To pledge or not to pledge… Net neutrality, an international dilemma

8 - minute read

As net neutrality pledges have been multiplying in the last couple years, taking stock of what they involve is timely. One examines how robust these pledges are and the extent to which they are fraught with greenwashing.

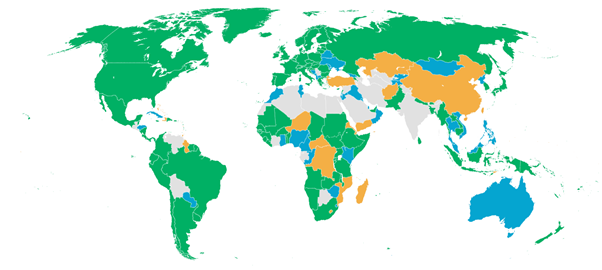

As of February 2022, the existing net zero targets stem from entities (countries, regions, cities and companies) accounting for around 88% of carbon emissions, 90% of global GDP and 85% of populations (see Figure 1 below). In comparison, in November 2019, more than 110 countries had stated their ambition to become carbon neutral between 2040 and 2060 (see our article “The global race to net-zero: what about hic et nunc decisions?”).

Figure 1: Net Zero Tracker’s database

Source: Net Zero Tracker

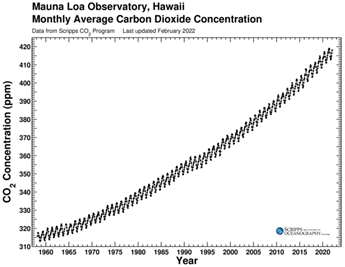

One pinpoints that at COP 26, the gap between pledges and actions has further widened (see our article, COP26 – A fragile win). Are Net Neutrality Pledges falling in the category of noncommittal and vague pledges? Quite far in time, these pledges and their implementation do not engage current leaders to take immediate action (note that a form of commitment vis-à-vis these targets is taken through the issuance of Sustainability-Linked Bonds incorporating Nationally Determined Contribution (NDC) targets, as Chile just did last February). Indeed, despite commitments proliferation, global GHG emissions are still on the rise (CO2 concentration in the atmosphere reached 418ppm in January 2022, +2.6ppm compared to January 2021).

Figure 2: Increase of CO2 at Mauna Loa [1] since pre-industrial time

Source: Global Monitoring Laboratory, Earth System Research Laboratory, Feb. 2022

The physics behind net neutrality call for semantic moderation

According to the IPCC, net zero carbon dioxide (CO2) emissions are achieved when anthropogenic CO2 emissions are balanced globally by anthropogenic CO2 removals over a specified period of time. Net Neutrality is therefore a global physical state. A company, on its perimeter, can therefore contribute to Net Neutrality but is hardly carbon neutral itself. It would make sense from a carbon accounting standpoint but not from a physical one.

However, this concept is increasingly used at national and corporate level. It is imposing itself as a mainstream standard for climate engagement. If the concept is universally shared, its interpretation varies per country and per company. It is difficult to differentiate frontrunners from laggards as comparability is hindered by the heterogeneity of claims and approaches (entity perimeter, emission scope, and role of negative emissions). The language and vocabulary must be cautiously used to prevent greenwashing (see our article this month on ADEME’s guidance around net zero claims).

To standardize net neutrality approaches, organizations such as the Science Based Target initiative (SBTi Corporate Net-Zero Standard) or Carbone 4 (Net Zero Initiative) have designed guidelines for net zero target setting.

SBTi Corporate Net-Zero Standard Carbone 4 - Net Zero Initiative

Lost in an ocean of unsubstantiated claims

Mounting pressure from civil society and international negotiations urges actors to commit on emissions reduction (COP, climate strikes, NGOs suing states and companies cf. L’affaire du Siècle in France and Shell climate ruling before the Hague Court). More than 140 countries have now set (60/140) or are considering (80/140) a target of reducing emissions to net zero by mid-century [2] (Figure 1). Although the end-goal is the same, these commitments are not equal, including among companies.

On the other hand, distant net neutrality pledges are insufficient and must be followed by immediate action. According to the International Energy Agency (IEA), “All the climate pledges made globally as of today still leave a 70% gap in the amount of emissions reductions needed by 2030 to keep 1.5 °C within reach. Governments are making bold promises for future decades, but short-term action is insufficient.” (Nov. 2021).

Initiatives and acronyms regrouping financial actors pledging to reach net zero emissions are blooming (NZBA, NZAOA, NZIA, NZAM, NZFSPA [3]). They are all regrouped under the Glasgow Financial Alliance for Net Zero (GFANZ). It currently includes over 450 financial firms across 45 countries responsible for assets of over $130 trillion. The group is working on aligning financial actors on sector-specific pathways to reach net-zero, eliminate discrepancies in pledges and build a common understanding of net neutrality and what it implies in action.

