Strides in Oil and Gas transition methodologies with the release of ACT & SBTi guidance

8-minute read

The Sciences Based Targets initiatives (SBTi) and Assessing low-Carbon Transition (ACT) have simultaneously developed transition methodologies for the Oil & Gas (O&G) industry. This builds on other sustainable frameworks and tools encouraging investors, private and public companies to transition and tackle climate change, such as the EU Taxonomy (see our latest report here).

Oil & Gas companies now face a twofold challenge, which makes consensual strategic decisions difficult to reach: firstly, almost all low carbon scenarii foresee a slowdown in global energy demand and secondly, major shifts in O&G industry are both expected and necessary for a global transition to a low carbon economy. Therefore, these two methods, supervised and/or endorsed by the Carbon Disclosure Project (CDP) and the French Environmental Agency (Agence De l’Environnement et de la Maîtrise de l’Energie, ADEME) are timely milestones in the transition assessment journey.

The SBTi aims at determining science-based decarbonization targets for companies. It specifies how much and how quickly businesses need to reduce their GHG emissions by:

- Defining and promoting best practices in science-based target setting within specific sectors

- Offering resources and guidance to reduce barriers to their adoption

- Assessing and approving companies’ targets

The methodology sets GHG reduction targets in line with “well-below 2°C” or in line with 1.5°C scenarios, as stated in the SBT report “SBTi Criteria and Recommendations’” (April 2020). General target setting guidelines, which are not sector-specific, are available in the “Science-Based Target Setting Manual” (April 2020). Current SBTi target setting methods are only developed for Scope 1 and 2, but companies are encouraged to inform their Scope 3 targets by adapting the methodology by themselves (guidance is provided on the “Science-Based Target Setting Manual”).

The ACT methodology, which is also sector-specific, assesses the preparedness of a company to a transition to the low-carbon economy. It validates companies’ strategies as being aligned with ACT sectoral trajectory decarbonization[1] adapted to their activities and sector. To do so, it assesses their climate performance and provides an independent rating of that performance based on both qualitative and quantitative data. Sets of indicators are developed for several sectors to benchmark a state of alignment with low-carbon transition and to measure how far away companies are from that state. Therefore, the ACT methodology includes a forward-looking climate strategy robustness and credibility assessment, where SBTi focuses on assessing the alignment of a company’s current commitments. As detailed in the ACT generic Framework, when providing non-sector specific guidance for assessment and rating, companies should use science-based targets, which could be defined through the SBTi approach. Therefore, the two methodologies are complementary to each other.

In the case of the O&G industry, the two methodologies, whose sector supplement are still under development, are particularly complementary as they evaluate corporate action in different stages. The SBTi supports companies when setting science based targets, helping them to define a clear pathway to be in line with a 1.5°C or a 2°C decarbonization pathway, whereas ACT supports companies to achieve the low carbon transition by assessing their climate strategy, action plans, their operational impacts and dependencies based on historical and current data, as well as future projections.

