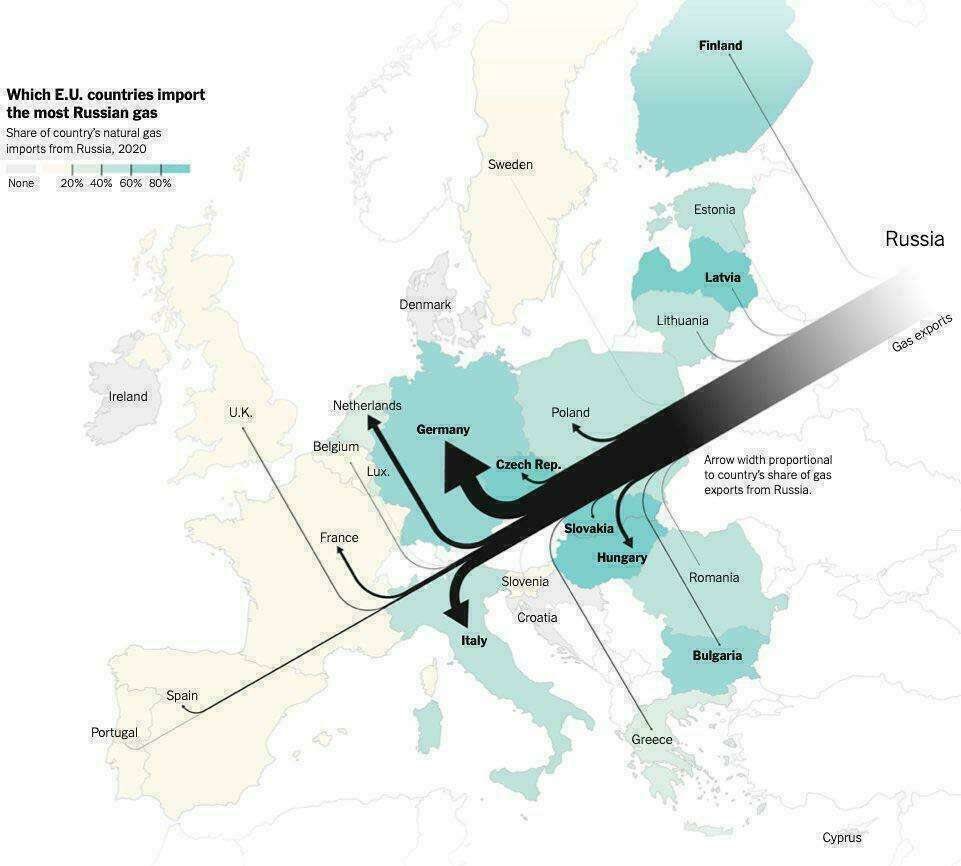

- Germany, Italy, Hungary, Slovakia and the Czech Republic have been the most dependent on gas imports in 2020. It revived debates around national energy mixes.

- Dependency on Russian gas has far-reaching consequences on many sectors as increased prices have been impacting agriculture and its fossil-fuel derived nitrogen fertilizers and pesticides.

- Last but not least, gas and gasoline prices are undermining households’ purchasing power, increasing (risks of) fuel poverty.

*Source: Centre for Research on Energy and Clean Air, details on methodology available here

......

European gas imports from Russia: an extensive and differentiated dependency

Source: New York Times (March 2022), How a Ukraine conflict can reshape Europe’s Reliance on Russia

Energy transition: short-term actions & medium-term objectives collide

Energy security in the short run…

In the long run, the net effects on GHG emissions of this War on Europe will be uncertain and likely ambivalent. Indeed, some decarbonization efforts are accelerated – demand-side management including sobriety and efficiency, support to renewable and nuclear energy [2] –, while others are being loosened, specifically postponing coal phase-outs or building new LNG terminals fraught with carbon lock-in and stranded assets risks [3].

The War could escalate and give birth to a multi-faceted conflict spanning over decades. However, it is unlikely that the access to fossil fuel resources from Russia would be barred to Western markets forever. Therefore, additional capacities and related infrastructures built in the interim period could become stranded should radical political changes occur in Russia, and/or a U-turn in Western diplomacy takes place.

Moreover, history taught that countries and regimes that are deemed pariah at some point in history are rarely shunned forever [4]. For instance, sanctions against Iran and Venezuela may opportunistically be lifted to meet oil supply shortfalls. All the more so that the cut off from the international community is not unanimous and that Russia is shifting southwards to China.

The reliance on Russian fossil fuels imports can either be reduced at the discretion of European countries in order to implement a fully comprehensive set of sanctions against a Rogue State, or unilaterally imposed by Russia and used as a blackmailing weapon. In the meantime, both parts are trying to get rid of this interdependency, Europe by diversifying its supply of gas [5], and Russia by expanding its exports capacities to China through the new pipeline “Power of Siberia 2”. Nonetheless, diversification measures cannot come to fruition overnight. In any case, European households are unarguably going to face skyrocketing energy prices and subsequent fuel poverty risks (see our April 2021 article on fair transition finance).

