Extended Taxonomy: acknowledging “in betweenness” to soften elitism

6 - minute read

The Platform’s March 2022 recommendations on extending the Taxonomy [1] are timely and meaningful but unlikely to be politically endorsed [2]. Nonetheless, market participants must not wait for unpredictable legislative procedures to consider or even test the suggested concepts. See our dedicated flagship report here.

The current Taxonomy scheme is too static, notably because of its binarity, and incidentally too “elitist” [3]. We believe the Platform’s proposals would allow more inclusiveness, while preventing transition washing.

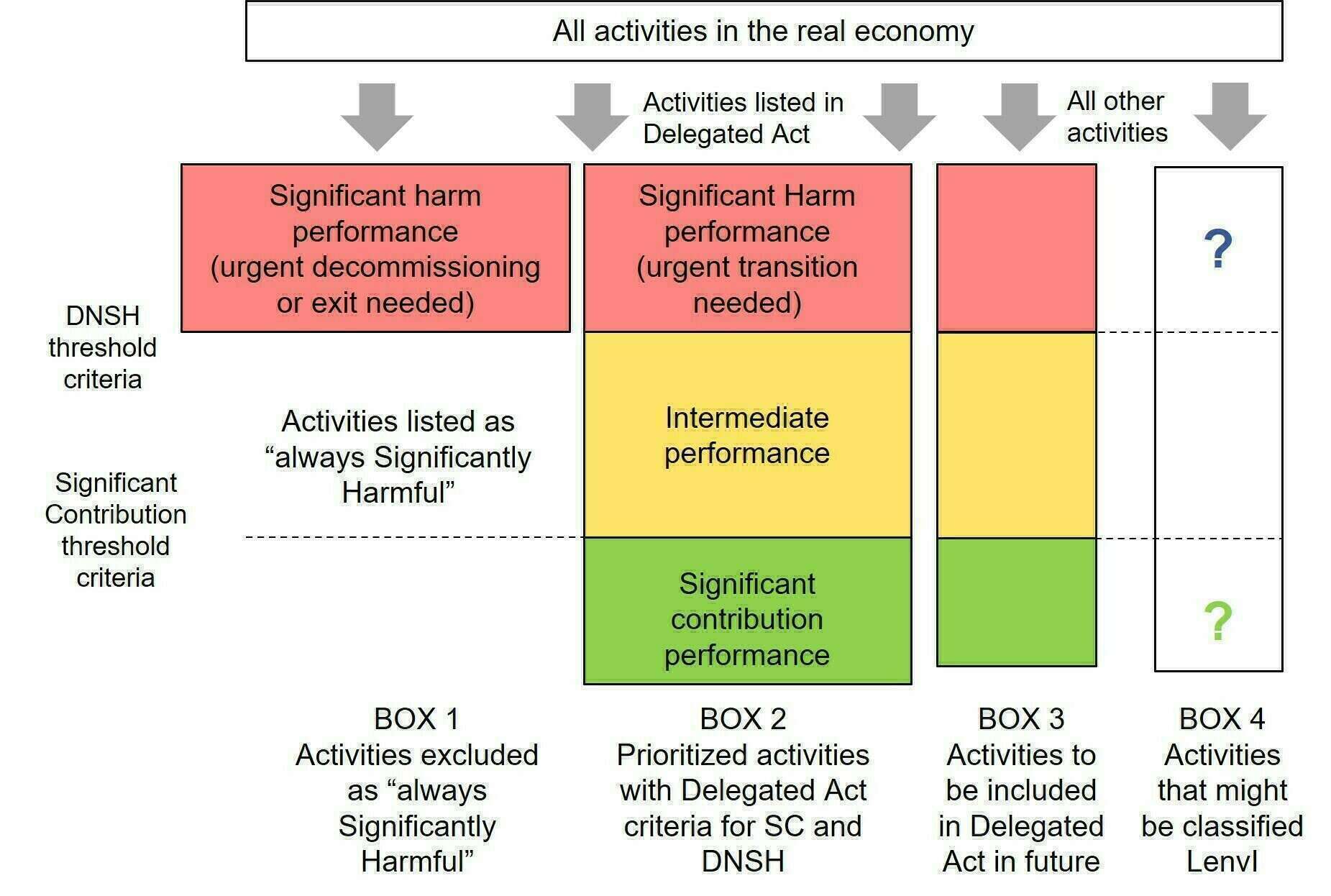

The group of experts proposes to explicitly introduce additional performance levels, in particular “amber” for intermediary performance (IP) and “red” for significantly harmful (SH) performance. The latter would notably require “urgent exit” and pave the way to decommissioning finance.