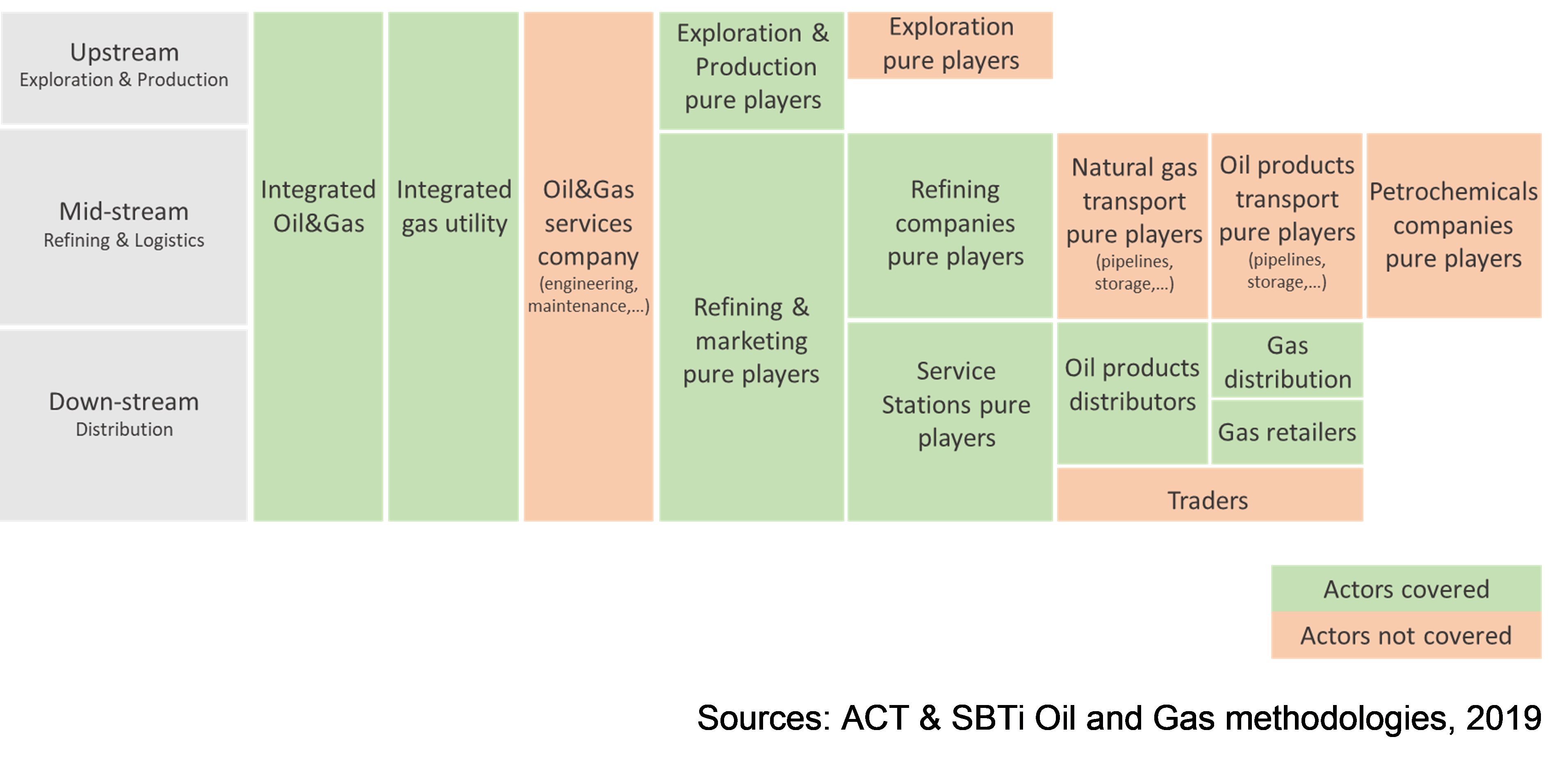

For the development of these methodologies, the O&G industry has been divided into three main segments that can be assessed:

- Upstream: comprising exploration, drilling, production, and O&G field services;

- Midstream: comprising pipelines, terminals, marine transportation, storage, and midstream services;

- Downstream: comprising refineries, retail outlets, natural gas distribution, and petrochemicals

Thereby, integrated companies that are companies operating across more than one segment of the value chain can also be assessed.

The players covered by the O&G guidance are the same for the two methodologies.

Figure 1. Companies in the O&G value chain covered by the SBT and the ACT O&G methodologies

Nonetheless, not all parts of the O&G value chain are addressed. Indeed, several activities are not considered sufficiently distinct or significant in terms of carbon emissions:

- O&G services and logistics, which are not considered to have an important decisional impact on investments needed to transition.

- O&G transportation and storage. Pure players are excluded as they are responsible for a small percentage of overall O&G sector emissions.

- Trading that is not seen as a strong lever for transition.

- O&G and electricity equipment manufacturing, since these activities fall in other sectors

- Petrochemicals

The SBTi methodology is out for public consultation and still lacks tangible details

SBT has published several documents on Oil & Gas and Integrated Energy Company emissions reduction target setting for public consultation[2], from August 10th until October 4th 2020. Several guidance documents have been released in addition to the Guidance on Setting Science-Based Targets for Oil & Gas and Integrated Energy Companies (67 pages).

As stated in the guidance document, the methodology “will address embedded emissions in fuel supplied, but will also seek to address scope 1 emissions (energy and methane process emissions). At a later stage the project should consider scope 2 emissions and links to refinery and petrochemical industry, consistent with the SBTi’s chemical sector development.”

First, to set a target within O&G industry, companies have to choose the scenario they plan to follow since this would influence the outcome of the target setting exercise, as well as the validation of those targets. For the moment, two scenario are proposed (well below 2C° target or a 1.5°C target) but the public consultation raises the hypothesis of developing other scenarios : “Should any scenario that meets WB2C or 1.5C be allowed, or are considerations around levels of overshoot, need for early action and approaching uncertain physical planetary limits reasonable criteria to select scenarios? “

Secondly, the SBTi provides a set of recommendations for target setting depending on six aspects: the type of company (integrated, upstream, midstream or downstream), the ambition level, the emissions scopes, the time horizon for the target, the target type (intensity or absolute), and the base year.

Then, companies have to choose their allocation method, namely, the means by which the emissions budget of an environmental scenario is divided up and allocated. Methods, details and calculations are provided in the guidance document.

Nonetheless, to be effective, further crucial details are needed, especially with regards to the target setting. Indeed, there is still a debate about the nature of the target measured through intensity or absolute reduction. The current SBT proposal is to “accept intensity targets set in a 5-15 year window, which reflect changes in final demand (final energy increasingly decarbonized), with a recommendation to set a long-term target as well. In addition to this requirement, IOCs/IECs (Integrated Energy Companies), as well as Upstream companies should also set an absolute, short-term target on the extraction, reflecting the necessary changes that need to occur at the supply side (decrease of fossil fuel supply)”.

Having said that, SBTi is seeking external opinion and included in the public consultation two interesting questions related to the measurement methods:

- “In your opinion, is it acceptable for companies to set only intensity targets or do you think they should also set absolute targets?”

- “Do you think that requiring companies to set an intensity target, reflecting changes in demand, and an absolute target, reflecting changes in supply, is sufficient to address the concerns about the climate integrity of the targets set by companies?”

The following transition modes are proposed in the document

- Energy company: diversifying to other forms of energy.

- Carbon company: transition to a circular economy model around carbon dioxide.

- Managed decline: ramping down Oil and Gas operations and returning capital to shareholders while maximising shareholder value.

- New direction: transition away from Oil and Gas to other activities.

We would argue transition is a combination of all these levers.

Meanwhile, another important question relates to “removal accounting”. How removals should translate into corporate GHG accounting is an issue currently under discussion and the document states it is not clear who should be credited for the removal, namely:

- If it should be the company that operates the asset with removal equipment;

- Or the company operating/owning/financing removal equipment;

- Or the company that effectively stores, monitors and holds the liability for long-term storage of CO2;

- All the three options, but clearly distinguishing between direct and indirect removals between participants in the removal and storage value chain

Therefore, the public consultation’s answers should hopefully provide a strong methodology development.

In addition to the work in progress for O&G industry, several other sectors are also developed by the SBT:

|

Publication of the final guidance |

|

|

Publication of the final guidance and the Science-based Target Setting Tool |

|

|

Publication of the guidance for passenger, freight and OEMs (methods and guidance for shipping and aviation companies in development) |

|

|

First draft guidance and target-setting tool in public consultation in August 2020. Launching of the methods, criteria and guidance in Fall 2020. |

|

|

Publication of the “Understanding and Addressing the Barriers for Aluminum Companies to Set Science-Based Targets “ as foundation |

|

|

Publication of the first report at the end of 2020 |

|

|

Initiation of the project, expected to be completed by Q2 2021 |

The ACT methodology is under review

After the public consultation held from mid-March 2020 until mid-April 2020, the draft Oil & Gas ACT methodology (130 pages) has been under a series of tests conducted by a pilot group of O&G industry companies, since June. The project is scheduled to last 5 months, plus 1 month for approval of final deliverables and must be completed by mid-November 2020 at the latest.

