Historic deal reached on the EU recovery package and budget

6-minute read

On July 21 2020, following a marathon EU-summit in Brussels, the European Council, composed of the leader of the EU’s 27 Member States, agreed on ambitious post-Covid Recovery Plan. It brings to life, albeit with important changes, the Franco-German and European Commission’s proposal we extensively discussed last month (see our editorial “Covid-19 crisis in Europe: a midwife for a federalist green & social leap forward”).

The deal spending package worth €1.8 trillion and is composed of two elements:

- A total of €750bn package aimed at funding post-pandemic relief efforts across the EU called “Next Generation EU” (NGEU)

- The EU’s regular 2021-2027 budget is reaching nearly €1.1 trillion (so-called Multi-Financial Framework (MFF) of 2021-2027).

As expected, a number of concessions has been made to the four frugal states (namely, Austria, Denmark, Sweden and the Netherlands) - rebates and cuts to some budgets including on fair transition, health and research, being the most affected sector. Nonetheless, overall this is a landmark agreement, with a strong ESG/climate content both on the spending and resource sides. This is the first time the EU, as a block, will issue bonds (through the European Commission) at large scale to support fiscal stimulus. To pay the debts back, EU members may be inclined to concede the EU more taxing authority.

Financing the recovery plan

The financing mechanisms of the plan marks a step towards a deeper integration hailed as historic (an important step towards a federal structure of the EU). Indeed, to finance the €750 bn Next Generation EU plan, equivalent to 4.7% of the EU GDP, the Commission will be authorized to borrow funds on behalf of the Union on capital markets, using its triple-A credit rating, and the proceeds will be transferred to Union programmes. This plan has been agreed alongside the EU’s next seven-year budget worth €1.074 trn, the MFF, which will also partially support the recovery from the socio-economic fallout caused by the COVID-19 pandemic. Bear in mind that the Recovery Fund does not pool countries’ existing debts.

The funds borrowed could be used for loans up to an amount of €360 bn and for grants up to an amount of €390 bn (the most unprecedented aspect of the scheme) and the repayment, set up from 2028 onwards, is scheduled to ensure the steady and predictable reduction in liabilities until 31 December 2058. It is noteworthy that this amount of grants will somehow lead to substantial intra-EU fiscal transfers. The deal also stated that total amount of annual appropriations for commitments shall not exceed 1.46% of the sum of all the Member States' Gross National Incomes (GNIs). In terms of the repayment of the principal, the EU Commission declared that the amounts cannot exceed 7.5% per year of the €390 bn expenditure.

The European Commission will lend most of the Next Generation EU proceeds to EU countries under the Recovery and Resilience Facility (RRF), representing 90% of the total envelope of the Next Generation EU efforts. The RRF budget, disbursed as loans or grants, is to be used for investments and reforms including in the green and digital transitions (no further details provided on “how”). 70% of these grants will be committed in the years 2021 and 2022, allocation will be based on the 2015-2019 unemployment rate, Gross Domestic Product (GDP) per capita, and population share. Therefore 2021 and 2022 grants attributions will ignore the actual impacts of the covid-19 crisis despite the initial claim to support the most affected regions (as it was stated by Ms. Von der Leyen “those parts of the Union that have been most affected and where resilience needs are the greatest”). The remaining 30% will be fully committed by the end of 2023, based on other criteria that in our view partially take into account covid-19 adverse consequences such as the drop in real GDP over 2020, the overall drop in real GDP 2020-2021, GDP per capita and the population share. To ensure a legitimate usage of the funds, the European Council must approve the assessment of Member states’ plans. As a rule, the maximum volume of the loans for each Member State will not exceed 6.8% of its Gross National Income (GNI).

