EU Green Bond Standard

EU Green Bond Standard

A bedrock for market rules and integrity

Natixis Green & Sustainable Hub is delighted to share with you our EU Green Bond Standard special report.

With this publication, Natixis GSH intends to raise understanding on what is at stake, on the key takeaways as well as providing you with our in-depth analysis of the EU GBS (compared with Green Bond Principles and observed market practices) and of the potential impact of such a standard on existing or coming Green Bonds.

This report is a second of a series. After our EU Taxonomy special report “Vade mecum to digest the 414-page Report from the TEG”, coming next our analysis of the Climate benchmarks and benchmarks’ ESG disclosures.

Editorial

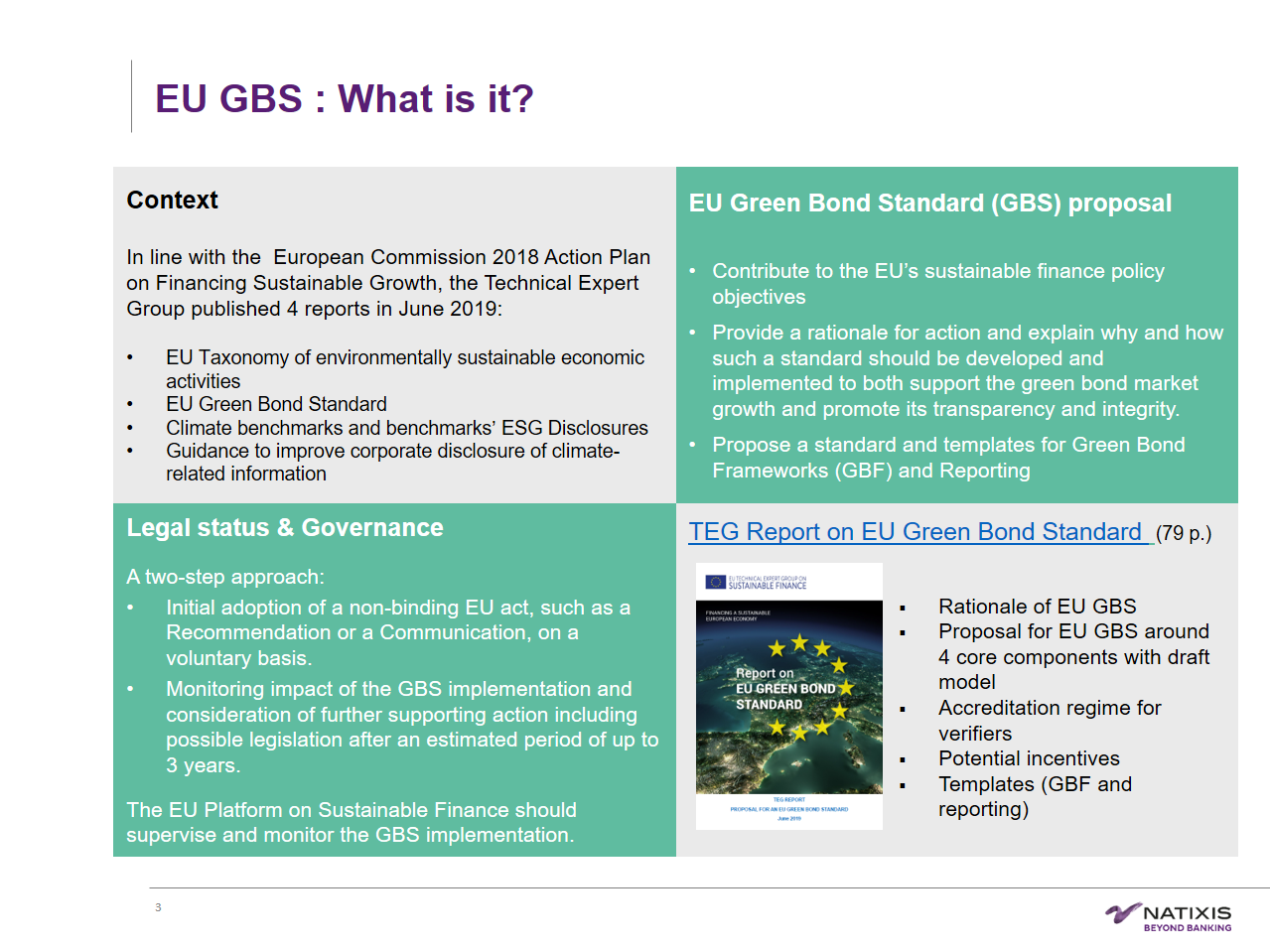

To implement its Sustainable Finance Action Plan, the European Commission mandated a Technical Expert Group to come forward with a standard for green bonds. This EU Green Bond Standard (GBS) proposal report provides impressive efforts and interesting content on the background to how the TEG is analyzing and understanding the green bond market, including its barriers and its practices. The proposal’s main outcome is a set of recommendations to the market on how to support and monitor the implementation of the EU GBS, and more importantly, ensure the market makes most use of it.

The EU GBS has been drafted to focus on two main objectives: supporting the green bond market growth and promoting its transparency and integrity.

An EU Green Bond is now defined as “any type of listed or unlisted bond or capital market debt instrument issued by a European or international issuer, defined as meeting the 3 following requirements:

- Green bond framework;

- Proceeds to green projects;

- External verification.”

From a legal perspective, the TEG recommends implementing the EU GBS according to a two-step approach. Firstly, an initial adoption of a non-binding EU act, such as a Recommendation or a Communication, on voluntary basis. Then, monitoring the impact of the GBS implementation to consider possible legislation after an estimated period of up to 3 years.

We believe the transparency and integrity objectives are well addressed with this version of the EU GBS. However, the success of this initiative will only come from its wide adoption, albeit voluntary to start with. Hence, the report contains a strong call to action for the entire market’s stakeholder: from issuers to investors as well as regulators, central banks & supervisors or banks.