… Energy independency in the medium…

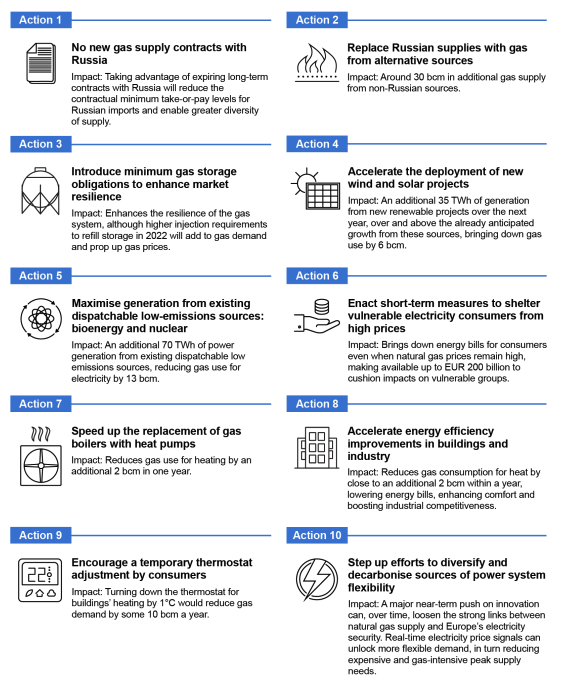

The IEA’s proposal to get rid of Russian gas and cut oil use

The International Energy Agency (IEA) released a plan to reduce the EU’s dependence on Russian Natural Gas on March 3rd. The range of measures is comprehensive, touching upon demand diversification measures, storage capacities, but also support to demand changes and management (replacement of gas boilers by heat pumps, temporary thermostat adjustment, etc.).

IEA’s 10-Point Plan to Reduce the European Union’s Reliance on Russian Natural Gas

With Russia’s invasion of Ukraine causing lower supplies to oil markets ahead of peak demand season, IEA's 10-Point Plan to Cut Oil Use, released on March 18th, proposes actions to ease strains and price pain. “Immediate actions in advanced economies can cut oil demand by 2.7 million barrels a day in the next 4 months.”

REPowerEU Plan

Building on IEA’s proposal, the European Commission proposed an outline titled “REPowerEU Plan” on March 8th.

On top of the aforementioned measures on gas independency, the EU’s blueprint encompasses further actions such as:

- A reassessment of the electricity market design,

- Temporary taxation of windfall profits to finance consumer protection,

- Boosting the Fit for 55 proposals with higher and earlier targets such as doubling biomethane targets to 35 billion cubic meters per year by 2030 (for the reference, see our July 2021 article on the Fit for 55 package).

These measures aim at eliminating the dependency on Russian gas well before 2030 and reducing it by two-thirds by year end.

Versailles Declaration

The European Heads of State or Government gathered on March 10th & 11th in Versailles and endorsed the Commission’s blueprint. The latter is asked to put forward a plan to ensure security of supply and affordable energy prices during the next winter season by the end of March.

Time-bound and precisely budgeted measures shall be disclosed to reduce EU’s overall reliance on fossil fuels, diversify its supplies (use of LNG, development of biogas), further develop hydrogen market, speed up the development of renewables (streamline authorisation procedures).

Heads of State or Government agree to complete and improve the interconnection of European gas and electricity networks and fully synchronize power grids throughout the EU, improving energy efficiency and the management of energy consumption, and promoting a more circular approach to manufacturing and consumption patterns.

“Russia’s war of aggression constitutes a tectonic shift in European history” said the Versailles Declaration. Alike to what the pandemic crisis ushered, the European Union is reinventing itself (see our June 2020 article “Covid-19 crisis in Europe: a midwife for a federalist green & social leap forward”), notably by extending its competencies and fiscal capacities (e.g., joint procurement and investment in defense capabilities and more broadly to mitigate identified strategic shortfalls; see below).

