Social bonds: easy come and easy go?

The fate of Social Bonds was the topic of a panel at Environmental Finance’s ESG in Fixed Income event on April 17th. “Social bonds, could they die on our watch?” This was the thought-provoking title of a conversation moderated by Cédric Merle from the Green & Sustainable Hub. The state of the social bonds market, its key features and ongoing trends were discussed.

On this occasion, Natixis prepared the following article titled “Social bonds: Easy come and easy go?” It is accompanied by a set of graphs (sample of slides accessible here, for a more detailed version, please contact us). Feel free to reach out for bilateral meetings or to share feedback.

Executive Summary

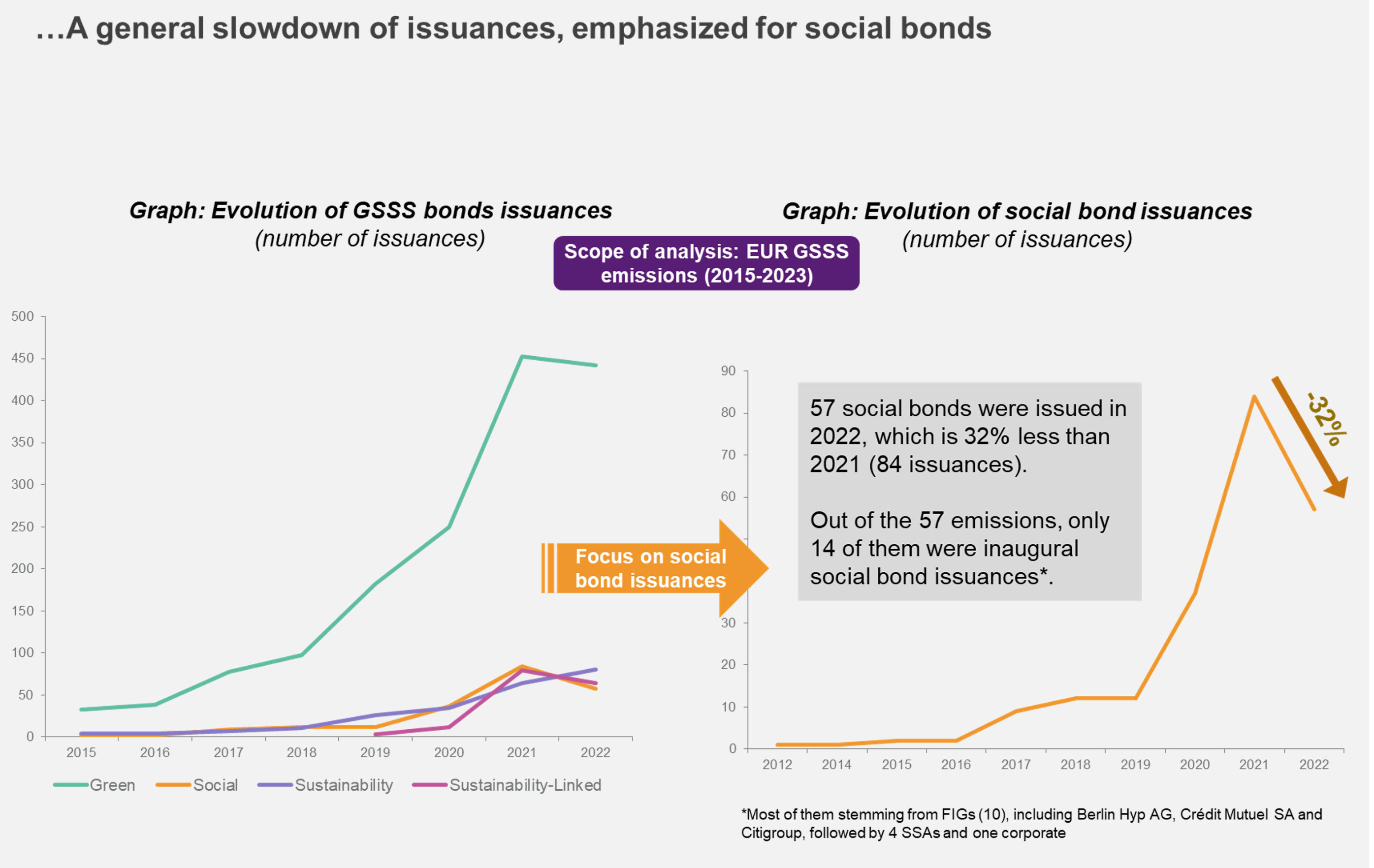

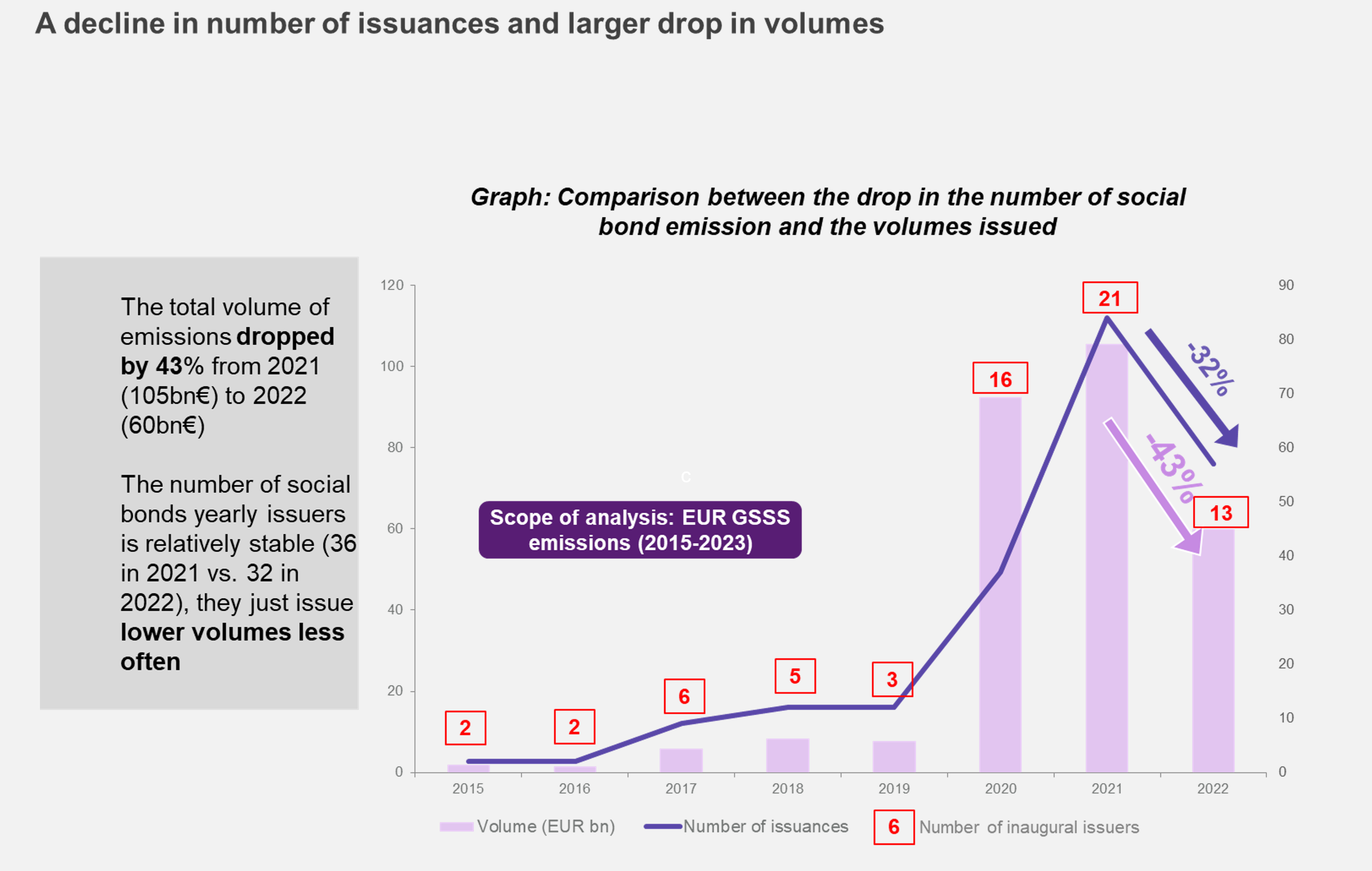

Pandemic roller-coaster. Social bond issuances and volumes greatly increased in reaction to the Covid19 crisis. As the market was gaining traction, the number of new issuers grew five-fold. The market proved to be highly elastic to circumstances: the total volumes issued grew by a staggering 1,253% from 2019 to 2021 (though