Figures 1, 2, 3: Extended Taxonomy explanation charts

Source: Final report on Taxonomy extension, Platform on Sustainable Finance, March 2022

Currently, several performance levels exist but only by default: Do No Significant Harm (DNSH), Significant Contribution (SC) and what is implicitly in between. The Platform suggests formalizing such a multi-level system, including by adding Low Environmental Impact activities (ex: accounting services to small businesses or childcare). The co-legislators never had in mind to set various performance levels, the three implicit levels interpretation is thus far stretched or even a contra legem interpretation. Above all, the existing implicit three performance levels were not set to work in a dynamic space.

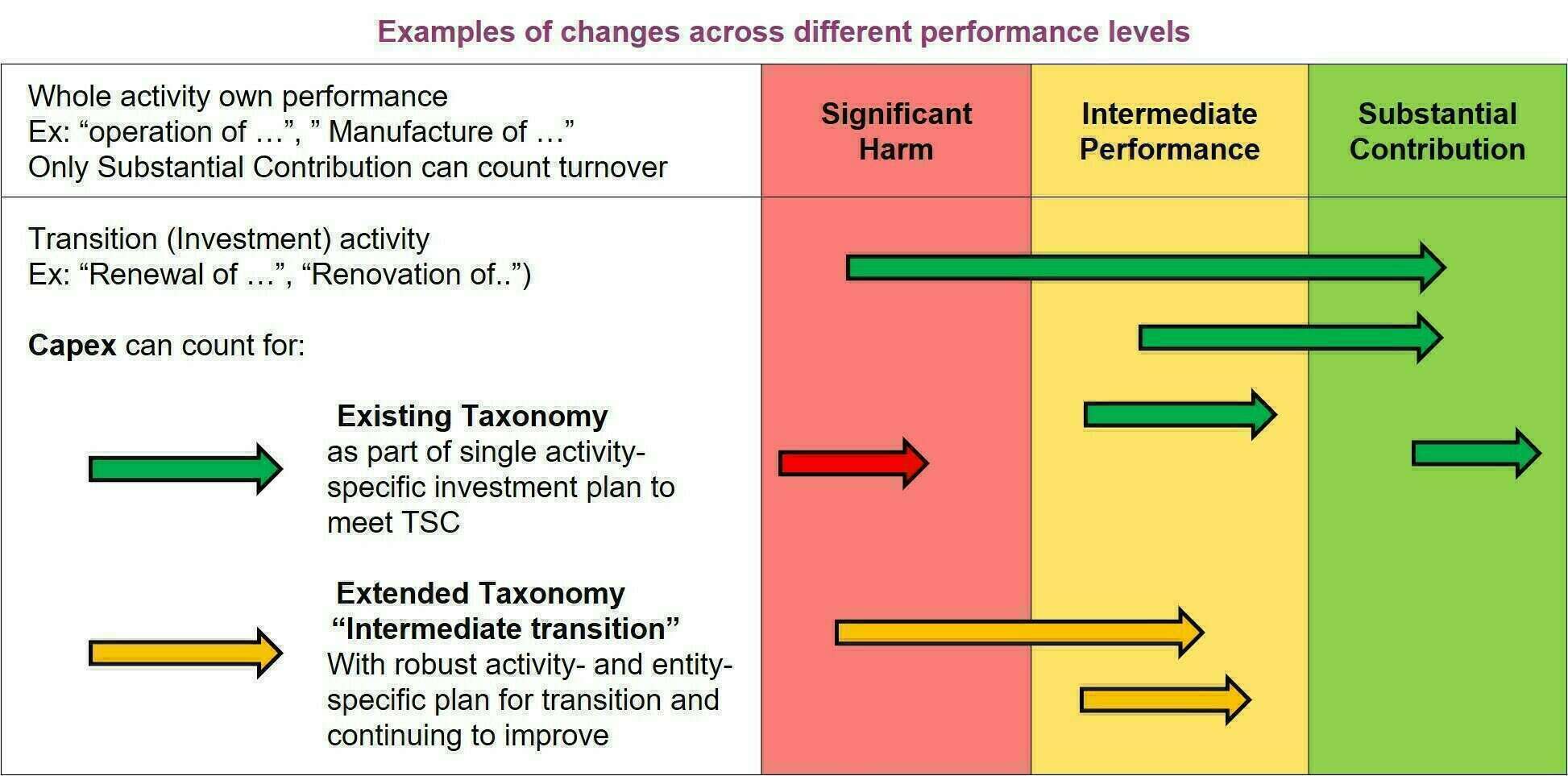

Thus, what is groundbreaking is to acknowledge changes from a performance level to another (ex: red-to-amber transition) and track dynamics. Such shift must be “constant” argues the Platform, for instance requiring to continuously staying out of significant harm performance level (red zone). Moreover, the boundaries of the red zone are tightening over time, what is being called “falling curves” by the Platform.

To properly factor and encourage “enhancing movements”, the Platform partially breaks with pure activity-level canvas of assessment (throughout the report, the erratic back-and-forth between asset, activity and entity-levels performance levels are bewildering). We commend this entity-level conceptual move and confess it inescapably increases complexity. Recently, we already noticed that the Complementary Delegated Act on gas power generation deviated from the activity-level tenet (although regrettably with many shortcomings, cf. our analysis “Taxonomy criteria’s Achilles heel unearthed by the War in Ukraine”, March 2022).

For years, we have been advocating transition finance frameworks applicable at entity-level and anchored on shades of green and brown, and holistic criteria (“Why we need a shaded taxonomy from green to brown and in between”, 2019 and our “Transition Tightrope Series”, 2021). However, whether such performance up-notching must be backward and/or forward-looking is largely eluded by the Platform, as well as verification safeguards. The cornerstone concept on which too many provisions are resting is the notion of “transition plan”, which remains too vague (the CSRD simply refers to business model and strategy compatibility with the objective to achieve climate neutrality by 2050 at the latest, see our article on the EU-Green Bond Standard).

The need for accountability or even opposability is made more daunting by the Taxonomy extension avenues laid down by the Platform. It once again raises the question of third-parties’ roles and responsibility. The pitfalls of forward-looking criteria and system can be summarized in one oxymoron: “intents enforcement”. Policy makers and market watchdogs must handle the discrepancies between intended or contemplated transition ambitions or plans, and what actually comes to tuition. Any transition plan cannot be taken for granted based only on intent. Who takes responsibility for such gaps, on what basis, and with what product and labelling consequences, remain unsolved. In contrast, performance up-notching that would be only backward-looking would limit sustainable finance instruments to refinancing, with mere zero additionality. When must the color of a transition plan be attributed? Should it be completed, simply announced, or already started? One suggests a trade-off requiring an already launched transition plan with preliminary achievements, granular near-term milestones and a reasonable completion period.

Defining the red space is of utmost relevance, especially for non-exclusion or divestment purposes. Decommissioning or urgent transition financing are welcome, in particular if attention is paid to employment aspects (fair transition, see one of our articles). However, the Platform’s report falls short of “breakthrough” examples defining activities technologically “doomed” (with no possibility of adequately improving their environmental performance, see the table below).

Table 1: The Platform only identified four activities falling into the always significantly harmful category

Source: Authors based on Final report on Taxonomy extension, Platform on Sustainable Finance, March 2022

Furthermore, we believe explicit nuances are necessary within the “red space”: activities that must be decommissioned, the ones that urgently need to transition, and the ones that are “simply” failing on the DNSH criteria must be handled differently.

Framing red-to-amber transitions is probably what could contribute the most to carbon cuts. To define significantly harmful activities, the Platform proposes to “reuse” the DNSH criteria. Thresholds already exist for various heavy-industrial activities. It acknowledges the limitations in doing so, and the extra work that would be required, in particular for inapplicable and qualitative DNSH, or the ones simply built on the respect of environmental or social law.

The timeline for Taxonomy extension is blurred, due to Taxonomy-related bottlenecks (complementary DA on gas and nuclear, adoption of technical criteria for the four non-environmental objectives, unlikely extension to social objectives). Regulatory fatigue is noticeable among protagonists, despite real implementation and appropriation progress (see the takeaways of a panel we recently organized at Environmental Finance Conference, Apr. 2022). We doubt the European Commission has the guts to launch the several years legislative fight to formalize red/significant harm performance levels (which can be perceived as an “exit signal” and will be fiercely opposed by economic and political lobbies). This is probably why the Platform advocates a rapid phasing in (as rapid as possible), and a voluntary reporting (based on the first legally in-force climate Delegated Act criteria). In the meantime, it says the necessary work to identify activities for which no technological possibility of improving their environmental performance to avoid Significant Harm must be initiated as soon as possible.

We believe the overall complexity should not be overstated if the different color /performance levels are set alongside the same unit and metric. The entry costs of mapping out activities against technical screening criteria can be lowered once and for all.

The present article and our forthcoming flagship report on the topic are therefore there to help launching the “trial period” and spur the voluntary uses encouraged by the Platform. There must be a continuum between industry-led standards/initiatives and hard-law requirements. The growth of regulations does not disregard market innovation. It simply requires exploring new domains where experimentation is needed prior to legislators or supervisors’ intervention.

APPENDICES

Diverging interests have loudly coalesced in calling for such extension, but any practical modality will hardly accommodate clashing expectations (see table 1 below). It is impossible to satisfy everybody, the legislators should thus try not to dissatisfy everyone.

Table 1: Sometimes clashing demands vis-à-vis Taxonomy extension

|

Main grievances |

Market participants and stakeholders calling for… |

|

1. Less “elitism” and need for “light green” criteria (more inclusiveness) |

… More nuances arguing that the performance bar is too high. They request to add more achievable criteria set around “light green” performance levels. Significant contribution performance levels are overall ambitiously calibrated, reportedly in line with net neutrality pathways. Consequently, the bulk of carbon-intensive activities is often out of track and indistinctly apprehended. Indeed, an activity very close to reaching the sustainability performance level set in the Taxonomy technical screening criteria and another one very far from it are equally treated. The entire classification is barely actionable to spur transition pathways for the bulk of companies that are “in between” levels of performance. |

|

2. Need for “brown” or “red” criteria defining significantly harmful activities and/or performance levels |

… A definition of “medium brown” performance level to properly manage transition risks, incl. supervisory authorities. For being useful, such delineation should not overlap with exclusion policies. It should go beyond “dark brown activities” such as coal power generation or mining. But no one politically dares to complete the list and delineate such a “red space”. Companies operating in high emitting sectors will consider it as “stigmatizing” or “divisive”. Opportunities around decommission finance may help convincing such opponents. |

|

3. Awarding enhancement pathways and dynamics rather than static and “out of the blue” point in time performances |

… Pathways and dynamics aspect to be better awarded. But forward-looking criteria often open a Pandora Box in terms of external verification, risks of investors misleading, changing criteria over time colliding with initial performance pathways improvement, etc. |

|

4. Enhancing the classification scheme usability at entity-level on top of activity-level provisions |

… A better usability of the Taxonomy at entity-level. Factoring performance up-notching or down-notching is more meaningful at entity level, possibly at facility-level. Asset or product are hardly upgradable (one exception being building). In contrast, mix of sold products or services can evolve. |

|

5. Improving the simplicity and usability of the overall classification scheme

|

… More simplicity. In its current design, the Taxonomy is already heavily criticized for its use complexity. |

Source: Authors (Natixis CIB)

[1] On March 29th, 2022, the Platform for Sustainable Finance released its long-awaited final report on Taxonomy extension avenues. The pursued goal is to set a more holistic and inclusive classification system. This report is the straight output of the article 26 of the Taxonomy Regulation (TR). According to this article “the Commission shall publish a report describing the provisions that would be required to extend the scope of this Regulation […] to cover economic activities […] that significantly harm environmental sustainability”.

[2] The stakeholders who have been the most vocal on the Taxonomy’s pitfalls may be facing a new scheme that explicitly identifies activities that must be exited. They are afraid of harsher financing conditions or access, or worse divestment, as a result of not being deemed sustainable as per the current Taxonomy. One can therefore anticipate their hostility to “red” criteria.

[3] The Taxonomy extension has been requested or advocated by many stakeholders, including us at Natixis (see Orith Azoulay’s article “Why we need a shaded Taxonomy from brown to green and in between”). Markets participants agree that the current framework consists in a rather binary classification: an activity is either deemed sustainable or not.