Mounting political momentum for carbon markets

6-minute read

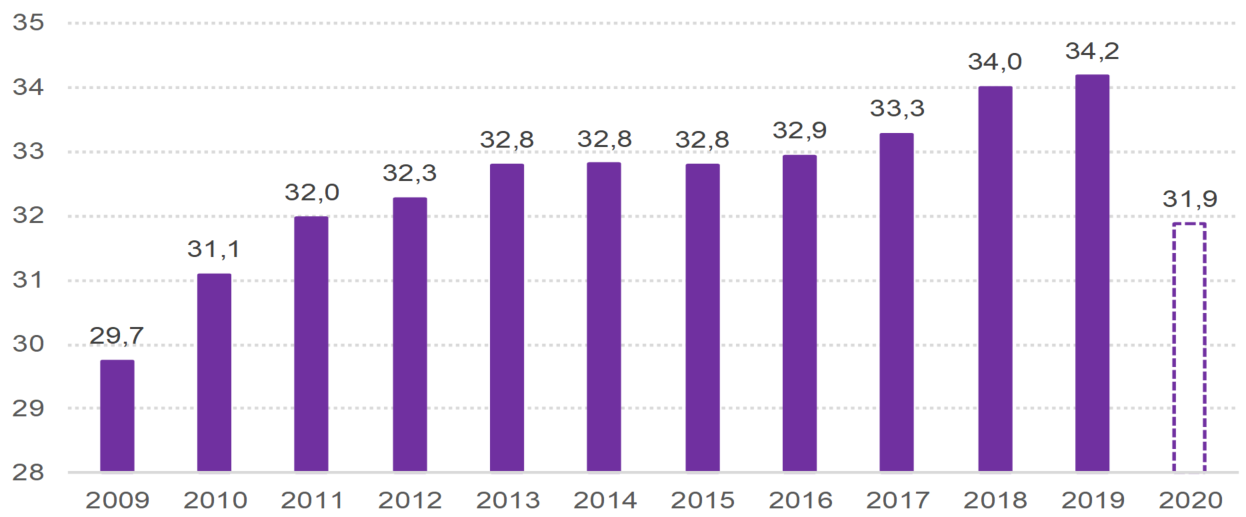

Despite the decline observed in 2020 in an unprecedented context of a global health crisis, the levels of worldwide CO2 emissions still represent a considerable challenge in the fight against climate change. Indeed, CO2 emissions dropping by some 6% in 2020 according to preliminary estimates cannot overshadow the upward trend observed since 2009 (see chart below). This trend must itself be analyzed in light of the trajectory of carbon emissions necessary to achieve the objectives set by the Paris Agreement of December 2015. Let’s recall this agreement sets the objectives of “holding the increase in the global average temperature to well below 2° Celsius above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5° Celsius above pre-industrial levels”. Such targets entail reaching carbon emissions neutrality around 2050 followed by negative emissions thereafter.

Table 1. Trend in worldwide carbon emissions (2009-2020 - GtCO2)

Sources: BP, Nature.com

It is against such backdrop that the last six months saw three significant political developments on the front of the fight against climate change:

- The return of the United States to the Paris Agreement following the election of Joe Biden (see our editorial this month)

- The announcement by China of an ambition climate neutrality by 2060 (see our recent article on countries’ neutrality targets)

- The increase by the EU of its greenhouse gas reduction target by 2030 (-55% vs. -40% previously from 1990 levels).

Sign of a reinforced consensus around the urgency of climate action, these developments have already been followed (China) or should be followed (EU) by initiatives in the field of carbon markets, these schemes remaining for the moment confined to the regional scale in the United States.

China’s carbon market: a lenient, benchmark-based scheme covering power producers… for the time being

In early February 2021, China introduced a national carbon emissions trading market for the electricity sector. This market concerns 2,225 installations across China with annual emissions of at least 26,000 tCO2 or 10,000 tons of standard coal equivalent energy consumption. It operates on the basis of a benchmark of 877 kg CO2/MWh for standard coal plants over 300 MW and 979 kg CO2/MWh for standard coal plants below 300 MW. For less common plants that burn coal gangue and coal water slurry, the benchmark is 1,146 kg CO2/MWh, while for gas-fired plants it is 392 kg CO2/MWh. Under the scheme, China’s power operators will have to buy emissions permits if their plant exceeds these carbon intensity benchmarks.

