Launch of the long-awaited China’s National ETS market: a decisive milestone

8-minute read

After a decade of preparation and repeatedly delayed launch, China’s national Emissions Trading Scheme (ETS) officially made its debut on July 16, 2021. The national ETS market closed at CNY 51.23 ($7.9) per ton of CO2 on the first trading day. The trading volume of carbon emission allowances (CEA) reached 4.1 million tons on this inaugural day, with a turnover of CNY 210 million ($32 million). For the time being, only the power sector is covered with a first batch of emitting entities included in this ETS accounting for more than 4 billion tons of CO2, making it the world's largest ETS market by volume (with around 12% of global CO2 emissions). This launch is unarguably an excellent news in the fight against climate change. At the minimum it will increase companies’ abilities to monitor, verify and report their emissions in a reliable manner. For the time being, price levels are likely to remain low and compliance obligations are loose. However, despite low predictability on the effects of the ETS in the short-term, the scheme provides China with market engineering capacities and ability to speed up the transition at its discretion.

A decade of trial and error experimentation

China has been discussing the introduction of carbon emissions trading mechanism since 2010. Prior to the establishment of a unified national carbon market, the government launched several carbon trading pilots projects at provincial and municipal levels, based notably on local economic and industrial development and carbon emissions intensity.

With the first successful transaction on the Shenzhen Emissions Exchange in June 2013 at CNY 30 per ton ($4.5), China's carbon trading pilot regions began to operate substantially. In the following years, eight carbon-trading pilots, including Beijing, Shanghai, and others, have been launched one after another, with significant differences in their design and operations (e.g. sectorial coverage, allocation mechanisms, glut/oversupply of allowances, unintended consequences resulting from incentives to increase output, prices heterogeneity). Although the pilot ETS market has accumulated a lot of experience for the national one in terms of institutional mechanism, the pilot areas are small in volume and not too active in terms of overall participation. According to the Chinese Ministry of Ecology and Environment (MEE), the regulator of national ETS, the cumulative trading volume from 2013 to June 2021 in China's ETS pilot regions was about CNY 11.4 billion (1.5 billion euros). By comparison, in 2020 alone, the trading volume of the EU ETS market was over 200 billion euros[1].

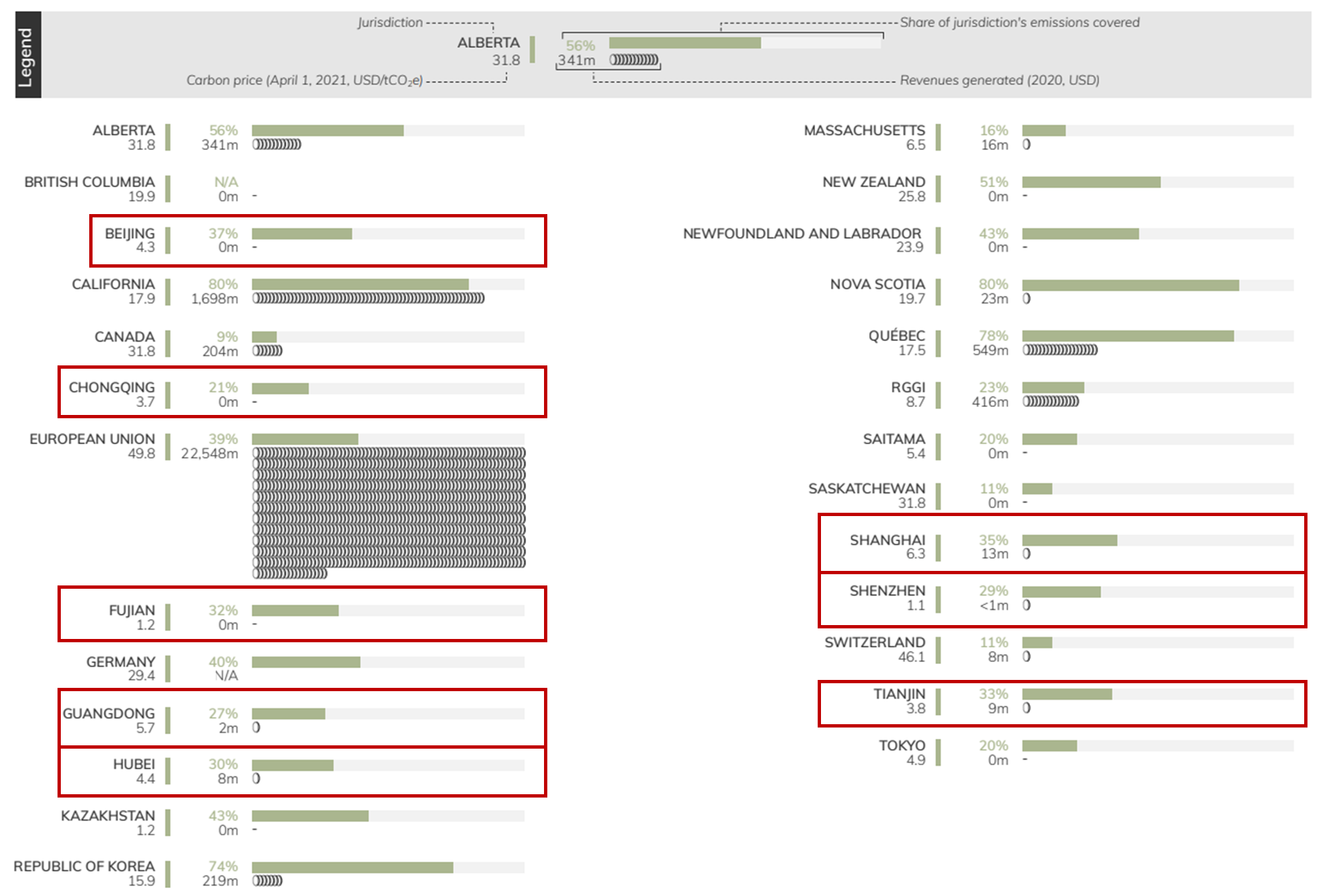

Figure 1. Global Carbon price, coverage and revenues generated by emissions trading systems

Source: World Bank, State and Trends of Carbon Prices 2021, available here.

The decision to create a national carbon market was released on September, 2015 in the China-US Joint Presidential Statement on Climate Change[2]. At that time, China mentioned planning to launch a national ETS in 2017. Since then, the construction of the relevant top-level design and supporting facilities have been in full swing. However, by the end of 2017, despite an initial framework[3], the national ETS was not ready to be launched. It was insufficiently mature and there were many ongoing debates on administrative measures among policymakers. It was only after President Xi Jinping announced the “dual-carbon” goals in 2020 (peak CO2 emissions as soon as possible before 2030 and reach carbon neutrality by 2060), that a series of breakthroughs and concrete plans were subsequently unveiled.

A National ETS mechanism with “Chinese characteristics”

The main differences between the national ETS in China and the ETS in other regions worldwide relate to emission allowances allocation methods or the scope of industries covered.

In the initial phase, due to the intended emissions reduction impact, the necessary availability and verifiability of emissions data, China’s national ETS only covers the power sector. However, the latter accounts for around 40% of national CO2 emissions. As a whole, this power sector emissions represents circa 12% of global CO2 emissions.