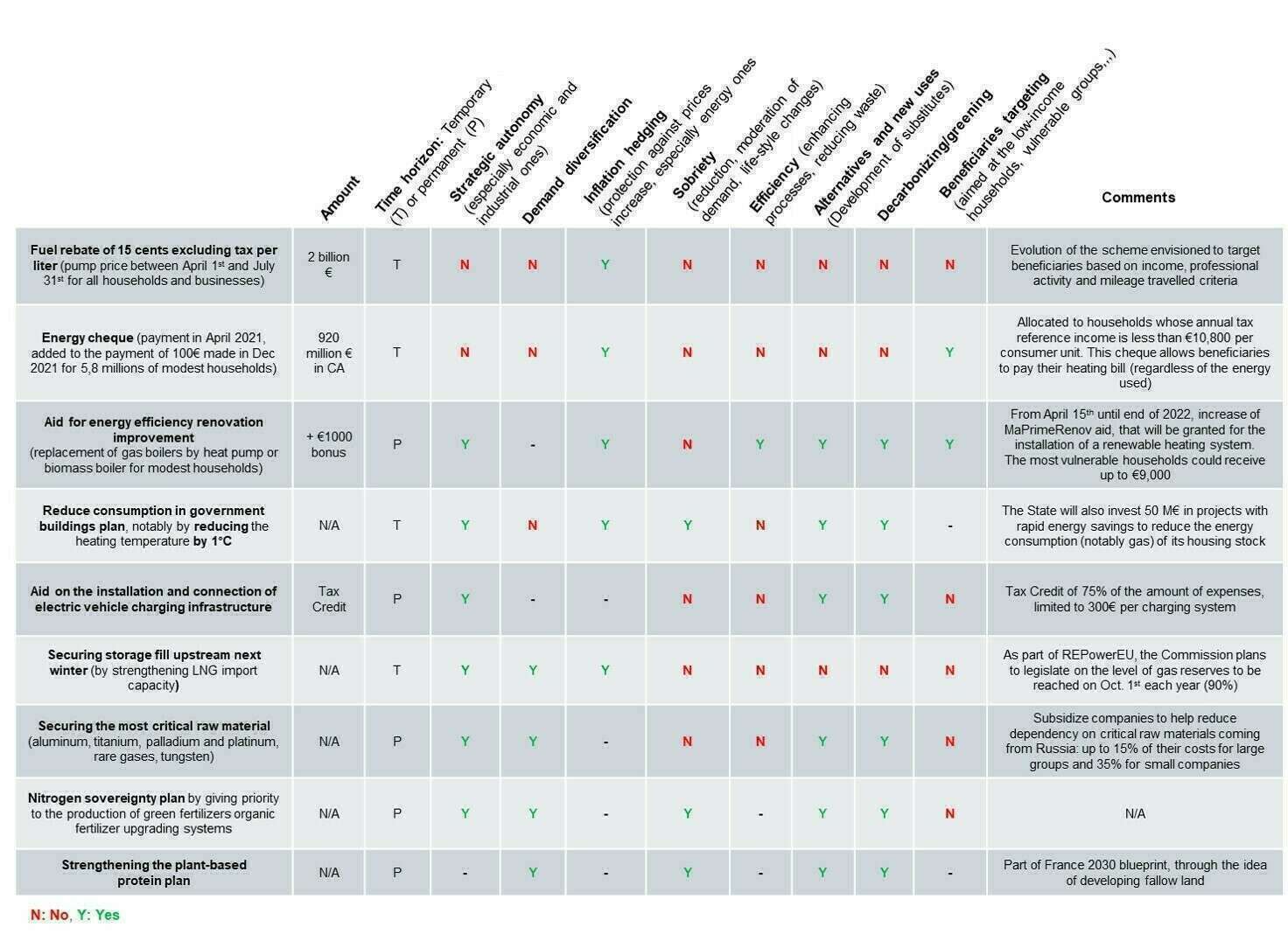

France’s resilience blueprint

On March 16th, the French government released an “Economic and Social Resilience Blueprint” [6]. We analyzed some of the measures through several criteria that we consider as highly critical and likely to become the “lenses” of ESG analysis, enriching the saliency of co-benefits.

Co-benefit trackers

Source: Authors (Natixis GSH)

Source: Authors (Natixis GSH)

