Taxonomy criteria for non-climate objectives: a welcomed hard work with some inconsistencies

12 - minute read

On March 30th, 2022, the Platform on Sustainable Finance (hereafter PSF or the Platform) published its final report containing technical screening criteria (TSC) for the four remaining environmental objectives of the Taxonomy Regulation.

As a reminder, in the European Environmental Taxonomy, six environmental objectives are defined:

- Objective 1 – Climate change mitigation

- Objective 2 – Climate change adaptation

- Objective 3 – Sustainable use and protection of water and marine resources

- Objective 4 – Transition to a circular economy

- Objective 5 – Pollution prevention and control

- Objective 6 – Protection and restoration of biodiversity and ecosystems

The Platform here provides the rationale and the methodology used to define the non-climate Technical Screening Criteria (part A [1]) as well as a batch of 51 economic activities assessed (part B [2]). Animal production or crop production and fishing regarding protection and restoration of biodiversity are included, while they were not in the Climate Delegated Act.

The Platform also took advantage of this Report to develop criteria for 14 new economic activities on the climate mitigation and adaptation objectives. It is worth noting the inclusion of the aerian sector assessed against climate change mitigation.

Natixis welcomes the assessment of activities present in the Climate Delegated Act [3] against these new objectives. Assiduous work has been revealed with 10 economic activities that have now TSC provided for more than two environmental objectives.

Nevertheless, the high technicity level of some TSC and the hurdles existing when articulating some activities already covered in the Climate Delegated Acts (DA) (diverging scope of activity, environmental contribution being based on conflicting references) display consistency gaps. Such discrepancies will bring difficulties for company to report.

Moreover, considering substantial contribution, we distinguished four types of alignment criteria based on the various metrics found in the PSF’s report: abidance by Standards, labels and regulations; technology eligibility; intensity-level performance; and relative improvement performance requirements. Such diversity in substantial contribution could lead to inconsistencies when monitoring transition plan and evaluating the share of economic activities aligned with the Taxonomy (and to include various performance levels, as suggested in the extended taxonomy report, see our editorial).

Additional recommendations on TSC by the PSF for other economic activities were expected in May 2022 and September 2022. Notably for activities already covered in the first DA and that will be assessed on the remaining four objectives. One can expect progress on forestry, electricity generation and power from cogeneration of heat/cool and power. In parallel, other activities and TSCs have been challenging to assess because of the difficutiles to demonstrate a substantial contribution. One can think of land-based mining and quarrying, other than, lignite, crude oil/petroleum or natural.

Following the Platform’s recommendations, the European Commission should adopt several Delegated Acts to finalize the Taxonomy Regulation scheduled to be fully in force by the 1st of January 2023.

******

TABLE OF CONTENTS

I - Defining the four remaining non-climate objectives

a) Objective #3 – The sustainable use and protection of water and marine resources

b) Objective #4 – Transition to a circular economy

c) Objective #5 – Pollution prevention and control

d) Objective #6 – Protection and restoration of biodiversity and ecosystem (B&E)

II - Rationale and methodology to define Technical Screening Criteria for the Non-Climate objectives

III - Articulation between economic activities in Taxonomy DA and in TSC Report from the Platform

IV - Glimpse at the different categories of metrics and thresholds for substantial contribution criteria

V - Hurdles when assessing substantial contribution alignment

a) Concerns on technical level and application raised questions on substancial contribution's feasibility

b) Diverging definitions, scope and reference

VI - What has the PSF left for us

VII - Conclusion

******

I - Defining the four new non-climate objectives, rationale, and methodology

The rationale behind the definition of the non-climate objectives, proposed by the PSF, is linked to environmental strategies and

policies in place for the respective objective. Some examples are stated on the table below.

Table 1: Environmental strategies and policies used as references for the definition of the objectives

|

Objective |

Link to environmental strategies and policies (not exhaustive list) |

|

Objective 3: The sustainable use and protection of water and marine resources |

|

|

Objective 4: The transition to a circular economy |

|

|

Objective 5: Pollution prevention and control |

|

|

Objective 6: The protection and restoration of biodiversity and ecosystems |

|

Source: Authors (Natixis GSH), based on the Platform’s report

The Platform suggests an articulation between the non-climate objectives and their impact on each other as described in the figure below:

Figure 1: Interrelations among the different non climate objectives of the Taxonomy

Source: Authors (Natixis GSH), based on the Platform’s report

a) Objective #3 – The sustainable use and protection of water and marine resources

The third objective is defined as “ensuring at least good status [4] for all water bodies by 2027, and good environmental status for marine waters as soon as possible and to prevent the deterioration of bodies of water that already have good status or marine waters that are already in good environmental status.”