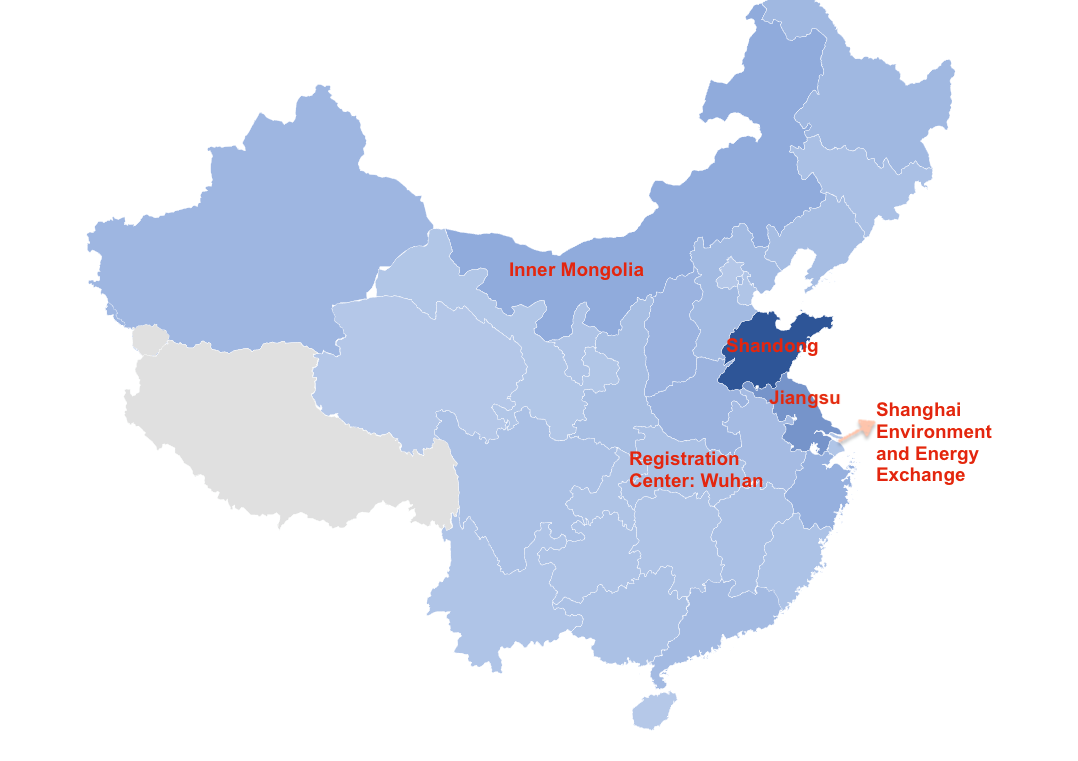

2,225 key emitting entities in the power sector with annual carbon emissions above 26,000 tons are included, concentrated in Shandong province, a traditional brown industrial hub. These entities are required to monitor, report and verify their emissions in 2019 and 2020.

According to a Carbon Brief article, available details on the 2,225 ETS sites are scarce, with only the name of the company, the provincial location and a “Unified Social Credit Identifier” (USCI), which is a unique 18-digit code used to identify business registration and taxpayers in China[4]. Moreover, a large number of industrial sites among heavy-industries such as aluminum, iron and steel are going to be indirectly impacted when they are powered by dedicated fossil-fuel power capacities (i.e. captive power plants, i.e. not connected to the general grid, these plants are also called “self-use power plants”).

[1] Refinitiv (January 2021), “Carbon market year in review 2020”, available here.

[2] China-U.S. Joint presidential Statement on Climate Change released on September 25, 2015: available here.

[3] On 18 December, 2017, China released an initial framework on national ETS: available here.

[4] Carbon Brief (June 2021), In-depth Q&A : "Will China’s emissions trading scheme help tackle climate change ?", Liu Hongqiao, available here.

Figure 2. Geographical concentration of trading participants in China's National ETS

Source: This map on trading participants in mainland China is generated by

Microsoft Bing using data and information compiled by Ministry of Ecology and Environment

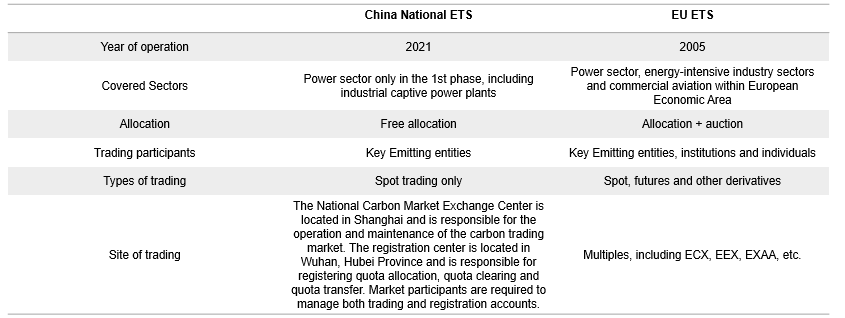

Compared to the EU ETS, the Chinese one is different in trading products, participants, and allocation:

- China's national ETS only has spot trading; nevertheless, futures and other derivatives are under consideration.

- The trading participants are limited to high-emitting entities in the power sector, whereas it is more diversified in the EU ETS (see our article this month on the Fit for 55 package proposal, with an extension of the ETS to air and maritime transportations).

- The Chinese national ETS encompasses "a flexible cap" that can alternatively increase or decrease over time, depending on the production (MWh) of the regulated sites. The current design of China’s national ETS raises concern on oversupply of electricity because the more a regulated power plant produces electricity, the more it gets permits. This is partly because China targets to reduce its intensity of emissions instead of absolute emissions for the time being.

- During the first implementation cycle, the verified allowances granted to all regulated entities are essentially determined by their electricity/heat generation outputs and the corresponding industrial intensity benchmarks. There are four benchmarks in terms of different power generation types (conventional coal-fired generators with installed capacity above 300MW and below 300 MW, unconventional coal-fired generators and gas-fired generators). In the current stage, ETS permits are completely free, auction is not yet implemented.

Also note that the existing regional pilots will continue to run in parallel of the national scheme. Their integration in it faces challenges related to sectoral coverage mismatches and different thresholds.