Russia is sowing the seeds of distress around food security

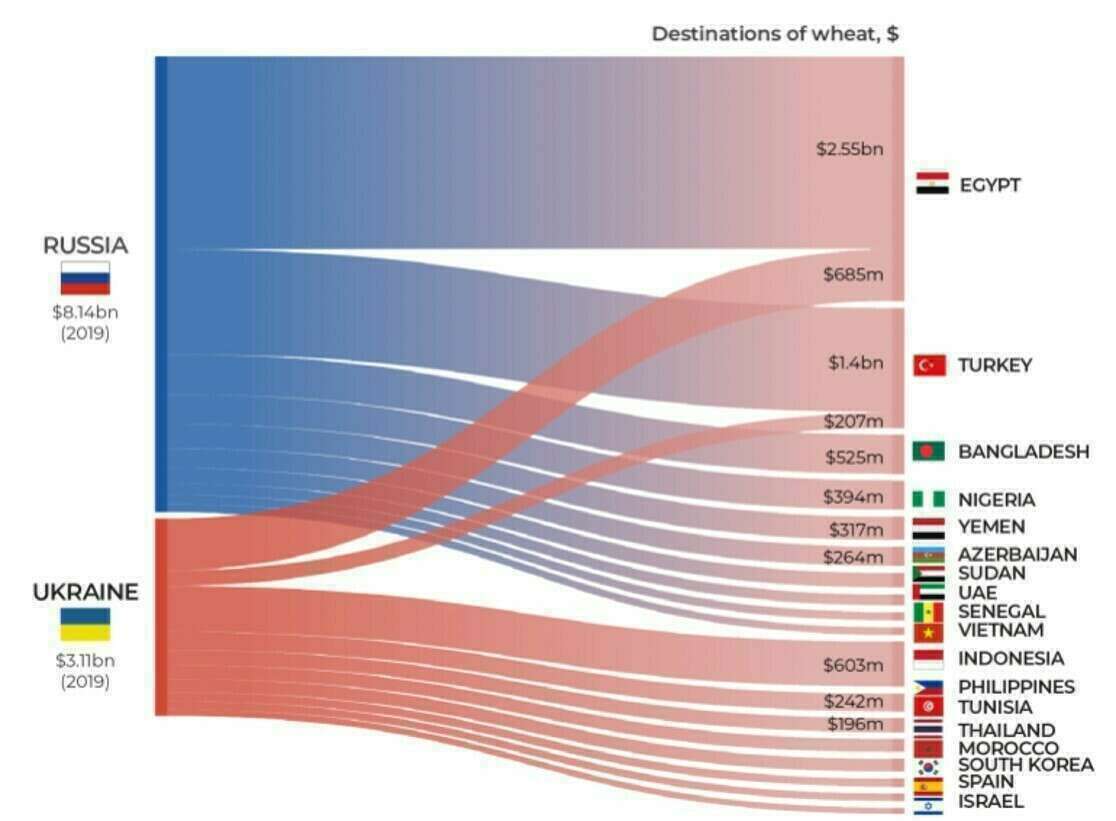

Energy is not the sole dependency the world has on Russia. Large groups of countries are now facing hunger geopolitics as together Ukraine (10%) and Russia (18%) supplied the world with 28% of wheat exports in 2021 [7]. Russia is blocking all Ukrainian Black Sea harbors and the country’s wheat exports, leading to a surge in wheat prices.

Wheat exports from Russia and Ukraine

Source: Middle East faces severe wheat crisis over war in Ukraine, Deutsche Welle, March 2022

Russia, Ukraine: a quarter of global wheat supply in 2019

Source: ALJAZEERA on OEC data from 2019, February 2022

Contrary to energy, Europe is not directly depending on Russian and Ukrainian wheat exports but could help in handling the looming food crisis. One remembers that wheat and bread skyrocketing prices fed social unrest in Egypt and Tunisia in 2011 and led to Arab Spring protests. These two countries are the most depending on Russian and Ukrainian wheat per capita (see figure 2). The subsequent social turmoil contributed to war outbreak in Libya and Syria. The EU could decide to increase its efforts on food systems to partly cushion the effects of war.

As part of its Green Deal, the EU designed its Farm to Fork Strategy in 2019. On top of sustainability, the strategy aims at increasing food-systems security and resilience not only in times of crisis (sanitary, climate, political, economic).

On the supply side, European farmers apprehend fertilizer shortages because of exports restrictions imposed by Russia (top exporter of nitrogen fertilizers and the second leading supplier of both potassic and phosphorous Fertilizers in 2021 [7]), China (the largest phosphate producer) and Ukraine. The European Union pushes to reduce the use of fossil-fuel derived nitrogen fertilizers and pesticides and compensate with alternative agricultural practices such as crop rotation or mechanical weeding. As part of Farm to Fork, the EU intends to create incentivizing mechanisms in its Common Agricultural policy and enhance provisions for integrated pest management.

Among measures put forward on the demand side, the EU plan recalls that a change in diets is crucial for various reasons, mainly health and environmental ones. Indeed, reducing animal-based foods could add up to 49% to the global food supply without expanding croplands [8]. Competition for crops & land use must be reconsidered in the current crisis. Indeed, less meat consumption would allow for a reduction of crops used for livestock feeding and incidentally limit prices increase and soften shortages for direct human intake of grains.

In particular, the impacts of animal products can markedly exceed those of vegetable substitutes, to such a degree that meat, aquaculture, eggs, and dairy use represent ~ 83 % of the world’s farmland and contribute 56 to 58 % of food’s different emissions, despite providing only 37 % of our protein and 18 % of our calories [9].

Such efforts would help in safeguarding peace as Mediterranean basin countries are at risk of food riots. Egypt (which imported almost 70% of wheat from Russia and 10% from Ukraine in 2021), Tunisia, Lebanon are highly dependent on Ukrainian and Russian wheat and the Sahel region is already facing major levels of food insecurity caused by long-lasting droughts. Such detrimental effects on agriculture and harvests have been documented once again by the IPCC in its AR6 Report on adaptation and linked to climate change.

PART II: Taxonomy criteria’s Achilles heel unearthed by the War in Ukraine

In this backdrop of events and decisions, the European Taxonomy’s recent edits for gas and nuclear power need to be put in perspective and questioned.

In particular, two cornerstone notions of the latest version of the green classification are being challenged:

- Gas criteria ignoring indirect emissions in face of LNG increasing importance and;

- The scope of DNSH and Social Minimum Safeguards assessments (how their respect should cascade along the value chain, including in countries supplying raw materials, see our article this month on the Social Taxonomy and scope of assessment of social minimum safeguards).

Back on the Delegated Act on gas and nuclear activities

The European Commission presented the criteria for the inclusion of certain gas and nuclear activities in the European Green Taxonomy on February 2nd [10]. It followed a first draft leakage on December 31, 2021 [11] that we extensively commented last January 2022 (see our article “Nuclear & Gas in the EU Taxonomy: integrity safeguarded despite postures and outrages”). It already seems to be another era, but at the time of the complementary Delegated Act release, the geopolitical aspects of gas and supply security were secondary in the discussion.

In light of the war in Ukraine, the terms of an already hard-to-find consensus must be revamped. Inclusion in the Taxonomy uncovers a bitter truth. At first controversial for being a fossil fuel in a “Green Taxonomy”, such inclusion became a sovereignty issue.

First of all, and once again, eligibility and alignment must not be mistaken. Eligibility involves featuring in the Taxonomy, while alignment is a whole other kettle of fish. It requires meeting a defined set of criteria to be deemed as “sustainable” in the hope of attracting additional capital and benefitting favorable funding terms or various support measures.