With this publication, the second of our “TEG 101” series, Natixis Green and Sustainable Hub (GSH) intends to both raise awareness and enhance the understanding of the EU GSB proposal. Inside we share our key takeaways and provide an in-depth analysis of the EU GBS. In particular we compare it to the ICMA Green Bond Principles and observed market practices, and also offer our thoughts on the potential impact of the EU GBS on the existing and coming Green Bond market.

Transparency & Integrity

In our view, the EU GBS has met the transparency objective, especially by bringing additional clarity to the definition of eligible Green Projects via the linkage to the EU Taxonomy. The requirement to incorporate the Use of Proceeds within the legal documentation will also contribute to enhanced transparency and accountability on the issuance of EU Green Bonds.

By defining Green Projects as taxonomy-aligned projects, the TEG turns the EU Taxonomy into the cornerstone of the EU GBS, placing integrity as a key principle behind EU GBs. We also welcome, through the EU Taxonomy, the formal integration of any associated environmental and social risks along with the need to mitigate externalities in particular the Do No Significant Harm & Social safeguards sections.

However, we are concerned that the expected level of stringency in eligibility metrics & thresholds are likely to harm the growth objective for the green bond market while preserving its very necessary integrity. Having said that, there is still substantial room for interpretation. In particular, the “Do no Significant Harm” application and/or when activities not yet covered by the Taxonomy and/or for its usability at the asset level.

In our earlier handbook on the EU Taxonomy, we extensively commented the stringency of the proposed thresholds , and how far they often are from market practice and observed industrial performance levels. We would probably argue that the newly added (and very welcome) definition of “transitioning” activities” approach is very (too) narrow, long sighted and demanding and could allow for a more progressive approach to thresholds (and thus eligibility criteria) over the next decade.

Though, one should not lose sight of the purpose of the EU Taxonomy: define environmentally sustainable activities which would underline sustainable financing / investing products, set standards and regulations, as well as the needed disclosure to design them. Essentially, eligible activities are defined as those allowing for carbon neutrality in 2050.

