TEG 101 - EU Climate Benchmarks

Natixis Green & Sustainable Hub is delighted to share with you its EU Climate Benchmarks special report: “Reality and consistency check”

Published on September 30th, the EU TEG Report on Benchmarks defined minimum technical criteria for the newly created EU Climate Benchmarks, as well as ESG disclosure requirements for all benchmarks.

Less under the spotlight than the EU Taxonomy and Green Bond standard, EU Climate Benchmarks represent nevertheless a major milestone for sustainable capital markets as they should bring more clarity and homogeneity in the climate/low carbon indices universe. Two climate benchmarks have been created: Climate Transition and Paris-Aligned benchmarks, with similar objectives but different levels of ambition.

- What does Paris Alignment mean at a portfolio level?

- Are proposed criteria usable for investors? Why, how, under which conditions?

- Reality check: are existing major climate indices (MSCI, Euronext) compliant with those criteria?

Our report intends to address those questions by providing in-depth analysis of EU requirements and highlighting their implications for market players.

This report is a third our TEG 101 and follows our EU Taxonomy and EU Green Bond Standard reports.

All you need to know about EU Climate Benchmarks

1. What are EU Climate benchmarks?

A benchmark means any index by reference to which the amount payable under a financial instrument or a financial contract, or the value of a financial instrument, is determined.