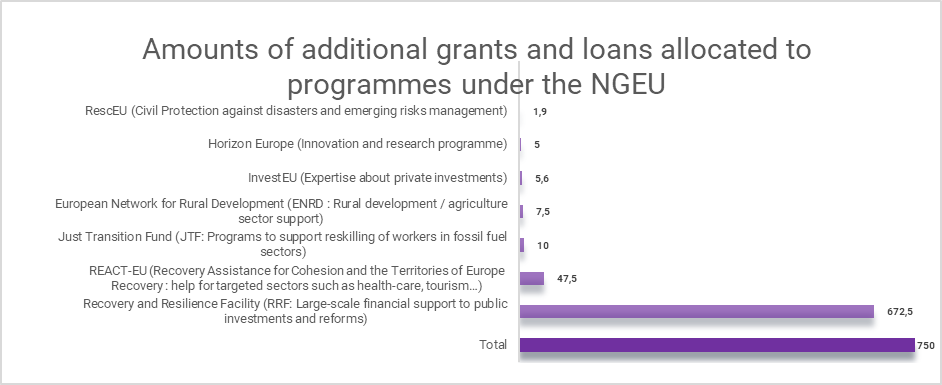

The Recovery and Resilience Facility (RRF), the EU’s flagship investment, is part of a series of European programmes under the Next Generation EU mechanism. The EU Commission has defined the budget for each of them as shown below.

Source: European Council – July 2020

Conditionalities introduced on structural reforms and respect for the rule of law

The use of the attributed European funds represents a thorny point of the deal as Mark Rutte, the Dutch prime minister, secured an “emergency brake” that would allow any country to raise concerns that another was not honoring promises to reform its economy, and temporarily halt transfers of EU recovery money by Brussels. This mechanism represents a major change in the fund attribution within the EU as the final text said EU leaders should “as a rule” take no more than three months to address any complaint to the Commission, that will take the final decision.

Another point that triggers harsh debates among the EU leaders is the link between the funds to the respect for the rule of law as respect of judicial independence in Poland and in Hungary, two countries that are both large net recipients from the European budget, is questioned. To address this issue, a group of leaders led by the Chancellor Angela Merkel and Krisjanis Karins, the Latvian prime minister, delivered a plan that would allow a weighted majority of EU governments to block payments to a country over rule-of-law violations. Therefore, a "conditionality regime" should be introduced, after negotiations that are set to begin in the coming weeks.

Green & Social resources

To facilitate the repayment of the capital raised, the European Commission will propose additional new own resources at a later stage of the 2021-2027 financial period. As thought, most of the proposals are related to ESG issues.

As a first step, a new resource based on non-recycled plastic waste will be introduced and apply as of 1 January 2021. As a basis for additional own resources, the Commission will put forward in the first semester of 2021 proposals on a carbon border adjustment mechanism and on a digital levy, with a view to their introduction at the latest by 1 January 2023. In the same spirit, the Commission will put forward a proposal on a revised Emission Trading System (ETS) scheme, and will possibly extend it to aviation and maritime sectors. Finally, the Union will, in the course of the next MFF, work towards the introduction of a Financial Transaction Tax but the discussions are still on the table. Yet, the final deal specifies that the proceeds of the new own resources introduced after 2021 will be used for early repayment of NGEU borrowing.

Climate change and social issues

The public investments and reforms funded under the Recovery and Resilience Facility aim also at achieving the objectives identified in the last European Semester, including the Green and Digital Transformation and the “Just Transition” plans.

As a general principle, say the conclusions, “All EU expenditure should be consistent with Paris Agreement objectives”. The plan itself states it has to “reflecting the importance of tackling climate change in line with the Union’s commitments to implement the Paris Agreement and the United Nations Sustainable Development Goals”. The European Commission insisted on climate action, that will be mainstreamed in policies and programmes financed under the MFF and NGEU.

At least 30% of the total amount of Union budget and NGEU expenditures must comply with the objective of EU climate neutrality by 2050 and contribute to achieving the Union’s new 2030 climate targets. This could see nearly €550 bn spending that must theoretically be taxonomy compliant over 2021-27 but the deal does not explicitly declare what mechanism will be used to ensure funding goes to climate-friendly schemes. Although there is no explicit reference to the EU taxonomy, we believe this classification is the simplest way to guarantee spending complies with the EU’s climate neutrality objective. Indeed, the technical screening criteria have been reportedly calibrated to achieve this goal. Furthermore, the European Parliament, as well as the EU Technical Expert Group (TEG) will hardly push for such use of the Taxonomy.

