The London Stock Exchange Group launches a dedicated “Transition Bond Segment”

4-minute read

Mid-February the London Stock Exchange Group (LSEG) announced the expansion of its Sustainable Bond Market by creating a so-called Transition Bond Sub-Segment, which is not defined by a format per se (it can be Use-of-Proceeds and General Corporate Purpose Instruments alike). The LSEG is the first exchange to establish a “transition overlay” to its existing market components (see table 2 on Stock Exchanges’ Sustainable Finance Instruments Segments). A specific body of transition criteria presented below delineates this layer of analysis.

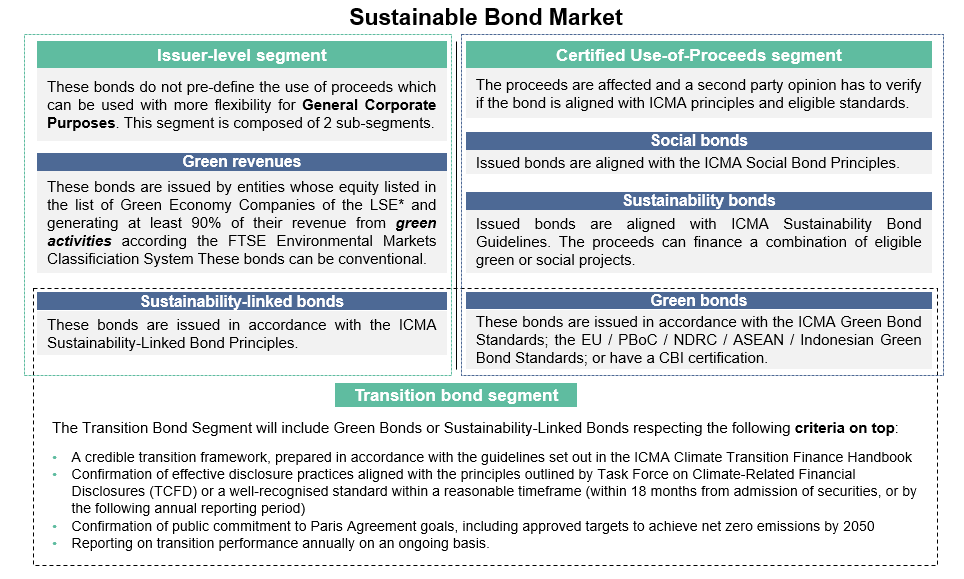

Composition of the Sustainable Bond Market Segment

The Sustainable Bond Market (SBM) is a market component within the Debt Capital Market (“Bonds”) segment [1] of the LSEG exclusively listing sustainable finance debt securities. The SBM currently lists bonds from 23 countries worth more than £56bn. The Transition Bond Segment, which remains unsolicited for the time being, is a sub-segment within the SBM alongside the Use-of-Proceeds and General Corporate Purpose segments. An investor can thus distinguish between the different sustainable debt instruments listed on the LSE and efficiently single out transition bonds.

A Dedicated Transition Bond Segment

Transition bonds can be both Use-of-Proceeds and General Corporate Purpose formats considers the LSEG. It has specified that, in essence, transition bonds can be either sustainability-linked or green bonds with specific added criteria aimed at ensuring the transition of high-emitting companies; it is an additional layer or attribute. Table 1 details the structure of the SBM.

Table 1. Structure of the London Stock Exchange Group’s Sustainable Bond Market

Source: London Stock Exchange Group, Sustainable Bond Market (SBM) Factsheet - available here

*These companies generate more than 90% of their revenue from green activities: the underlying methodology is the Green Revenues taxonomy developed by FTSE Russell (available here). As of now, 78 bonds corresponding to the Green Revenue Segment are listed. They are issued by the EBRD, Pennon Group, Severn Trent Plc, Tesco, and United Utilities Water Finance Plc.

In order for a debt instrument to be included in the transition bond segment, the issuer is expected to comply with the following requirements set out by the LSEG:

Table 2. Analysis of the four requirements needed to solicit entrance in the transition bond segment

|

LSEG Transition Bond Requirements |

Our opinion on the proposed criteria |

|

A credible transition framework (not necessarily a bond issuance framework), prepared in accordance with the guidelines set out in the ICMA Climate Transition Finance Handbook, or as measured by well-recognized market frameworks such as the Transition Pathway Initiative (TPI). |

Maintaining a substantial, sound and “science-based” [2] transition scenario is one of the core recommendations of the ICMA Climate Transition Finance Handbook. There are currently discussions about the methodologies testing the science-based feature of these transition scenarios (ACT, SBTi, TPI) and issuers are free to choose among various methodologies. Criteria are clear in theory. One wonders who will carry the assessment within the LSEG and what are the minimum requirements, for instance, what is necessary in terms of level of “management quality” when using TPI as a reference.

|

|

A confirmation of effective disclosure practices aligned with the principles outlined by Task Force on Climate-Related Financial Disclosures (TCFD) or a well-recognized standard within a reasonable timeframe (within 18 months from admission of securities, or by the following annual reporting period)

|

This requirement is mandatory to verify the credibility and effectiveness of the transition strategy. In fact, the ICMA emphasizes the importance of a quality disclosure specific to climate-related data in order for the climate transition strategy of the issuer to be credible. The TCFD is recommended as a recognized reporting framework but other frameworks are allowed (TPI or ACT). |

|

A confirmation of public commitment to Paris Agreement goals, including approved targets to achieve net zero emissions by 2050 |

The ICMA’s handbook does not involve a strict requirement for entities to be on a 2°C scenario - even though the ICMA notes that the design of the transition scenario should be “guided by the objective of limiting global temperature increases ideally to 1.5°C and, at the very least, to well below 2°C”. Consequently, the LSEG seems to set the thermometer lower than 2°C/set the bar higher/. However, the way this commitment is approved is not specified but one believes SBTi or ACT or verifiers might be solicited. |

|

A reporting of the transition performance annually on an ongoing basis. |

It is essential to assess progress and required for green and sustainability-linked bonds that are two of the forms a transition bond can potentially take. |

These requirements are essentially safeguards allowing the LSEG to identify transition bonds. Nonetheless, it is unclear whether a dedicated verifying body or team is set to be in charge of guaranteeing the criteria are fulfilled. Further the LSEG has noted that it if these criteria are not met, but supporting materials are provided, it reserves the right to include bonds in this segment on a discretionary and case-by-case basis.

The rationale behind transition bonds

According to the LSEG, transition bonds are a type of sustainable debt finance instruments serving low-carbon transition efforts and are particularly relevant for high-emitting sectors. Highly emitting companies have historically not been able to tap into dedicated / delineated sustainable finance opportunities (i.e. beyond ESG integration or some Indexes). Emphasizing the transition efforts of high emitting companies through sui generis/ad hoc filters, segments or approaches, could help such companies preserving their access to capital in the context of investors’ portfolios transition strategies (defensive approach), or even attract additional capital from investors poised to be activist from a climate change mitigation standpoint (offensive approach).

As of now, there is no agreed definition on the exact meaning of transition and transition bonds (see our transition tightrope webpage). The criteria proposed by the LSEG have some virtue as they reuse existing standards. However, temperature scenario alignment and disclosure are far from sufficient and most of the criteria required in situ and case-by-case analysis.

Table 2. Stock exchange with green, social or sustainable segments

|

Name of the Stock Exchange |

Type of dedicated section |

Launch date |

|

Oslo Stock Exchange |

Green Bonds |

January 2015 |

|

Stockholm Stock Exchange |

Sustainable Bonds |

June 2015 |

|

London Stock Exchange |

Sustainable Bond markets |

July 2015 |

|

Shanghai Stock Exchange |

Green Bonds |

March 2016 |

|

Mexico Stock Exchange |

Green Bonds |

August 2016 |

|

Luxembourg Stock Exchange |

Luxembourg Green Exchange |

September 2016 |

|

Borsa Italiana |

Green & Social Bonds |

March 2017 |

|

Taipei Exchange |

Green Bonds |

May 2017 |

|

Johannesburg |

Green Bonds |

October 2017 |

|

Japan Exchange Group |

Green & Social Bonds |

January 2018 |

|

Vienna Exchange |

Green & Social Bonds |

March 2018 |

|

Nasdaq Helsinki |

Sustainable Bonds |

May 2018 |

|

Nasdaq Copenhague |

Sustainable Bonds |

May 2018 |

|

Nasdaq Baltic |

Sustainable Bonds |

May 2018 |

|

Swiss Stock Exchange |

Green & Sustainability Bonds |

July 2018 |

|

The International Stock Exchange |

Green Bonds |

November 2018 |

|

Frankfurt Stock Exchange |

Green Bonds |

November 2018 |

|

Santiago Stock Exchange |

Green & Social Bonds |

July 2019 |

|

Moscow Exchange |

Sustainable Bonds |

August 2019 |

|

Euronext |

Green Bonds |

November 2019 |

|

Hong Kong Exchange |

Sustainable & Green Exchange |

June 2020 |

|

Singapore Stock Exchange |

Green, Social & Sustainability Bonds |

TBA |

Source: Climate Bonds Initiative, Green Bond Segments on Stock Exchanges – available here.

[1] Approximately 12,000 debt securities are listed on the London Stock Exchange.

[2] ICMA, Climate Transition Finance Handbook (December 2020) – available here