Ultimately, the EU GBS is making the call that an EU GB should be financing green activities as defined by the EU Taxonomy, though not taking any stance on whether activities falling outside the taxonomy deserve, or not, financing overall. In that context, stringency is what we expect from the EU Taxonomy, as it aims to preserve the integrity of Sustainable Finance; a lack of which is the main risk to its development.

What is new about the EU GBS ?

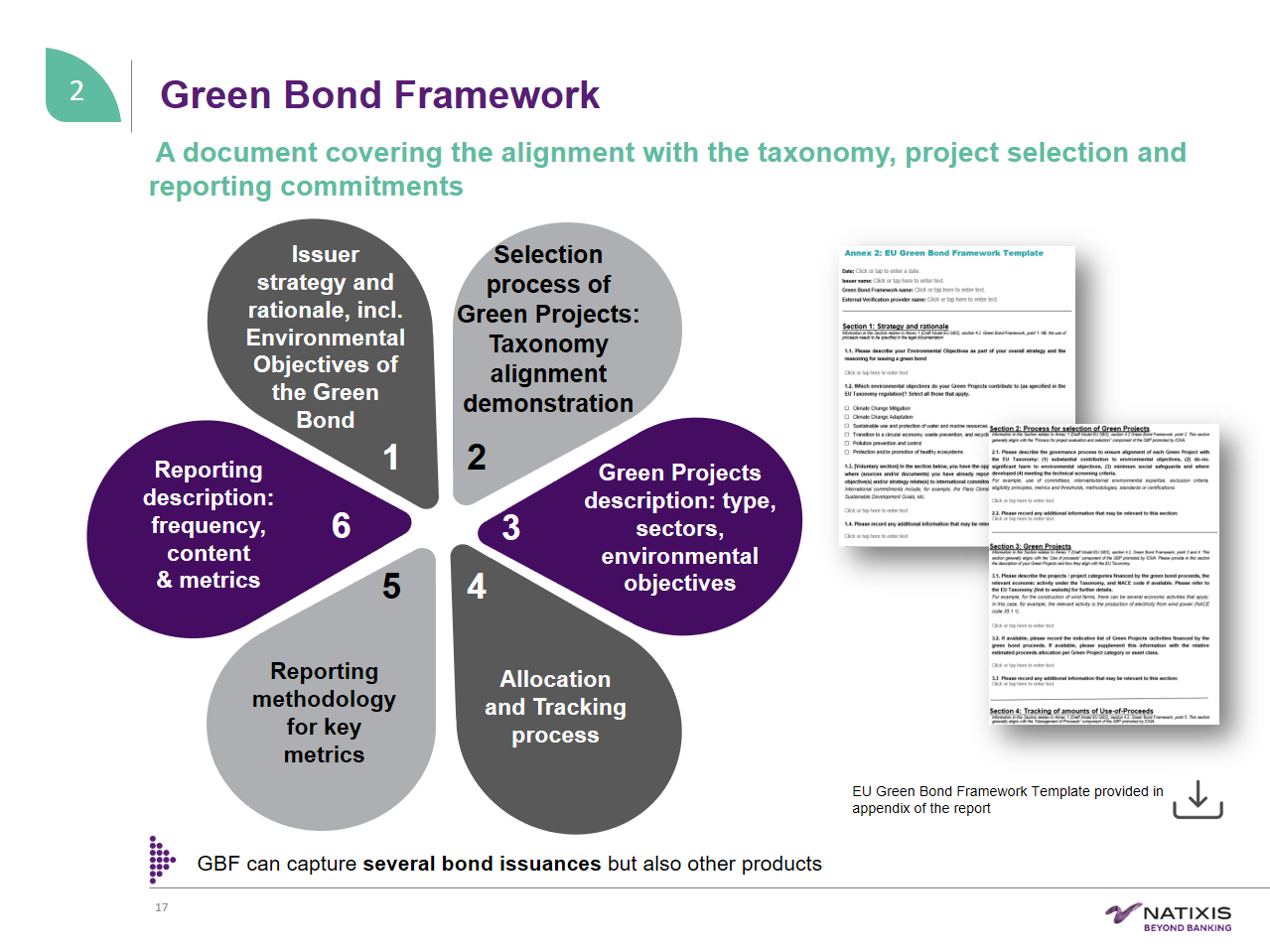

The ICMA Green Bond Principles are very clearly embedded within the EU GBS(four components, Green bond framework etc.).The key evolution relies on the prescriptive nature of some of the key characteristics of the EU GBS: most of GBP recommendations are turned into actual requirements, especially for explicit alignment with issuer's strategy, mandatory reporting of both allocation and impacts, bond by bond reporting, pro-rated share of impact, financing vs refinancing disclosure, and mandatory verification.

At the same time we clearly notice the attempts of the EU GBS to address some of the criticisms (or actual market practices) repeatedly expressed by market participants. Namely: administrative burden, type & characteristics of eligible assets, equivalence demonstration in the management of proceeds, one-off reporting, no look back period for capex, selected opex / public investments & subsidies, open door to Green Liability Management, etc.

In particular, we welcome the expected alignment of the Green Bond environmental objectives with the issuer's strategy and rationale. This is, in our view, of the utmost importance to demonstrate consistency and evidence of an issuer transition pathway. However, we regret the choice not to go one step further in the issuer level scrutiny of the EU GB issuance process. We would have supported the formal integration of some issuer level ESG performance considerations, or at least transparency in the EU GB documentation, which we view as a relevant proxy for the ability and credibility of an issuer to deliver on their green projects. Similarly, while the mandatory pre and post issuance reporting is very much welcome and in line with market practices, we would have welcomed mandatory impact reporting until bond maturity to ensure a sustained dialogue and accountability between bondholders and issuers as well as some reference to ex-ante/ex-post impact measurement.

