Sustainable Taxonomy development worldwide: a standard-setting race between competing jurisdictions

9-minute read

On July 12, the Platform on Sustainable Finance published two draft reports about a social taxonomy proposal and an extension of the current green taxonomy to significantly harmful (SH) and no significant impact (NSI) activities. In other words, the second report is related to the development of a brown taxonomy (see our October 2019 “Why we need a shaded taxonomy from green to brown and in between”).

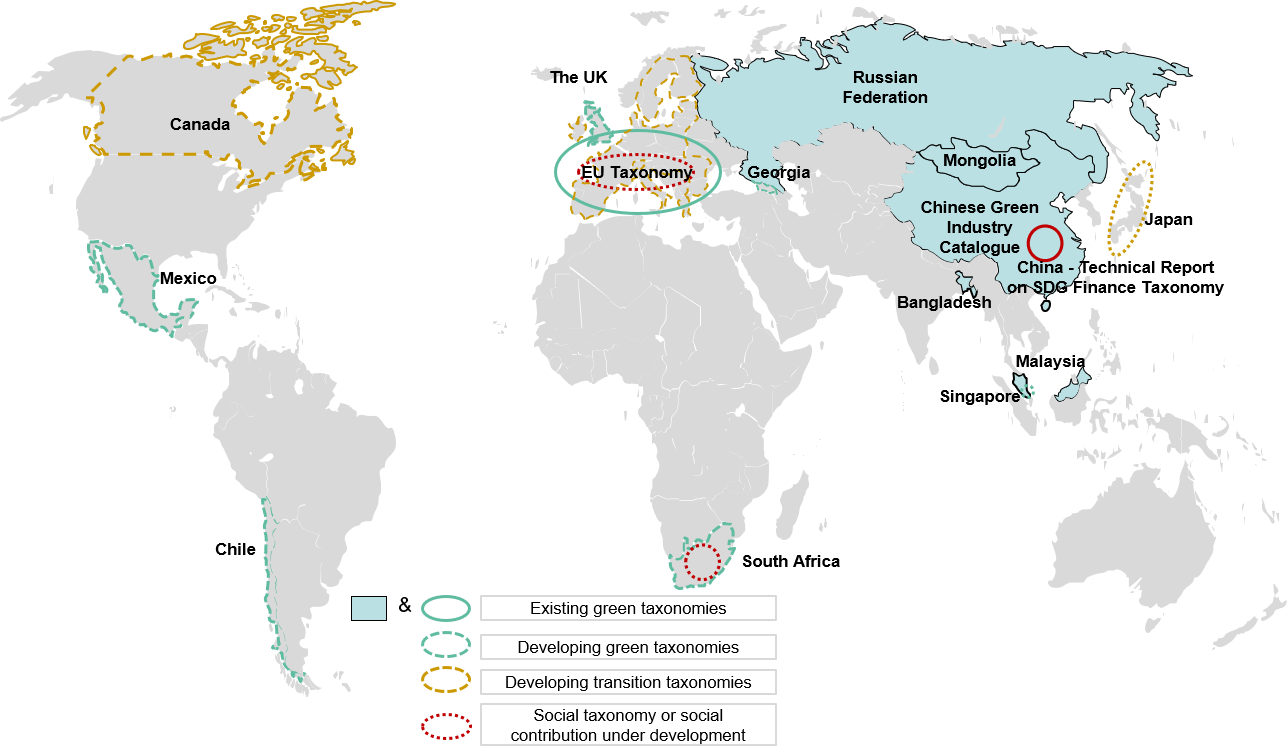

Besides the European Union (EU), China, and many other jurisdictions have developed or are developing taxonomies worldwide. Over the last two years, we have been witnessing a multiplication of taxonomy development initiatives across the world in what we depict as a standard-setting race (forthcoming report on the topic to be released in early September).

In our opinion, there are three main tendencies and lanes in this race:

- The development of social and brown/transition taxonomies;

- The heterogeneity of approaches to develop and implement taxonomies using the EU environmental Taxonomy either as a benchmark or as a source of inspiration;

- A strive to make taxonomies dominant and influential by competing jurisdictions

What is a sustainable finance taxonomy?

A sustainable finance taxonomy (hereinafter “a taxonomy”) is a classification tool helping investors and companies make informed investment decisions on sustainable economic activities. It is supposed to establish market clarity on what is sustainable in terms of green or social issues. For the moment, green taxonomies have been the most widespread, but developments regarding transition and social taxonomies and their subsequent criteria are ongoing.

