France strengthens sustainable funds management monitoring tools

4-minute read

Since COP21, the French authorities have positioned themselves at the forefront of a thriving sustainable finance market. As of 2015, two labels were created, the SRI Label for ESG funds carried by the Ministry of Finance and the Greenfin Label for Green Funds supported by the Ministry of Environment (formally called TEEC).

At the same time, the Autorité des Marchés Financiers (AMF) has progressively taken up the topic of communication associated with this product category and ended up with a first update of its investor information policy at the beginning of 2020.

In order to cope with an increasingly sustained market dynamics, new initiatives are to be noted in recent months, with on the one hand the review of the eligibility criteria and scope of application of the SRI label and on the other hand the review of the AMF doctrine.

Revision of the SRI Label

Four years after its launch, the SRI label has been updated, opening the way to more eligible funds and a review of its expectations on transparency, proof of ESG performance and description of shareholder engagement, changes that will apply as of October 2020.

The philosophy of the SRI label remains unchanged: a “best in class” approach, with the application of a methodology focusing mainly on the process of ESG analysis and portfolio construction (ie. elimination of a least 20% of the lowest scores based on these ESG criteria compared to fund’s investment universe). The changes focus in particular on steering and monitoring extra-financial performance: from now on at least 2 indicators chosen by the fund manager, a better result relative to the starting universe or the benchmark is required over time. In addition, engagement actions with issuers must be explained and implemented in relation to each of the ESG indicators and votes in AGM must be publicly disclosed.

After a long groundwork phase, the SRI Label is now open to real estate funds

Two new products’ categories are now eligible for SRI labelling: institutional management mandates – which must meet the same requirements as retail funds - and real estate funds for which a dedicated set of criteria has been developed.

The logic of selecting the best-in-class assets (oftentimes recently built) in the market has only limited relevance in the case of real estate funds where the question of improving the ESG characteristics of existing buildings is just as crucial as that of new constructions. Thus, real estate asset managers may choose between two methodological options:

- A selection of assets with ESG characteristics greater than minimum values defined by the management company (cannot be below minimum legal requirement) but to be legitimized by market standards,

- Or work on improving the energy performance of buildings with the objective of a minimum improvement of 20% over three years for all buildings that are below the minimum values defined above.

The real estate SRI label naturally focuses its criteria on the energy performance of buildings, but it also incorporates criteria designed to meet the ESG triptych. Thus, criteria for accessibility of buildings to public transport or more generally to all services, selection and information of tenants, requirements for comfort, safety and health of buildings, or the choice of service providers is expected to feed the “environmental”, “social” and “governance” pillars.

This framework, defined in consultation with market participants, offers the advantage of relying on existing market practices. On the other hand, it avoids the implementation of predefined thresholds or a carbon trajectory logic that would allow its requirements to be put into perspective with the current state of regulation, best available market practices, or the trajectory required to bring the profession in line with the objectives of the Paris Agreement.