The first deadline for achieving at least good status for all water bodies in Europe set out in the Water Framework Directive (WFD) [5] was 2015. The recent controversy about the missing opportunity to ensure that the so-called EU Marine “Protected” Areas are truly protected by banning destructive fishing methods such as bottom trawling reminds us that the notion of what is considered as “good status” for water body is complexed and blurred.

b) Objective #4 – Transition to a circular economy

The fourth objective is defined, by the Platform, as the following “by 2030 economic growth is decoupled from extraction of non-renewable resources and depletion of the stock of renewable resources is reversed, and by 2050 economic activity is largely decoupled from resource extraction, through environmental design for a circular economy to eliminate waste and pollution, keep materials and products in use at their highest value, and to regenerate ecosystems”.

As of today, there is no quantitative overarching EU ambition level for the circular economy, the ambition builds on a range of published strategies and targets. In February 2020, the EU Parliament called for binding targets for 2030 to significantly reduce the EU material and consumption footprints and bring them within planetary boundaries by 2050. As of April 2022, a new planetary boundary has been transgressed, bringing to six (out of nine) the number of boundaries that have been trespassed (biosphere integrity, land-system change, novel entities, biogeochemical flows, climate change, and freshwater change) [6].

c) Objective #5 – Pollution prevention and control

The fifth objective is a “zero-pollution vision for 2050 for air, water and soil pollution to be reduced to levels no longer considered harmful to health and natural ecosystems, that respect the boundaries with which our planet can cope, thereby creating a toxic-free environment. This 2050 vision target is seen in the context of the UN 2030 agenda for Sustainable Development and has a series of associated targets for 2030 to help achieve the overall 2050 goal.”

The European Commission adopted the ambitious EU Action Plan “Towards a Zero Pollution for Air, Water and Soil” (ZPAP) in April 2021 to reach this goal but the recent evolution of the geopolitical situation in Europe and the absolute necessity of securing the EU supply of metals required to transition will probably add uncertainty to this Plan (see our article “The clash between sovereignty and sustainability”).

d) Objective #6 – Protection and restoration of biodiversity and ecosystem (B&E)

The last objective is “to ensure that by 2050 all of the world’s ecosystems and their services are restored to a good ecological condition, resilient, and adequately protected. The objectives of the EU Biodiversity Strategy will be achieved at latest by 2030. From today the world’s biodiversity needs to be put on the path to recovery and no deterioration in conservation trends and status of all protected habitats and species by 2030 will be ensured.”

To inform the development of the technical criteria for biodiversity, ambition levels will need to be defined by ecosystem, restoration needs to be defined against a baseline and “sufficient and adequate” levels of biodiversity protection and restoration need to be defined in terms of both quantity and quality.

|

The special case of offsetting According to the PSF there are four reasons why the use of offsetting is inappropriate to deliver substantial contribution to an environmental objective in the Taxonomy.

Excluding offsetting from biodiversity substantial contribution is important to avoid important risk of greenwashing (see our dedicated articles [1] & [2]) while companies impacted by the NFDR and the future CSRD [7] will report information on the way corporates operate and manage social and environmental challenges. The expected adoption of the latter is October 2022. This does not alter the fact that meaningful criteria for carbon offset exist (see our report “Brown industries – The transition tightrope”). |

II - Rationale and methodology to define Technical Screening Criteria for the Non-Climate objectives

The PSF has been mandated to establish technical screening criteria (TSC) for determining the conditions under which a specific economic activity can be qualify as contributing substantially to one or more of the four non-climatic environmental objectives.

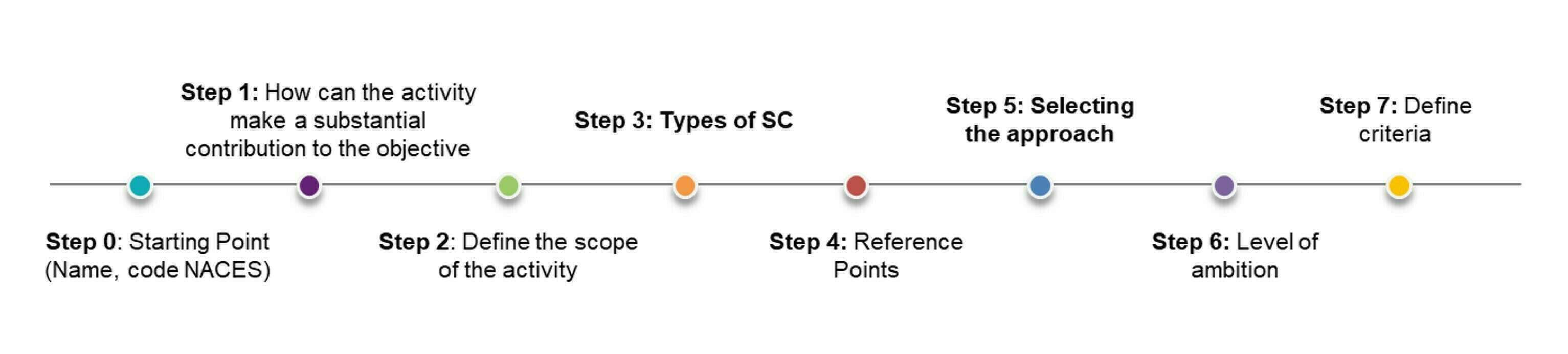

The methodology used by the PSF to develop technical screening criteria has been implemented accordingly to the Joint Research Center (JRC) report “Development of the EU Sustainable Finance Taxonomy – A framework for defining substantial contribution for environmental objective 3-6” [8].The steps for establishing technical screening criteria defined in the methodology are representing on the figure below.

