The sustainable finance disclosure regulation (SFDR): enhancing clarity on sustainable investment products

7-minute read

The Sustainable Finance Disclosure Regulation (SFDR) is one of the key pillars of the European Commission’s 2018 Sustainable Finance legislative package. It came into force in December 2019 and certain key provisions are expected to apply from March 2021 onward. The Disclosure Regulation is expected to be fully applied by December 2022.

The SFDR involves transparency requirements related to ESG integration and so-called sustainable investments, which apply to all entities providing investment or insurance services within the EU. Non-EU actors – who have subsidiaries located within the EU – are also impacted by the Regulation

The Disclosure Regulation arose from the need to improve industry-wide comparability and prevent greenwashing. It improves market transparency from financial market participants (FMPs) and financial advisers (FAs), as they will be required to provide investors with periodic information.

The new regime impacts both product and entity levels. At the product level, the classification is divided into several ESG categories, among which, articles 8 and 9:

Art 8: Transparency of the promotion of environmental or social characteristics in pre‐contractual disclosures: this article concerns products that promote environmental or social characteristics. For example, products with an exclusion investment strategy.

Art 9: Transparency of sustainable investments in pre‐contractual disclosures: it applies to products that have sustainable investments as underlying. Those investments must have an environmental or social objective: they must not harm the other objective and use minimum governance standards (e.g. impact funds).

Table 1. Overview of the SFDR disclosure requirements at both product and entity levels

At the product level, the Regulation requires financial market participants (FMPs) and financial advisers (FAs) to disclose their policies regarding the consideration of principal adverse impacts (PAI) of investment decisions on sustainability factors. Adverse impacts are then defined as “an entity's negative impact on environmental and social issues”. In order to measure this, the European Supervisory Authorities (ESAs) identified 50 environmental and social indicators, on which 32 mandatory and 18 optional (see the exhaustive list of indicators in the appendix).

RTS on SFDR: Level 2 measures have been postponed, and mandatory Principal Adverse Impact (PAI) indicators were reviewed.

As with many EU Regulations, the SFDR requires a detailed Regulatory Technical Standard (RTS) - Level 2, to be published before market participants have a complete picture of how the legislation is intended to be applied. As a result, in February 2021, the three European Supervisory Authorities (EBA, EIOPA and ESMA) have published their final report about the regulatory technical standards on the SFDR[1].

While financial market participants and financial advisers are still required to comply with the SFDR level 1 provisions from March 2021, the application of the RTS was delayed to a later date as specified by the European Commission in a letter addressed to the ESAs in October 2020[2].

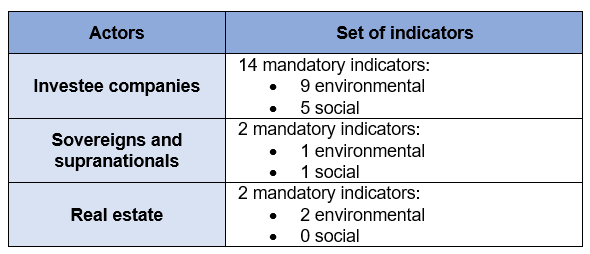

In addition, some changes have been made in the final draft. At the product level, the European Supervisory Authorities have introduced of a mixed type product where only part of the investment is sustainable. At the entity level, they limited the number of principle adverse impacts (PIA) indicators on which Financial Market Participants (FMPs) must report upon. From the 32 mandatory adverse impact indicators, the final draft came down to a shortlist of 18 mandatory indicators. Most social-based indicators are no longer mandatory.[3] The adverse impact indicators were also divided into the following three categories:

Table 2. Overview of the adverse impact indicators after RTS - Level 2

Natixis’ remarks and conclusion

In overall, we welcome the initiative of disclosing common and standardized data on the sustainable activities of financial market participants. Suchlike disclosures are useful when making investment decisions, allowing for enhanced insight on the environmental and social impacts of the entity managing or selling the product, along with information about the product itself.

However, as the SFDR just applies to certain actors, we believe that it might create an unlevel playing field, as some non-EU players might benefit from lighter requirements while still selling products to European investors. This raises the competitive (dis)advantage issue: Firstly, due to the integrated nature of the financial system, the first financial market participant able to provide the market an outline of the PAI assessment on each indicator will get a considerable competitive advantage. Secondly, due to the significant reporting costs the implementation of the draft RTS would entail, the European Regulation is implicitly pushing smaller players to either stay below the 500-employee threshold set by SFDR or relocate their activities outside the EU. Indeed, financial institutions located outside the EU but marketing products within the EU (example of an US asset manager marketing a fund registered in the EU) will not be subject to the entity level reporting, unlike European players. Such an unlevel playing field raises a significant risk for the production and distribution of investment products in the EU.

Regarding the reporting data chain: The reporting requirements apply to financial institutions that have diverging roles in the reporting chain, which creates additional challenges due to the lack of data availability. Indeed, financial institutions have different roles depending on their position in the supply chain: manufacturers or distributors subject to the SFDR, but some manufacturers not subject to SFDR can also be part of the reporting data chain since they sell their products to distributors subject to SFDR.

The indicators proposed are not aligned with existing legislations: The list of indicators proposed by the ESAs is not based on any widely accepted non-financial reporting standard, which creates a significant issue regarding data availability. We provide in the appendix our opinion about each of the 50 indicators proposed in the draft RTS (April 2020) both in terms of data availability and in terms of relevancy from an ESG perspective.

Lack of clarity regarding the definition of ESG products: While SFDR establishes 2 categories of ESG products (defined in Articles 8 and 9 SFDR), the classification of existing products into those categories is the responsibility of each financial institution. No explicit guidelines have been issued by European authorities to help market players do this job, while the definition of both products remain blurred. While market participants are debating together to define the market

Implementation deadline: In its recent letter to the European Supervisory Authorities[4], the EU Commission has made clear that it will not accept delays on the general application deadlines of the SFDR- Level 1 that will be implemented next month. Is now time for the Financial Market Participants and Financial Advisers to start adapting to the Level 1 of the new regulation.

TO GO FURTHER

[1] ESMA, Final Report on draft Regulatory Technical Standards (February 2021) - available here

[2] European Commission, letter to the European Supervisory Authorities on sustainability-related disclosures in the financial services sector (October 2020) - available here.

[3] Responsible Investor, an overview of the new reporting indicators: "EU regulators cut number of mandatory reporting indicators in final SFDR draft" (February 2021) - available here

[4] See European Commission, letter to the European Supervisory Authorities on sustainability-related disclosures in the financial services sector - available here.