The European Commission adopts an ambitious Sustainable Finance package including the long-awaited Taxonomy Delegated Acts

9-minute read

On April 21, the European Commission ratified the EU Climate Law Regulation [1], setting a legally binding goal to cut GHG emissions by at least 55% [2] by 2030 compared to 1990 levels. The same day, the Commission adopted [3] an ambitious and comprehensive set of measures. It is comprised of the long-awaited EU Taxonomy Climate Delegated Acts [4], including climate mitigation and climate adaptation technical screening criteria, a proposal for a Corporate Sustainability Reporting Directive (replacing the Non-Financial Reporting Directive), and six amending Delegated Acts to ensure that financial firms, such as advisers, asset managers and insurers, include sustainability in their procedures and their investment advice to clients. This set of measures represents a key milestone for the European Green Deal, forasmuch as it creates a comprehensive sustainability framework that seeks to alter companies’ business models accordingly and ultimately prevent greenwashing.

The EU Taxonomy Climate Change Delegated Acts

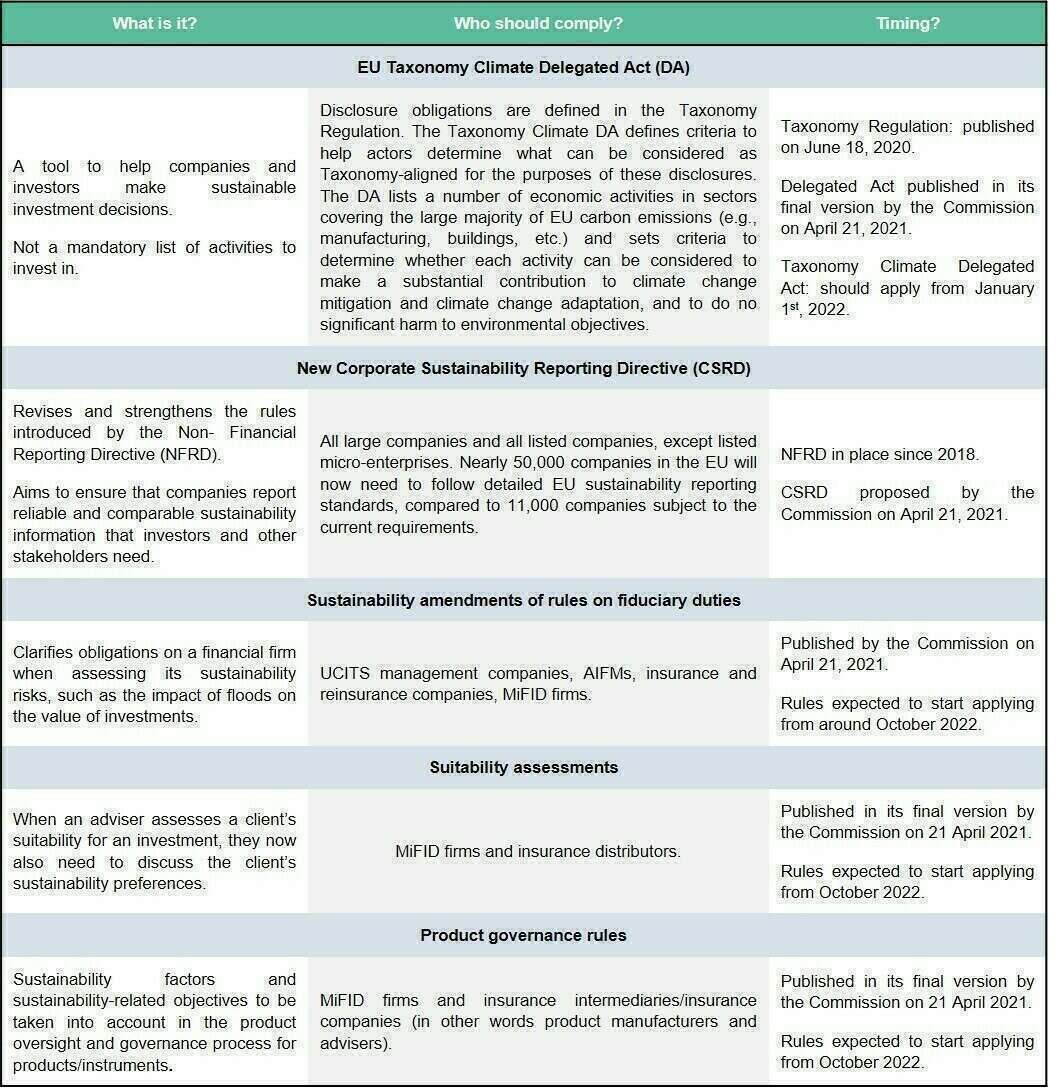

The EU Taxonomy Climate delegated acts serve as a legal text that delivers the first set of technical screening criteria (TSC) under which specific economic activities should qualify as contributing substantially to climate change mitigation and adaptation. It also defines the do-no-significant harm criteria (DNSH) regarding the other Taxonomy environmnental objectives that are:

- Sustainable use and protection of water and marine resources

- Transition to a circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems

These remaining criteria are imperative, as activities need to be within the aforementioned criteria as well as respect social minimum safeguards to be considered sustainable. The activities and criteria are based on the recommendations of the Technical Expert Group (TEG), which has been replaced by the Platform on Sustainable Finance and following public feedback.

The European Commission estimates these Delegated Acts to cover the economic activities of roughly 40% of EU-based listed companies, in sectors which are responsible for almost 80% of direct greenhouse gas emissions in Europe.

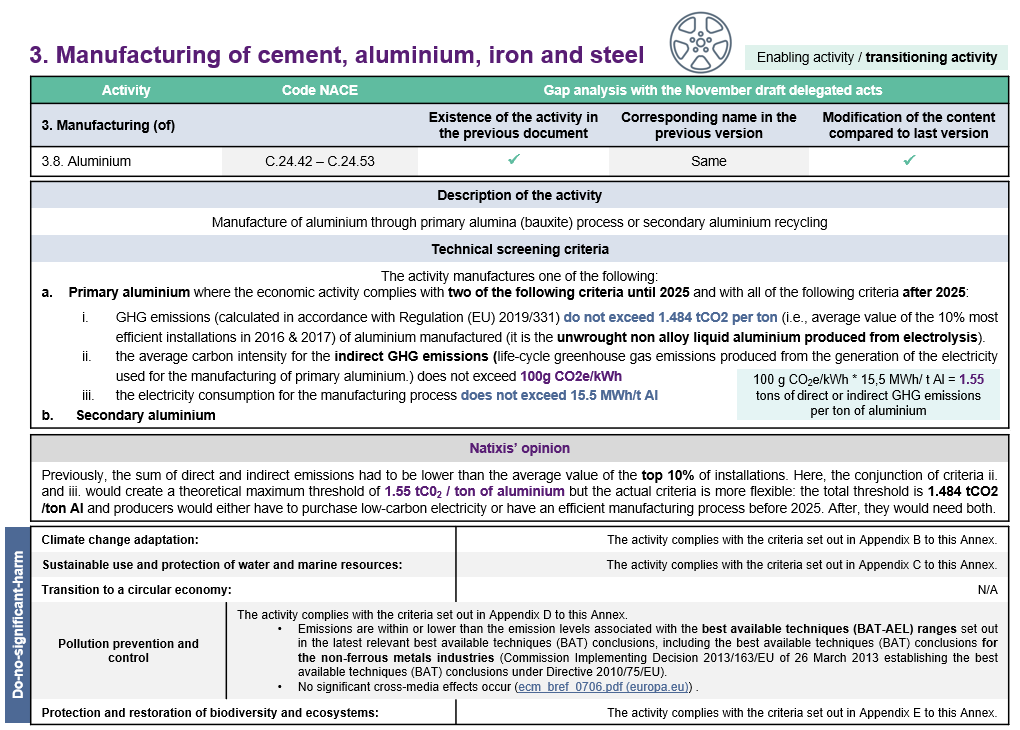

As of today the Climate Change Delegated Acts cover 88 economic activities. Technical screening criteria are alternatively set:

- as a quantitative threshold or minimum requirement,

- as a relative improvement,

- as a set of qualitative performance requirements,

- as process or practice-based requirements,

- as a precise description of the nature of the economic activity itself where that activity by its nature can contribute substantially to climate change mitigation.

All the indicators required by the Article 8 of the EU Taxonomy to be reported by entities falling within the scope of the CSRD (see explanations below about its scope of application) will be specified in a separate delegated act. Entities not yet complying with any technical screening criteria would be allowed to count the expenditure (CAPEX and relevant OPEX) of their investment plan to achieve compliance as Taxonomy-aligned.

