Draft guidance on Taxonomy alignment disclosure published by the European Commission

7-minute read

On May 7, 2021, the EU Commission published a call for public feedback on the contemplated content, methodology and presentation of the information that companies will have to disclose in the context of the EU Taxonomy Regulation. This call for public feedback is composed of a proposal for a Delegated Act[1] including the details of the methodologies and the templates proposed by the Commission for the calculation methodology.

The Article 8 of the EU Taxonomy Regulation

The article 8 of the EU Taxonomy Regulation (see our Taxonomy publications) relates to the content and presentation of the information to be disclosed. It requires companies subject to the Non-Financial Reporting Directive (NFRD)[2] to publish extra-financial information to include a non-financial statement on “how” and “to what extent” their activities relate to economic activities that qualify as environmentally sustainable under the Taxonomy Regulation (technical screening criteria, DNSH, etc.).

Scope of application

This Regulation applies to financial and non-financial undertakings that are subject to the NFRD[3]. EU rules on non-financial reporting currently apply to large public-interest companies with more than 500 employees. On 21 April 2021, the Commission adopted a proposal for a Corporate Sustainability Reporting Directive (CSRD), which would amend the existing reporting requirements of the NFRD. All companies issuing securities on a regulated market (including SMEs) will be subject to it, as well as large companies meeting at least 2 of the following criteria:

- +250 employees

- total balance sheet > €20M

- total turnover > €40M

The Delegated Acts on Article 8 are excruciatingly important regarding the Taxonomy Regulation as they provide a user-guide explaining thoroughly what and how companies must calculate and report their taxonomy alignment. The rules set out in the Delegated Act specify the content and presentation of information to be disclosed allowing companies to translate the technical screening criteria of the Climate Delegated Act (and the future other environmental criteria) into quantitative key economic performance indicators (KPIs) meant to be publicly disclosed.

Information to be disclosed by non-financial and financial companies

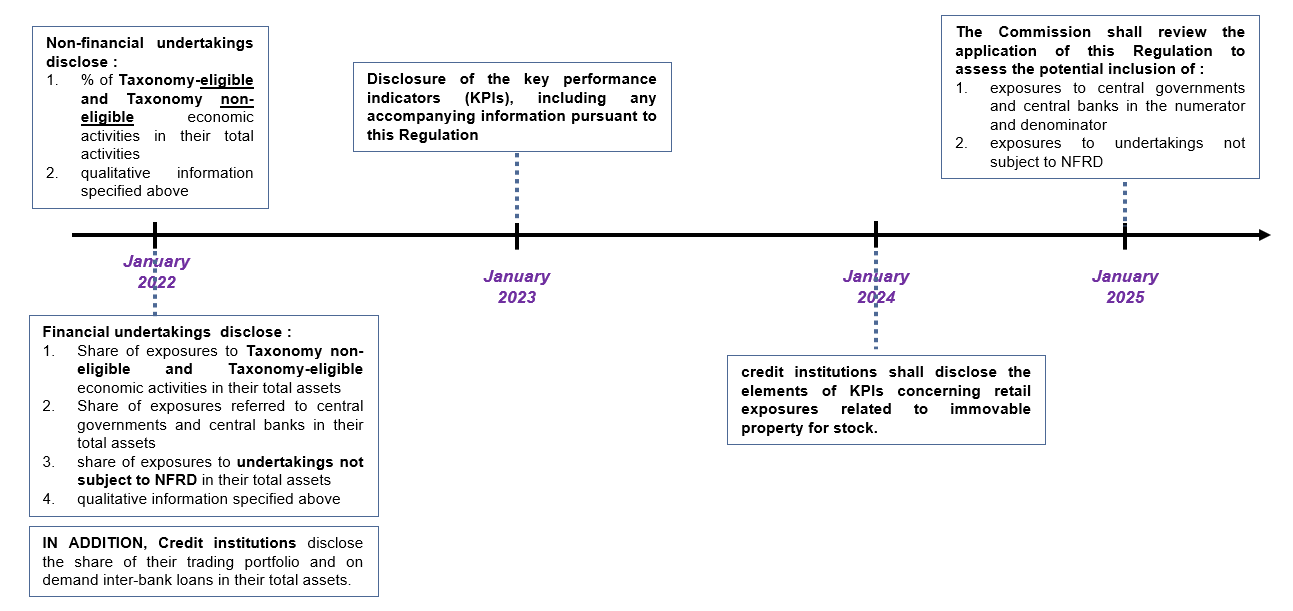

Non-financial companies shall disclose the proportion of environmentally sustainable economic activities that are Taxonomy-aligned:

- The turnover KPI represents the proportion of the net turnover derived from products or services that are taxonomy-aligned. The Turnover KPI gives a static view of companies’ contribution to environmental goals.

- The CapEx KPI represents the proportion of the capital expenditure of an activity that is either already taxonomy-aligned or is part of a credible plan to extend or reach environmental sustainability. CapEx provides a dynamic and forward-looking view of companies’ plans to transform their business activities.