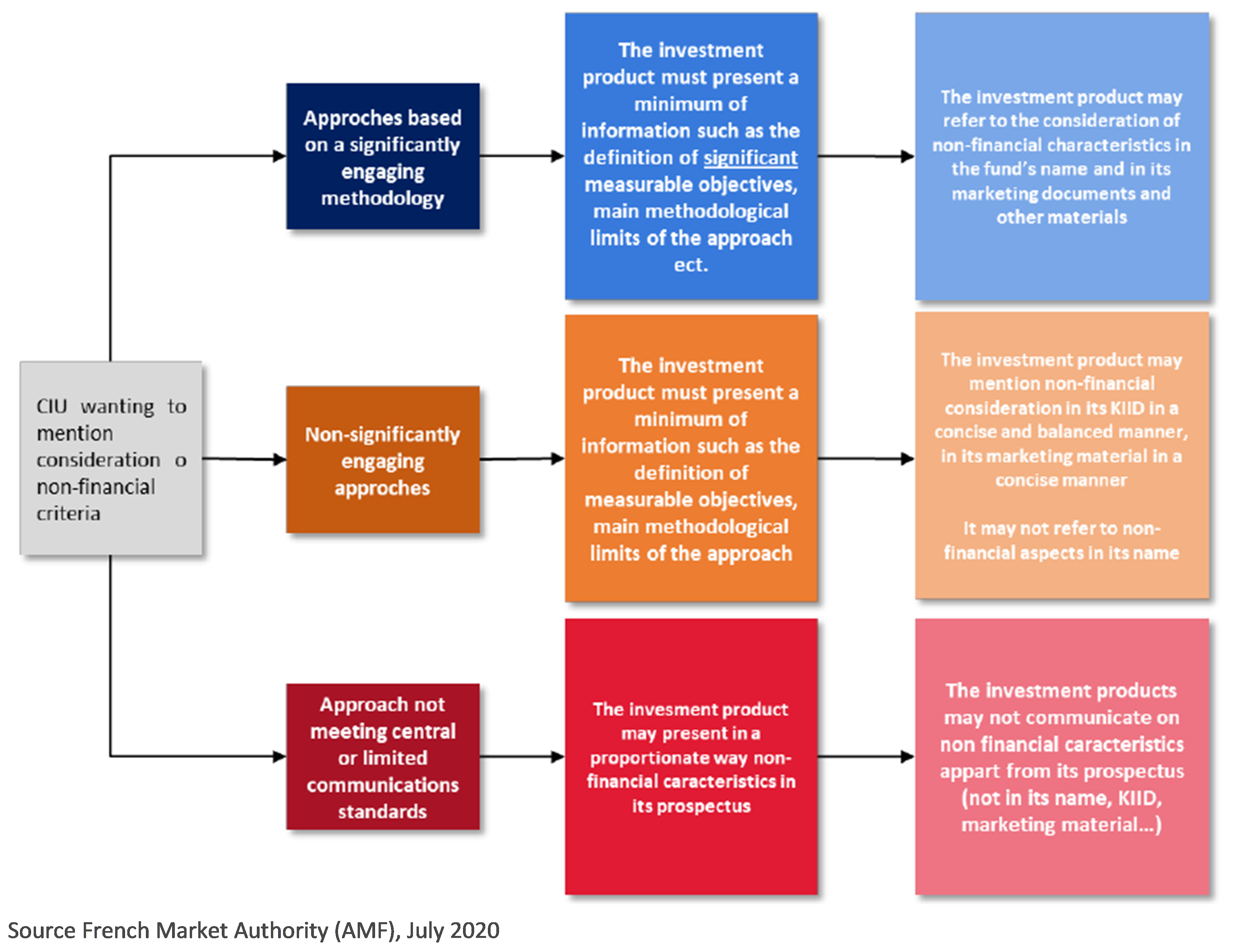

The AMF is (already) reviewing its doctrine on the terms for communicating sustainable funds to investors

Last March, the Autorité de Marchés Financiers (AMF) had unveiled an objective to limit the communication on sustainable dimension of investment products when they only differ marginally from traditional management by defining requirements to communicate significantly on the ESG (read our April 2020 article: French market authority issues a first set of requirements to control sustainable funds communication).

Four months later, the regulator is already reviewing this stance to take it one step further in its categorization of products. The two initial categories remain unchanged: on the one hand, funds which do not take into account ESG criteria at all, for which communication on the subject is banned, and on the other hand products which have the SRI Label or can demonstrate a discriminatory consideration of ESG criteria, for which the ESG communication is authorized. But the AMF now introduces an intermediate category associated with a so-called 'reduced' communication for funds that take into account ESG criteria in their management without making it a “significant” commitment.

This new granularity is certainly good news for all funds practicing ESG integration while not integrating any pre-established selection constraints. However, the threshold between non-significant commitment and absence of ESG criteria consideration remains relatively vague. The next few months will allow us to identify precisely where the AMF departments intend to set the bar… until a future review of these categories?

At the same time, in its response to the European consultation on sustainable finance, the AMF proposes to establish minimum requirements at EU level “for funds that use ESG as a central element of their communication”, on the model of what it began to implement in France. The Authority also hopes that work will be launched to develop common definitions at European level of the main concepts of sustainable management and to develop more labels for sustainable finance, in addition to the EcoLabel currently under consideration. The AMF is therefore in favour of an “ESG” label including a rating system, with the objective of “establishing a new internationally known standard” and limiting the current fragmentation of the market among the nine existing national labels.

While France has been ahead in terms of market structuring and regulation regarding responsible investment, its leadership is challenged: the SRI Label has been followed (?) by others in Europe (Belgian Sustainability Standard, Nordic Swan EcoLabel, etc.) and the European EcoLabel is expected sooner or later. And AMF attempts to regulate ESG funds communication towards investors may be soon exceeded by the various initiatives being developed by the EU Commission in the framework of its action plan on sustainable finance, as well as the revision of Shareholders and Reporting directives… This raises questions about the legitimacy of national pilot initiatives to the detriment of the EU-wide approach and risk of a duplication syndrome.