The methodology not only addresses GHG emissions from along the value chain, such as extraction or transformation assets, but also takes into account GHGs released by the end use of the products sold (combustion of various fuels).

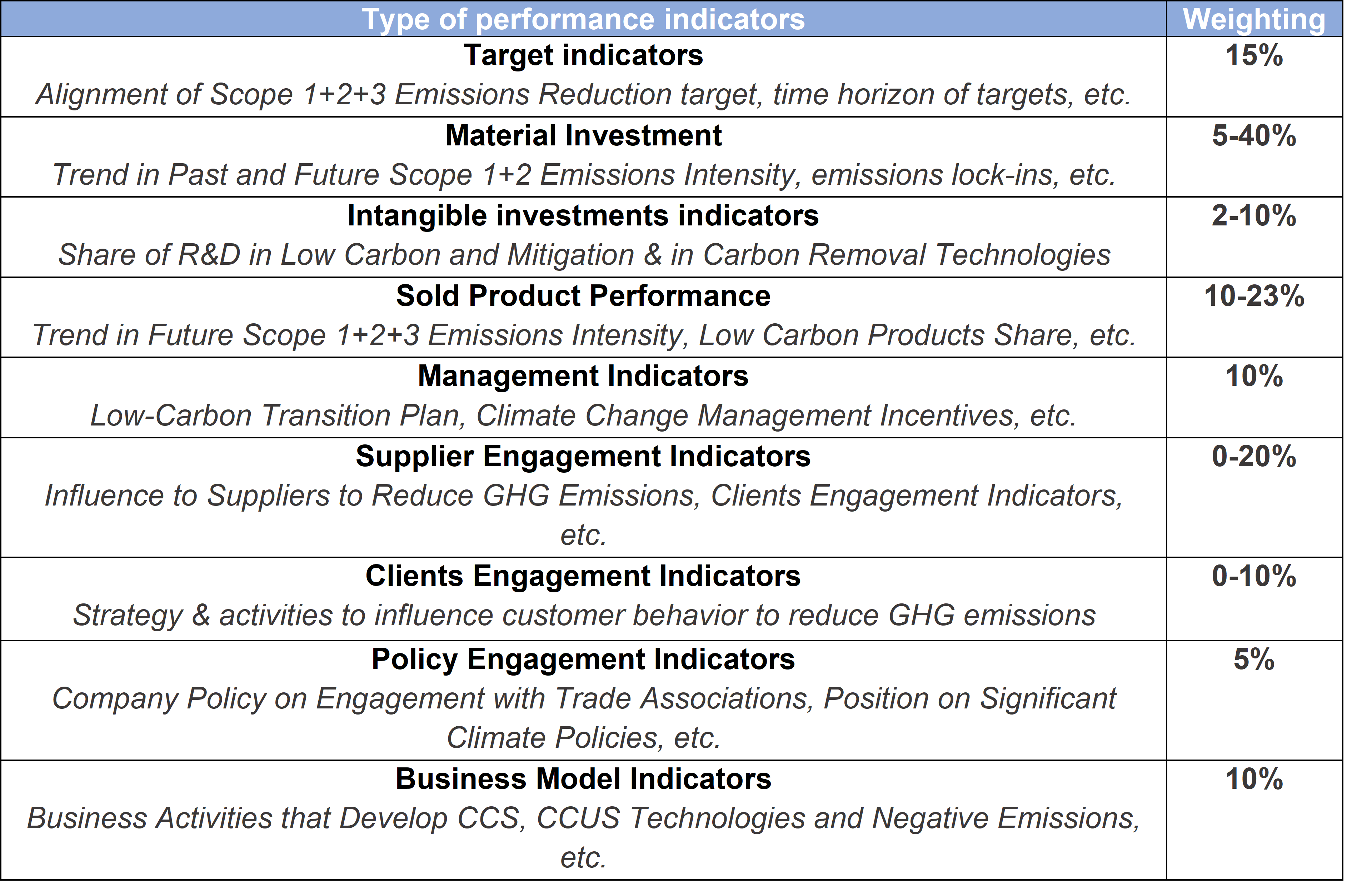

The assessment methodology is composed of nine modules, with quantitative indicators and qualitative ones. (see table 1). In addition to business model considerations, other qualitative indicators included are the company’s stance on climate change regulations and engagement with the supply chain. The current developments aim at testing this methodology and collecting feedback for improvements.

The proposed methodology includes all GHG sources in the reporting boundaries, from Scope 1 to Scope 3 Upstream and Scope 3 Combustion of Sold Products.

- Scope 1 and 2 GHG emissions are considered to be relevant at every step of the value chain, and are under the control of the O&G company

- Scope 3 Upstream GHG emissions are key for midstream and downstream activities, in order to integrate efforts of companies to source low carbon feedstock and products

- Scope 3 Combustion of sold products is the major stake in the climate transition and is dependent of the product mix brought to the market by the O&G companies.

The final assessment consists of a rating of the company, which includes three dimensions:

- Trend score related to forecast of future rating changes

- Performance score based on alignment measured with several KPI indicators

- Narrative score, which is the summary of the whole assessment

For the performance score, the weighting for each indicator scoring has been designed for each type of company covered by the ACT Oil & Gas methodology, in order to reflect the strategic stakes that are different from an upstream company to a downstream company (see table below).

Table 1. Nine modules assessed within the ACT O&G methodology: quantitative & qualitative indicators

Therefore, following the ACT methodology, an O&G company considered to be aligned should meet the following conditions:

- The company discloses a transition plan that details operation steps to achieve their objectives

- The company tries to lower emissions intensity of its whole value chain (scope 1,2 and 3) and to develop low-carbon projects

- The company has set science-based greenhouse gas reduction targets on every segment of the value chain