Figure 2: 7 steps to establish TSC by the Joint Research Center (JRC)

Source: Authors (Natixis GSH), based on the JRC’s report

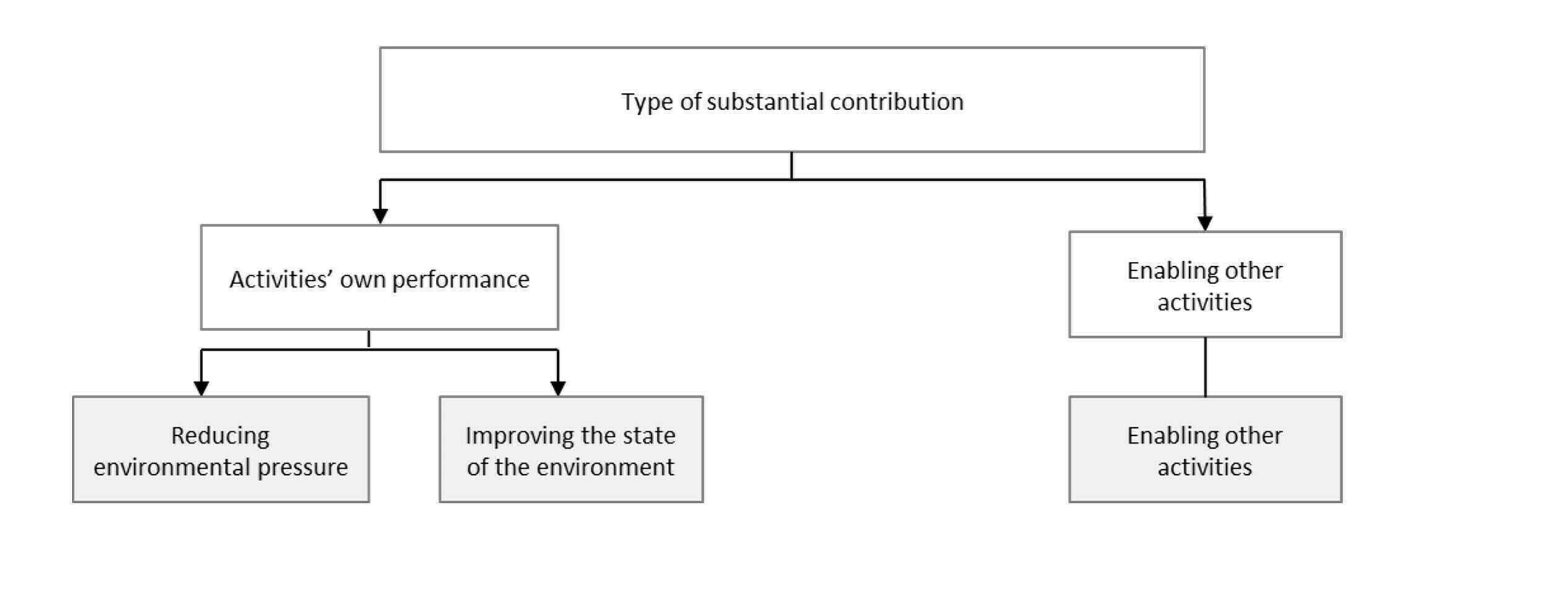

The report defines three main ways for an activity to make a substantial contribution to an environmental objective. The first two types of SC are related to the activity’s own performance while the third one concerns enabling other activities (see figure 2) [9].

Figure 3: 3 main ways considered to make a substantial contribution to an environmental objective