[1] Regulation (EU) 2020/0036(COD) of the European parliament and of the council establishing the framework for achieving climate neutrality and amending Regulation (EU) 2018/1999 (European Climate Law). [2] The bloc as a whole will cut GHG emissions by at least 55% by 2030 compare with 1990 levels, meaning individual member countries’ targets will vary, taking into account different socio-economic situations. As a reminder greenhouse gas emission in the EU-27 decreased by 24 % between 1990 and 2019, exceeding the target of a 20 % reduction from 1990 levels by 2020 (EEA). [3] The Delegated Act will be formally adopted at the end of May once translations are available in all EU languages. [4] The draft version was released in November 2020 and was initially planned to be adopted before the end of last year. For more information please refer to our article published in the November’s newsletter.

Figure 1. Example of activity assessment criteria spreadsheet by Natixis

The EU Taxonomy Delegated Acts are a set of “living” documents and will be subject to regular review to properly evolve over time to include developments and technological progress. As such, the European Commission gives stakeholders the possibility to suggest activities that are to be potentially included in the criteria via a web portal, which will be established in mid-2021 on the European Commission’s website. This will ensure that new sectors and activities, including transitional and other enabling activities, can be added in the scope of the EU Taxonomy over time.

Changes compared to the latest version

Compared to the draft release in November 2020, the final version of the Climate Delegated Acts has had some criteria eased. These included the criteria to produce hydrogen [5], and the construction [6] and acquisition [7] of building. For electricity generation from hydropower, the mention “electricity generation facility is a run-of river plant and does not have an artificial reservoir” has been added. For some specific manufacture activities [8], the use of EU emissions trading scheme (ETS) benchmarks [9] is confirmed, in the absence of objective alternatives to ensure environmental ambition. However, the main points to be highlighted remain the removal of the criteria for agriculture [10] and natural gas [11] as an energy source, while nuclear activities remain out of this set of criteria. As a reminder, agriculture and natural gas were included in the November draft version.

The EU Commission has decided to delay the inclusion of the agricultural sector until the next Delegated Act before the end of the year 2021 due to the current negotiation to define the common agricultural policy. Natural gas activities fulfilling the transitional activities requirements will be included in a future Delegated Act. For nuclear energy, assessment is still ongoing [12] and, as soon as the dedicated process is complete, the Commission will follow up based on its results in the context of this Regulation.

As a reminder, the technical screening criteria for the other four environmental objectives —sustainable use and protection of water and marine resources; transition to a circular economy, waste prevention and recycling; pollution prevention and control and protection of healthy ecosystems — will be published by the end of 2021 and are currently being designed by the Platform on Sustainable Finance.

Once formally adopted, the EU Taxonomy Climate Delegated Acts will be scrutinized by the European Parliament and the Council for four months (extendable once by two additional months).

Social taxonomy

Moreover, the Platform is expected to release a report on social objectives extending the current taxonomy by Q2 2021. The EU taxonomy is set to be expanded in order to encompass activities supporting the EU’s social objectives. In February, the European Commission has unveiled its Social Taxonomy Outreach presentation on the platform on sustainable finance.

The proposed structure is composed of 3 pillars:

- Respect for human rights: Impacts on workers, consumers, and communities

- Governance: Responsible lobbying and anti-corruption measures, and transparent and non-aggressive tax planning

- Promote Adequate living conditions for all: The fulfilment of basic human needs, including access to essential economic services and infrastructure, decent employment, and the promotion of peaceful and inclusive societies

A proposal for a Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive revises and strengthens the existing rules introduced by the Non-Financial Reporting Directive (NFRD) aiming to improve the flow of sustainability information to be disclosed by companies. Suchlike disclosure includes how climate change affects their business operations, and the impact of their activities on people and the environment. The CSRD has an objective to bring a similar level of assurance for financial and sustainability reporting by introducing a general EU-wide audit requirement for reported sustainability information.

This new directive extends to all large [13] and listed companies the need for a sustainability report, increasing the number of entities involved from approximately 11,000 to nearly 50,000. To ease its implementation, the Commission proposes the development of reporting standards depending on the company’s size. The European Financial Reporting Advisory Group (EFRAG) will be responsible for developing these draft standards. It will enhance the consistency of corporate sustainability reporting so as to guarantee that financial firms, investors, and the broader public can use comparable and reliable sustainability information.

Regarding the CSRD Proposal, the Commission will engage in discussions with the European Parliament and Council to negotiate a final legislative text based on the Commission's proposal. If the negotiations go well, companies could apply these new reporting standards for the first time to reports published in 2024, covering financial year 2023.

Amendment to Delegated Acts on investor duties and investment advice

The EU released several Delegated Acts to amend existing rules on investor duties and investment advice to incorporate sustainability. These amendments are also a progress to fight against greenwashing.

