Climate Action 100+ Progress Report on investors engaging with high carbon emitters: now it’s aviation sector’s turn

3-minute read

The Climate Action 100+ (CA 100+) initiative has released its latest 2020 progress report on the actions undertaken by high-emitting industries, such as aviation, in order to reduce their impact on climate change.

The initiative CA 100+ is an investor initiative launched in 2017 by a large panel of investors to ensure the world’s largest corporate greenhouse gas (GHG) emitters take necessary action on climate change. To do so, it chose to observe the 100 highest emitting corporates, a panel that was then extended to about 160 global companies. Because of their significant greenhouse gas emissions, these companies are considered as critical to meeting the goals set by the Paris Agreement.

An innovative approach to measure company progress

CA 100+, supported by 545 investors representing ca USD 52 trillion in assets under management, has set up a new approach to measuring company progress: the Climate Action 100+ Net Zero Company Benchmark. This benchmark is composed of the following indicators:

- Net zero GHG emissions by 2050 (or sooner) ambition

- Long term (2036 to 2050) GHG reduction target

- Medium term (2026 to 2035) GHG reduction target

- Short term (2020 to 2025) GHG reduction target

- Decarbonation strategy

- Capital allocation alignment

- Climate Policy engagement

- Climate Governance

- Just Transition

- TCFD disclosure

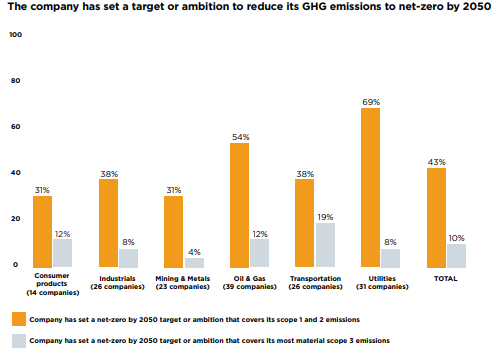

Thanks to this benchmark, CA 100+ spotted that about 43% of the initiative’s focus companies now have goals or commitments for net-zero emissions by 2050 or sooner in some form. While 51% also have short-term emissions reduction targets (to 2025) and 38% have medium-term targets (2026-2035).

Image 1. GHG Emissions by Sector 2020

Source: CA 100+, 2020 Progress report

Starting from this assessment, members of the Initiative can put all their investor engagement weight on the most lagging companies, making the initiative one of the most powerful and systematic transition tools initiated collectively by investors.

The aviation sector strategy at the heart of concerns

Being amongst the least advanced sectors on commitments to net-zero alignment, the transportation sector looks pale in comparison. There are currently 26 transportation companies on the CA 100+ focus list. These include automobile and truck manufacturers, shipping firms, and especially airline and aerospace companies.

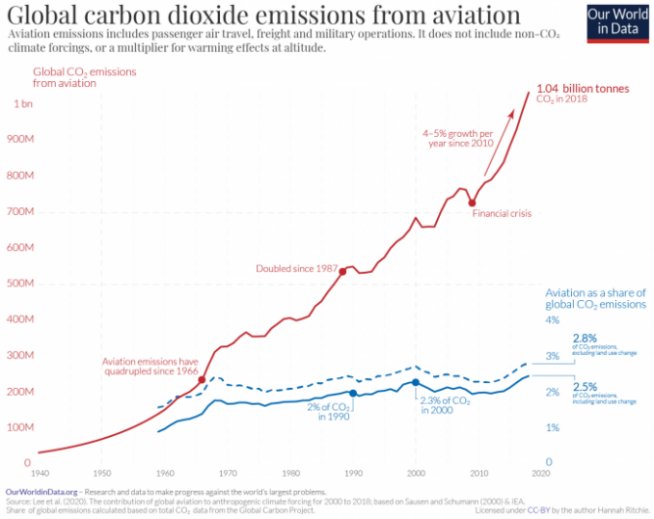

With 1.04 billion tons of emitted CO2 in 2018, including both passenger and freight, aviation is considered as a significant carbon-intensive mode of transportation. Aviation accounts for 2.5% of global CO2 emissions, but its overall contribution to climate change would be higher according to a scientific research led by David Lee in 2020. Indeed, the aviation sector also accounts for approximately 3.5% of effective radiative forcing. Radiative forcing measures the difference between incoming energy and the energy radiated back to space: if more energy is absorbed than radiated, the atmosphere becomes warmer.

Image 2. GHG Emissions from the Aviation Sector (1940-2020)

Source: Our World in Data

An urgent need for clearer guidelines

Despite the recent stop in travels due to the Covid-19 crisis, the sector is expected to grow rapidly in the next few years. Therefore, it is necessary to act and put new measures in place in order to address carbon emissions.

As an example, the International Civil Aviation Organisation (ICAO)'s fuel efficiency target recently introduced the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), which requires purchasing carbon credits. Few other measures were set up but they are insufficient to align with the goals of the Paris Agreement yet.

In a report published in January 2021, the CA 100+ concluded that the aviation sector should engage in two directions. First, from the supply-side, innovation will be key to create new technologies and fuels such as advanced biofuels and synthetic fuel. However, this part will require investments and policy intervention to succeed. Second, from the demand-side, actions to slow air transport demand, improve operational efficiencies and improve air traffic management seem necessary to complete the supply-side efforts.

CA 100+ recommendations to bounce back

Facing these problems, the CA 100+ initiative put forward four recommendations as follows:

- Airline and aerospace companies should make an explicit commitment to achieve net-zero GHG emissions by 2050 with short and medium term targets. Capital expenditures should first be aligned with the targets, but also be detailed enough between GHG reduction and carbon offsets projects.

- Companies should accelerate the adoption of sustainable aviation fuels (SAF), including advanced biofuels and synthetic fuels.

- Public policies need to be tougher in the sector as domestic and international policy will affect the ability of the sector to adapt to climate change. Policy lobbying and greater engagement will be expected from investors.

- Linked to the policy topic, disclosure will be key, as companies need to adopt the Task Force on Climate-related Financial Disclosures (TCFD) recommendations. Disclosures should include GHG emission-related metrics on Scope 1, 2 and 3, but also the specific carbon offsets projects.

Qantas Airways Limited could be mentioned as a best-in-class airline company. Indeed, it became the first airline in the world to commit to net-zero emissions by 2050 in October 2019, alongside a $10 million investment in sustainable aviation fuels, and a pledge to double its offset program.

The CA 100+ came forward with guidelines that could clearly help the aviation sector to go in the right direction. Recommendations embed the objectives of the initiative, which are to accelerate the business transition to a net-zero emissions future and to ensure that global economies are more resilient to climate change.

The journey to embark on will be long but crucial for both companies and investors engaged in the climate change fight. This progress report comes timely, and it will definitely mark the beginning of new expectations for aviation and all high-emitting industries more broadly.