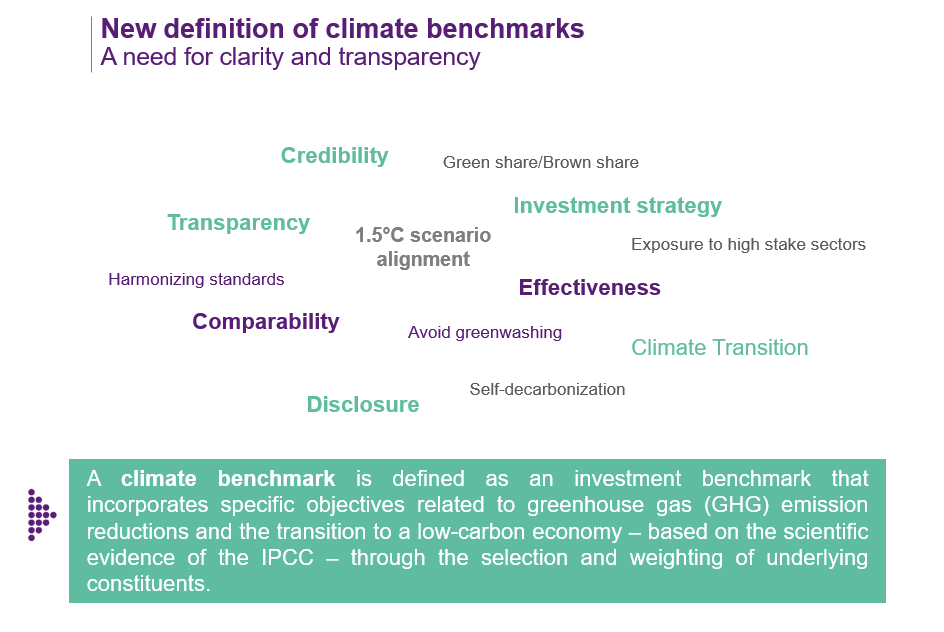

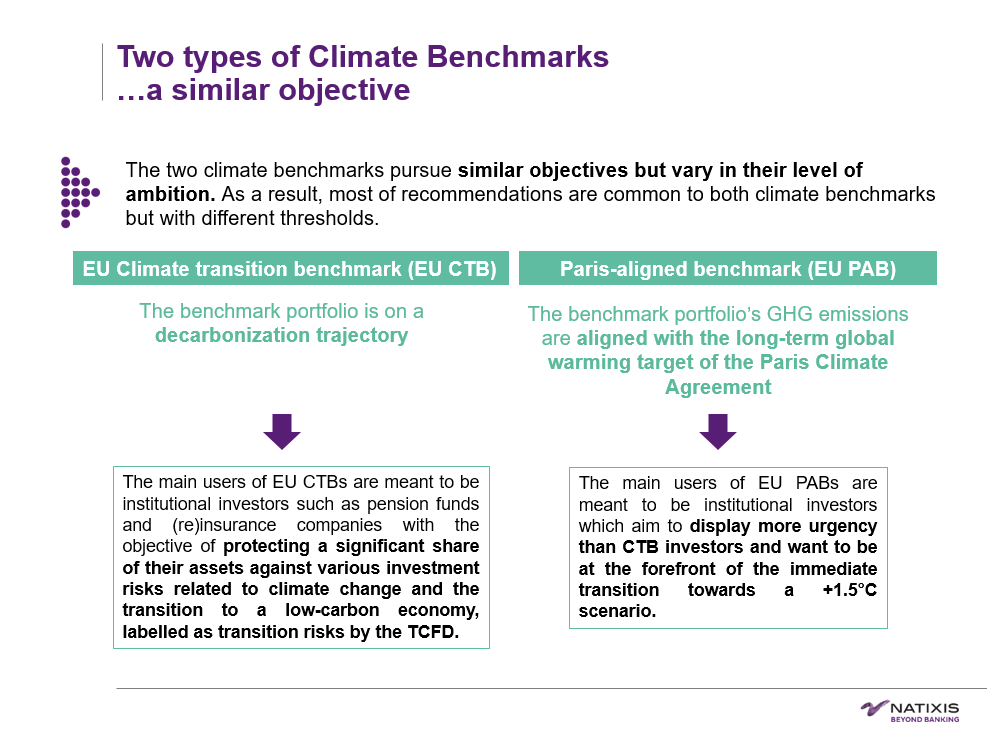

EU Climate benchmarks are investment benchmarks that incorporate specific objectives related to carbon emission reductions and the transition to a low-carbon economy. Two types of Climate benchmarks have been included in the Benchmark Regulation: “Climate-Transition Benchmark” (CTB) and “Paris-Aligned Benchmark” (PAB).

2. What is the difference between these two benchmarks?

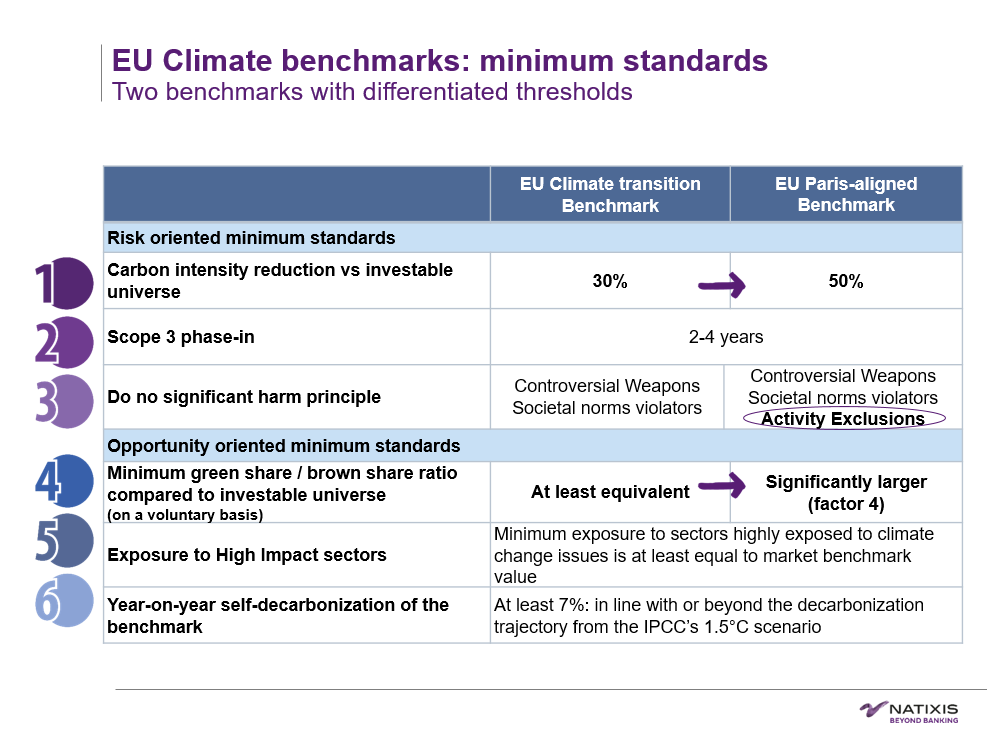

They pursue the same objective of de-carbonization trajectory but PAB is more ambitious and stringent. For example, companies involved in coal, oil and natural gas exploration are excluded from PAB but are tolerated in CTB.

