Etihad’s $600 million Sustainability-linked Sukuk: the first of many things

- 10-minute read -

Etihad Airways, the second flag carrier of the UAE, has launched the world’s first Transition Sukuk and the first sustainability-linked bond in aviation, under their Transition Finance Framework in October 2020. The Sustainability-linked bond is tied to one Key Performance Indicator (KPI): a reduction of 17,8% of its emission intensity in its passenger fleet by 2024, against a 2017 baseline of 574 CO2/Revenue ton kilometers (RTK)[1] for the total fleet.

The $600 million bond was slightly oversubscribed with an order book of more than $700 million. Etihad has announced a $3 billion sukuk program expected to be rated ‘A’ by Fitch. The issuance by the second largest air carrier in the United Arab Emirates is part of a broader strategy to support the purchase of the next generation of aircrafts and research & development programs on sustainable fuels for aviation purposes. Etihad Airways has also announced its willingness to achieve Net Zero Carbon emissions by 2050 (Scope 1 & 2) and a 50% reduction in net emissions by 2035 in a Sustainability Position Paper published in January 2020[2] which is more ambitious than the latest IATA target i.e. 50% reduction in net aviation CO2 emissions by 2050, relative to 2005 levels.

The selected KPI reflects a material issue for the issuer that is the carbon footprint of the aviation activity. This KPI is used by the International Energy Agency (IEA) and by the Transition Pathway Initiative (TPI) which explains its use as a benchmark.

Even though Etihad Airways’ 2025 targets for its emission intensity (in gCO2/RTK) are aligned with the sector’s currently defined targets with International Pledges scenario’s 2030 target, they are not in line with 2°C scenario targets. According to the TPI (which uses a science-based methodology to assess companies alignement to Paris Agreement 2°C scenario), companies’ carbon intensity should not be above 539 gCO2/RTK in 2024 and 522 gCO2/RTK in 2025 and have to reach 430gCO2/RTK in 2030 to be aligned with a 2°C scenario. In 2019, Etihad Airways’ carbon intensity was at 631 gCO2/RTK in 2019 and expected to be at 636 gCO2/RTK in 2020.

As a reminder, the International Pledges scenario is based on current commitments made by the International Civil Aviation Organisation (ICAO) and these commitments are known to be insufficient to set the aviation sector on a pathway compatible with the world of to 2°C warming or below, as aimed for by the Paris Agreement.

Aviation targets in term of intensity emission reduction

Source: Green & Sustainable Hub, Natixis (2020)

The issuer stated that the financial characteristics of the bonds will not be influenced by the achievement of the KPI and chose the “structural changes” option provided by the Sustainability-linked bond principles. Etihad Airways has committed to purchase carbon offsets if the SPTs are not met at the target observation date (i.e December 2024). One ignores precisely which type of carbon offsets, the magnitude and calculation parameters of the carbon offsetting.

To achieve these Sustainability Performance Targets, Etihad Airways will pursue three main pathways:

|

Energy efficiency |

Reduction of fuel consumption by improving the efficiency of demand side management |

Use of sustainable aviation fuels |

|

|

|

Note that Etihad Airways is also a signatory of the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) of the International Civil Aviation Organization (ICAO).

CORSIA is a global regime of market-based measures designed to offset the fraction of CO2 emissions from international flights exceeding their 2019 level. It requires aircraft operators to purchase carbon credits. CORSIA sets out two climate targets:

- Reducing almost 2.5 billion tons of CO2 in the aviation sector between 2021 and 2035.

- Mobilizing over USD40 billion in climate finance between 2021 and 2035 from the proceeds of CORSIA.

To achieves these goals, the International Air Transport Association (IATA), the trade association representing most of the world’s airlines, has defined environmental targets, namely:

- Improving energy efficiency by 1.5% per year until 2020 (In 2013, this target was raised to 2% per year, until 2050)

- Limiting the growth of air traffic emissions based on the level reached in 2020 (“neutral growth in CO2”)

- Reducing aviation's net emissions by 50% in 2050 vs 2005 levels.

Etihad Airways has also developed a partnership with Boeing focused on the Boeing 787 Dreamliner family of aircrafts in order to develop research on innovative technologies to improve flight efficiency, cut fuel consumption and support sustainable products and practices to reduce carbon emissions.

The development of Green Islamic Finance

The Etihad’s sustainability linked sukuk reinforces the development of green Islamic finance. A Green Sukuk is an investment aligned with the Shari’ah law and ethical standards. Six pioneer transactions have been observed in Malaysia and Indonesia in the Green Sukuk market. Tadau Energy in Malaysia issued a $64 million Green Sukuk in 2017 to finance a 50 MW solar project. The Indonesian government issued a $1.25 billion sovereign Green Sukuk to fund environment friendly projects in the country. All the issuances received multi-fold oversubscription by the investors.

In 2012, the Climate Bonds Initiative has launched the Green Sukuk and Working Party (GSWP) with the Clean Energy Business Council (MENA) and the Gulf Bond and Sukuk Association (GBSA) to promote and develop Shari'ah-compliant financial products to invest in climate change solutions.

Funds held by Islamic religious institutions then could contribute to the investment in environmental transition. The sustainability-linked sukuk of Etihad Airways is thus part of the emergence of a new Islamic green finance.

According to the CBI, there is a growing demand in the Middle and Far East for Shari'ah-compliant or Islamic bonds, but a shortage of product. The global Islamic finance market is estimated to be USD 2.4 trillion in 2017, marking an 11% growth in assets in USD terms according to Reuters[5]. The industry was represented in 56 countries by 1,389 sharia-compliant financial firms in 2017. The market for Islamic bonds accounted for $426 billion in deals outstanding in 2017, with 19 countries issuing sovereign sukuk worth a combined $85 billion.

The aviation industry is a hard-to-abate sector

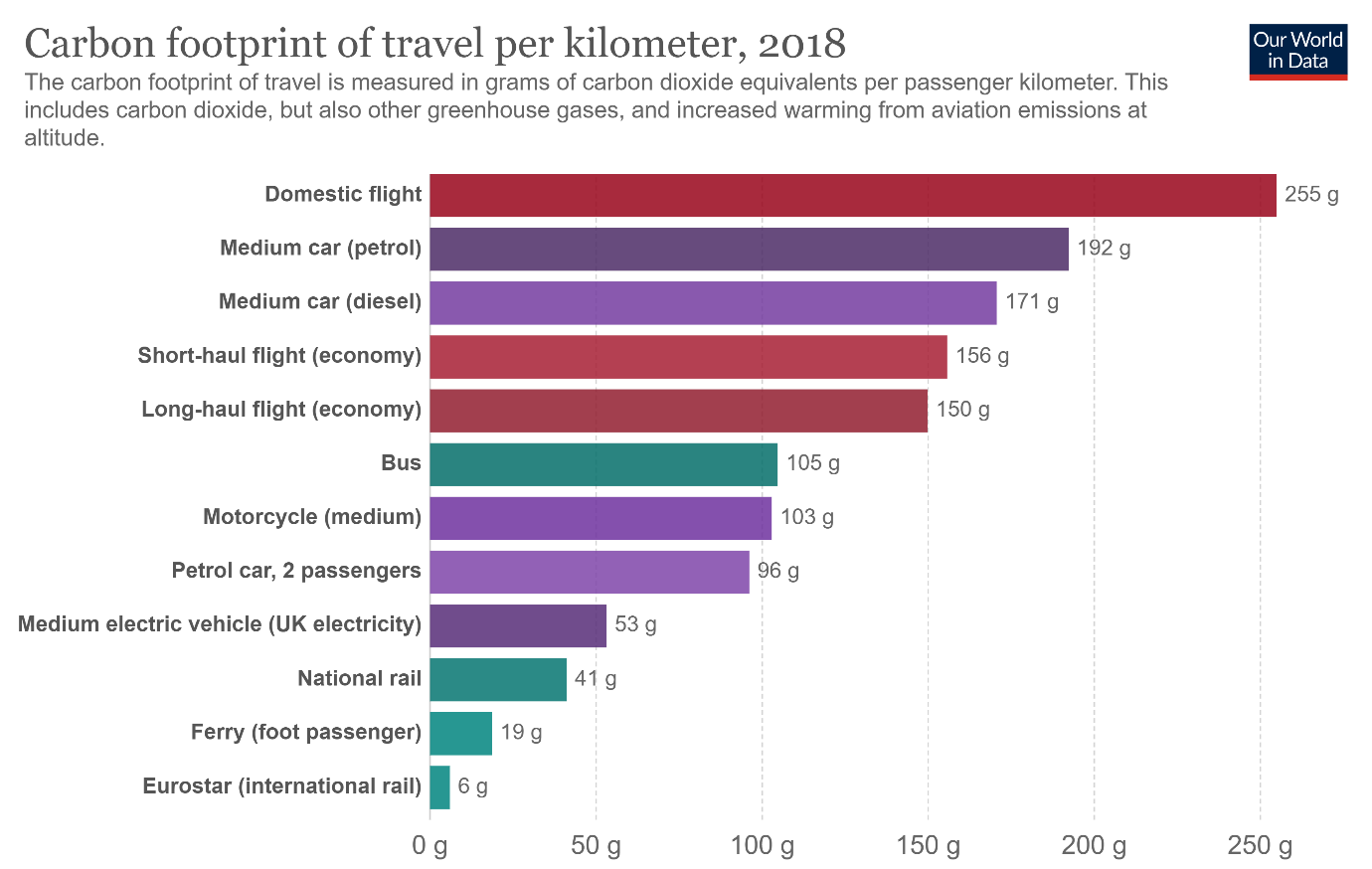

According to the Intergovernmental Panel on Climate Change (IPCC), in 2019, the aviation sector accounts for around 2.5% of the world’s emissions of CO2 and it has been projected that the industry's share of global emission may rise to 22% by 2050 if no new radical technologies or policies are introduced[6]. It is one of the most GHG-intensive mode of transport with an average carbon footprint of 285g CO2/passenger km.