Source: Authors (Natixis GSH), based on the Platform’s report

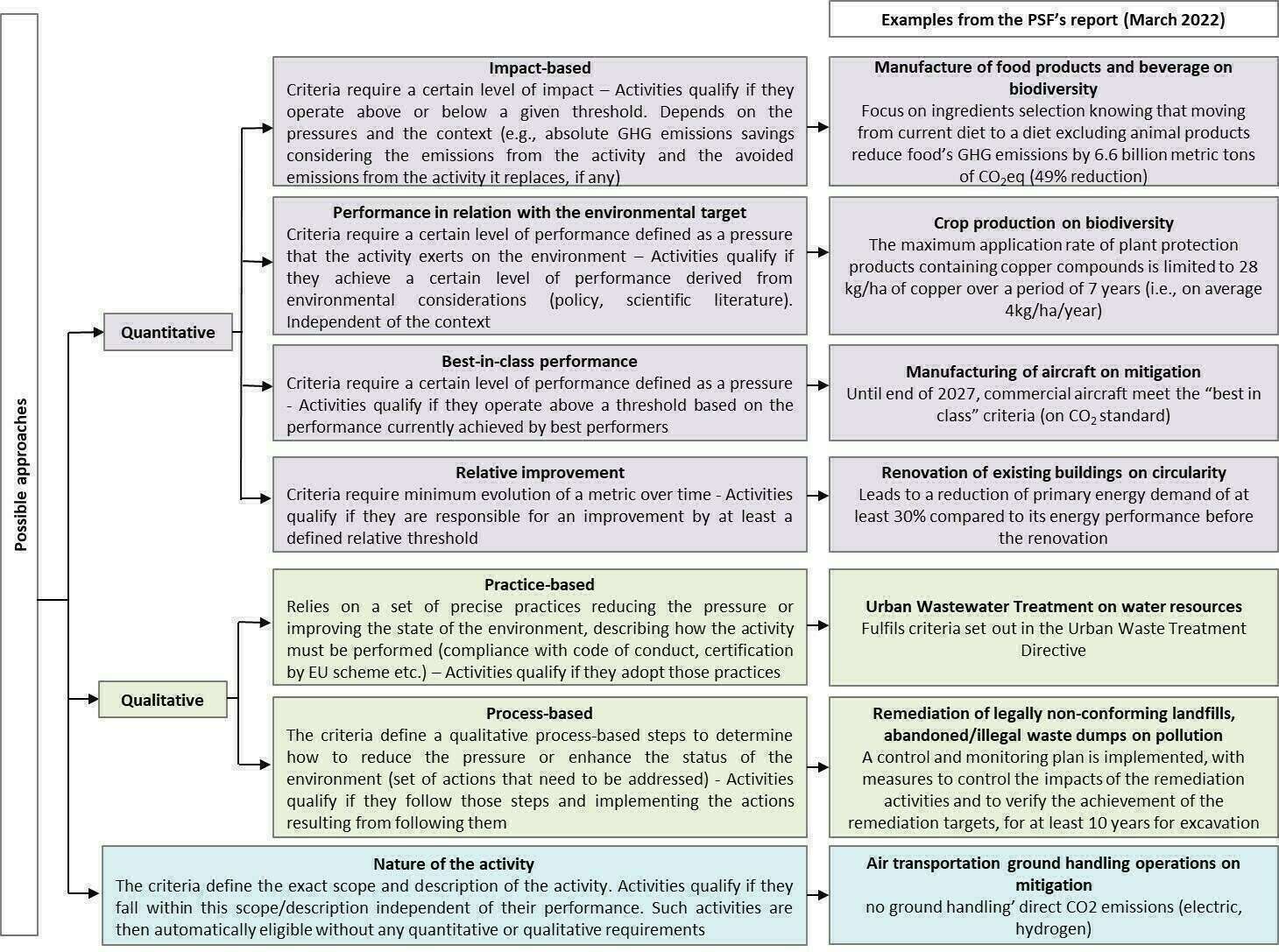

To set criteria, the JRC defined seven generic approaches. Potential approaches cover the way in which the environmental performance of an activity is measured (quantitative, qualitative, units used) and how the required level of environmental performance can be defined (implementation of certain practices, baselines, or comparison group).

Figure 4: Types of possible approaches

Source: Authors (Natixis GSH), based on the JRC’s and PSF's report

In order to ensure that the approach used for defining the technical screening criteria is suitable, it must meet four broad requirements:

- Policy coherence: where appropriate, the approach makes it possible to build on EU legislation, approaches, and policy goals;

- Environmental ambition and integrity: the approach makes it possible to follow scientific evidence and take into account life cycle considerations;

- Level playing field: the approach allows fair treatment of activities within the same sector;

- Usability of the criteria: the approach makes it possible to develop criteria that are of easy and unambiguous to implement and verify.

Nevertheless, while a quantitative approach is relevant with the assessment of criteria through measurable metrics, one can wonder about the robustness of a qualitative approach since it is relying on a subjective view (enhancing on how an activity will follow practices to reduce pressures rather than the actual performance of the activity). Regarding “the nature of the activity” approach, the latter does not seem to take DNSH into account. One can think of a wind farm project for which trees would be cut down to install it.

The level of ambition determines the performance required by technical screening criteria for activities making a substantial contribution to an environmental objective. The PSF provides guidance for setting a headline ambition level by being science-based, established on international agreements that EU supports and reflect EU’s response to international agreements or EU’s leadership on an objective.

III - Articulation between economic activities in Taxonomy Delegated Act and in TSC Report from the Platform

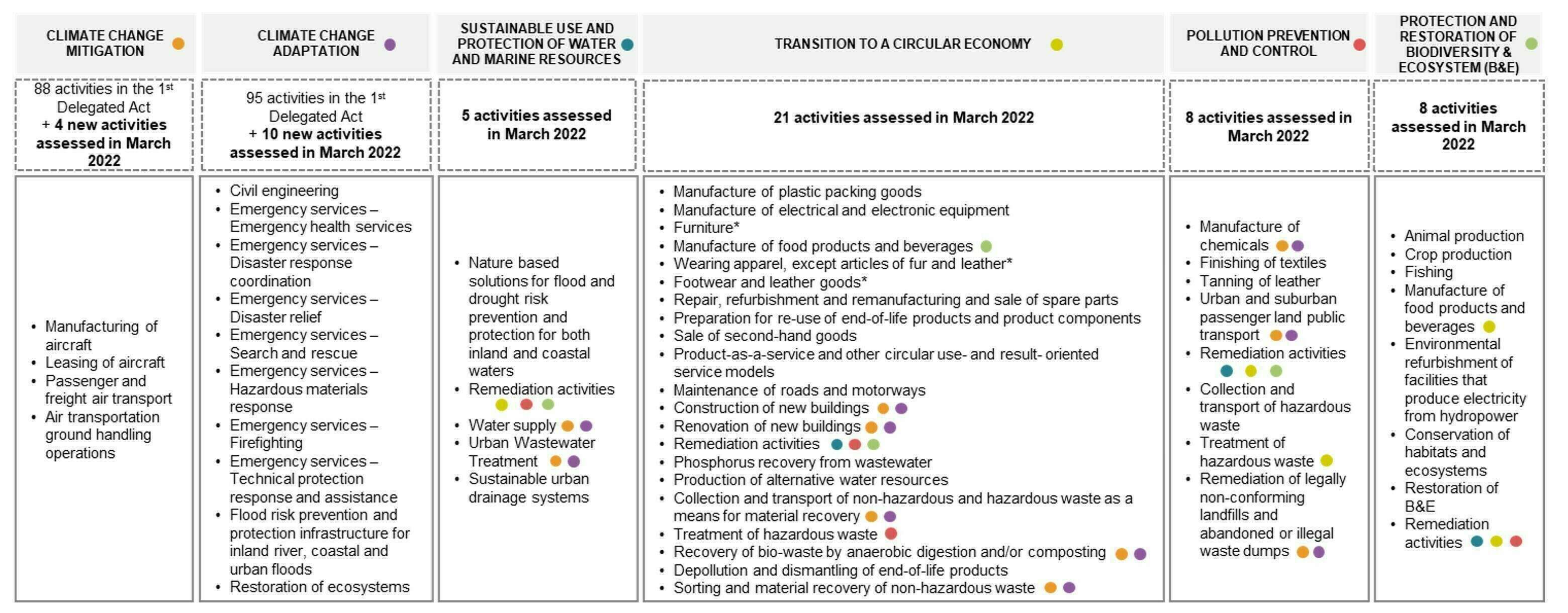

In its final report, the Platform assessed 37 economic activities against the non-climate objectives and 14 economic activities (see figure 2) against the existing climate objectives. Some activities are assessed against several objectives. One could notice that even after adding these activities we are still falling short to cover the 615 activities of the NACE classification. This will cause problems for companies requested to report their Taxonomy eligibility and alignment.

Figure 5: Overview of activities covered by the Platform in March 2022 [10]