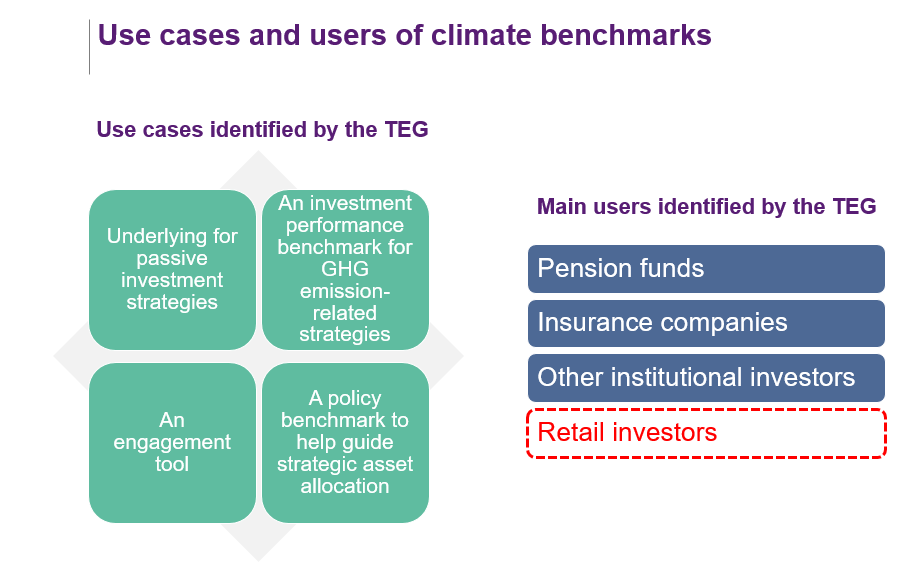

3. For whom have they been created?

Institutional investors, pension funds, benchmark administrators, but not only! The application scope goes far beyond benchmarks in practice. With these CTB and PAB criteria, the European Commission intends to provide all investors with a ready-to-use tool for asset allocation in order to align their portfolio with the Paris Agreement.

4. Why are they so important?

Current climate benchmarks do not always reflect investment beliefs and constraints of institutional investors, they also lack harmonization and clarity on objectives and methodologies. The EU TEG report published in September 2019 provides the list of recommendations for minimum standards, which will constitute a common language for investors.

5. Which asset classes are concerned?

Listed equities and corporate fixed-income benchmarks only. A pity that sovereign bonds are not in the scope.

6. What are the minimum standards to qualify as CTB or PAB?

A list of 7 criteria are defined, including notably i/ carbon reduction compared to the investable universe, ii/ minimum exposure to high impact sectors, iii/ year-on-year self-decarbonization. The criteria apply both to CTB and PAB but the thresholds are different for some of them. The main difference between the EU approach and current market practices is that standards are considered at portfolio level (weighted average), and not on a single-name basis.

7. Do these criteria make sense? Are they usable by investors?

Taken individually, yes, they do make sense: the level of stringency on carbon reduction is justified (-30% and -50% respectively), the differentiation between CTB and PAB based on activity exclusions is well defined, exposure to high impact sectors is a must-have.

However, the accumulation of criteria brings complexity in the portfolio construction. In addition, we are skeptical regarding the -7% YoY self-decarbonization requirement which disadvantages good performers and presents a backward-looking bias.

8. Are existing major climate/low carbon indices already actually compliant with EU Paris-Aligned Benchmark requirements?

According to our compliance test (6 benchmarks tested), none are aligned with the EU PAB.

And with Climate-Transition requirements? Very few of them. It is not surprising, as the first generation of low carbon indices were not always meant to follow a decarbonization trajectory.

9. Which relationship with the EU Taxonomy?

None of the requirements explicitly refers to the EU Taxonomy, but references are disseminated. In particular, the green/brown share ratio, albeit under a voluntary form, will be highly dependent of EU taxonomy which, so far, does not provide any guideline on brown shares and can be considered incomplete as to green shares.

10. What about the legislative process?

Now that the TEG recommendations are published and communicated to the EC, the Delegated Act to be published by the EC will enter into force in 30 April 2020 if Parliament and Council do not formulate any objections

How different from what already exists?

Overall, if amendments to the Regulation were passed, it could usher sustainable finance in a new era and so for various reasons. First, a double-sword approach is at last pushed, meaning that it is not only focusing on climate change risks management, as most of the existing low-carbon benchmarks do, but also take into account opportunities arising from the transition to a low-carbon economy. Existing Low-carbon benchmarks have been mostly built from a risk management standpoint (i.e. a tool for managing the risk of possible future regulatory intervention that might lead to “stranded” assets). They are mainly designed by removing or underweighting the companies with relatively high carbon emission footprints. The philosophy of EU CTBs and EU PABs is different; it aims not only at hedging against climate transition risks, but also at contributing to the transition and reaping its benefits and opportunities.