- The OpEx KPI represents the proportion of the operating expenditure associated with taxonomy-aligned activities or to the CapEx plan. The operating expenditure covers essentially non-capitalised costs relating to the maintenance and servicing of companies’ assets (plant, equipment) that are necessary to ensure the continued and effective use of assets.

Information to be disclosed by financial companies

Financial undertakings in the scope of the Delegated Act are asset managers, credit institutions, investment firms and insurance and reinsurance undertakings. The European Commission has based its regulation on ESA’s[4] advices made in early March[5]. The Article 8 Delegated Act set common rules for the different key performance indicators calculation and their disclosure by financial undertakings.

- Shall be excluded from the denominator the exposures to central governments and central banks

- Shall be excluded from the numerator the exposures to central governments and central banks, derivatives, exposures to undertakings not subject to NFRD

- Bonds issued under Union legislation on environmentally sustainable bonds and environmentally sustainable bonds issued under national legislation shall be included in the numerator of KPIs only up to the value of Taxonomy-aligned economic activities that the proceeds of those bonds finance

- Financial undertakings shall provide for a breakdown in the numerator and denominator of the KPI for exposures and investments in:

- non-financial undertakings

- financial undertakings

- non-financial undertakings that are not subject to NFRD established in the Union

- financial undertakings that are not subject to NFRD established in the Union

- non-financial undertakings established in a third country that are not subject to NFRD

- financial undertakings referred established in a third country that are not subject to NFRD

- derivatives

- other exposures and investments

A- Asset managers

To assess their level of Taxonomy-alignment, asset managers should report the proportion of investments in Taxonomy-aligned economic activities in the value of all investments managed (Green Investment Ratio).

- The Green Investment Ratio[6] should be computed thanks to the different investee undertakings Taxonomy-alignment ratios, these KPIs are appropriate benchmarks to capture the environmental performance of investee undertakings.

Asset managers shall disclose a KPI based on turnover KPIs of the investee companies and a KPI based on the CapEx KPI of investee companies.

B- Credit institution

The main KPI for credit institutions to reflect the credit institution’ on-balance sheet is:

- The green asset ratio (GAR)[7], which shows the proportion of the credit institutions’ assets invested in/financing Taxonomy-aligned economic activities as a share of total covered assets.

Credit institutions also perform other commercial services and activities generating fees and commission: they may manage underlying assets or provide financial guarantees, leading to off-balance-sheet exposures as well. To assess the Taxonomy-alignment of these activities, the Commission suggest using three different KPI:

- The KPI for fees and commission income (F&C KPI)[8] is linked to services associated with taxonomy-aligned economic activities. It shall be defined as a proportion of the institution’s fees and commission income derived from products or services (other than lending) associated with taxonomy-aligned economic activities, compared to total fees and commissions from products or services other than lending.

- The green ratio for financial guarantees to corporates (FinGuar KPI)[9] is defined as a proportion of financial guarantees supporting debt instruments to corporates financing taxonomy-aligned economic activities compared to all financial guarantees supporting debt securities to corporates.

- The green ratio for assets under management (AuM KPI)[10] is defined as a proportion of assets under management (equity and debt instruments) financing taxonomy-aligned economic activities, compared to total covered assets under management (equity and debt instruments).

In cases the trading portfolio has a more predominant role in the business model, the credit institutions should provide separate, more granular, quantitative information and a specific KPI for their trading book:

- The Trading KPI is a ratio of absolute purchases plus absolute sales of taxonomy-aligned securities compared to total absolute purchases plus total absolute sales of eligible securities.

C-Insurance and reinsurance undertakings

Insurance and reinsurance undertakings shall present the weighted average of investments that are directed at funding or are associated with Taxonomy-aligned economic activities.

- The KPI on investments is showing the share of Taxonomy-aligned assets in their overall assets to reflect the use of the funds collected from their underwriting activities.

- The KPI on underwriting activities themselves which shows what proportion of the overall non-life underwriting activities is composed of non-life underwriting activities related to climate adaptation. The disclosures shall be broken down by environmental objective in percentage terms and monetary units, where available.

D-Investment firms

Alongside credit institutions, investment firms provide a range of services which give investors access to securities and derivatives markets. Unlike credit institutions, investment firms do not accept deposits, nor do they provide loans on a significant scale. Relevant KPIs to monitor the degree of Taxonomy-alignment of an investment firm should cover both their dealing on own account and their dealing on behalf of clients.

- The GAR for investment firms, disclosure of the KPI for dealing on own account should focus on the investment firms’ investments, including debt securities and equity instruments in investee companies. It reflects proportion of the total assets composed of Taxonomy-aligned assets.

- the KPI for fees and commission income (F&C KPI) for activities on behalf of all their clients on the other hand, should be based on the fees, commissions and other monetary benefits that investment firms generate from their investment services and activities provided to their clients.