Sources: *Energy and Climate Intelligence Unit ** UNFCCC

Pledges’ shortcoming: between cherry-picking and a lack of transparency

Sovereign claims are not exempted of shortcomings

If sovereigns are fewer to have joined sustainable financial markets through Green, Social & Sustainable debt issuances (see our article on the State of the Green, Social and Sustainable Sovereign Bonds markets), they have been flooding the international community with net zero commitments, often unsubstantiated.

Indeed, only 20% of existing net zero targets meet a set of basic robustness criteria (target date, intermediary targets, action plans and regular reporting and tracking) according to The Energy & Climate Intelligence Unit and Oxford Net Zero.

As of February 2022, Climate Action Tracker assessed 23 countries’ net zero commitments (including the European Union). It found that only 4 (17%) were acceptable (rating methodology presented below) – Chile, Costa Rica, EU and United Kingdom – on a range from “poor” to “1.5°C compatible”. The same proportion was deemed either average (17%) or poor (17%). These commitments are lacking transparency and integrity as they either do not provide the information necessary nor commit on total emissions (scope 1, 2 & 3), rely on carbon offsetting or lack proper governance on the matter.

Around 60% of committing companies have set interim targets, 44% published a plan to reach their targets. It is considered reasonably high as many pledges are quite recent. Key details such as emissions scopes, the use of offsets and GHGs covered are not systematically shared. Overall, there is a lack of clarity around how countries and companies plan to get there and to which extent they rely on compensation or carbon dioxide removal (CDR).

About 11 (48%) countries were not transparent enough on their net zero commitments and provide sufficient information for a thorough analysis to be completed. It shows that net zero commitments come before reality checks and what they imply for the country in terms of measures and action plans. This is not necessarily bad as it sets a vision behind which measures can unfold, but for now, action plans remained to be seen for a large majority of net neutrality claimers.

Climate Action Tracker net zero targets assessment criteria

Another set of criteria was designed by the Climate Action Tracker – an independent scientific collaboration between Climate Analytics and NewClimate – to assess countries’ net zero pledges. It is made of ten key elements presented in the Table 3 below. Unlike the SBTi, Climate Action Tracker’s methodology does not assess the compatibility of net zero targets with limitations in temperature increase (1.5°C for example).

Figure 4: 10 key elements for net zero target setting

Source: Climate Action Tracker

Corporate net neutrality pledges are not equal in their scope, granularity and credibility:

Although the end-goal is the same, the means to reach neutrality can be quite different from an entity to another. If some of them are quite efficient (reduce inbound carbon emissions through diversification, changes in production processes and business practices), others excessively rely on yet to be developed technologies (carbon capture and storage) or compensation (carbon credits) with marginal core decarbonization.

Source: New Climate, Corporate Climate Responsability Monito 2022

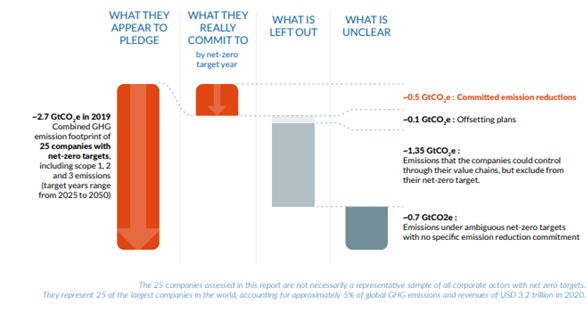

A New Climate Institute & Carbon Market watch report found that 25 major multinationals pledging to net zero actually pledged to reduce their total GHG emissions by only 20% by the time they reach their net zero deadline: by excluding scope 3 from their net zero targets, providing unprecise reduction commitments and relying on offsetting (Figure 3).

The report, titled Corporate Climate Responsibility Monitor: Assessing the Transparency and Integrity of companies’ emission reduction and net-zero targets, analyses 25 major multinationals, combining USD 3.18 trillion in revenues in 2020, 10% of the total revenue from the world’s largest 500 companies and self-reported GHG emissions footprint in 2019: 2.7GtCO2e, 5% of global GHG emissions.

Figure 3: Integrity of net zero pledges from 25 multinationals* and emissions reductions commitments

Source: New Climate Institute & Carbon Market Watch, Feb 2022

On the ambitious side, only 3/25 companies (Maersk, Vodafone and Deutsche Telekom) provide substantive core decarbonation targets above 90% of absolute emissions reduction over their entire value chains (Scope 1, 2 & 3 ) by the time they reach net zero. 5/25 less ambitious companies pledged to reduce their emissions by less than 15% by excluding scope 3 emissions of their commitments.

This is the result of cherry-picking practices (defining their own pledges boundaries: omitting scope 3 emissions) and heavy reliance on carbon offsets. Indeed, scope 3 emissions account on average for 87% of total emissions for the 25 companies assessed in this report, but only 8 of the 25 companies disclosed a moderate level of detail on their plans to address these emissions.

