A fury of Sustainable Finance announcements in the European Union

17-minute read

In July, a multitude of legislative proposals and strategies related to sustainable finance have been announced by the European Commission and the European Central Bank:

- The renewed Sustainable Finance Strategy (6th July, European Commission);

- The European Green Bond Standard, part of the Renewed Sustainable Finance Strategy (6th July, European Commission);

- Adoption of the Delegated Act supplementing Article 8 of the Taxonomy Regulation, part of the Renewed Sustainable Finance Strategy (6th July, European Commission), see our dedicated article last month;

- Action plan to include climate change considerations in its monetary policy strategy (8th July, European Central Bank – ECB), see our dedicated article this month;

- “Fit for 55” package – 13 legislative proposals to deliver the European Green Deal (14th July, European Commission), see our detailed editorial of this month.

Some of these proposals are truly novel, while others are revisions of former legislative texts. The European Commission's “Fit for 55” legislative package is a mix of both. If they were adopted, all these initiatives would contribute to achieving the objectives of the European Green Deal by 2030 and 2050[1].

In the meantime, the European Commission has declared in a letter that it has not been able to adopt the Sustainability-related disclosures in the financial services sector (SFDR) Regulatory Technical Standards (RTS) submitted by the European Insurance and Occupational Pensions Authority (EIOPA), the European Securities and Markets Authority (ESMA) and the European Banking Authority (EBA) on 4 February 2021. Financial market participants and financial advisors will get an extra six months[2] before the SFDR RTS start applying in full.

What are the drivers and key changes brought forward by the European Commission and the ECB through these proposals? How impactful can they be? What do they require and at what time horizon?

Strategy for financing the transition to a sustainable economy

On 6 July 2021, the European Commission published a new “strategy for financing the transition to a sustainable economy”. This renewed strategy builds on the first action plan on sustainable finance adopted by the European Commission in 2018[3], as well as a report on transition finance[4] and on a consultation held from April to July 2020.

According to Valdis Dombrovskis, Executive Vice-President for an Economy that Works for People, “(…) Today's Sustainable Finance Strategy is key to generate private finance to reach our climate targets and tackle other environmental challenges. We also want to create sustainable funding opportunities for small and medium-sized companies”[5]. The renewed strategy’s purpose is to contribute to the objectives of the European green deal, by creating an enabling framework for private investors and the public sector to facilitate sustainable investments. It aims to redirect private capital flows to green investments and to embed a culture of sustainable corporate governance in the private sector.

Within the framework of the European green deal, the Commission announced a renewed sustainable finance strategy. The Sustainable Finance Action Plan launched in 2018 laid a solid foundation for transforming the European financial system with three pillars:

- The EU Taxonomy;

- A disclosure framework for non-financial and financial companies;

- Investment tools, including benchmarks, standards and labels.

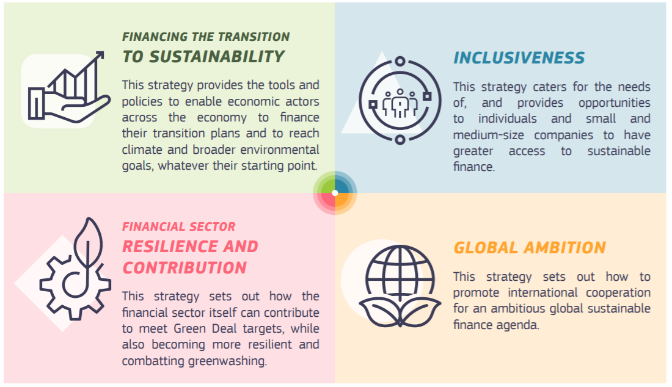

While this plan is being implemented, the European Commission recognizes that it needs to “meet the massive investment needs of the transition[6], to ensure the transition is fair and to adjust to the global context”[7]. A renewed strategy is thus needed as the global context evolved since 2018 (publication of the European Green Deal; increasing international cooperation on sustainable finance; Covid-19 pandemic; green recovery). This proposal goes further than the 2018’s action plan by identifying four new areas (see Figure 1) and six actions to achieve its sustainability objectives:

Figure 1. The new four main areas where additional actions are needed

Source: Factsheet - EU sustainable finance strategy

Table 1. Detail of the six actions to achieve sustainability objectives

|

Action 1: To develop a more comprehensive framework and help the financing of intermediary steps towards sustainability Area 1: “Financing the transition to sustainability” |

|

|

Action 2: To improve the inclusiveness of sustainable finance Area 2: “Inclusiveness” |

|

|

Action 3: Improving the financial sector’s resilience and contribution to sustainability: the double materiality perspective Area 3: “Financial sector resilience and contribution” |

|

|

Action 4: To increase the contribution of the financial sector to sustainability Area 3: “Financial sector resilience and contribution” |

|

|

Action 5: To monitor an orderly transition and ensure the integrity of the EU financial system Area 4: “Global ambition” |

|

|

Action 6: To set a high level of ambition in developing international sustainable finance initiatives and standards and to support EU partner countries Area 4: “Global ambition” |

|

Source: Annex to the Communication Report on “Strategy for Financing the Transition to a Sustainable Economy”

The renewed strategy builds on the tools created since 2018, notably the EU Taxonomy. Many topics present in this new action plan had already been announced, such as the potential creation of a brown taxonomy[9]. This would be an intermediate level of the taxonomy of green activities, which would include activities in transition towards sustainability. More generally, this renewed strategy continues to expand the scope of economic activities covered by the Taxonomy. The Commission confirmed its intention to adopt complementary delegated acts for the taxonomy to include nuclear and natural gas, two sectors that have caused much debates. The Commission will also consider proposing legislation to support the financing of certain economic activities, primarily in the energy sector, including gas, that contribute to reducing greenhouse gas emissions in a way that supports the transition towards climate neutrality throughout the current decade. However, there are some big changes:

- Scope of actors: While the 2018 action plan focused solely on financial actors, this renewed strategy includes a greater diversity of actors. This can be seen in Action 2, which extends its scope of action to citizens and SMEs, by wanting to increase “access of citizens and SMEs to sustainable finance advisory services”, or in Action 3 with the mention to credit rating agencies and supervisory authorities.

- Biodiversity: The topic has become one of the Commission's strategic priorities, with the publication of its “Biodiversity strategy for 2030” in 2020. As the mobilization of sustainable finance actors to preserve natural capital is accelerating at the international level (i.e. Taskforce on Nature-related Financial Disclosures (TFND), The International Union for Conservation of Nature (IUCN) World Conservation Congress, the Conference of the Parties to the Convention on Biological Diversity (CBD) (COP15), France’s article 29[10]), this renewed strategy aims to take up the biodiversity challenge. Specifically, the Commission will adopt another Taxonomy Delegated Act covering the remaining four environmental objectives (i.e. water, biodiversity, pollution prevention and circular economy) (1.d) ; strengthen tracking methodologies for climate and biodiversity spending and support Member States who want to redirect their national budget to green priorities (2.e); encourage the development of standards for assessing natural capital in the EU and globally; present a methodological framework and assess the potential financial risks associated with biodiversity loss and ecosystem degradation at both micro- and macro-level and explore the possible sustainable finance policy changes needed (3.e); propose to the International Platform on Sustainable Finance to expand its work to new issues, such as biodiversity (6.b).

- Greenwashing: We also note the ambition of the European Commission regarding the risks of greenwashing. Action 5.a plans to “enable supervisors to address greenwashing”, which could lead to a revision of the “supervisory and enforcement toolkit” necessary for monitoring, investigating and sanctioning greenwashing.

The Commission already achieved one of its objectives, with the publication in July of the first Draft Report of the Social Taxonomy. The platform will welcome comments on the social taxonomy and the Taxonomy extension options linked to environmental objectives from stakeholders until August 27. The final report should be published in autumn 2021.

The third pillar addresses the risks to the financial system and aims to change some of the rules for financial supervision. Given the risks that climate change poses to financial stability[11], the Commission wants to continue its work on integrating ESG risks into financial reporting and corporate accounting, working with the European Financial Reporting Advisory Group (EFRAG), its group of advisors on accounting standards, and international organizations such as the International Accounting Standards Board (IASB). As for financial institutions, the Commission is considering revising the prudential framework for banks and insurance companies so that ESG criteria are included in their risk management. Climate stress tests conducted by central banks under the ECB should also become systematic.

Transparency obligations of financial institutions on their sustainable strategy should be strengthened, to ensure that their voluntary commitments on climate objectives are credible. The Commission also wants to ask the European Insurance and Occupational Pensions Authority (EIOPA), the European insurance supervisory authority, to review the fiduciary duties of pension funds and investors. They should then better consider the impact of ESG risks in their investment decisions.

This new roadmap should lead the Commission's actions until the publication of a report on the implementation of the strategy in 2023[12]. The new strategy has already been the subject of numerous reactions, such as Reclaim Finance which regrets the absence of mandatory requirements[13]: “While the renewed strategy addresses the climate risk issue, it falls short of promoting mandatory measures that would mitigate these risks. When it comes to micro prudential regulation, the only constraints imposed on financial institutions are stress-tests, risk analysis and disclosure. These rather uncontroversial measures are a simple extension of current risk management practices”.

This strategy will now be presented to the European Parliament and the European Council. However, it is to be expected that the implementation of the ambitions of this strategy will be hampered by the negotiations.

The European Green Bond Standard

Following the 2018’s recommendation[14] of the High-Level Expert Group on sustainable finance (HLEG), the European Commission proposed on July 6, 2021, a Regulation to create the European Green Bond Standard (EUGBS). This proposal aims at creating a trusted and regulated environment for green bonds to overcome current obstacles (i.e. lack of common definitions green projects for issuers; risks of greenwashing for investors; additional costs created by the fragmentation of practices for external reviewers; insufficient standardization, transparency and supervision of external reviewers creating uncertainty and mistrust, etc.). The final goal of the EUGBS is to help the EU’s meet its environmental objectives by facilitating environmentally sustainable investments[15].

The EUGBS is designed to be compatible with existing market standards for green bonds (e.g., International Capital Market Association’s Green Bond Principles, Climate Bond Initiative’s Climate Bond Standard), but also to go further in certain key aspects:

- Avoiding greenwashing by setting a mandatory requirement for the Use of Proceeds (UoPs) to fully align with the EU Taxonomy criteria[16]. As the general rule, the UoPs should relate to activities that already meet the Taxonomy requirements or that will meet the Taxonomy-criteria within a 5-year timeline (which can be extended up to 10 years if justified and documented)

- Increasing transparency by creating a regime for the registration and supervision of external reviewers. European Green Bonds will be checked by an external reviewer to ensure that the bonds are compliant with the EUGBS Regulation, in particular the Taxonomy-alignment of the funded projects. External reviewers will be registered with the European Securities and Markets Authority (ESMA) and will need to meet the conditions for registration on an ongoing basis.

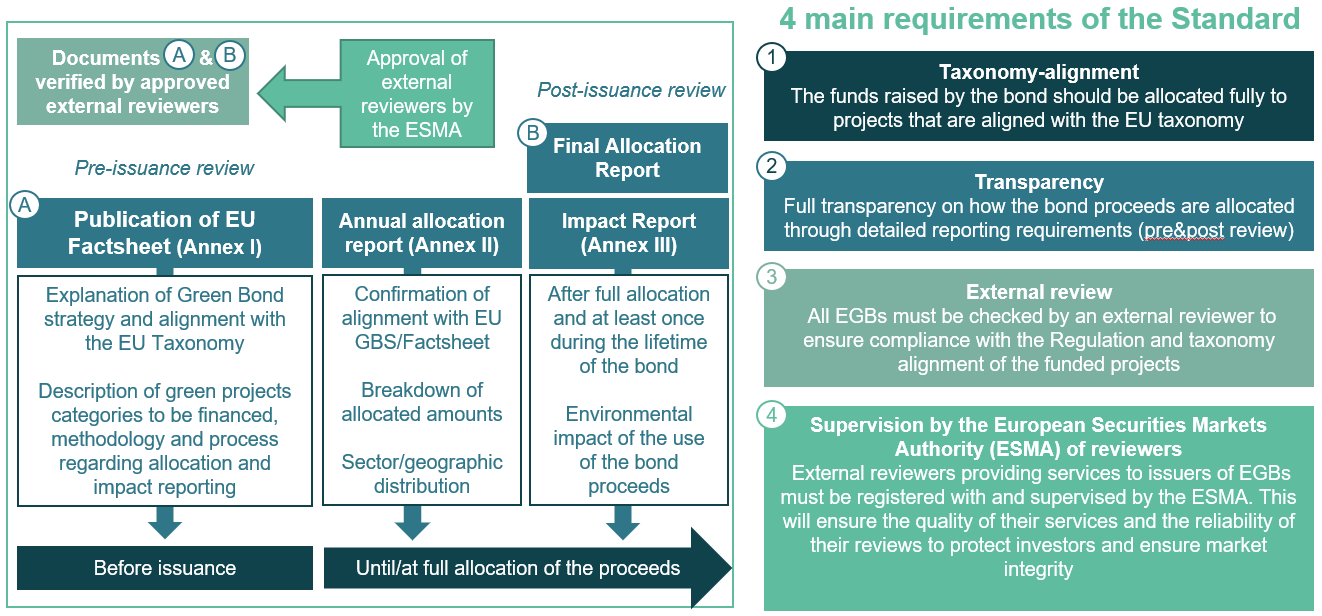

More generally, issuers will be required to draw up a “Factsheet” document (Framework) and obtain a pre-issuance external review on it, both of which need to be published on the issuer’s website prior to public offering. They will have to report annually on the allocation of proceeds until the proceeds have been fully allocated and issue an impact report at least once after the final allocation and during the lifetime of the bond; and obtain a post-issuance external review on the final allocation report (see Figure 2).

Figure 2. Schematic explanation of the EUGBS

Source: Natixis GSH

The EUGBS is intended to be a voluntary “gold standard” for green bonds. This standard will be open to all EU and non-EU issuers, including corporates, sovereigns, financial institutions, and issuers of covered bonds and asset-backed securities. Specific, limited, flexibility will be provided for sovereign issuers[17]. Concerning grandfathering, the proposal states that in the event of a change in the EU Taxonomy Technical Screening Criteria after bond issuance, issuers can make use of pre-existing criteria for five more years. If adopted[18], this Regulation has the potential to create a market of high integrity green bonds. By requiring compliance with additional stricter rules, the EUGBS establishes itself as a stronger label than existing market-based standards. This might directly benefit early adopters’ issuers, as explained by Sascha Stallberg, portfolio manager at Nordea Asset, “New innovations in the market tend to enjoy a bigger greenium in the beginning, because there’s little supply and much demand”[19]. According to the report, “the standard would provide clear advantages in terms of trust, which may translate into pricing advantages in the bond and provide a new incentive for issuers to use it. Likewise, issuers may want to demonstrate a stronger green commitment by issuing under the standard”. Finally, the proposal also anticipates two main consequences for investors and external reviewers: “Investors would be provided with a green bond segment that ensures a high degree of market integrity, transparency and comparability, and provides a common definition of green, thereby increasing comparability and trust. The initiative would provide investors with more choice and would benefit especially the most committed green investors, who value a stricter green definition. Institutional investors could clearly set themselves apart from the rest of the market by focusing their bond investments on European green bonds. External reviewers may incur additional costs if they want to comply with the standard. In addition to supervisory fees, which should be kept to a minimum for the time being, reviewers would have to incur some direct compliance”[20].