Qualitative disclosures for financial undertakings

In addition of the disclosure of quantitative measures the Commission also request financial undertakings to disclose some qualitative information to support their explanations and markets’ understanding of these KPIs:

- Contextual information including the scope of assets and activities covered by the KPIs, information on data sources and limitation

- Explanations of the nature and objectives of Taxonomy-aligned economic activities and its evolution starting from the second year of implementation

- Description of the compliance with the EU Taxonomy in the financial undertaking’s business strategy including target setting, product design processes and engagement with clients and counterparties

- For credit institutions that are not required to disclose quantitative information for trading exposures, qualitative information on the alignment of trading portfolios with the EU Taxonomy, including overall composition, trends observed, objectives and policy

- Additional or complementary information in support of the financial undertaking’s strategies and the weight of the financing of Taxonomy-aligned economic activities in their overall activity

Some clarifications are still required

This draft disclosure delegated act says that non-NFRD companies, including non-EU companies and SMEs, may report Taxonomy relevant information to financial institutions on a voluntary basis. In addition, it proposes to grant a period of phase-in for the reporting of Non-NFRD exposures by financial companies in the numerator of their green investment/asset ratio to start only in 2025. This transition period could be considered as essential for smaller companies in order for them to get time to adapt but another taxonomy may emerge in the meantime and be used by SMEs, which would cause the EU to lose its leadership.

Furthermore, determining the Taxonomy-alignment of certain activities based outside the EU could be challenging. Indeed, the ‘Do Not Significant Harm’ of the EU Taxonomy often refer to comply with some very specific European rules.

Finally, a question arises concerning activities not yet included in the Taxonomy. From a company point of view this could be a disadvantage and for financial undertakings, especially credit institutions, the inclusion of newly Taxonomy-aligned activities to their transactions backlog may be challenging. This could be even more true for retailers.

Timeframe

The public consultation launched by the Commission has closed on June 2, 2021 and the final Delegated Act is expected to be published by end of June 2021. Due to the entry into force and application of the Climate Delegated Act by end of 2021 and material difficulties for assessing compliance of economic activities in 2022 with technical screening criteria laid down therein for the previous reporting year, the application of this Regulation in 2022 should be limited only to certain elements and qualitative reporting. This Regulation should therefore apply fully only from 1 January 2023 on the basis of 2022 exercise.

Title 1. Entry into force and application

Source : Natixis

Next steps

The Delegated Act will be revised alongside the developments and future revisions of the Taxonomy Regulation, as well as the regulatory technical standards related to product disclosures (e.g. SFDR), and possible developments related to the review of the NFRD (CSRD proposal).

The Taxonomy-related reporting set out in this Delegated Act will serve as a basis for various future and ongoing initiatives in sustainable finance. Reporting under this Delegated Act will facilitate the development of EU-wide standards for environmentally sustainable financial products and the creation of labels that recognise compliance with these standards. Notably, the Commission proposals on the EU green bond standard (‘EU GBS’) and EU ecolabel for financial products are set to refer to the Taxonomy Regulation.

[1] Delegated Acts supplement parts of EU legislation, for example when it comes to detailing certain measures.

[2] The NFRD is currently being revised to become the Corporate Sustainability Reporting Directive (CSRD) (See our article published in our April Newsletter).

[3] Other undertakings not concerned by NFRD may apply this Regulation on a voluntary basis.

[4] The three European Supervisory Authorities (ESAs) are the European Banking Authority (EBA), European Securities and Markets Authority (ESMA), and the European Insurance and Occupational Pensions Authority (EIOPA)

[5] for more information please refer to the article published in our March Newsletter

[6] The numerator shall consist of a weighted average of the value of investments in Taxonomy-aligned economic activities of investee companies and the denominator shall consist of the value of all Asset under Management (AuM) without exposures to central governments and central banks resulting from both collective and individual portfolio management activities of asset managers.

[7] The numerator shall cover the loans and advances, debt securities, equities and repossessed collaterals, financing Taxonomy-aligned economic activities based on turnover KPI and CapEx KPI of underlying assets. The denominator shall cover the total loans and advances, total debt securities, total equities and total repossessed collaterals and all other covered on-balance sheet assets.

[8] The numerator of the KPI shall include the fees and commissions income from services other than lending and asset management provided to undertakings, associated with Taxonomy-aligned economic activities. For financial undertakings, the ratio from the counterparty to be applied shall be the same as for the KPIs for these undertakings. The denominator shall be the total amount of fees and commission income from undertakings from products or services other than lending and asset management.

[9] The methodology for the computation of the KPI on financial guarantees shall be the same as the methodology specified for the KPIs on loans and advances and/or debt securities towards undertakings, but applied to the underlying loans and advances/debt securities that the credit institution supports.

[10] The methodology for the computation of the AuM KPI shall be the same as the methodology for asset managers.