with a gigantic base effect). Once the pandemic was reined in thanks notably to vaccination, pandemic related spending decreased and the number of issuances decreased by 32%, along with a corresponding 43% drop in volume from 2021 to 2022.

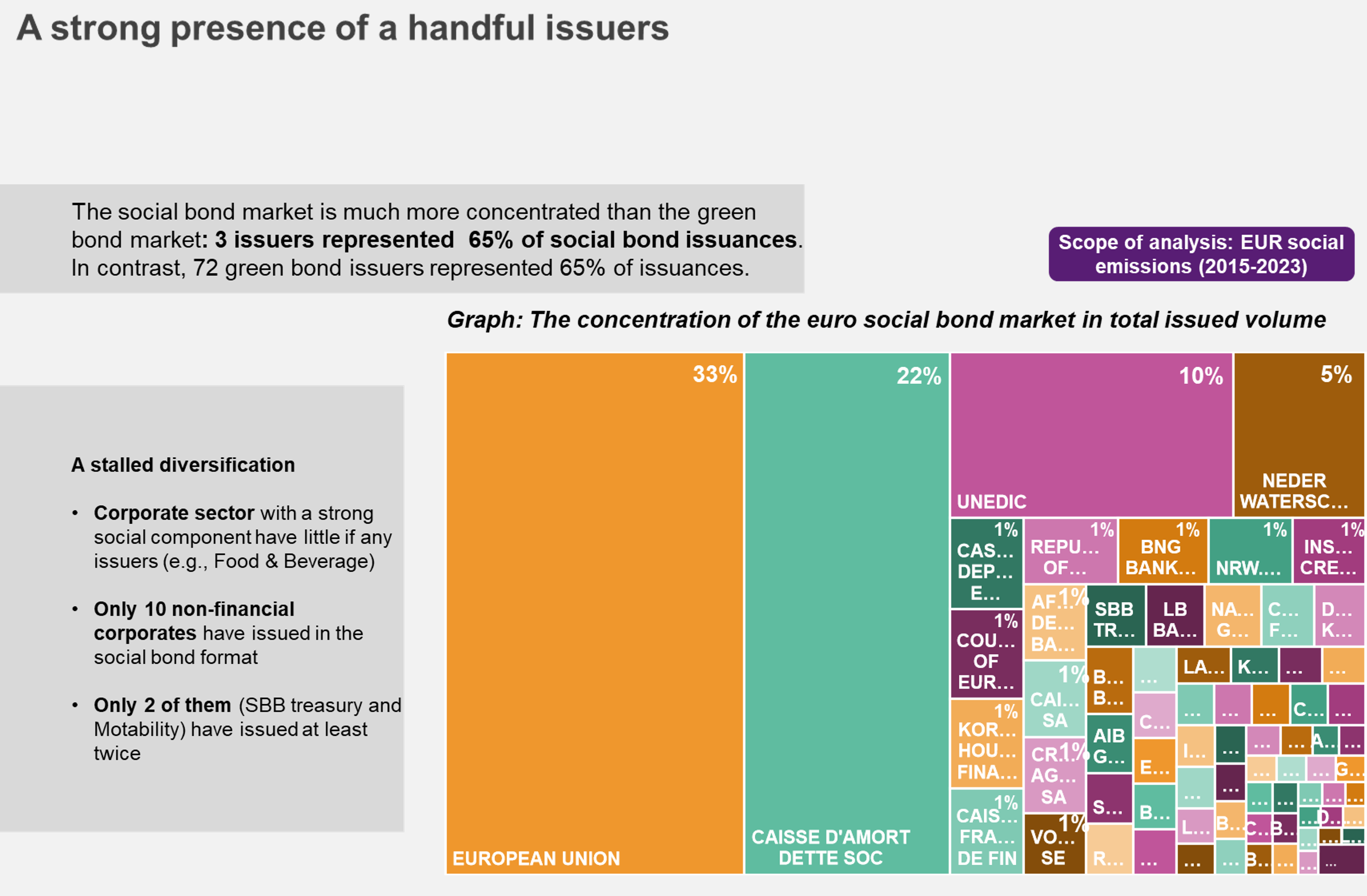

A concentrated market with a prevalence of SSAs. The social bond market is characterized by the preponderance of certain market participants, the top three issuers (EU, Cades and Unedic) representing 65% of the total volume issued in euro currency. Issuers are mostly SSAs (notably ones with a specific social purpose), followed by FIGS. Corporates are almost absent from the market. A great number of corporate issuers face difficulties of using the UoP social bond type out of lack of eligible social oriented capex. Some might have opted for other bond types such as green bonds with transparency on social co-benefits or the KPI format through sustainability-linked bonds. Lastly, an important number of them combine both social and green categories through sustainability bonds, with the bulk of proceeds being usually earmarked to social ones.