One of the key add-ons of the EU GBS relate to the mandatory pre and post issuance verification by accredited external reviewers.

We welcome the proposed mandatory verification by an EU accredited external reviewer, pre and post issuance. The accreditation process is likely to, progressively (until EU Taxonomy completion), drastically alter, if not “kill”, the current SPO format and turn an external review mission into a pure verification model leading to an evolution of the external reviewer landscape in favor of auditors.

However, the publication of the EU GBS ahead of a finalised EU Taxonomy[1], as well as the room for interpretation left in the Do No Significant Harm & Social Safeguard criteria, are good reasons to think that there is still quite some time before we reach that pure verification model for external reviewers. In the interim, external verifiers (or Second Party Opinion providers) will be required to bridge the gaps of the EU Taxonomy in terms of coverage and integrity assessment.

Here at Natixis, we have always been strong advocates of the need for common language as well as clear and common rules of the game. Against this backdrop, we welcome this new EU GBS proposal which we believe is aligned with both the ICMA GBP and best market practices. It is introducing a number of very welcome clarifications and has settled a great number of the debated features of green bonds, striking a balance between easing up on some market practices and tightening up others by means of prescriptive requirements.

If we allow ourselves to be picky, beyond our comments on the EU Taxonomy itself (becoming here the eligibility criteria), some clarifications are still expected, such as: cash management, proceeds recycling rules, allocation period, conditions under which green liability management is allowed, applicability of the EU GBS outside the EU (for both issuers and projects), especially for the Do No Significant Harm criteria.

Last but not least, the timing of its publication (i.e. ahead of the full EU Taxonomy completion) will lead to some level of confusion and uncertainty when it comes to compliance process, scope of certification, timeline, and above all usability. But one needs to start somewhere and this is a sound and useful start.

[1] i.e. the wide amount of GBP eligible categories and NACE activities yet to be covered by the EU Taxonomy, where the screening criteria becomes “substantial contribution to one or more environmental objective”