Source: Authors (Natixis GSH), based on the Platform’s report

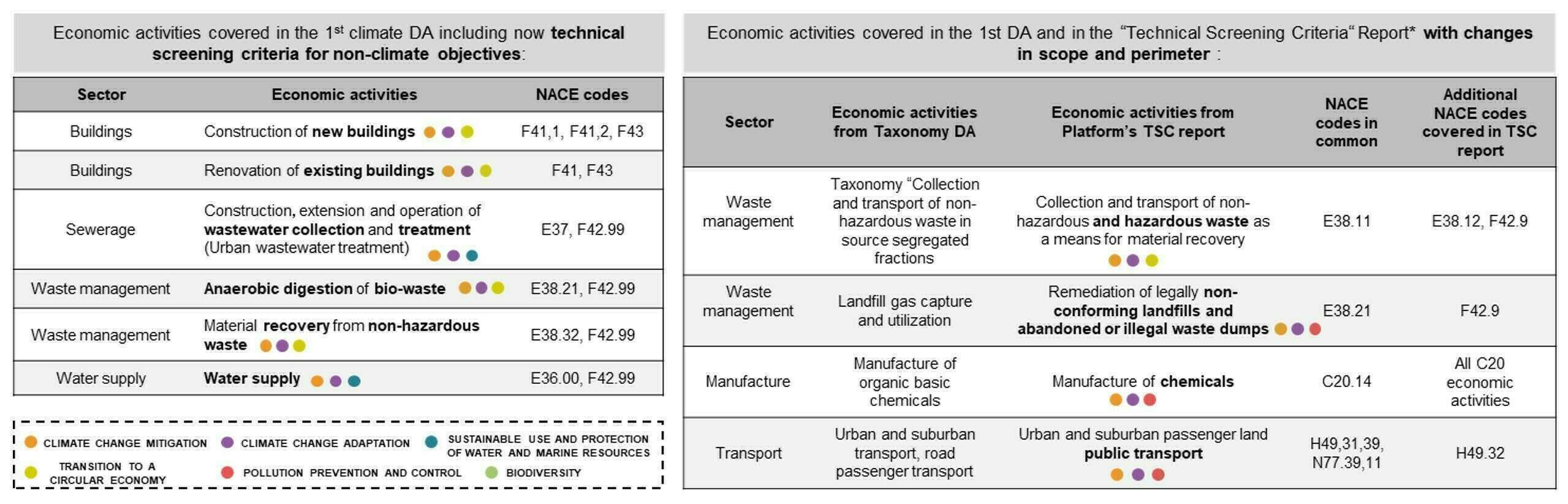

Besides being covered for the climate objectives in the first CDAs, 5 economic activities are assessed against transition to a circular economy objective, 2 activities against the protection of water and marine resources, and 3 activities against pollution prevention and control. More information on those activities is shown on the figure below.

Source: Authors (Natixis GSH)

Natixis welcomes the assessment of economic activities already included in the 1st DA against non-climate objective. Nevertheless, differences in activities’ scope and perimeter between both documents, such as differences in economic activities’ name and associated NACE codes, bring confusions.

Only 10 economic activities assessed in the 1st Climate Delegated Act (CDA) are now also assessed against a non-climate objective. One could have expected the Platform to assess economic activities already covered in the 1st CDA against non-climate objectives in order to monitor more precisely their transition (see our editorial on the Extended Taxonomy).

As shown on the right part of the figure above, 4 activities have undergone a change in their scope of appliance compared to the 1st DA. Such inconsistencies will increase difficulties for company to report. We strongly recommend harmonizing the economic activity description.

Some important economic activities are missing such as forestry, bioenergy, or mining, that are still under development by the Platform and should be added in an additional complementary Delegated Act planned to be delivered by the end of S1-2022.

IV - Glimpse at the different categories of metrics and thresholds for substantial contribution criteria

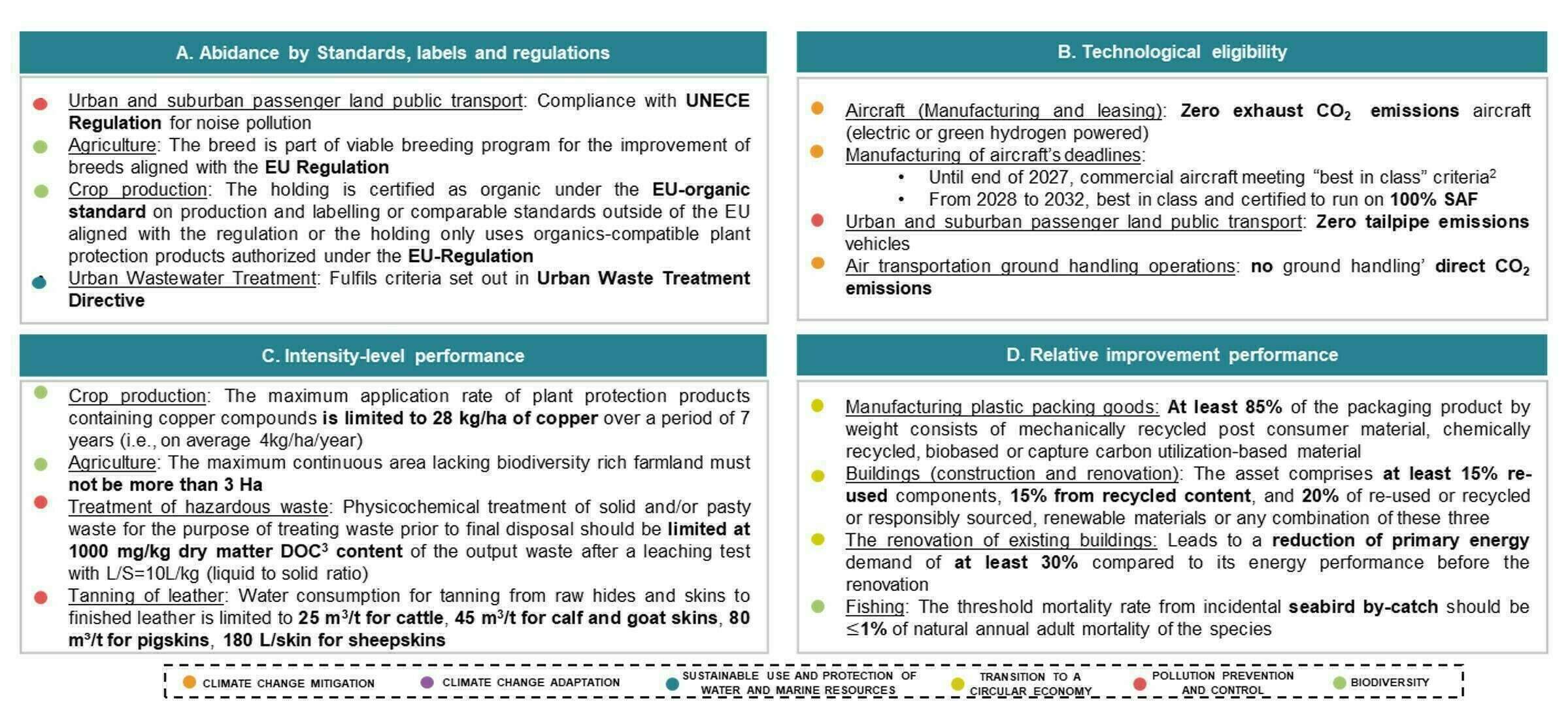

Through the TSC report published by the Platform, we identified four main types of alignment criteria based on the various metrics found:

- abidance by Standards, labels, and regulations: criteria based on compliance with regulations, labels, or standards in place

- technological eligibility: criteria that depends on the availability of technology

- intensity-level performance: criteria is limited by a quantitative threshold

- relative improvement performance: criteria that is conditional to a relative threshold

We listed some examples and the objective the activity is responding to respectively, on the figure below.

Figure 7: Examples of different type of alignment criteria based on different metrics found in the Platform's report

Source: Authors (Natixis GSH)

The lack of uniformity of substantial contribution criteria could lead to inconsistency to monitor transition plan and evaluate share of economic activities of a company really aligned with the Taxonomy.

V - Hurdles when assessing substantial contribution alignment

Example:

Activity Description: Manufacture of chemicals

Substantial contribution to pollution prevention and control

C. The produced substance is used as a replacement. Therefore, the operator has to demonstrate that an equivalent substance with comparable functionality, fulfilling any hazardous properties either included in the list of Substances of Concern or Acute toxicity for health (Cat. 1-3), Severe eye damage (Cat. 1) and Skin corrosion (Cat. 1), and Acute toxicity for environment, Aquatic Acute Cat. 1 (H400), is currently produced

One can wonder the relevance of a product used as a substitution to demonstrate the substantial contribution of a chemical product. Indeed, one can think of a product that doesn’t have an “equivalent substance with comparable functionality fulfilling hazardous properties”, but that could still contribute to the pollution prevention and control objective. Furthermore, one can think of the impact such criteria might have regarding an Extended Taxonomy [11], notably on how the activity should be classified. For example, if the activity complies with all of the very strict criteria but falls short of replacement criteria, then how should the activity be qualified? Could it be considered in the amber category? Or should it be referred to the red category?

a) Concerns on technical level and application raised questions on SC’s feasibility

The level of technicality for some SC criteria is so high that it seems almost impossible to monitor closely.

Example:

Activity Description: Treatment of hazardous waste

Substantial contribution to pollution prevention and control

2. Applicable to the physico-chemical treatment of solid and/or pasty waste (complementary to BAT 40 and 41 of WT BREF): Any physico-chemical treatment of solid and/or pasty waste for the purpose of treating waste prior to final disposal (e.g., in hazardous waste landfills) should be designed in order to:

• limit at 6% Total Organic Carbon (TOC) maximum in each single input waste to the landfill

• limit at 1000 mg/kg dry matter DOC (Degradable Organic Carbon) content of the output waste after a leaching test with L/S (Liquid to solid ratio) = 10 l/kg based on EU Standard EN 12457-2

Understanding correctly this criteria seems hardly doable even with a technical expertise background in this matter. One could question on the auditability of such information and so the possible tentative of greenwashing inherent to such hardy to verify information.

Despite climate methodology developments, it seems complicated for corporates to find and/or afford a niche expertise such as the one required for every non-climate objective. This concern also applies to external verifier that are responsible for verifying and certifying truthfully information issued by a company. It may result in an unfair competition between market participants depending on their financial situation, with some actors being enable to invest in the necessary equipment and thus being excluded.

b) Diverging definitions, scope, and reference

Other concerns raised regarding the articulation between the existing Technical Screening Criteria developed in the 1st Delegated Acts with the new ones. Natixis has analyzed the example of the “urban and suburban transport, road passenger transport activity”. This economic activity has already been assessed against the two climate change objectives. The new draft TSC report, reviews it against the “pollution prevention and control” objective.

On the figure below, Natixis assessed this activity’s SC and DNSH criteria against the 3 objectives.

Figure 8: Definition, scope and references inconsistencies - Focusing on urban suburban transport, road passenger transport” activity

Source: Authors (Natixis GSH)

Diverging definition between the draft of TSC and the 1st Delegated Act can be noticed. Indeed, NACE codes eligibility vary between the 1st DA and the draft TSC as the NACE codes H49,32 (Taxi operation) has been added in the TSC report published by the Platform.

Similar substantial criteria as the “zero tailpipe emissions” SC can be identified in different objectives (climate change mitigation and in pollution prevention and control).

Moreover, it appears that a DNSH criteria can become a SC criteria for another objective.

One can identify difficulties in assessing alignment as the scope of the DNSH criteria may vary from the SC criteria. Indeed, in the pollution objective, the criteria is dealing with category M and N road vehicle when the other objectives only consider category M.

References are also different between SC and DNSH criteria; under the pollution objective it considers the tires noise requirements limitation outlined in UNECE Regulation for the corresponding period of its application, while in the other objectives’ DNSH, tires noise requirements should comply with rolling resistance coefficient as set out in EU Regulation verified from EPREL.

There is a need to enhance coherence with the activities already covered. For companies to report under the future CSRD and for investors to monitor companies’ transition plans.

DNSH criteria resetting will be problematic and crucial for the implementation of the final report by the PSF, articulated with the Taxonomy DA.

VI - What has the PSF left for us

In its draft report [12] from August 2021, the PSF gave recommendations on TSC for 88 activities. Some activities being covered for several objectives (such as “digital solutions exploiting space-based earth observation” or “manufacture of machinery equipment”), one can find 17 activities assessed regarding climates objectives and 91 activities against the four remaining ones.

As one can notice when comparing with the final version of the report from March 2022, there is still a wait for activities covered in the draft but absent in the final report from the PSF. Details on those missing activities are presented on the table below. The recommendations on TSC for those activities should be revealed in May 2022 and in September 2022.

Figure 9: Overview of the activity covered by the PSF in the draft report in August 2021, but not in the final report in March 2022 [13]

Source: Authors (Natixis GSH), based on the Platform’s draft report in August 2021

Natixis is eager to analyze the remaining activities, notably the 26 activities that are already covered in the 1st DAs, such as electricity generation, power from cogeneration of heat/cool and power, sea, and coastal water transport (that are assessed for pollution prevention and control objective).

VII - Conclusion

Rather than analyzing economic activities already covered in the 1st Delegated Acts against non-climate objectives the Platform has mainly added new activities (41 out of 51).

Ten existing activities are now assessed against a non-environmental objective, but NACE Codes involved, the description of the activity or the Technical Screening Criteria, are sometimes inconsistent with the ones defined in the Climate Delegated Acts.

In addition, from being far to cover the entire economy (~100 out of 615 NACE codes), this new report raises questions about the evolution of the assessment of an economic activity. Can we conclude that a majority of economic activities will only be covered against one objective? From a transition point of view, what should a company targeted in priority between complying with an objective Substantial Contribution or meeting DNSH criteria?

On the economic activities covered by more than two objectives, shall it be assessed for the remaining environmental objectives, attention shall be paid to avoid an increase of complexity. Indeed, high complexity brings one to be skeptical on the implementation period of such TSC, that might be too long to apply adequately. Hence, it may discourage entities to be aligned to the Taxonomy and potentially weaken the European leadership on the matter.

[1] “Part A – Methodology report“, available here

[2] “Part B – Annex: Technical Screening Criteria”, available here

[3] The first Climate Delegated Acts dedicated to climate mitigation and adaptation entered into force on January 1st, 2022.

[4]In the Water Framework Directive, water bodies good status is defined with reference to dimensions such as good ecological status and good chemical status. Good ecological status covers the quality of the biological community, supporting elements (nutrients, oxygen), river basin specific pollutants, hydrological characteristics, and the presence of priority substances, while chemical status refer to compliance with all the quality standards established for chemical substances et European level

[5] Water Framework Directive, available here. In the WFD, the qualities of water bodies has been distinguished between the good ecological status (in which has been covered the quality of the biological community, certain supporting elements such as nutrients and oxygen, river basin specific pollutants regulated at national level, hydrological characteristics, and the presence of priority substances which determine the chemical status) and the good chemical status (that expressed in terms of compliance with all the quality standards established for chemical substances at European level)

[6] Stockholm Resilience Centre, “Freshwater boundary exceeds safe limits”

[7] The Corporate Sustainability Reporting Directive (CSRD) would amend the existing reporting requirement of the Non-Financial Reporting Directivie (NFRD). The CSRD will require disclosure on the eligibility and alignment of financial and non-financial entities activities with the EU Taxonomy. Several topics are discussed in the EU Parliament and the Council: the scope (in the EU Parliament some want to return to the exclusion of SMEs, others want to include all SMEs, including unlisted ones, as long as they are in a high-risk activity); the extra-territoriality of the rule; and the end of the reporting exemption for subsidiaries (proposed by Parliament)

[8] The JRC “Development of the EU Sustainable Finance Taxonomy – A framework for defining substantial contribution for environmental objectives 3-6”, available here

[9] Worth noting that these types of SC vary in their applicability to the different environmental objectives

[10] Please note that we used color dots as legend for the six objectives to show the relation one activity might have with other objective(s). For example, “Manufacture of chemicals” is proved with substantial contribution criteria for pollution prevention and control, climate change mitigation and adaptation

[11] Final report on Taxonomy extension options supporting a sustainable transition, by PSF, March 2022, available here

[12] PSF TSC draft report from August 2021, available here

[13] Please note that we used color dots as legend for the six objectives to show the relation one activity might have with other objective(s). For example, “Electricity generation from wind power” is proved with substantial contribution criteria for pollution prevention and control, climate change mitigation and adaptation