- The company is currently investing in R&D projects related to low carbon and removal technologies

- The company’s targets, transition plan, present action and past legacy show a consistent willingness to active the goals of low-carbon transition

Following the same model, methodologies for five other sectors have already been completed and available and eight other sectors are being developed under the ACTmethodology[3].

Following the public consultation and the series of tests, the respective SBTi and ACT methodologies can be expected to provide cornerstone guidance for the transition of the Oil and Gas industry.

Within an overall environment characterized by escalating political and societal pressure on climate change action, and by uncertainty on the extent of oil demand recovery after the end of the health crisis, there are noticeable structural trends within the Oil and Gas industry (See our Newletter’s June issue: European O&G Groups: actively trending towards electric utilities’ business models? and our article this month “BP intensifies its transition efforts amid asset value and oil demand forecast revisions”). Such methodologies are very much welcomed to help market participants assess their ambitions and practicality.

[1] The ACT methodology is based on the Sectoral Decarbonization Approach (SDA) developed by the SBTi (see the Framework document “Sectoral Decarbonization Approach : A method for setting corporate emission reduction targets in line with climate science”, 2015 available here).

The SDA is a scientific method to set GHG reduction targets necessary to stay within a 2°C temperature rise above preindustrial levels. The SDA allocates the 2°C carbon budget to different sectors and takes into account inherent differences among sectors (mitigation potential, sector growth, etc.).

[2] SBTi Oil&Gas and Integrated Energy Company Methodology development is supported by a technical working group including: World Wildlife Fund (WWF), Shell, Galp, Total, bp, Eni, Repsol, Agence de la transition écologique (ADEME), California Resources Corporation (CRC), World Resource Institute (WRI), i Care & consult, UN Global Compact, Imperial College London, University of Queensland Business School, Carbon Tracker, Climate Accountability, Aviva Investors, HSBC, World Benchmarking Alliance, OG Authority.

[3] The methodologies can be downloaded here.