A Greener Green Bond Catalogue: The incoming China’s unified Taxonomy notches new win

On 29th May 2020, the People’s Bank of China (PBoC), the National Development and Reform Commission (NDRC) and the China Securities Regulatory Commission (CSRC) jointly issued the Draft for Public Consultation of the "Green Bond Endorsed Project Catalogue (2020 Edition)" (hereafter referred as " 2020 Catalogue").

A prerequisite for developing a robust and thriving green bond market is to define eligibility criteria clearly. To ensure the sound and orderly development of the green bond market, China has rolled out a succession of catalogues of green projects to better clarify the scope of the use of proceeds eligible from issuing green bonds. This 2020 Edition, like its previous versions, will serve as a reference basis for green bond approval and registration, third-party green bond evaluation, green bond rating and related information disclosure.

According to 2019 Green Bond Market Summary by Climate Bonds Initiative, China continued to top the country rankings and just was second to the USA, contributing USD31.3bn (the figures for China only include issuance that are aligned with international definitions of green) to market. Nevertheless, an addition USD24.2bn worth of labelled green bonds from Chinese issuers is not in line with international green bond definitions, as shown by the figure below.

Figure: Quarterly volumes of Chinese green bonds issuance (in USDbn) divided into internationally aligned and non-aligned green bonds

Source: Climate Bonds Initiative

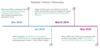

Since the end of 2015 when the PBoC and the NDRC published its first “Green Bond Endorsed Project Catalogue (2015 Edition)” (hereafter referred as “2015 Catalogue”), becoming the first green bond standard in China, green bonds have become important financing tools for China’s capital market to serve the real economy. In January 2016, the NDRC issued the "Guidelines on Green Bond Issuance"(2016 Edition) to encourage the issuers of corporate bonds to invest in 12 key types of projects, including energy-conservation and emission-reduction, green urbanization and circular economy. Meanwhile, these guidelines were also considered as another green bond standard by the market. In March 2019, seven ministries and commissions such as the NDRC and the PBoC jointly formulated the China’s first "Green Industry Guiding Catalogue (2019 Edition)", which clarified the definition and classification of green industries and green projects and laid the foundation for the new green bond catalogue. The development is presented in the figure below.

Figure: Recent significant developments of Chinese taxonomies regarding green bonds guidelines

Source: Natixis GSH

The draft 2020 Edition has been attracting widespread attention across the globe following its release and is under public consultation until June 12, 2020. The introduction of the 2020 edition indicates that China will soon realize the harmonization of the green bond standards locally and while also achieving a better alignment with global standards, which is of great significance.

Figure: The timeline of chinese taxonomies related to green bonds

Source: Natixis GSH

Interestingly, the stated objectives in drafting the 2020 Catalogue include:

- Aligning with NDRC "Green Industry Guiding Catalogue (2019 version)";

- Screening green projects with significant and positive environmental impacts in the areas of climate change, circular economy, and environment improvement;

- Taking mainstream international green finance taxonomy into consideration and continuously improving internationalization of the Catalogue.

The logic, framework and main contents of the "2020 Catalogue” are consistent and in synchronisation with the "Green Industry Guidance Catalogue (2019 Edition)" issued by NDRC in March 2019, unifying the currently fragmented supervision of China’s green bond standards, which created some confusion. Meanwhile, it also takes the convergence with the former edition of green bond standards and the related international standards into consideration, especially attitudes vis-a-vis so-called clean coal.

“The removal of utilisation of clean fossil fuel-based energy in the Catalogue 2020 demonstrated China's action in tackling climate change issue while pursuing pollution control and efficient utilisation of natural resources, which is highly aligned with its commitment in implementing the Paris Agreement.”

- Dr. Ma Jun, Chairman and President of Hong Kong Green Finance Association (HKGFA)

Harmonized Green Definitions in Closer Alignment with International Practices – Removal of Clean Utilisation of Fossil Fuel

Although China’s green bond standards are basically consistent with the international green bond principles, there are or were (depending on the adoption of the draft Catalogue) however some differences which are mainly reflected in two aspects.

The first one is the use of proceeds. While coal still plays an important role in energy generation in different parts of the world, China stands out as the world’s largest producer and consumer of coal, which accounted for around 60% of China’s total energy consumption for the last year. The country has been seeking to use green finance to pay for its transition to a cleaner mode of growth, but the 2015 Catalogue allowed it to be raised for the “clean use of coal” projects (e.g. coal-fired power generation, clean coal and fuel production, etc.), while international standards exclude fossil fuel projects.

Secondly, in terms of the use of proceeds, China’s green corporate bonds allow issuers to use up to 50% of proceeds to repay bank loans or to invest in general working capital, while the international green bond guidelines believe that issuers should use the proceeds to focus on green project related projects.

The inclusion of “clean coal” in the 2015 Catalogue had put China at odds with global standards, a point of contention for some international investors and many environmental groups, and has become the key to the integration of Chinese and International relevant standards. According to the latest 2020 draft plan, China has removed “clean utilization of fossil fuel” projects from the list of programs that can be funded by green bonds to achieve an alignment between the 2020 catalogue and international relevant standards, in addition to enhancing China’s discursive power in the landscape of green bonds, which means fossil fuels are no longer considered “green” by China. Instead, clean coal projects have been replaced by clean energy, reflecting a shift in China’s priorities from controlling air pollution to reducing greenhouse gas emissions.