Table 1. China-EU ETS comparison summary

Source: Natixis GSH

Is the National ETS fit for China’s reduction targets?

When the national ETS trading went live, experts highlight its positive impact on tackling emissions reduction. The Chinese government and society have high expectations for this market-based mechanism, hoping to reach carbon neutrality before 2060 in a cost-effective manner[5]. However, as pinpointed above, the too narrow sectorial coverage, allocation method and the absence of a firm cap on emissions have drawn skepticism in the scheme effectiveness to curb absolute emissions. For the Chinese ETS scheme to become instrumental, it must be linked to the national climate ambitions with adequacy and proportionality between the official GHG emission reduction targets and the scale of emission permits in the carbon market.

Another loophole pinpointed by observers is the toothless penalty in case of non-compliance or erroneous information, with an upper limit on fines set at CNY 30,000 ($4600). In addition, China’s allocation plan set a controversial rule to relieve the compliance burden of coal-fired power plants and incentivize the development of gas-fired plants. The upper limit of compliance obligation for coal-fired power plants is at “free verified allowances + 20% of extra permits purchase”, the rest will be exempted. For example, if a coal-fired power plants exceeds its budget of allowances (provided for free) by 50%, it will only have to purchase credits for 20% of this emission excess (upper limit). For gas-fired plants, the purchase of permits above of their free verified allowance is even not required for the time being. The objective of such rule is to incentivize the switch from coal to gas. Nevertheless, a revised draft for public consultation of the management regulation on carbon emissions trading rights mention stricter fines and offenses, and proposes to integrate the record of activity in the carbon market to the social credit system. Several administrations could be involved in the supervision and guidance of the national carbon market (namely the National Development and Reform Commission, Ministry of Industry and Information Technology, and the National Energy Administration).

Regarding the sectorial coverage, the Ministry of Ecology and Environment is working to collect necessary data from seven carbon-intensive industries, namely petrochemical, chemical, iron and steel, non-ferrous, building materials, paper and pulp, and aviation. Entities in these 7 sectors are also asked to monitor, report and verify their emissions. They are expected to be included in the scope of the ETS during the next 5 years (iron and steel are likely to be the first included). The expansion of China's national ETS coverage is also an option to actively offset the potential impact of the European carbon border adjustment mechanism (see more about the mechanism in July's article on the Fit for 55).

Coupled with the fact that enterprises do not have additional costs to obtain initial allowances and the loose compliance obligation, the upward pressure on the carbon price in the short term is not significant. This may be due to the Chinese government's prioritization on stabilizing carbon price and market, which provides some time for key emitting entities to adapt to the low-carbon transition.

In the long run, the current design leaves some flexibility for future adjustments, and the government may gradually optimize the national ETS mechanism based on the operation of the first phase. According to ZHANG Xiliang, director of the Institute of Energy and Environmental Economics at Tsinghua University and major designer of China’s national ETS, the carbon price should be around $7 (about RMB 50) to $15 in 2020-2030, rising to roughly $25 by 2035, and $115 in 2050. Therefore, the cost of the national carbon market should gradually increase as the national ETS is expected to gradually tighten allowances allocation and introduce the auction as in the EU ETS.

At the initial stage of the national ETS, only spot trading is included. The pilot ETS markets have carried out a series of explorations in carbon funds and emissions allowance pledge loans, which are valuable trials for the national one. In the future, financial institutions should be encouraged to innovate carbon financial products in the national ETS market to help key emitting entities succeed in the low-carbon transition.

***

The effectiveness of current China’s national ETS requires time to be tested and constantly adjusted, just as the EU ETS has undergone more than a decade of development and adjustment. China's national ETS market is likely to mature and be coupled with other policies, such as power system reform and the continued promotion of green finance, to help achieve the carbon neutrality goal by 2060. In any case, command-and-control policies will remain decisive in China, with a high need for coordination with market-based mechanisms (see the section p.22 on policy instruments in our flagship report “Brown industries: the transition tightrope”).

[5] China released its Fourteenth-Five Year Plan in March 2021, and targeted to reduce 13.5% in energy intensity for the next 5 years and a 18% cut in its CO2 emissions intensity, available here.

To go further:

- Daily trading volume, prices and announcements tracking from Shanghai Environment and Energy Exchange: available here

- China’s National Carbon Emissions Trading Scheme Interim Administrative Measures: available here

- Public consultation on China’s National Carbon Emissions Trading Scheme Interim Management Regulation: available here