Rushed and partial pledges make for misleading commitments that can be a way to delay action and maintain the status quo. It shows the need for common standards and robust criteria to assess net neutrality pledges.

How to build robust pledges? Standards and criteria

Alongside with its analysis, the New Climate Institute & Carbon Market Watch [4] provided key robustness criteria to assess net neutrality pledges’ transparency and integrity:

1. Tracking and disclosing emissions:

- Disclose Scope 1, 2 & 3 GHG emissions on an annual basis with a breakdown of data to specific emissions sources

2. Setting specific and substantiated targets:

- Coverage of all scope 1, 2 & 3 GHG emissions

- Set emissions reduction targets independent from offsetting that are aligned with 1.5°C pathways

- Set interim targets aligned with the long-term vision at a maximum of 5 years from the pledge

3. Reducing emissions:

- Implement deep decarbonization measures and disclose detailed action plans

- Source energy used from highest quality low carbon energy available

4. Climate contributions and offsetting:

- Provide funds to support climate change mitigation beyond the value chain not claiming neutralization of the company’s emissions

- Avoid misleading claims and pledges by purchasing only high-quality, additional and permanent carbon offsets

There seem to be a consensus on these criteria as they are close to what the Science Based Target initiative proposes in its Corporate Net-Zero Standard and Carbone 4 in its Net Zero Initiative.

SBTi, safeguarding integrity but falling short of transparency

The Science Based Target initiative became the gold standard for corporates’ climate commitments. It is a partnership driven by four international organizations, the Carbon Disclosure Project, the World Resources Institute, the UN Global Compact and the World Wildlife Fund.

On October 28th 2021, the SBTi launched its Net-Zero standard. It intends to provide a robust standard against which to assess net-zero pledges. It also announced that it was increasing its ambition threshold for targets to be science-based. Indeed, 1.5°C-aligned targets are now the most common choice, representing 66% of all submissions to the SBTi in 2021.

On top of its science-based target setting methodology, the SBTi created a standard to assess net-zero pledges considering that all pledges were not equal nor science-based. Near term targets (5-10 years) on scope 1 and 2 emissions will have to be in line with a 1.5°C pathway (previously well-below 2°C) to be considered science-based starting July 15th, 2022. Scope 3 emissions targets should be aligned with a well-below 2°C (previously 2°C). Companies with already approved targets will be encouraged to upgrade their targets as soon as possible, and to review them within five years of target approval as per the SBTi criteria.

For a company to have their net zero pledges validated by SBTi, it must:

- Set near-term targets: commit to make rapid emissions cut in the 5-10 years to come with sector-specific or cross sector (absolute reduction of Scope 1 emissions: 4.2% p.a., Scope 3 emissions: 2.5% p.a.) targets

- Set long-term targets: commit to reduce its value chain’s emissions (scope 1, 2 & 3) by at least 90% by 2050

- Scope 3 targets (both near and long-term) are mandatory for companies for which it represents more than 40% of total emissions. Near-term Scope 3 targets must cover at least 67% of Scope 3 emissions while long-term targets must at least cover 90%

- Only a maximum of 10% of residual emissions (after reaching long term targets) can be neutralized through beyond value chain mitigation (offsetting projects outside of the company’s value chain i.e. reforestation in a country where the company has no activity whatsoever).

SBTi has recently updated its fossil fuel policy and will no longer accept commitments or validate targets from fossil fuel companies. This decision is fully aligned with science:

- In its Roadmap for the Global Energy Sector (2021), the IEA insisted that to reach a global state of net neutrality by 2050 ,“No new oil and gas levels fields approved for development”

- A 2021 study published in Nature[5] finds that nearly 60% of oil & gas reserves (2018 base) must remain unextracted to maintain a 50% probability of limiting global warming to 1.5°C by 2050.

- IPCC AR5 report on the Mitigation of Climate Change stated back in 2014: “under the constraint of stabilizing climate change at 2 °C above pre-industrial levels only a small fraction of reserves can be exploited (Meinshausen et al., 2009)”.

This standard makes it impossible for companies to cherry-pick on net neutrality. Nonetheless, if the standard is good to assess targets, it does not assess action plans to meet the targets (companies’ capital and R&D expenditures, reliance on realistic technological innovation, changes in business models and diversification).

[1] The carbon dioxide data on Mauna Loa constitute the longest record of direct measurements of CO2 in the atmosphere

[2] Net Zero Tracker, Energy and Climate Intelligence Unit, 2021

[3] Net Zero – Banking Alliance, - Asset Owner Alliance, - Insurance Alliance, - Asset Manager initiative, - Financial Service Provider Alliance

[4] Corporate Climate Responsibility Monitor : Assessing the transparency and integrity of companies’ emission reduction and net-zero targets, New Climate Institute & Carbon Market Watch, Feb 2022

[5] Unextractable fossil fuels in a 1.5 °C world, Welsby, D., Price, J., Pye, S. & Ekins, P. Nature, 2021.