Indeed, the TEG has already outlined five principles that should be applied to the recovery plan:

- Plan a recovery focusing of building back better with a focus on climate change issues

- Build resilience through an economically and environmentally sustainable model

- Ensure that recover funds meet the minimum safeguards and “Do No Significant Harm” Requirements

- Apply these measures to both private and public sector

- Collaborate internationally, to create “a common global language around sustainability”

However, there are some downsides in this deal about the fight against climate change. The “Just Transition Fund”, which is part of the “Just Transition Mechanism” budget and is worth €100 bn, was attributed an additional €10 bn– which is far less than the initial €40 bn plan. This drastic budget allocation reduction highlights, to some extent, the neglect of environmental issues during the talks. The budget for other programs have also been drastically cut down such as the “Invest EU“ or the “Horizon Europe”, now in line for €80.9 billion (compared to an initial €94.4 billion plan).

There is a bit of conditionality regarding climate objectives as countries that have not signed up to an EU-wide target to become “climate neutral” by 2050 will only get half of this fund’s share. Nevertheless, the more ambitious proposal to force countries to commit to climate neutrality at a national level was dismissed.

Main concessions

To reach the agreement on the recovery plan, concessions regarding the European have been made by the French-German tandem.

Leaders signed up to cuts in top-up funding for EU programmes compared with earlier proposals in order to reach the deal. As mentioned before, some budgets allocated to some programs have decreased such as for the “Horizon Europe”or the “Just Transition Fund”, in addition to more stringent allocation conditions (introducing austerity reforms like conditionality).

Furthermore, a smaller sum, worth €390 bn, has been attributed to the Next Generation EU as the package originally proposed in May by the German Chancellor Angela Merkel and the French President Emmanuel Macron reached €500 bn.

The final deal also rules out the idea of a major €26 bn solvency instrument that would have helped to recapitalize struggling companies (and accompany European Champions and fight back hostile takeovers that threaten economic sovereignty). The “Frugals” successfully pushed for some revisions of “future-oriented” areas, such as research, health-care or climate, partially covered by these funds.

The discounts, granted to “frugal countries” were maintained and even raised compared to what was expected before the summit, meaning that for the period 2021-2027, flat-rate adjustments will reduce the annual GNI contribution of Denmark, Germany, the Netherlands, Austria and Sweden.

What is next?

The Commission requested an expansion of the “budget headroom”, namely, the gap between actual spending and the maximum the EU can raise from member states. This expansion, which will be pushed through national parliaments for approval throughout the EU, is needed in the borrowing process.

On the top of this, the European Parliament should vote to bringing the plans on to statute books (vote on the MFF not on the NGEU), and the deal needs to be ratified by the 27 EU Members. European Commission President Ursula von der Leyen said "We've taken a historic step, we all can be proud of. But other important steps remain. First and most important: to gain the support of the European Parliament.”. We can expect the European Parliament to obtain increases in some areas that suffer from budget cuts.

The implementation of the green and social measures contributing to the EU resources will be decided by the European Commission in the coming years, with evident uncertainty. The stated objective is to implement the GAFA tax and the carbon tax by 2023 at the latest.

This historic agreement transforms the EU despite some weaknesses and contradictions. Nonetheless, what is better is the enemy of what is good. Ultimately, the post-covid crisis period is a critical time for the EU since the measures can be reachable springboards for a more federalist Union. This milestone deal moved the union closer to a “fully fledge fiscal union” and would certainly help the EU turning greener and more social. Some points of the deal are still on the table and will be clarified later on this year. In such circumstances, the ratification by all EU Members, the terms of the funds attribution and the verification mechanism of the proceeds’ usage will be at the core of forthcoming European discussions.

To go further: