Verbund issues world’s first bond combining Use-of-Proceeds earmarking and KPI-linking mechanism

4-minute read

Verbund, an Austrian leading electricity company (Baa1/BBB+), has issued in March 2021 the first Bond combining both Green Use-of-Proceeds (Green Bond) and Sustainability Key Performance Indicators (Sustainability-linked Bond), called “Green and Sustainability-linked Bond”. Through a new Green Financing Framework, Verbund states it contributes to the Climate Change Mitigation environmental objective, as outlined in the April 2021 Climate Delegated Acts on the EU Taxonomy.

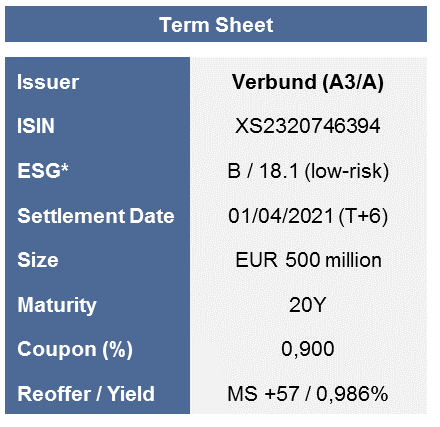

Verbund Term Sheet (*ESG Ratings (ISS-ESG / Sustainalytics))

Bond characteristics

Verbund has issued a EUR 500 million Bond with a maturity of 20 years at MS +57 bps. ISS ESG provided a second party opinion. The bond is structured with a 25bps coupon step-up from year 2033 to maturity (2041), if one of the two sustainability performance targets (SPT) is not met by December 2032. The company decided to choose the following KPIs and subsequent SPTs:

- KPI#1: Newly-installed production capacity of hydropower, wind power and photovoltaic (PV) solar renewable energy. The SPT is set at 2,000 MW by 31/12/2032 (baseline of 8,687 MW as of 31/12/2020).

- KPI#2: Additional transformer capacity to facilitate interaction with the grid and integrate renewable energy. The SPT is set at 12,000 MVA by 31/12/2032 (baseline 30,810 MVA as of 31 /12/2020).

Investors’ comments

Investors’ reaction to this innovative structure has been positive, with a book x4 oversubscribed and a price tightening by 28 bps from IPT to reoffer. The main advantage seen by market participants is the “adequacy between the Use of Proceeds (UoP) and the explicit sustainable KPIs set at the issuer level”. Moreover, the claimed alignment with the EU Taxonomy strongly encouraged the investors to participate. Meanwhile, if investors have developed internal analysis frameworks for Green Use-of-Proceeds bonds, it is not necessarily the case for Sustainability-linked Bonds yet, as it is a much more nascent market. Thereby, a Bond combining both features can more easily fall into dedicated Green Investment Portfolios than a sole SLB (see our investor survey). The combination of both formats is seen as bringing increased transparency and easier monitoring of the issuer’s sustainability achievements, rather than adding complexity.

The financial mechanism used is a coupon step-up (the one accepted for the European Central Bank eligibility, and to date the most frequent one). Yet, some market participants are not convinced about the step-up mechanism, which can be perceived as contradicting ESG investors’ philosophy. These investors have indicated a preference for alternative mechanisms such as coupon step-downs or compensation to a third party, amongst others.

What’s next ?

It is too early to make a view on whether bonds combining both UoP earmaking and KPI-linking mechanism will thrive. One wonders if it is poised to be only a sub-part of the Market, alongside Use-of-Proceeds Instruments and Sustainability-linked Instruments. Will some issuers consider the combined approach, or instead stick to one format? It is noteworthy that some issuers are currently including in their overarching framework the option to issue SLBs alongside UoP Green Bonds (e.g. Voltalia’s framework gathering both formats, although only UoP has been activated so far, see our article).

As a reminder, the Sustainability-Linked Bond format has notably emerged to overcome hurdles for issuers with limited CAPEX and/or willing to comprehensively embed their corporate startegy with a forward-looking instrument, or issuers who felt excluded from the Green Bond market to date, such as those from very GHG intensive sectors. Therefore, combining both format features is not suited to all categories of issuers. One of the stated goals to support SLB development was to lift issuance size limits while providing a holistic view an issuer’s sustainability performances. Furthermore, one of the hidden motives is also the simplicity and a less burdensome tracking and monitoring process for SLBs. However, experience is beginning to show that SLBs can also be prone to controversy, and that there is pressure and sensitivity around their design, “less meticulous work but more stress, scrutiny and pressure”.

Issuers that have developed highly-robust proceeds selection and allocation mechanisms, as well as advanced annual impact assessment processes, may prefer not to waive such expertise. For them, combining both features would unarguably send a strong message to investors, offering different and complementary lenses of analysis. For instance, we see some potential in “combined format” / “joint-format” issuances by transportation companies, utilities or real estate companies (non exhaustive list).

In our view, the pending questions are :

- Do the KPIs selected and SPTs need to be “tied” to the Use-of-Proceeds in the sense that they correspond to the impact expected to be delivered specifically by the projects and activities to which UoP are allocated? Note that in the case of Verbund, the proceeds raised are to be allocated within 3 years from the issuance, while the SPTs observation dates are twelve years after issuance.

- Should the projects commissioning date and the SPT observation dates coincide when possible?

- Can the UoP only partially (although significantly) contribute to the achievement of the SPT ?

- Should that share of contemplated contribution be disclosed (in %)?

- Should the KPI chosen be a means or output indicator focusing on areas such as capacity, effort, or overall CAPEX (as does Verbund); or rather focus on performance and impact, such as over GHG emission reductions?

- Should the impact be issuer-level (company-wide) or asset-level?

Tying the KPIs and SPTs to the impact of the Use-of-Proceeds would introduce an efficiency spending analysis angle. Indeed, 200M€ spent in renewable energy or in green buildings could result in significantly different impacts. One highlights that Verbund’s Framework states that impact reporting will include “where suitable data is available, an indication of the environmental benefits attributable to the achievement of the KPIs (e.g. tCO2e avoided as a result of meeting Verbund’s Sustainability Performance Targets)”.

Meanwhile, can we imagine bond issuances with different tranches, one being UoP - whose total amount is determined by the pool of foreseeable eligible expenses - the other being SLB. For the latter, how should the amount issued be determined? Only based on the remaining funding needs, or on another basis?

In a nutshell, this first issuance is ground-breaking. The scalability of this combined format is uncertain. It depends on market appetite and acceptance from issuers who are in position to combine both (not all sectors can do it). It raises various questions around KPIs and UoPs consistency and adequacy, or issuance size determination.