However, taxonomies are also public policy tools and can become the basis of further regulations or programs. We provide some features of taxonomies in Table 1.

|

Table 1. Features of sustainable finance taxonomies |

|

|

Characteristics of a taxonomy: |

What a taxonomy is not or should not be: |

|

A taxonomy includes a set of criteria (technical or qualitative) defining economic actors deemed sustainable, green or social. It can be a:

|

|

|

Authoring bodies of taxonomies: |

|

|

|

|

Entry-point and level of definition of activities provided by taxonomies: |

|

|

Sustainable finance taxonomies can be built upon and structured around:

|

|

i. The development of social and brown/transition taxonomies on top of green taxonomies

- Green taxonomy

A green taxonomy focuses on pure green activities or activities that are considered unconditionally green in the sense that they positively contribute to the environmental objectives covered by the taxonomy. The granularity, scope, criteria and environmental objectives of these taxonomies can vary greatly. These are yet the most common types of taxonomies. The EU Environmental taxonomy seems the most advanced and ambitious to this day, but other jurisdictions developed or are developing green taxonomies. The Climate Bonds Taxonomy focuses purely on climate change mitigation and has been developed by a non-governmental institution – the Climate Bonds Initiative – to certify “Climate Bonds”.

- Social taxonomy

Social taxonomies per se, do not exist in their final form to this day, however, a Social Taxonomy draft has been published by the EU Sustainable Finance Platform upon the EU Commission’s request (see our related article). Social taxonomies focus on positive contribution to social objectives. The EU Social Taxonomy draft advocates for an architecture of criteria defining Substantial Contribution and Do No Significant Harm symmetrical to the EU Environmental Taxonomy. The objectives associated with this Social Taxonomy could be related to health, human rights, equality, and non-discrimination matters.

The contribution of products and services to adequate living conditions is central as the philosophy of a social taxonomy is not only to define minimum social safeguards that are already outlined even in environmental taxonomies (e.g., EU, Mongolian, South African taxonomies) but mainly to focus on the positive contribution that can be understood as the advancement of socio-economic characteristics or the filling of social needs or issues.

South Africa intends to progressively include social dimensions (positive contribution) or to develop a Social Taxonomy after the release of a green taxonomy. Moreover, in June 2020, the UNPD and China International Center for Economic and Technical Exchange (CICETE) released a SDG Taxonomy segmented between 6 sectors that mimics the ICMA SBP’s eligible activities, i.e., basic infrastructure, affordable housing, health, education technology and culture, food security and financial services. This taxonomy has been developed by an Advisory Committee and a Technical Committee under the joint effort of UNDP China and CICETE that consulted industry leaders, authorities and professionals.

- Brown or transition taxonomies

While environmental and pure green taxonomies are sometimes considered static, binary and/or too ambitious; transition or brown taxonomies are meant to provide criteria and methodologies assessing the transition paths of companies operating in traditionally brown sectors for climate change mitigation for instance. Indeed, green taxonomies’ criteria depict an end state and criteria allowing to consider a company, an asset or an economic activity aligned with a 2°C world in the case of climate. By comparison, transition taxonomies are allegedly more dynamic in the sense that they seek to identify and award companies that are transitioning and reducing their GHG emissions. To this day, no brown or transition taxonomies has been released. The European Union is considering an extension of its green taxonomy towards “transitional activities” and criteria through a “traffic-light system” with red, yellow and green colors, red meaning the activity does not have the potential to become compatible with a 2°C World, and yellow meaning the activity is transitioning. Canada and Japan are on their path to develop transition taxonomies, with Canada to release its first draft in 2021.

Map 1. State of taxonomy development worldwide

ii. Various approaches to taxonomy development and implementation

In the race to develop taxonomies, sovereign states use a variety of approaches and governance schemes. To our knowledge, in Canada, the development of a Transition Taxonomy is not sponsored by the Federal Government and the initiative comes from and is financed by the private sector (6 major banks, pension funds and insurance companies) and some corporations. In Japan, it is a group of researchers that first proposed guidelines on the development of a transition taxonomy. The Expert Panel on Sustainable Finance suggest participating in international discussions on taxonomies that “promote transition finance or include the formulation of roadmaps for high emission industries” (source).

In the EU, the Permanent Platform on Sustainable Finance received a mandate to develop the EU Taxonomy Regulation criteria, their implementation and extension. It is composed of 6 working groups, out of which two groups worked on the recently published Advise on extension of Taxonomy to social objectives and Advise on extension of the Taxonomy to significantly harmful and low impact activities. Almost all countries mandated technical working groups composed of experts of the field, while some countries decided to cooperate with non-governmental institutions with the reputation of structuring the Sustainable Finance agenda like the IFC, the UNDP or the World Bank.

On the other hand, as the EU environmental taxonomy is the most advanced and ambitious taxonomy for activities having a positive contribution to the EU’s 6 environmental objectives, many countries decided to build upon it. Country specificities are taken into account when developing these taxonomies. These different approaches are presented in the following tables.

Table 1. First approach to taxonomy development

In a nutshell: countries that view the EU Taxonomy as a benchmark (i), follow other international developments and best practices (ii), seek to adapt them to local context (iii) with the main goal of accelerating sustainable investment through better data (iv).

|

Country |

Details - Strategies to taxonomy development, partnerships and specific goals |

|

Mexico |

|

|

United Kingdom |

|

|

Georgia |

|

|

South Africa |

|

|

Bangladesh |

|

Table 2. Second approach to taxonomy development

In a nutshell: countries seeing the EU Taxonomy as a source of inspiration (i) with some metrics as benchmarks. They seek to close existing taxonomies' gaps or include activities not covered (ii). Pure green and transitional metrics will be distinguished and included (iii).

|

Country |

Details - Strategies to taxonomy development, partnerships and specific goals |

|

Chile |

|

|

Canada |

|

|

Malaysia |

|

|

Singapore |

|

iii. Competition between jurisdictions over taxonomy development: a standard-setting race

Besides environmental (climate change, biodiversity, pollution control) and public policy objectives (becoming carbon neutral by 2050, reducing waste, pollutant use in industry), jurisdictions also pursue broader political goals when developing taxonomies. In our opinion, there is a race to govern through norms and indicators on one side (a), and to assert positions as leading countries in the fight against climate change or towards sustainability (b).

a. Indeed, while some taxonomies are being developed at the initiative of the private sector (Canada), of academia (Japan) or by non-governmental institutions (CBI, ISO), most of them are developed by sovereign states. As such, companies are often objects/recipients of taxonomies and are not yet equipped to align to these taxonomies.

We believe that as taxonomy-aligned disclosures will emerge, the process of alignment in terms of regulation and disclosure in itself will be costly on top of business model and economic asset alignment. A branch of taxonomy-alignment services could emerge, especially if in the future, taxonomies not only serve as guidance and guarantees of quality and integrity among sustainable finance product issuers and investors, but also as bedrocks for public incentives or programs. For instance, in France, the climate strategy for public export financing includes climate reward mechanism for export project support (through credit-insurances) for activities deemed sustainable based on the EU Taxonomy (see our article for more details).

b. On the other hand, states - and to a lesser extent non-governmental institutions - are involved in taxonomy development which we perceive as a race. By scrutinizing communications related to taxonomy development among various actors, one could notice the seeking of singularity. Russia, Mongolia, Malaysia, China and the EU are already well advanced on the development of green taxonomies, the UK seeks to position itself at the forefront of green finance in the context of an already existing competition between British and French leaders to make London or Paris green finance centers. Singapore is actively seeking to develop a green taxonomy that would be used countries in the ASEAN (a member, Malaysia, already published a Climate Change Taxonomy) and to become the green finance hub of South-East Asia. On the other hand, Canada and Chile are developing taxonomies with the first one being specifically a transition taxonomy that could be used in high-emitting countries and even in the United States, while Chile seeks to develop criteria for the mining and other extractive industries that could provide guidance for other countries as well.

In this context, at Natixis, we believe this standard-setting race will be short-lived and that in the mid-term, after four to five years, the phase of harmonization and standardization will gain more momentum in already existing platforms like the International Platform on Sustainable Finance (co-chaired by the EU and China) that is to develop and publish a Common Ground Taxonomy in mid-2021.

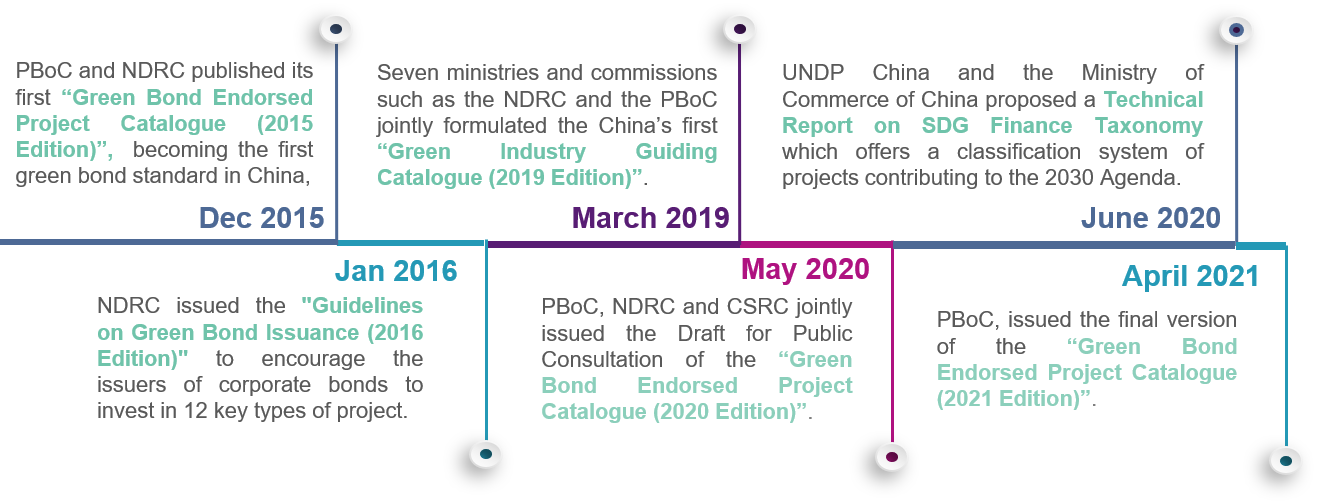

Table 3. The timeline of Chinese taxonomy development

Source: Natixis GSH – June 2020 article on the Chinese unified Green Bond Catalogue

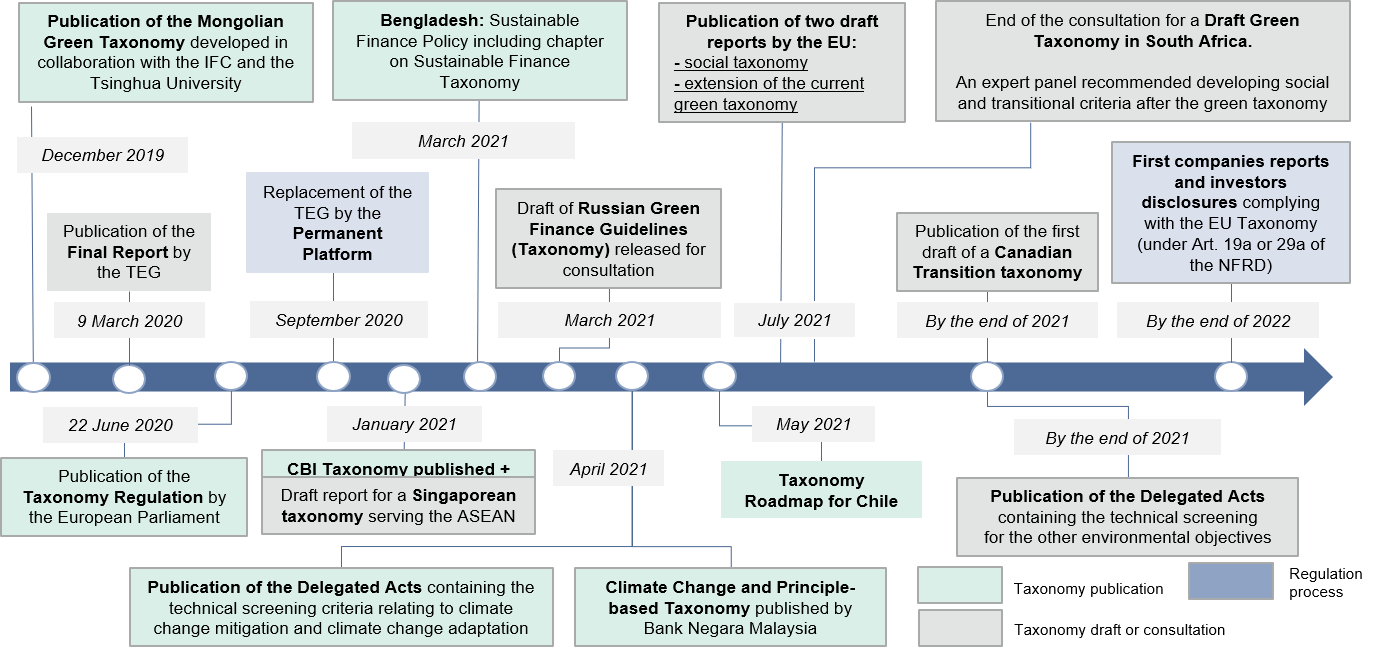

Table 4. The timeline of taxonomy development worldwide (excluding China)

See sources below

To go further:

- EU Taxonomy Regulation – available here.

- Mongolian Green Taxonomy – available here.

- Climate Bonds Taxonomy – available here.

- Sustainable Finance Policy of Bangladesh – available here.

- Chinese Green Industry Guiding Catalogue (2021 Edition) – available here.

- Technical report on SDG Finance Taxonomy of China – available here.

- Malaysian Climate Change and Principle-Based Taxonomy – available here.

- Russian Taxonomy for Green Projects – available here.

- South African Draft Green Finance Taxonomy – available here.

- Taxonomy Roadmap for Chile – available here.

- Roadmap for Sustainable Finance in Georgia – available here.

- Green Finance Industry Taskforce, “Identifying a Green Taxonomy and Relevant Standards for Singapore and ASEAN” (January 2021) – available here.