- On investment and insurance advice: when an adviser assesses a client's suitability for an investment, they now need to discuss the client's sustainability preferences: the qualification of those preferences are determined by the new text.

- On fiduciary duties: amendments clarify the obligations of a financial firm when assessing its sustainability risks, such as the impact of floods on the value of investments.

- On investment and insurance product oversight and governance: manufacturers of financial products and financial advisers will need to consider sustainability factors when designing their financial products.

These amendments will be scrutinized by both the European Parliament and the Council for a three-month period and extendable once by three additional months. They are expected to apply as of October 2022.

[5] The activity complies with the life-cycle GHG emissions savings requirement of 73.4% (versus 80% previously) for hydrogen [resulting in 3tCO2eq/tH2 (versus 2.256 t CO2eq/tH2 previously)] and 70% for hydrogen-based synthetic fuels relative to a fossil fuel comparator of 94g CO2e/MJ. [6] The Primary Energy Demand (PED), defining the energy performance of the building resulting from the construction, is at least 10% lower (versus 20% previously) than the threshold set for the nearly zero-energy building (NZEB). [7] For buildings built before 31 December 2020, the building has at least an Energy Performance Certificate (EPC) class A. As an alternative, the building is within the top 15% of the national or regional building stock expressed as operational Primary Energy Demand (PED) (The last sentence has been added). [8] Manufacture of cement/ aluminium/ iron and steel/ carbon black/ soda ash/ chlorine/ organic basic chemicals/ nitic acid. [9] The technologies, products or other solutions either enable the target activities to be carried out with substantially lower GHG emission, which aim at a 30% reduction compared to the relevant EU ETS benchmark or the average value of the 10% most efficient installations in 2016 and 2017 (t CO2 equivalents/t) as set out in the Annex to the Implementing Regulation (EU) 2021/447. [10] The previous version contained three categories relating to agriculture – growing perennial crops, growing non-perennial crops, and livestock. [11] The November draft version mentioned the electricity generation and the cogeneration of heat/cool and power from gaseous and liquid fuels including natural gas complying with the Taxonomy’s key thresholds: a low threshold (100gCO2/kWh) below which energy generation technologies are considered “sustainable”. The higher threshold, (270gCO2/kWh) determines energy technologies which are deemed to make “significant harm” to the environment. [12] In June 2019, the TEG was unable to reach a definitive conclusion on potential significant harm to other environmental objectives. In 2020, the EU Joint Research Center JRC started a review to assess nuclear energy generation under the “do no significant harm” (DNSH) criteria. It analyzed the effects of the whole nuclear energy life-cycle in terms of existing and potential environmental impacts across all the taxonomy environmental objectives, with emphasis on the management of the generated nuclear and radioactive waste. In March 2021, the JRC published a report concluding that the fuel can be deemed as sustainable. It reads: “The analyses did not reveal any science-based evidence that nuclear energy does more harm to human health or to the environment than other electricity production technologies already included in the Taxonomy as activities supporting climate change mitigation”. [13] Large companies are defined in the Accounting Directive as those with more than 250 employees rather than the NFRD threshold of 500. Large undertakings shall be undertakings which on their balance sheet dates exceed at least two of the three following criteria: (a) balance sheet total: EUR 20 000 000 ;(b) net turnover: EUR 40,000,000 ; (c) average number of employees during the financial year: 250.

The detailed April package

Table 1: In more detail the April package, © European Union, 2021

Five members of the Platform on Sustainable Finance step down in protest

Just a few hours after the adoption of the EU sustainable finance package, five members [14], out of 57, of the Platform on Sustainable Finance (PSF) have decided to step down. They protested at the European Commission’s decision to classify some highly emitting businesses such as “dirty cargo ships”, “gas buses”, and “logging and burning trees”, as sustainable investments. They all have suspended their involvement in the PSF platform and call other members do to so as well. These members accuse politicians and lobbies of interfering in the debates to water down the recommendations made by the Technical Expert Group (TEG) on Sustainable Finance. They have declared they will not return to the process until the Commission returns to science.

The associations also intend to protest at the opaque decision-making process. Most of the participant in the Platform were informed that many of the criteria proposed by the TEG had been removed through leaks in the press. The PSF’s Chairman Nathan Fabian proposed that the Commission inform its members of the criteria selected and justify them when they from their proposals. They are now awaiting the Commission's response.

[14] Transport & Environment, WWF European Policy Office, BirdLife Europe and Central Asia, the Bureau Européen des Unions de Consommateurs (BEUC), and ECO