Proceeds allocation channeled towards two dominant categories. Despite the variety of eligible categories (2 or 3 per framework on average), most of the proceeds are allocated to “access to essential services” and the target populations which appear the most are people “living below the poverty line”. “Employment generation” is only mentioned in 14% of social bonds frameworks, nonetheless, it gathers almost half of the estimated proceeds allocation overall.

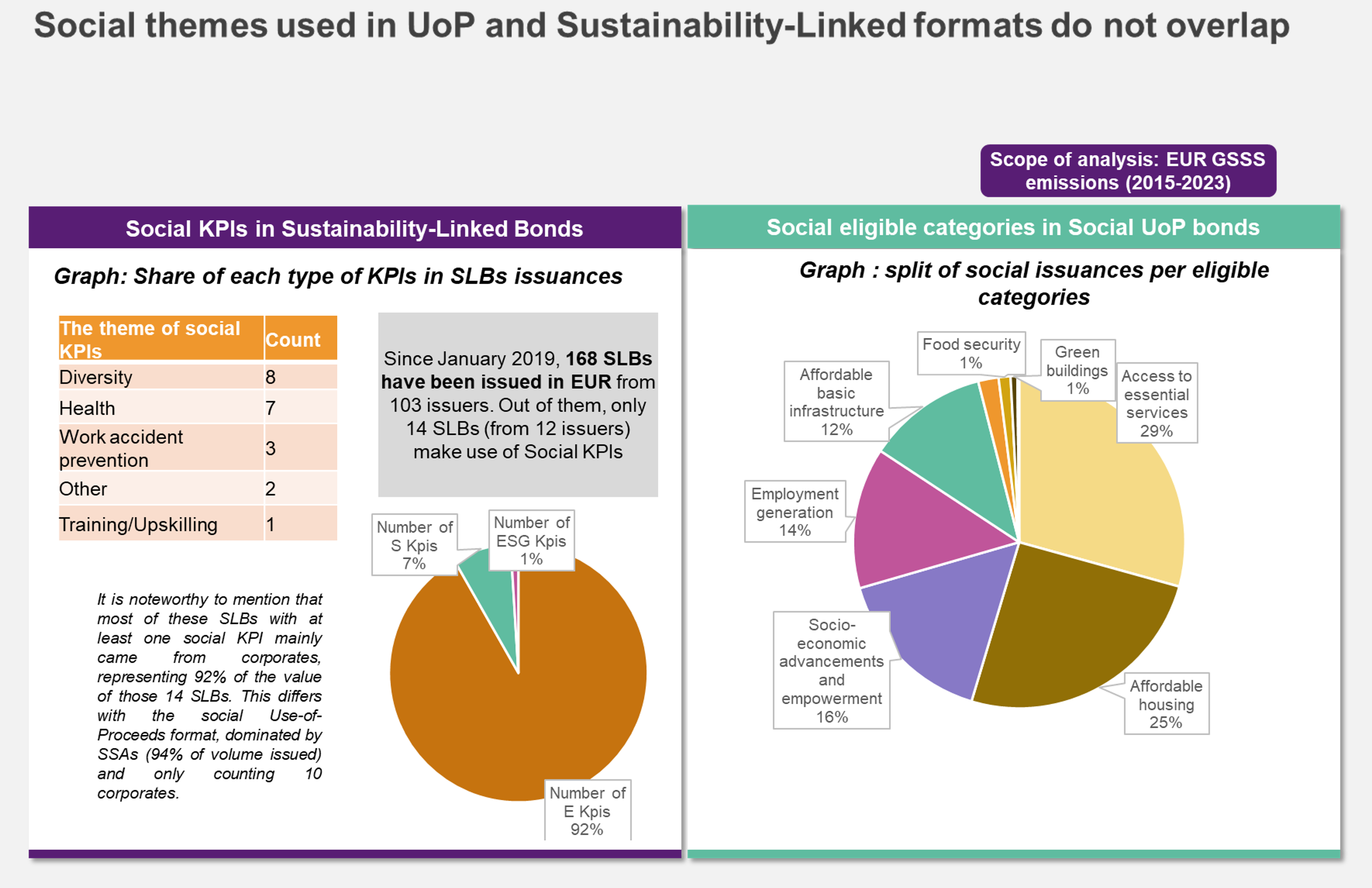

Complementary lenses on “social themes” between SLBs and UoP bonds. SLBs incorporating social KPIs tend to tackle themes such as workplace diversity or safety, in contrast to UoP Social Bonds which focus on access to essential services and affordable housing. Since the emergence of the SLB market in 2019, 14 EUR SLB issuances incorporating social KPIs, accounting for 10% of the total SLB volumes were identified. 9 out of them paired social KPIs alongside environmental ones.

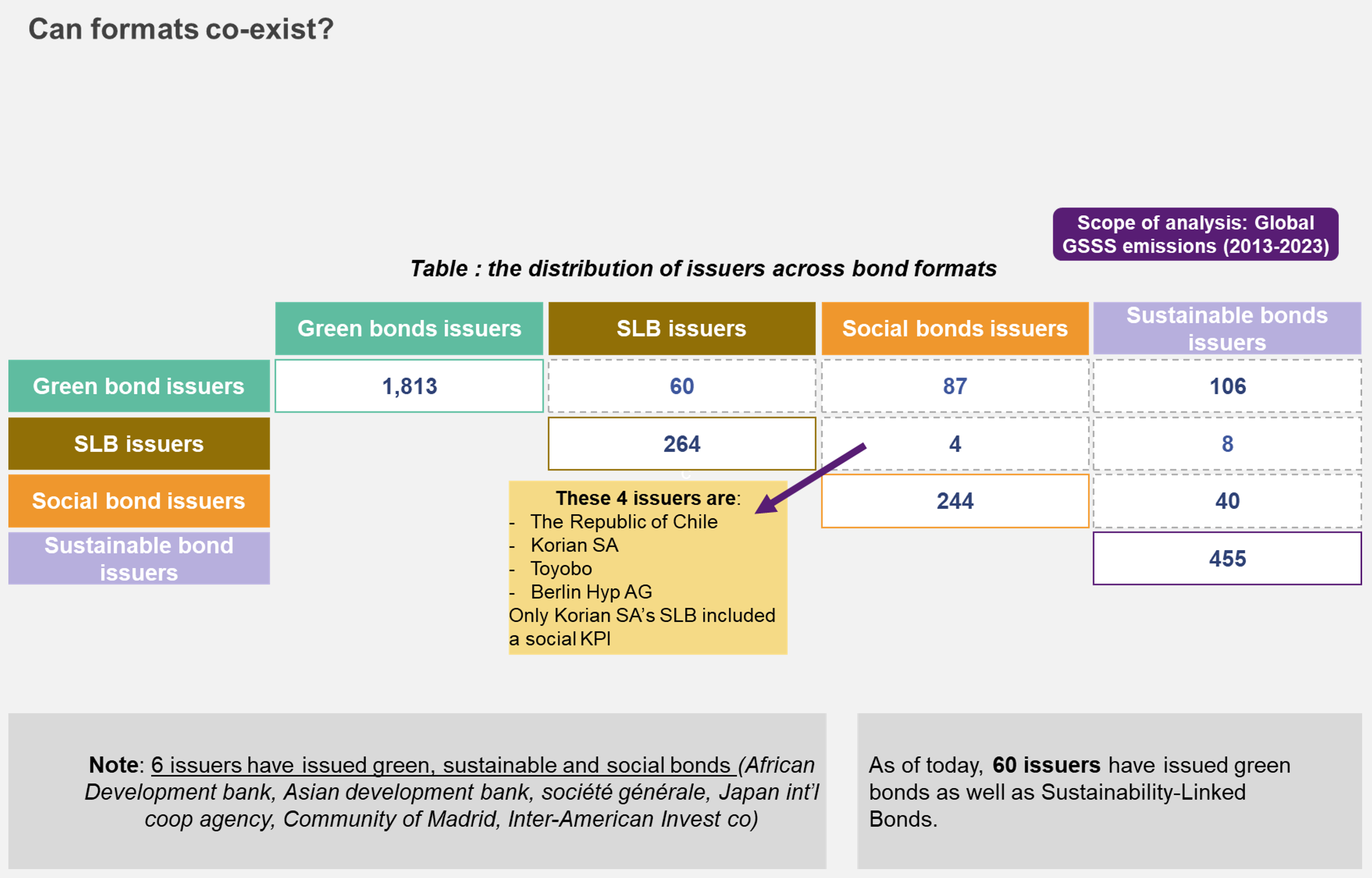

Issuers’ arbitrages between GSSS bonds. Overall issuers tend to choose between bond types. There are no issuers which have issued all types of GSSS bonds, only 6 have issued green, sustainable and social bonds. Even though social bonds and green bonds can be used jointly, the majority of issuers limit themselves to one type.

Upcoming market challenges: conciliating diversification and standardization. Some regulations such as the Corporate Sustainability Reporting Directive (CSRD) are expected to increase the availability and standardization of social KPIs for SLBs. Moreover, the Corporate sustainability due diligence Directive (CS3D)[1] will strengthen due diligence on social matters. In parallel to regulatory developments, the concept of "fair transition" is gaining traction, and is increasingly being incorporated by SSAs and corporates.

What’s in it for investors: Because the market for social bonds is less mature and diversified than the green bonds one, this limited supply poses diversification and liquidity challenges for social bond funds. In addition, the lack of harmonization in social bond impact reporting is also a difficulty for investors when attempting to publish their own impact report.

Deciphering the market

The social bond market by the numbers

After a boom of the GSSS and overall bond market, a clear slowdown took place starting in 2022. More specifically, social bonds issuances remarkably increased in the context of the pandemic, and the magnitude of their fall was larger than other types[2]: 84 social bonds were issued in EUR in 2021[3] versus only 57 in 2022.

The number of active issuers is rather stable: 36 issuers opted for a social bond in 2021, whereas 32 did in 2022. Newcomers are limited as only 14 inaugural issuances occurred in 2022. In contrast, the volumes issued were sharply decreasing (around €105bn in 2021 vs €60bn in 2022). In short, the number of yearly social bonds issuers is more resilient, but they issue lower volumes less often.

Zooming on the EU GSSS bonds market...

Source: Natixis Green & Sustainable Hub's Internal Market Data

Endless questions

One wonders: Was 2021 the apex of the social bonds market? Or is the market simply undergoing transformation? If so, what types? Social bond issuances seem highly counter cyclical and elastic to crisis. Is this financing instrument fit for “ordinary times” or only for turbulent ones? Are social eligible categories and green eligible categories vying for market share? Is the social bond type exclusive and requires or leads issuers to waive other types of bonds? Are Use-of-Proceed and Sustainability-Linked formats competing against each other? Are social spendings or investments hard to identify and segregate, or not large enough in terms of amounts to sustain recurrent social UoP issuances? Could social matters therefore be better captured through KPIs at issuer-level? Is social performance or contribution rather delivered through procedures or policies? Do issuers with a core social remit need such financing and what value add does it bring to investors? And why is the social bond market so concentrated with limited diversification and such very low participation from non-financial corporates?

A multi-faceted significant social contribution

By essence, social matters are diverse and intertwined. This multiplicity partly explains the current state of the market described thereafter: limited diversification, some absentees, or the heterogeneity of criteria and practices. In the context of social finance, and more specifically social bonds, a “significant social contribution” relies on a diversity of criteria around locations (e.g.: disadvantaged areas, territories hit by extreme weather events), contexts or situations (e.g.: “ordinary” times or emergency or crisis), project categories and activities (e.g.: social housing, healthcare), as well as target populations (e.g.: low-income or unemployed people). A substantial contribution to environmental objectives is defined more univocally (with carbon intensity thresholds for instance). “Access to essential services” (a catch-all category with different sub-categories) and “Affordable housing” are dominant in frameworks. Over the last years, very few new categories such as public supply or support to cultural activities have appeared.

A highly concentrated market

Out of all the types of social bond issuers, SSAs are clearly the most prominent (52% of the total issuers overall) especially supranationals (e.g. the EU) and government agencies (e.g. UNEDIC and CADES), which have a pure social remit. Supranationals and agencies are followed by public banks and a very few sovereigns[4]. SSAs emissions appear to be highly cyclical. The volumes at stake vary according to issuers profiles. On the one hand, SSAs such as the European Union tend to mobilize significant amounts of capital (and are therefore able to earmark social expenditures). On the other hand, FIGs can also identify significant amounts of financings mainly for social infrastructure, whereas corporates show low social capex (to enable benchmark size UoP formats).

The concentration of the social bond market

Source: Natixis Green & Sustainable Hub's Internal Market Data

SSAs are clearly the most prominent social bond issuers (52%), followed by FIGs (45%) and corporates (3%). Overall, the social bond market is much more concentrated than the green one: three issuers account for 65% of the total volume issued as of today[5]. In contrast, the green bond market is far less concentrated, the 72 largest issuers accounting for 65% of total volumes issued. We note that 6 social bond issuers have stopped issuing conventional bonds for at least two years[6].

Specifically, SSAs issuances focus on targeting employment generation and access to essential services. For example, the EU represents 94% of access to essential services allocation according to our estimates. In terms of target populations, the most recurrent ones in frameworks are people “living below the poverty line” and “aging populations and vulnerable youth”. The most common geographical regions in allocation reports are Italy, France, Spain, Romania, Belgium and Germany. Noticeably, there are gaps between eligible categories mentioned in frameworks and actual proceeds allocation. For instance, using the data available, our analysis finds that overall “affordable housing” is only the fourth most allocated proceed gathering 10% of allocations, behind “access to essential services” (36%), “employment generation” (33%), and “socio-economic advancements” (19%). However, if the same analysis is conducted on SSA issuers only, “employment generation” is the eligible category receiving the most funds allocated (40%), with Unedic representing 39% of allocations.

The eligible social categories

Source: ICMA social bond principles

The split of social issuances per category

Source: LGX

Developed countries vs. emerging countries

There is a clear contrast between issuances numbers and their volumes in developing countries’ and in developed countries. As developing countries represent around 6% of the total volume issued, developed countries gather a staggering 94%. In the case of developed economies, SSAs such as the Walloon Region and the NRW Bank[7] have issued social bonds in the last few years to fight back social disparities, harmonize living conditions and further social inclusion. In general, developed countries’ SSAs tend to focus more on SDGs 11 (Sustainable Cities and communities) and 4 (Quality Education) whereas emerging economies’ SSAs target SDGs 10 (reduced inequality) and 1 (No poverty). Hence, the developed economies concentrate their issuances on the access to essential services and socio-economic advancements and empowerment as well as affordable housing, and in parallel, emerging economies focus more on socio-economic advancements and affordable housing. Nonetheless, it is worth mentioning that some supranationals (listed as developed countries’ issuers) are predominantly involved in emerging countries’ growth through social bonds (for which they represent a third of the total volumes issued) and sustainability bonds.

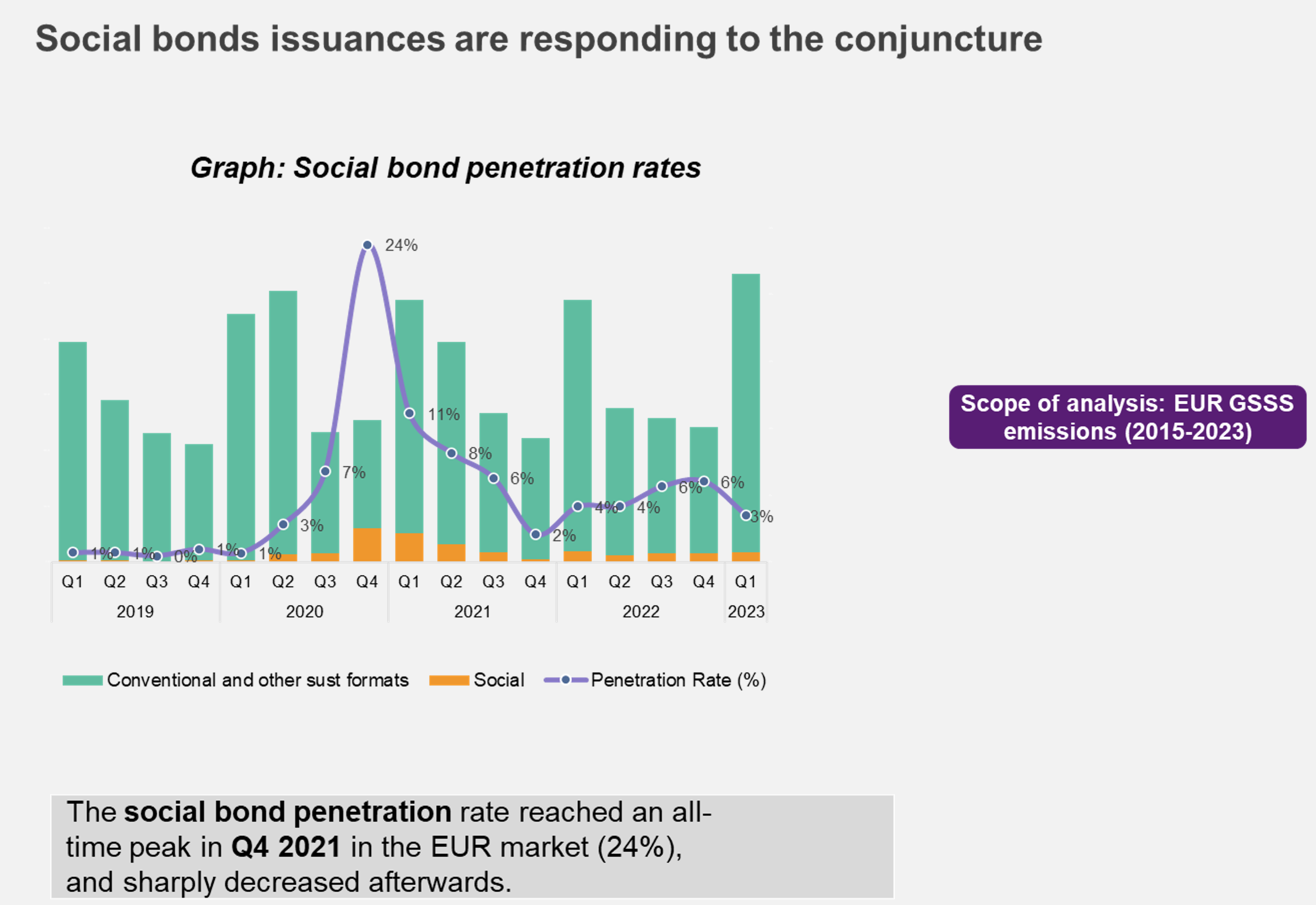

Fluctuating penetration rates

Between 2019 and today, the penetration rates for social bonds in EUR debt financing compared to the total volume of bonds issued has been 5% on average. Most importantly, it reached an all-time high during Q4 2020 at 24%, and sharply decreased after that. In contrast, the penetration rate for green bonds is more stable. After a considerable surge in 2020, the penetration rate for green bonds has stayed around 30% of total debt financing.

Penetration rates in euro issuances

Source: Natixis Green @ Sustainable Hub's Internal Market Data

Adaptability of the market

Cyclicity & elasticity to circumstances

Social bonds issuance volumes– at least for some issuers and Use-of-Proceeds categories – are largely affected by major events and economic or social cycles. Nonetheless, no one would argue that the world economy went back to “normal” after the pandemic. This holds particularly true for Europe.

Why did the market not swiftly react to the invasion of Ukraine and the subsequent food and energy crisis, or the global inflation surge? Is it because of time lags between the outbreak of a crisis, expenditures disbursement to alleviate its effects, and actual fundings operations ringfenced towards those expenditures? Or is it because of the very nature of the organizations delivering the necessary funds, as they are not directly issuing bonds? As the market is presently more mature, with frameworks readily available for issuance, one could expect shorter timeframes between an emergency/crisis outburst and counter-cyclical spending issuances.

A high counter-cyclicity and elasticity to crisis

Source: Natixis Green @ Sustainable Hub's Internal Market Data

Inflation crisis: unnoticeable effects on the market

Conversely to covid-19 related measures, which largely ended-up in social bonds proceeds, programs or support to households or companies to contain inflation[8] have not yet percolated into issuances. This is possibly because a big part of these programs took the shape of fossil fuel subsidies, therefore not being eligible for sustainable finance products despite a strong social impact (shield against fuel poverty). In fact, worldwide fossil fuel subsidies more than doubled between 2021 and 2022, reaching more than USD 1 trillion, according to a report from the IEA[9]. Conversely, total spending in clean energy was expected to increase by USD 0.1 trillion in 2022 according to the IEA[10]. Regarding elasticity, one should therefore scrutinize the absolute volumes of proceeds allocated to renewable energy within the next two years to identify a potential correlation.

Supporting Ukraine: another once-in-a-century social effort

In the aftermath of the invasion of Ukraine, Council of Europe bank (CEB) issued several social inclusion bonds to bolster its response to Ukraine refugee crisis. The bonds proceeds were used to finance social loans to CEB member countries to support the longer-term needs of Ukrainian refugees and their host communities. Meanwhile, the Canadian sovereign issued a “Ukraine Sovereignty Bond”[11], focusing on providing Ukraine with essential services such as pensions, fuel purchase subsidies and the restoration of the energy infrastructure. Through this 5-year C$500 million bond, the total proceeds will be transferred to Ukraine through the IMF. Apart from those two examples, the Ukrainian question has had little effect on the social bond market so far. We believe it is a matter of both nature of interventions, and timing.

First, for the time being, a big chunk of Ukraine-related spending consists of weapons and military support, which does not fall into the social bond remit, but for which ESG/sustainability minded investors start adjusting their stance. Some now consider defense as a prerequisite for rule of law, human rights protection and wellbeing and have accordingly adjusted their exclusion policies. In parallel of the €18 bn support package of the Commission on essential public services, macroeconomic stability and restoring critical infrastructure[12], the European Council has also agreed to a total of €4.6 billion aid for military spendings[13]. In contrast, the EU has raised a total of almost €100bn using social bonds to overcome the Covid19 crisis[14]. However, the costs of the reconstruction and recovery of Ukraine after the war are estimated to reach €383bn according to World Bank Assessment[15].

Second, on the medium and long-term, the massive mobilization of capital to rebuild Ukraine and to enable its EU membership through reforms may sustain the social bond market, as a significant portion of this spending will come from the EU, possibly financed through social bonds. Development financial institutions, supranationals and agencies will predominantly finance such endeavor. Private companies will be involved as well but to a lesser extent. Later, businesses involved in the construction sector may also be involved in this task (Japanese companies in the sector are regular issuers of social bonds), alongside utilities (waste, water, power, etc.), but this will require the situation to stabilize.

Arbitrages between issuance types

We identified 78 issuers who have issued a social bond in EUR since 2012. 55% of them have also issued a green bond, and 14% have issued sustainable bond. Out of those 78 social bonds issuers, only 24 rotate between social bonds and other types of GSSS bonds regularly, mostly SSAs[16]. There are various reasons in picking one type of bond versus another. It could be because of the availability of proceeds and time necessary to “reload” a large enough pool (while maintaining a flexibility buffer[17]), demand from investors, or availability of data for impact reporting, among other reasons.

Arbitrages between issuance types

Source: LGX

Sustainability Bonds: two sides of the same coin

Issuers also opt for sustainability bonds, which mix both green eligible categories as well as social eligible categories. As of today, 96 issuers have issued at least one euro-denominated sustainability-bond. Compared to the euro-denominated social bond market which represents €303bn of total volume issued, the sustainability bond market is clearly less volumetric, as the total volume issued only stands at €172bn. As one could expect, SSA’s are leading the way, representing the biggest share of unique issuers (43%)[18], followed by FIGs (39%) and corporates (19%). Interestingly, many corporates operating in the telecommunications sector (such as Telecom Italia, Telefonica Europe or Orange SA) have issued sustainability bonds. Likewise, SSA’s are also accountable for more than 80% of the total volume issued in sustainability bonds.

The social categories that are the most referred to in sustainability issuances are “Access to essential services” and “Socio-Economic advancements and empowerment”. On this topic, it is interesting to point out that, according to our estimations, social categories receive 51% of the total proceeds allocation, implying that social matters are deeply rooted in sustainability issuances[19].

SLB’s social footprint

One wonders whether the social thematic could also be addressed through other instruments outside of the UoP format.

There are several distinct situations for choosing the SLB format to address social impacts: issuers which could not access the social bond market for lack of identifiable eligible expenditures and consider that KPIs better capture their social efforts and impacts, and the ones discouraged by the “rigidity” of the ringfencing needs and reporting processes.

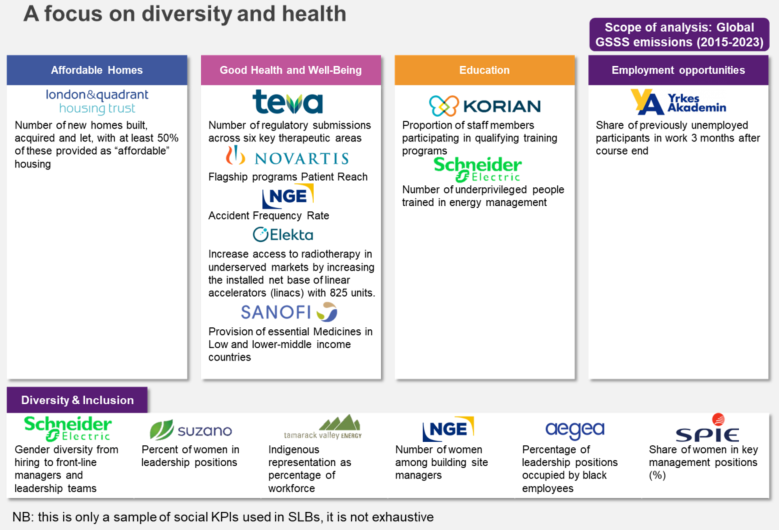

Since the emergence of the SLB market in 2019, 14 EUR SLB issuances incorporating social KPIs, accounting for 10% of the total SLB volumes were identified. 9 out of them paired social KPIs alongside environmental ones (e.g., from Teva Pharmaceuticals, Edenred and Schneider Electric) and only 5 contained social KPIs only (Sanofi, Novartis AG, Mota-engil and M Finance SASU).

The social KPIs used in SLBs

Source: Natixis Green @ Sustainable Hub's Internal Market Data

It is noteworthy to mention that most of these SLBs with at least one social KPI mainly came from corporates, representing 92% of the volumes issued of those 14 SLBs. This is contrast with the social UoP format, dominated by SSAs (94% of volume issued) and only counting 10 corporates. Nonetheless, one reminds that SSAs are barely present on the SLB market, with only two sovereigns (Chile and Uruguay).

Social themes across bond types

Source: LGX

What the future holds

A long-awaited diversification: social bond market absentees

Issuer types and sectors of social bonds are stable. The necessary diversification does not seem to be underway. Sectors with a strong social component such as Food & Beverage corporates have little if any issuers. 10 non-financial corporates[20] chose to issue a social bond, and only two[21] of them have issued at least twice. The main barriers for corporate relate to low social capex, with social dimensions being tackled in a more diffuse and policy driven manner.

Additionally, out of the 23 sovereigns which issued a GSSS bond, only 6 have issued a sustainable bond with social categories mainly related to access to essential services and employment generation, accounting respectively for 8bn € and 36 million € in proceeds allocations.

We have observed very few inaugural social bond issuances since January 2022 (only 14), most of them stemming from FIGs (10), including Berlin Hyp AG, Banque Fédérative du Crédit Mutuel SA and Citigroup, followed by 3 SSAs (Investitionsbank Berlin, Agenzia Nazionale per l’Attrazione degli Investimenti e lo Sviluppo d’Impresa and Asian Development Bank) and one corporate (Vonovia SE). But this could evolve, notably thanks to regulatory developments (see hereafter about CSRD).

Some issuers are surprisingly absent from the social bond market even though their “remit” is social or their business positioning is highly material from a social standpoint, for instance in the food industry or the catering sector . Corporates operating in the health or education sectors are noticeably absent from the social bond market despite the existence of a number of thematic equity funds tackling those themes, which proves that eligibility criteria exist.

For sovereigns, the challenge lies in rigorously delineating “social expenses” from “non-social ones” (guaranteeing cohesion, solidarity, insertion, equality, education versus regalian functions around maintaining social order, defending borders). One could argue that states’ entire budgets are social by nature. However, only 5 sovereign issuers have opted for a social bond.[22] Issuing a social bond could be puzzling or misleading, implying that older bonds or non-earmarked programs are less socially beneficial and impactful. It could feed endless political discussions on eligibility or spending efficiency. However, health or education programs appear to be the most consensual despite lingering debates around the eligibility of payroll or operating expenditures. For sovereigns, “social” could be defined as “welfare” related, with subsequent debates around “general population” vs. “vulnerable groups”. For instance, “Migrants and/or displaced persons” as well as “Excluded and or marginalized populations” are rarely mentioned in frameworks.

Initiatives and constraints on investors’ side

Compared to green bonds, themes present in social bonds are unquestionably much more diverse (e.g., poverty, education, inequalities, health, etc.) and, as a consequence, less straightforward. As explained above, social bonds can help address issues that are either localized or global, urgent or for the longer term, and that encompass multiple topics. The market for social bonds is also rather restricted: since 2015, more than 5,200 green bonds issuances (all currencies included) took place, while only 796 social bonds were issued[23]. The lack of available supply in social bonds could be a reason for the limited number of social bond funds, as investors aim for portfolio diversity to reduce risk. This could also be an explanation for why the existing social bond funds have a restricted number of assets in their portfolios compared to other funds. In fact, less than 10 social bond funds have been identified[24], whose whose number of lines range from 48[25] to 274[26].