The entry into force of this carbon cap-and-trade marks a new stage in China's climate policy. In fact, the limitation of this market to the power generation sector alone should only be temporary, with the probable (in a still undetermined time horizon) inclusion of carbon-intensive industrial sectors (refining, steel production, chemicals). However, it is unlikely that in its current form, the market will severely penalize utilities and, above all, guide investments in new generation capacities outside of coal. China, which depended on this fossil fuel for 65% of its electricity production in 2019, does not intend to phase out from coal in a foreseeable future, on the model of the policy currently pursued in Germany. Characteristically, approvals for new coal projects in China increased in 2020 with plans for 40.8 GW of new coal plants - equivalent to the entire coal generation fleet of South Africa - being proposed in the sole H1. In this perspective, the definition of emissions benchmarks would serve mainly to orient investments in the electricity sector towards the most efficient coal capacities from a thermal point of view. For instance, new, “ultra-supercritical” coal-fired plants achieve a net thermal efficiency of around 48% with induced CO2 emissions of 700 kg CO2/MWh, to compare with old coal-fired plants displaying much lower efficiency rates (circa 38%) and accordingly much higher carbon intensities (circa 900 kg CO2/MWh).

Observers nonetheless point to the scheme offering a working basis to go much further in decarbonizing the Chinese economy, starting with the electricity sector before extending to the aforementioned CO2-intensive industrial activities.

EU ETS: more stringent rules expected under phase 4 to reflect revised emissions reductions targets

On the EU side, the recent upward revision of intermediate decarbonization target by 2030 should lead to significant changes in the operating rules of the community market, the European Trading Scheme (ETS, which at the beginning of the year entered phase 4.

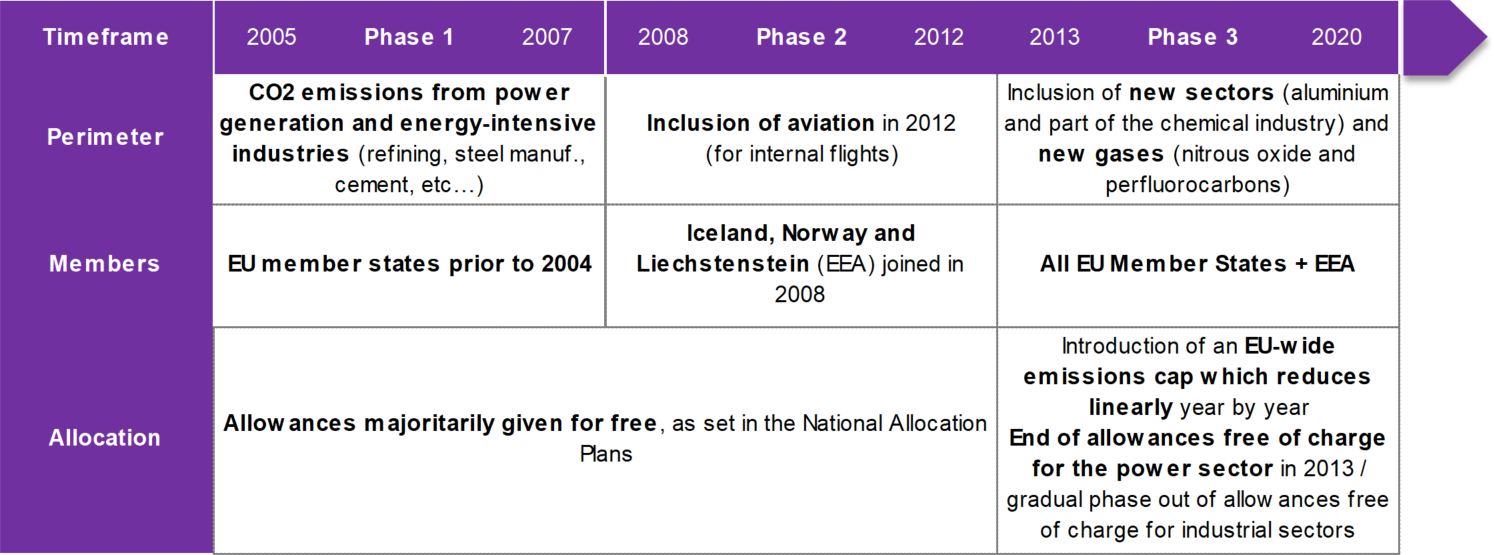

Set up in 2005, the EU ETS was until the start of this month the world's first international emissions trading system. Since inception, its primary vocation has been to enable the EU to reduce its greenhouse gas emissions (-40% reduction targeted by 2030 from 1990 levels until December 2020, now -55% from the same base levels) and, in so doing, help Europe progress towards carbon neutrality by 2050.

Since inception in 2005, the EU ETS has undergone various transformations aimed at enlarging the scope of emissions covered and favoring the emergence of carbon price signals incentivizing the use of the least CO2-intensive technologies and processes, this through:

i. The gradual enlargement of the EU ETS’ scope, resulting in 45% of EU’s carbon emissions now being covered by the scheme, but more importantly

ii. The introduction in 2013 of an EU-wide emissions cap which reduces linearly (1.74% p.a. until 2021, 2.1% p.a. thereafter) and the concomitant introduction of explicit auctions at national level for the allocation of carbon allowances.

Table 2. Main changes introduced in the EU ETS since its entry into force in 2005

Source: I4CE, Natixis

That being said, a clear distinction has to be drawn for the time being between the power generation sector, on the one hand, which must cover all of its emissions by purchasing allowances put up for auction and, on the other hand, industrial sectors exposed to a risk of relocation in the event of an excessive increase in the carbon constraint ("carbon leakage"). These sectors (steel, cement, glass, chemicals, pulp and paper, etc.) still continue to receive free allowances covering the major part of their CO2 emissions. However, it should be noted (see below) that this system of free allocation of quotas is doomed to gradual extinction throughout phase 4 (2021-2030).

While gradually amending the ETS to make it suitable for serving the EU's decarbonization targets, EU decision-makers also had to cope with the impact of the market oversupply which developed as a result of the 2009 economic crisis (allocation of allowances in 2009 based on an incorrect GDP growth scenario, EU's economy contracting by 5% that year).

A series of measures were announced at the end of 2017 with the aim of bringing down excess allowances from over 1,700 tCO2 at year end-2017 to less than 0.8 t tCO2 by year-end 2030, namely:

i. The linear EUA reduction factor will be 2.2 % from 2021 (vs. 1.74% previously), as proposed by the European Commission (EC);

ii. Each year from 2019 to 2023, 24% of the cumulative surplus of allowances will go to the Market Stability Reserve (MSR); from 2023 the allowances held in the reserve above the total number of allowances auctioned during the previous year should be cancelled;

iii. Conditional lowering of the auction share by 3% of the total quantity if needed, to avoid application of the cross-sectoral correction factor (this is between the 5 % proposed by Parliament and 2 % proposed by Council).

These measures were instrumental in partially rebalancing the market but more importantly in restoring ETS’ perceived ability to play a meaningful role in the EU economy’s decarbonization. These elements account for the spectacular rise in carbon prices throughout 2018, from €7/t in January to €25/t in September, and then for EU carbon allowances trading on average at €26/t over the past two years (see chart below). Such trend is all the more remarkable considering the various sources of uncertainty market players have had to face over the past two years (timing and implications of the Brexit on the EU ETS, impact on the sanitary and economic crisis on the supply-demand balance, etc.).

Table 3. EU ETS: trend in carbon allowance price (€/t) since 2017

Source: Bloomberg

The abovementioned measures announced at the end of 2017 to rebalance the EU ETS were part of a general market design aiming to achieve a 40% cut in greenhouse gas emissions by 2030 from 1990 levels. Rules governing ETS phase 4 which entered into force last January 1 therefore need to align with the -55% cut in greenhouse gas emissions now targeted by 2030.

It is against such backdrop that the EC launched last fall a public consultation with a view to adapting the ETS to EU’s new decarbonization objective for 2030. The EC is scheduled to present legislative proposals in the summer. Some changes will likely be enacted sooner than others, experts say, in order to give European industry as much time as possible to adjust to the new emissions limits before 2030 arrives.

The considered changes go in three main directions:

i. Inclusion of new sector in the ETS. The EC wants to add emissions from intra-EU shipping, while also considering inclusions of sectors such as buildings, road transport, as well as potentially all fossil fuel-burning activities. Alternatively, the consultation says these sectors could be covered by a new ETS, possibly linked to the existing scheme.

ii. Fewer free allowances. The EC considers accelerating the reduction of the volumes of free allowances to sectors subject to the carbon leakage risk. Furthermore, free allowances could be “replaced” by the EU’s plan to impose carbon cost on imported goods in some of the sectors subject to the carbon leakage risk (through the considered carbon border adjustment mechanism- CBAM ), or only given to companies that invest in emissions cuts.

iii. Supply cuts. Such cuts could be implemented through various channels, namely faster cap cuts than the -2.2% p.a. agreed on in 2017 and/or more aggressive use of the MSR (see above) that is currently used to gradually reduce the volume of excess allowances by removing from the market a fixed portion of total permits put up for auction (currently 24% p.a. up until 2023). Another option considered by the EC is the mandatory cancellation of allowances pertaining to polluting power plants upon closure.

One may therefore expect a growing scarcity of available emission allowances and an extension of the scheme to other carbon-intensive sectors (road transport) from forthcoming legislative proposals from the EC. We believe they are inevitable in order to allow the EU to take a step forward in its decarbonization journey, this by promoting, via relevant carbon price signals, the transformation of sectors such as transport and industry which are still very dependent on fossil fuels. These elements are the basis of the anticipation — now consensual — of a markedly upward trajectory in carbon allowance prices in Europe until 2030 (from € 40/t today to possibly €60- €90/t in 10 years from now).

TO GO FURTHER