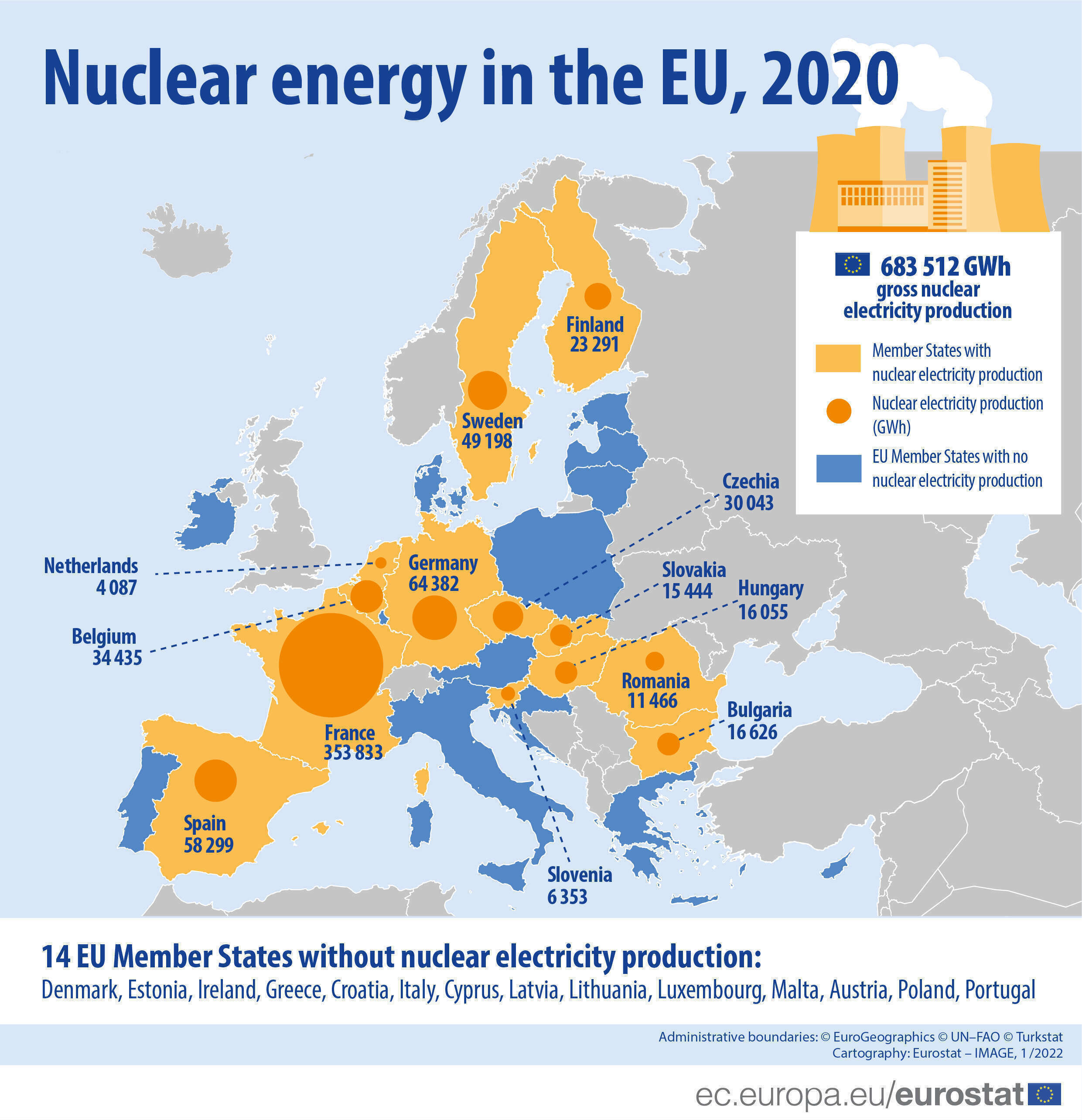

Several Member States relentlessly maneuvered for acknowledging gas and nuclear power as steppingstones on the path to carbon neutrality. One must bear in mind that nuclear is the #1 source of electricity generation in the EU, providing 25% of the electricity generated in 2020 [12]. Gas is the 2nd largest source of electricity with 20% of the electricity generated in 2020 [13].

This lobbying effort from Member States intervened in a context of rising inflation, notably fueled by energy price surges, and heightened risk of fuel poverty for lower-income households.

A “transitional” role

Brussels gave in on gas without writing a blank check: its tolerance is temporary, running until 2030 for gas, 2040 for the extension of existing nuclear plants and 2045 for the construction of new ones. Initially proposed criteria have been slightly amended and even weakened in the case of gas, sidestepping most of reactions to the December proposal.

However, before the outbreak of the war in Ukraine, we thought that the European Parliament or the Council were unlikely to veto the Delegated Act. A reverse qualified majority (20 Member States) in Council or a majority in Parliament are required to blockade the text. Nonetheless, more than 7 Member States support the Delegated Act and according to the press, the EPP, the majority party in Parliament, would support it. A total of 102 EU MPs has called on the European Commission to reconsider its proposal to include gas in the taxonomy arguing that Russia’s invasion of Ukraine has rendered the proposal obsolete [14].

Meanwhile, it is unclear whether the appeal to the CJEU of Luxembourg and Austria may result in censorship or withdrawal of the text, on the basis that these matters are too salient to be dealt with only through Delegated Acts (whose rank in the hierarchy of European norms is deemed too low).

More stringent requirements for nuclear

Scientists are unanimous in their findings regarding nuclear contribution to the decarbonization of economies (IPCC, IEA [15]). The crucial challenge is ensuring that other environmental objectives are not significantly harmed (“DNSH criteria”) – such as preventing pollution and protecting biodiversity. With this in mind, the Complementary Delegated Act encompasses several demanding requirements, including detailed plans to have in operation, by 2050, a specific disposal facility for highly radioactive waste.

The Delegated Act goes beyond current safety standards – already bolstered in the wake of Fukushima – to require the use of secure Accident Tolerant Fuels (ATF) from 2025, which constitutes an additional requirement to the first leaked version of the DA. ATFs are a technological innovation offering higher safety in normal operation, in transient conditions and in accident scenarios (loss of active cooling in a reactor, for example). On top of safety improvements, ATFs also make power plants more competitive, as fuels last longer, allowing a reduction up to 30% of fuel used. They also shorten maintenance time and costs over the asset lifetime while increasing performance for the same amount of fuel (higher burnup).

Overall, the criteria does not seem to be a low hanging criteria as the technology is relatively new and industrials are planning to commercialize it no earlier than between 2025 and 2030.

European States [16] relying on nuclear energy could benefit from the inclusion of nuclear in the Taxonomy:

- Incumbent French President Macron announced, on February 11th as part of his reelection program, the construction of 6 reactors (EPR of 2nd generation) in the short term, and potentially 8 more in the medium term [17]. Furthermore, the development of the new Small Modular Reactors (SMR) is a priority of the “France 2030” investment plan [18];

- Poland plans to deploy up to six reactors by 2040, the first one should be put into operation in 2033;

- Finland just connected a new reactor to the national grid (Olkiluoto 3);

- Czech Republic decided to build a new reactor in 2019;

- Netherlands to launch the construction of two new reactors by 2025;

- Slovakia will start operating a reactor in 2022 followed by another one in 2023;

- Belgium decided to extend its two largest nuclear reactors lifespan (Doel 4 and Tihange 3 with net capacity of 1038 MWe each) beyond their original shutdown scheduled in 2025.

Nuclear Safety in times of War

Against this backdrop, the Russian attacks on Chernobyl and on administrative buildings of Ukraine’s largest nuclear power plant triggered fear of nuclear accidents. It summons further studies on nuclear power plant security as facilities might be transformed into a ticking bomb in host countries.

The situation echoes the demands from the Sustainable Finance Platform for more precisions regarding high risk, low probability events (such as terrorist attacks or wars) that could put nuclear assets at risks. Should the complementary DA on nuclear be revised, it should address in a more explicit fashion this key angle to nuclear security, a crucial element of the risk aversion towards the technology.

A 2018 French parliamentary report on nuclear safety concluded that nuclear reactors and waste disposal facilities are not vulnerable to any type of terrestrial weapons. Nonetheless, the parliamentary commission could not verify dedicated studies as they were “classified”. Nevertheless, infrastructures might be vulnerable to plane crashes and explosives. Safety measures do exist to palliate most infrastructures vulnerabilities as a secondary level of safety behind intrinsic infrastructure safety (such as a secondary cooling circuits). The probability for a large plane to hit the most sensitive part of the asset was deemed extremely low in the report. Infrastructures built in France after 2001 incorporate a “plane” type hull to protect sensitive areas. Another way to mitigate related vulnerabilities is to decrease the storage capacity of highly radioactive waste in dedicated pools. Deep geological repositories may therefore be part of the answer.

Gas before the invasion: no one was satisfied

The Complementary Delegated Act exempts gas from complying with the technology agnostic 100 gCO2e/kWh threshold until 2030. Introducing a transitory and laxer threshold of 270 gCO2e/kWh. Yet, it is at this stage unachievable for cutting edge power plants without carbon capture. An alternative criterion – annual GHG emissions not exceeding a yearly average of 550kgCO2e/kW capacity– allows for less efficient plants to be aligned while capping their utilization rates according to their carbon intensity. Furthermore, the average spans over a permissive 20-year time-period.

Meanwhile, other cumulative criteria are required, such as the prior replacement of backward coal-fired or gas-powered facilities, and the absence of renewable alternatives, although the terms are blurred. These plants will also have to ensure a 55% cut in emissions. Compared to the first version that leaked on December 31, 2021, this reduction is no longer expressed in intensity per kWh but rather in absolute terms across the new asset’s lifecycle (this applies only to the electricity generation from gaseous fuels). We believe such a change from intensity to absolute undermines the relevance and usability of this criterion.

Stranded asset risk made in EU

Furthermore, gas power plants will have to be fueled entirely by low-carbon gases by 2035 (100%). But the elimination of intermediate milestones in 2026 (30%) and 2030 (55%) is undermining the key notion of progressivity and pathways’ credibility. Meanwhile, shortages of low-carbon gases or surging prices would require curtailing power plant utilization rate, unless operators decide to infringe the Taxonomy criteria. Doing so could trigger potential claims from misled investors. Ironically, the EU could create a textbook case of stranded assets, denting facilities’ value by failed attempts to comply with its own Taxonomy.

Legal uncertainty

Critics are up in arms, while companies directly or indirectly involved in gas activities will have to deal with legal uncertainty. One foresees legal disputes, particularly involving auditors who have to issue an opinion on compliance with equivocal criteria (forward-looking low-carbon gases integration, load factor limitations, irreplaceability by renewable energies), against a backdrop of mounting climate litigation and a – much warranted – strengthened fight against greenwashing (see our article this month on ESMA’s sustainable finance roadmap) [19].

This will probably discourage companies from embarking on Taxonomy earmarking processes for their gas related investments. The hypothetical benefits from a greenium could well be measly considering operational constraints imposed by the taxonomy criteria and particularly the sheer uncertainty surrounding their verification.

Uncertainty surrounding forward looking alignment for gas (meeting low-carbon gases requirements by 2035) makes it ill-suited to green bonds or loans. However, transition bonds or sustainability-linked bonds are a worth-considering option, with financial penalties or premiums linked to the accomplishment of targets set out at the time of issuance. One could imagine a coupon step up when the gas asset financed fails to meet the Taxonomy performance thresholds.

Criteria obsolescence due to the war in Ukraine and LNG extended role

Taxonomy Gas criteria’s Achilles heel is unearthed by the War in Ukraine. The argument made by the Platform on Sustainable Finance [20] on disregarding indirect emissions for gas criteria appears truer than ever. Integrating lifecycle considerations in defining substantial contribution for power generation from gas is necessary. This is truer if the gas is supplied by the sea and undergoes liquefaction and gasification processes. The latter are extremely carbon intensive (gas combustion to power refrigeration compressors and electrical generators, fired heaters, flares, incinerators, carbon dioxide venting, fugitive losses). Significant energy is lost in conversion.

According to a study from the Oil and Gas Authority (2020) on British LNG imports from Qatar compared to gas extracted in the UK Continental Shelf (UKCS): the process of liquefaction, combined with the emissions produced by the transportation and regasification of the LNG is responsible for more than doubling gas’ cradle-to-gate carbon intensity (from 22 kgCO2e/boe for UKCS to 59 kgCO2e/boe for LNG imported from Qatar).

{kind=link}

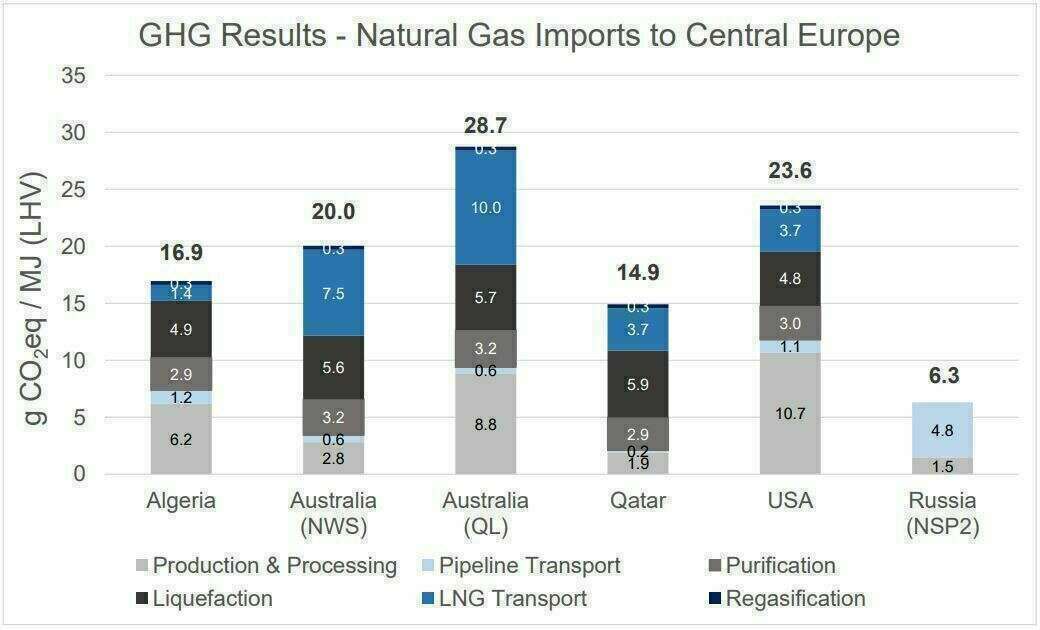

A 2017 report by a Stuttgart university backed LCA consultancy (Thinkstep) compared the GHG intensity of gas transport in the case of Nord Stream 2 construction against LNG imports from the Algeria, Qatar, the United States or Australia. It found that LNG import GHG results are from 2.4 (Qatar) to 4.6 (Australia) times higher than GHG results for the pipeline import from Russia via Nord Stream 2 (NSP2).

Source: GHG intensity of natural gas transport, Thinkstep, 2017

If climate mitigation is a crucial parameter, the Do No Significant Harm criteria are to be considered as well, especially for hydraulic fracturing techniques used in the extraction of shale gas in the US.

If uncertainty remains about fugitive emissions weight in lifecycle assessments, all things being equal, LNG seems to be more carbon intensive than gas transported by pipeline. With that in mind, the unchanged inclusion of gas without LNG safeguards in the Taxonomy would widen the gap between the political inclusion in the taxonomy and climate science.

Final words: the Taxonomy, the whole Taxonomy and nothing but it

The EU Taxonomy polarizes excessive expectations and fears. Many actors expect the entire world’s energy, technological, financial and political ills to be fixed with it. Amber, brown and even social aspects are mentioned (see our article on the social taxonomy) and these are not without justification. The risk is of an excess of inapplicable and counterproductive standards.

The European Taxonomy’s importance and influence could make it through the current turmoil, as it is by far the most sophisticated green finance classification in the world. However, it is now increasingly complex, fragmented and less consensual. European policymakers must take stock of the unprecedented geopolitical situation and adjust their proposal by including upstream emissions in defining substantial contribution for power generation from gas. It would dissipate bewilderment, underlining the benefit of the prompt action desperately needed to tackle the climate emergency.

To go further:

- European Commission, Complementary Climate Delegated Act on climate change mitigation and adaptation covering certain gas and nuclear activities, 2 February 2022, available here.

- EU Platform on Sustainable Finance, Response to the Complementary Delegated Act, 21st January 2022, available here.

- Green & Sustainable Hub, “Vade mecum to digest the 414-page Report from the TEG”, July 2019, available here.

- Green & Sustainable Hub, “EU Taxonomy for sustainable activities”, September 2020, available here.

- Green & Sustainable Hub, “Green-washing allegations are jolting the financial industry: heightened needs for cautiousness, integrity and guidance”, 30 September 2021, available here.

- Green & Sustainable Hub, “Nuclear & Gas in the EU Taxonomy: integrity safeguarded despite postures and outrages”, 20th January 2022, available here.

- Green & Sustainable Hub, ESMA article, 28th February, available here.

References

[1] Informal meeting of the Heads of State or Government, “Versailles Declaration”, 10 and 11 March 2022, available here.

[2] Belgium decided to extent by 10 years the lifespan of two reactors which were meant to be shut down by 2025 (Doel 4 and Tihange 3 with net capacity of 1038 MWe each), South Korea could extend and build new reactors following Wednesday March 9th presidential election.

[3] The German Chancellor, Olaf Scholz, revealed plans to build two LNG terminals (“decision to rapidly build two LNG terminals in Brunsbüttel and Wilhelmshaven”). See his major speech on February 27, 2022, available here.

[4] North Korea exception is irrelevant as it does not stand the comparison because of its economic size and lack of ties with the rest of the World.

[5] The Italian Foreign Minister Luigi Di Maio flew to Algeria and Qatar in an attempt to cut more than half of its Russian gas imports which represent 40% of gas imported in the country.

[6] Plan de résilience économique et sociale (available only in French), March 16, 2022, available here.

[7] The importance of Ukraine and the Russian Federation for global agricultural markets and the risks associated with the current conflict, 2022, FAO

[8] Diet change—a solution to reduce water use? Jalava et al, 2014.

[9] Reducing food’s environmental impacts through producers and consumers, Poore et al, Science, 2018

[10] European Commission, Complementary Climate Delegated Act on climate change mitigation and adaptation covering certain gas and nuclear activities, 2 February 2022, available here.

[11] European Commission, Draft Commission Delegated Regulation amending Delegated Regulation (EU) 2021/2139 and Delegated Regulation (EU) 2021/2178, 31 December 2021, available here.

[12] Eurostat, January 2022, available here.

[13] Eurostat, January 2022, available here.

[14] Euractiv (March 2022), “Lawmakers urge Brussels to ditch green label for gas in EU taxonomy”, available here. The letter was signed by 102 lawmakers coming from the European Parliament’s five main political groups: the centre-right European People’s Party (EPP), the Socialists and Democrats (S&D), the centrist Renew Europe, the Greens, and the Left.

[15] Intergovernmental Panel on Climate Change (IPCC), Global warming of 1.5°C, October 2018, [Chapter 2-Section 2.4.2.1, page 131], available here.

International Energy Agency (IEA), Nuclear Power in a Clean Energy System, May 2019, available here.

[16] In the European Union, 13 countries have operational nuclear power reactors (France, Spain, Belgium, Germany, Sweden, Czech Republic, Finland, Hungry, Slovakia, Bulgaria, Romania, Slovenia und the Netherlands), International Atomic Energy Agency (IAEA), “Nuclear Power Reactors in the World”, n°2, 2021 Edition, July 2021, p. 7-8.

[17] Ministère de la Transition écologique, press release, 18 February 2022, available here.

[18] Emmanuel Macron, Speech for the presentation of the France 2030 investment plan, 12 October 2021, available here.

[19] Green & Sustainable Hub, “Green-washing allegations are jolting the financial industry: heightened needs for cautiousness, integrity and guidance”, 30 September 2021, available here.

[20] Platform on Sustainable Finance, “Response to the consultations on the taxonomy draft complementary Delegated Act”, 24 January 2022, available here.