In addition to the limited supply of social bonds, producing an impact report for issuers themselves, and thus for fund managers is a highly difficult task to carry out, as social metrics tend to be more of a qualitative nature[27]. This is emphasized in Amundi’s social bond funds’ impact reporting[28], which encourages issuers to go beyond ICMA’s social bond principles and harmonize impact indicators for each category of action. Thus, one could ask: is the challenge of social impact reporting deterring some players to opt for social bonds?

The foreseeable push from EU regulations

Surprisingly, while greenwashing is on everyone’s lips, it seems there are less concerns or controversies around social washing. Classification efforts on social matters are limited, and the proposal on an EU Social Taxonomy[29] is still on hold.

However, social matters are handled in other regulations which are not product-based, mostly through CSRD. Issuer-level disclosure on social themes will increase both qualitatively and quantitatively through the European Sustainability Reporting Standards (ESRS), of which the first draft was published in November 2022.

One expects a greater availability and standardization of social KPIs for SLBs or UoP Bonds in Europe, with multiple indicators, related to issuers’ own workforce (S1), workers in the value chain (S2), affected communities (S3) and consumers/end-users (S4)[30]. For instance, the KPIs requested for S2 include the percentage of employees and non-employees workers earning less than the fair wage benchmark[31]. In addition, the CS3D is supposed to be implemented starting in 2025 and will strengthen due diligence on social matters by requiring more than 16,000 firms to establish, publish, implement and monitor a “vigilance plan“ (as per Duty of Care).

Fair transition momentum

Among the promising topics and drivers of market growth, one also highlights fair transition. In 2016, the International Labour Organization (ILO) published its guidelines for a just transition, and it seems that the thematic is increasingly present and considered by SSAs and corporates. It is yet to be determined whether the current initiatives such as Institut de la Finance durable (former Finance for Tomorrow) will bridge the lack of indicators and data and make the topic investable[32]. Some initiatives have already taken place. For instance, Renault included a fair transition eligible use of proceeds category in its sustainable bond framework: by creating reskilling and upskilling programs for Renault and the sector’s employees. Thanks to the ReKnow University project, the group aims to maintain and protect employability for all in the automotive sector. A sector that is experiencing deep transitions. Similarly, EDF opted for a sustainability-linked loan, with KPIs involving employees, customers, suppliers and communities, related to just transition[33].

“Social” beyond social bonds?

Interestingly, social themes used in UoP and Sustainability-Linked formats do not perfectly overlap. Some themes are prominent in SLB issuances, namely workplace diversity (ethnic and gender), but are quasi absent in UoP formats. Some themes are equally present in both formats such as access to essential services, especially health. Furthermore, topics such as inequalities or forced labour lack suitable criteria for UoP instruments. These are better tackled through SLBs. Plus, they are more a matter of risk management than direct investments per se.

The difficulty of capturing social issues throughout Use-of-Proceeds format becomes increasingly apparent. Some social mega trends or concerns such as large-scale involuntary migration (see WEF’s Global risk report 2023) are hardly addressable through fixed-income products.

In conclusion, apart from pure social UoP bonds and SLBs with social KPIs, we anticipate a greater inclusion of social considerations in labelled issuances. It will occur through the strengthening of minimum safeguards and greater disclosure on social co-benefits. Also, the growing importance of European directives on reporting (CSRD) and due diligence (CS3D) contribute to a better consideration of social issues. Therefore, the volume of social UoP bonds is only a partial indicator of the growing importance of social challenges. The latter are ubiquitous and will certainly remain a top priority in the development of sustainable finance.

[1] On April 2023, a political agreement was found on the EU’s Corporate Sustainability Due Diligence Directive (CS3D).

[2] The “type” of bonds differentiates UoP bonds between themselves (social, green, sustainable), whereas the format pertains to their underlying mechanism or configuration (Use-of-Proceeds earmarking or sustainability-linked with KPIs)

[3] All the market figures presented relate to € social bond issuances as of Friday 31st of March 2023.

[4] Mostly emerging sovereigns such as Chile, Mexico or Ecuador.

[5] EU, CADES & Unedic.

[6] CADES, UNEDIC, the Chilean Government, Deutsche KreditBank, AIB and Motability.

[7] See framework : NRW Social bond Framework, 2022

[8] See our article : Greenflation, the new normal?, June 2022

[9] IEA, Fossil fuel consumption subsidies 2022, February 2023

[10] IEA, World Energy Investment 2022, June 2022

[11] For further details, see Ukraine Sovereignty Bond, November 2022.

[12] European Commission, Press Release, November 2022.

[13] Under the European Peace Facility, see European Council, Press release, April 2023.

[14] European Commission, SURE Program.

[15] See World Bank, Updated Ukraine Recovery and Reconstruction Needs Assessment, March 2023.

[16] Including the EU, BNG, NRW Bank and the Council of Europe Development Bank.

[17] To replace eligible assets to which proceeds were allocated that would lose their eligibility, this is a common market practice.

[18] The top 5 biggest SSA issuer in sustainability bonds: Land Nordrhein-Westfalen, International Bank of Reconstruction and Development, BNG bank, International Development Association and Agence Française de Développement.

[19] It is important to note that some eligible categories referred to as “other” are accounting for 8% of the allocations. Proceeds allocation to green categories represent 41% of the total

[20] Air Liquide, EDF, Vonovia, Motability, Danone, Korian, SBB Treasury, Icade santé, Medicover and Gewobau

[21] SBB Treasury and Motability

[22] Ecuador, Mexico, Chile, Peru and Canada

[23] Source: Natixis GSH internal market data

[24] According to Morningstar

[25] See Franklin Templeton Social Leaders Bond Fund’s Factsheet (February 2023)

[26] See Threadneedle European Social bond fund’s Factsheet (February 2023)

[27] See our study: The Art of Social Bond Impact Reporting (June 2021)

[28] See Amundi’s social bond Fund Impact reporting (2021)

[29] See our article: EU Social Taxonomy Proposal: simpler and meaningful but half-way through, March 2022

[30] See the dedicated draft for European Sustainability Reporting Standards (ESRS) : S1 Own Workforce, S2 Workers in the value chain, S3 Affected communities, S4 Consumers and end-users

[31] See draft, European Sustainability Reporting Standard S2 Working Conditions, February 2022, EFRAG

[32] See our article: A growing momentum for Fair Transition Finance (April 2021).

[33] See press release (December 2021), EDF.