This Regulation should entry into force in more than one year[21], but is already very promising, as some organizations are already voluntarily aligning their green bond frameworks with the EU Taxonomy[22]. In addition, the UK might explore the development of its own green bond standard after the publication of the EUGBS[23].

Adoption of the Delegated Act supplementing Article 8 of the Taxonomy Regulation

On 6 July 2021, the Commission adopted the Delegated Act (DA) supplementing the Article 8 of the EU Taxonomy Regulation. It relates to the content and presentation of the information to be disclosed. It requires companies subject to the Non-Financial Reporting Directive (NFRD) to publish extra-financial information to include a non-financial statement on “how” and “to what extent” their activities relate to economic activities that qualify as environmentally sustainable under the Taxonomy Regulation (technical screening criteria, DNSH, etc.). This DA specifyies the methodology to comply with that disclosure obligation and provides several templates. For more information, see our article on the subject here.

European Central Bank’s historic pledge on climate

See our full article of this month on the subject here.

Fit for 55: : Delivering the European Green Deal

On July 14, the European Commission outlined a far-reaching legislative package to deliver on the targets agreed in the European Climate Law. This package has the potential to make the EU's policies fit for reducing CO2 emissions by at least 55% by 2030 (compared to 1990 levels). Achieving these emission reductions in the next decade is to meet the Green Deal’s objectives. The 13 proposals already define the shape of a greener Europe.

With this package, “Europe is now the very first continent that presents a comprehensive architecture to meet our climate ambitions. We have the goal, but now we present a roadmap for how we are going to get there” according to Ursula von der Leyen[24].

8 proposals are revisions of existing laws and 5 are new legislative proposals:

Table 2. Summary of directives changes proposed by the European Commission

|

Old directive |

Updates |

|

EU Emissions Trading System (EU ETS) Update available here. |

|

|

Update available here. |

|

|

Land use and forestry regulation |

|

|

Update available here. |

|

|

Update available here. |

|

|

CO₂ emission performance standards for cars and vans Update available here. |

|

|

Alternative fuels for sustainable mobility in Europe Update available here. |

|

|

Update available here. |

|

Source: Press Release – European Commission

Table 3. Summary new proposals made by the European Commission

|

New directive |

Proposals |

|

|

|

|

|

|

|

|

|

EU Forest Strategy (see here, p.30) |

|

Source: Press Release – European Commission

The publication of this holistic package with a strong emphasis on transport has already provoked numerous reactions[25]. While most stakeholders recognize the overall ambition of the measures, they are also voicing their demands, as a phase of negotiations with the Council and the Parliament begins, which should lead to changes in the initial texts. It will take months of negotiations for the 27 Member States and the Members of the European Parliament to reach a compromise, and for these proposals to be transformed into directives and other regulations with the force of law. Not to mention the lobbies that will be keen to defend their interests. Some measures, such as the Carbon Adjustment Mechanism at the borders, the creation of a second carbon market, the Social Climate Fund or the Effort Sharing Regulation will lead to tough negotiations.

Fore more information, see our dedicated editorial of this month.

[1] In April 2021, the EU has tightened its net emission target by 2030 from 40% to at least 55% compared to 1990 levels to achieve climate neutrality target by 2050.

[2] “We therefore plan to bundle all 13 of the regulatory technical standards in a single delegated act and defer the dates of application of 1 January 2022 by six months to 1 July 2022” said John Berrigan, the Director-General for Financial Stability, Financial Services and Capital Markets Union (FISMA) of the European Commission.