Too stringent? As for the EU Taxonomy technical screening criteria and thresholds, the question of stringency comes up. The minimum standards proposed by the TEG reminds us, from a different and more macro perspective, how far our economy is to the necessary trajectory to keep global temperature increase below 2°C by the end of the century. This Benchmarks piece is important because one says that transition must be rather monitored at holistic and aggregate level, at least macro-sectors, and that making a view of an individual company alignment is of limited interest. So we are definitely not on track, and the reality test we made when applying the criteria to existing indices revealed the magnitude of this gap. Current benchmarks are more aligned with a business-as-usual scenario (constituents tend to be even more carbon emitting than non-listed companies), where temperature rise ranges from 4°C to 6°C.

Overview of our feedback

First, we welcome the introduction of Climate benchmarks in the BMR as it should bring more clarity and homogeneity in the current climate/sustainability/low-carbon indices universe. This report of the TEG paves the way for a new generation of climate strategies.

Yet, how usable and scalable those benchmarks are will depend on the right balance between ambition and pragmatism.

Sovereigns not included: what a pity. We bemoan that Sovereign Debt is not (yet) included in the scope whereas resources and tools to assess their alignment exist and are more robust than for equity. Due to the sheer weight of sovereign debt in portfolios, it is the elephant in the room we must address, now rather than later. At least as a policy benchmark to help guide asset allocation (discretionary use of the criteria). It is wrong to say there is a lack of data, it is even quite the contrary, so-called alignment and assessment of the level of ambition of nationally determined contribution (NDS) and implementation exist and tend to be more robust and relevant (the more holistic you get, the most relevant an alignment assessment becomes!).

Taken individually, the criteria do make sense: the level of stringency on carbon reduction is justified, the differentiation between CTB and PAB based on activity exclusions is well defined, exposure to high impact sectors is a must-have. The green vs. brown share ratio on a voluntary basis is a nice to have indicator but hard to implement (until more robust methodologies and clarifications on brown revenues are available).

You need to get your portfolios dirty to clean up.

The sectorial constraints weighting is “a must have” and fortunately it is a prerequisite in the TEG's proposal. As a matter of fact, “you need to get your hands dirty to clean up”, meaning that the higher potential for decarbonization lies by essence within high-emitting sectors.

Overload of criteria. However, the accumulation of constraints and objectives restricts flexibility and technological options for benchmark administrators. Some criteria may even reveal incompatible. Asking cumulatively for a 30 or 50% cut in emissions against comparable universe, a 7% annual decrease and the respect of sectorial weighs (compared to parent index) seems hard to reach. Scalability is questionable as such complexity is barely compatible with systematic index rules (and national regulators’ requirements).

The YoY self-decarbonization requirement disadvantages the good performers and presents a backward-looking bias. YoY self-decarbonization of the benchmark of at least 7% is not taking into account efforts made by companies previously to this scenario. By requiring such annual rate, there is a risk to exclude companies that have in the past significantly reduced their emissions and that could be currently operating under science-based targets. Nor this 7% captures the non-linearity of emissions reductions. Furthermore, the forward-looking dimension is absent. We agree that it is challenging, because the information is missing but maybe that “green-brown capex ratio” or the ambition of public climate (science-based) targets would be an interesting indicators.

Intensity twists. Not a new issue, nonetheless still very relevant: carbon intensity may not always reveal to be a meaningful metric. The question of absolute emissions is eluded, and it remains unclear if the 7% self-decarbonization is an average of the constituents individual self-decarbonization rates. In that sense, as it is formulated, the criteria would treat equally self-decarbonization rate from a media or health company than from an oil and gas one, ignoring absolute emissions.

For PAB, companies involved in coal, oil and natural gas are excluded. While a clear difference between CTB and PAB is welcomed, such exclusion thresholds appear a bit dogmatic, especially for oil and natural gas companies. They could historically and predominantly belong to fossil fuel industry but having boldly started their transition with extensive diversification towards low-carbon energy sources. Furthermore, such exclusion thresholds hurt the 7% self-decarbonization rate which is more likely to be achieved by transitioning oil and gas companies.

Reality check. We tried to test TEG’s proposals to assess if the existing auto-labelled climate / low carbon indices comply with these EU forthcoming criteria. Unsurprisingly, we found hard to come up with examples of benchmarks fulfilling the proposed conditions. The next question mark now is whether a new generation of climate indices as defined in this report is able to fulfill the need for transparent, impactful, yet scalable benchmarks.