Clarified Definition of Green Bond

Whereas, the "2020 Catalogue" stated the definition of green bonds rather distinctly: "Green bonds refer to the use of raised proceeds to support green industries, green projects or green economic activities that meet the prescribed conditions, and are issued in accordance with legal procedures and Securities that are agreed to pay back principal and interest, including but not limited to green financial bonds, green corporate bonds, green debt financing instruments, and green asset-backed securities."

Unification of The Green Bond Standard

The draft emphasizes one basic principle, which is “Continuous Adjustment”, i.e. working toward harmonization of local standards. Previously, green corporate bonds followed the standards in the "Guidelines on Green Bond Issuance"(2016 Edition). Meanwhile, other kinds of green bonds, including green financial bonds, green debt financing instruments, and green asset-backed securities, followed the 2015 PBoC Catalogue. In terms of principle, the two sets of standards are basically consistent with the general direction, but the classification of the categories and the scope of some specific projects are different.

The latest version of the catalogue now unifies the standards of China's green bonds, and the scope covers all types of green bonds, "including but not limited to green financial bonds, green corporate bonds, green debt financing instruments and green asset-backed securities.", making a single standard for sustainable finance-worthy projects in China going forward.

“Unifying the policy within the country’s various regulators is a “hugely significant step that will be welcomed by international investors.”

- Sean Kidney, Chief Executive Officer of CBI

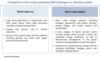

In addition, the 2020 Catalogue also considers the convergence with the previous standards. Although it is fundamentally based on the framework of "Guidance Catalogue for Green Industries (2019 Edition)", but there are also considerations for convergence and correspondence with the 2015 Catalogue, maintaining the same idea of its Level- II classification and Level-III classification.

Figure: main changes between the 2015 and 2020 versions of the Catalogue.

Source: SynTaoGreen Finance

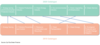

In terms of specific endorsed projects, compared with the 2015 Catalogue, the 2020 Catalogue has refined the three-level classification of the "Guidance Catalogue for Green Industries (2019 Edition)". The recent edition now contains a four-level classification, which puts endorsed green projects into 6 Level-I industry categories, which are presented below:

- Energy-saving and Environmental Protection Industry

- Cleaner Production Industry

- Clean Energy Industry

- Eco-environment Industry

- Green Upgrading of Infrastructure

- Green Services

Moreover, the Catalogue includes 25 Level-II industry categories, 48 Level-III industry categories and 204 Level-IV industry categories. The figure below illustrates the Level-I and Level-II industry categories.

Figure: Level-I and Level-II industry categories in the 2020 version of the Catalogue

Source: Natixis GSH

Moreover, each category (from each of the 4 levels) can be further broken down into more specific sub-categories corresponding to the type of activity and asset, as illustrated by the figure below. This additional level of granularity in turn makes this Catalogue very useful for structuring of green bonds.

Figure: Illustration how the different categories can be further broken down into several levels of granularity

Expanded Categories Related to Green Projects & More Detailed Descriptions/Conditions

A larger pool of green projects that can be identified and thereby earmarked for green bonds issuances under the 2020 edition is greatly broadened. Compared to the 2015 Catalogue, the Level-III categories are extended from the previous 38 to 204 in the 2020 Catalogue, suggesting that more green projects could be identified as green bond eligible projects, conducive to the expansion of the green bond market. The 2020 edition has expanded categories with more technical specifications, instructions and conditions, thus increasing the requirements on the third-party verification of green bonds. Moreover, the draft 2020 catalogue has listed sectorial standards and regulations for some categories (which contains rich technical details) and has recommended reference to any relevant qualitative, safety, technological and environmental national / industrial standard. In terms of “Solar Power Equipment Manufacturing” Project, for instance, the 2020 Catalogue details the technical specifications that the production of photovoltaic cells should have to reach the Level-I Standard specified in the Clean Production Evaluation Index System of the Photovoltaic Industry (No. 21, 2016 Edition). An example threshold of this is the total energy consumption in waste silicon processing which should be no more than 0.6 kw∙h/kg.

Conclusion

This 2020 draft unified catalogue represents a major step in China’s ability to re-boost its domestic green bond markets as well to attract more international green-driven capital now that one of the key controversies (clean coal) has been addressed and that greater clarity / transparency has been reached through a unique taxonomy.

Though, the 2020 catalogue is yet to clarify some more details and transparency guidance. For instance, it does not provide guidance on the type of eligible assets (cf. addressed in "Guidelines on Green Bond Issuance", 2016 Edition) which allowed issuers to use no more than 50% of the Use of Proceeds to repay bank debt or to finance Working Capital), or any guidance on reporting and external reviews. Natixis is working together with other Hong Kong Green Finance Association members to provide our feedbacks on the Consultation to PBoC.

Sources:

- Green Bond Endorsed Project Catalogue (2020 Edition)

- Green Industry Guiding Catalogue (2019 Edition)

- Guidelines on Green Bond Issuance"(2016 Edition)

- Green Bond Endorsed Project Catalogue (2015 Edition)