[3] The recommendations of the High-level expert group on sustainable finance form the basis of the action plan on sustainable finance adopted by the Commission in March 2018.

[4] See the “Transition finance report” published by the Platform on sustainable finance in March 2020, available here. More generally, the renewed strategy build up on the work done by the High Level Expert Group (HLEG) on Sustainable Finance and the Technical Expert Group on Sustainable Finance (TEG).

[5] See full quote here.

[6] Europe will need an estimated EUR 350 billion in additional investment per year over this decade to meet its 2030 emissions-reduction target in energy systems alone, alongside the EUR 130 billion it will need for other environmental goals. See p.1 of the Communication here.

[7] See p. 20 of the Communication Report, available here.

[8] See “Draft Report by Subgroup 4: Social Taxonomy”, available here.

[9] See our article here.

[10] The new Article 29 will replace the pioneering Article 173, which has required French investors to disclose their climate-related risks on a comply-or-explain basis since 2016. The notable difference is that Article 29 now requires all French financial institutions – including banks, investors and insurers – to disclose biodiversity-related risks as well as climate-related risks.

[11] See the Report published in July 2021 “Climate-related risk and financial stability” by the European Central Bank (ECB) and the European Systemic Risk Board (ESRB), available here.

[12] “The Commission will report on this strategy’s implementation by the end of 2023 and will actively support Member States in their efforts.”, see p.20 of the Communication of the Strategy for Financing the Transition to a Sustainable Economy.

[13] See Report “The EU Sustainable Finance Strategy: Repeating Past Mistakes”, available here.

[14] Establishing such a standard was a recommendation in the final report of the High-Level Expert Group on sustainable finance, see p. 30 of the Final Report here.

[15] This legislative proposal aims to better exploit the potential of the single market and the Capital Markets Union to contribute to meeting the Union’s climate and environmental objectives in accordance with Article 2(1)c of the 2016 Paris Agreement on climate change , and the European Green Deal. . Despite vigorous market growth, issuance of green bonds remains at a fraction of overall bond issuance, representing about 4 % of overall corporate bond issuance in 2020. Further growth in the market for high quality green bonds will be a source of significant green investment, thereby helping to meet the investment gap (EUR 336 billion per annum for the 2021-2030 period) of the European Green Deal, see p.1 of the proposal here.

[16] All use of bond proceeds shall relate to economic activities that make a substantial contribution to one or more of the environmental objectives, do not significantly harm any of those environmental objectives, comply with the minimum safeguards and the technical screening criteria of the Regulation, see p.26, Article 6 of the proposal, here.

[17] There are two types of flexibility proposed for sovereign issuers of European green bonds: ability to use state auditors or other public entities instead of registered external reviewers to review the allocation report (i.e. the post-issuance review), as is common practice among EU Member States already issuing green bonds (i); An exemption from having to demonstrate project-level EU Taxonomy-alignment for certain public expenditure programmes, such as funding or subsidy programmes and tax relief schemes. In those cases (for example a subsidy-scheme for home-owners to install solar panels), it will be enough for the sovereign to show that the funding programme itself is Taxonomy-aligned in its terms and conditions (ii).

[18] The Commission proposal will be submitted to the European Parliament and Council as part of the co-legislative procedure.

[19] Quote from Bloomberg’s article “EU’s Gold Standard in Green Will Command Biggest Debt Premiums”, available here.

[20] See p.9 of the proposal, here.

[21] 18 months according to the article “The proposed EU Green Bond Standard - will this transform the market for green bonds?”, from Lexology, available here.

[23] In a consultation paper, the UK Financial Conduct Authority, along HM Treasury asked “Should the FCA, alongside the Treasury, consider the development and creation of a UK bond standard, starting with green bonds?”, see p.33 here.

[24] See “Statement by President von der Leyen on delivering the European Green Deal” here.

[25] See Reuters’ article "Reactions to EU's "Fit for 55" climate plan", available here.