Source: Source: UK Department for Business, Energy & Industrial Strategy[7]

Therefore, the sector has mechanically a key role to play in the low-carbon transition. However, the aviation industry is a hard-to-abate sector because there are currently no available options to significantly reduce the carbon footprint of air traffic in the foreseeable future. While biofuels can indeed be used to reduce the carbon footprint of aviation, blending ratios remain low. In the long run, there are two potential solutions for low-carbon aviation: electric and/or hydrogen planes. However, these are currently in the R&D stage and commercial availability could be reached within the next two decades, not sooner, according to industry actors. With the very noticeable exception of the 2020 pandemic related crisis, there has been a steady demand, driven notably by global tourism and by the economic development of emerging markets. Alternative modes of transport cannot compete with some of the key features of air transport (time saving and distance) and the powertrains of airplanes are hard to electrify in the short term at least. Hence, in the short term, operators in this industry principally turn to their own (scope 1 & 2) decarbonization as a lever to scale down the carbon emissions from their activities.

Four short-term decarbonization entry points have been identified to reduce emissions in aviation:

- Operating efficiency

- Innovative technologies

- Sustainable energy fuels

- Carbon offsetting

Analysis of the four main decarbonization strategies of the aviation industry

|

Levers |

Solutions |

Potential contribution (ICAO) |

Lifecycle CO2 emissions reduction per aircraft in % (IEA) |

Availability/ potential year of introduction |

Examples & Initiatives |

|

Operating efficiency |

More efficient operations

|

Even under the most optimistic scenario, ICAO estimates long-term fuel efficiency improvements to be 1.37% per annum. 0.98% and 0.39% from technology and operations respectively. This is lower than ICAO’s goal of 2% per annum. The IEA states that fast-tracking the renewal in the global fleet could reduce aviation’s carbon footprint by nearly 10% by 2030. |

- Air traffic management improvements: 5-10% - Increasing utilization: 3% - Early replacements of old aircrafts: 1-9% - Retrofitting existing aircrafts: 4-5% - Engine retrofits: ~15% - New-generation aircrafts: 15% |

Existing technology/ solutions, can be introduced in the short-term ~2018 - 2025 |

Safran for example has developed an e-taxiing system (unit cost is EUR1 million) that reduces 4% on fuel expenditure per flight. |

|

Sustainable energy fuels |

Sustainable aviation fuels (SAFs)

|

In the short term, 2020 scenarios result in a fuel replacement rate up to 2.6% and GHG emissions reduction up to 1.2%.To 2050, SAFs are estimated to have the potential to achieve 19% net CO2 emission reduction

The share of hybrid solutions in the aviation sector is not expected to become a significant share of worldwide commercial traffic until 2050 according to ODDO BRH. |

Synthetic fuels: 13-26% Note: current biofuel consumption is minimal and insufficient, compared to IEA’s Sustainable Development Scenario – 10% of fuel demand in 2030 |

Certain technologies need to reach industrial scale production. Others (e.g. hydrogen, non-drop-in) still in development ~2020 |

HEFA (Hydroprocessed Esters and Fatty Acids), also called HVO (Hydrotreated Vegetable Oil), is a renewable diesel fuel that can be produced from a wide array of vegetable oils and fats. It has a direct carbon footprint that’s about half that of jet fuel (40-50g C02/MJ vs 89g C02). The European Union revised the regulation on biofuels’ footprint in the REDII directive. It is being advocated that the industry focuses on the development of biojet fuel based on non-food crop. |

|

Innovative technologies |

Innovative aircraft technologies

|

Notable impact as the operation of electric or hydrogen aircraft will not be associated with CO2 emissions from fuel combustion. However, life cycle benefits also depend on whether the electricity or hydrogen is obtained from lower carbon sources |

Next-generation aircrafts: 30-70% |

Airbus E-Fan X (hybrid electric demonstrator) ready to fly in 2021, ambition to bring hybrid or fully electric technology with up to 100 sets in the 2030s ~2035 |

Airbus’ E-Fan X single-aisle aircraft is said to have a 2MW electric motor and three turbo-generators for a 100-seater craft, while an American start-up Wright Electric claims that it has filed a patent for a 50-seater all-electric aircraft. |

|

Carbon offsetting |

Market-based measures (CORSIA) – emission increases from international flights will have to be compensated for through carbon offsets |

Complements the other measures by offsetting the CO2 emissions that cannot be reduced through use of technological improvements, operational improvements and SAFs with emission units from the carbon market |

Pilot phase 2021-2023 First phase 2024-2026 Second phase 2027-2035 |

||

Source: Green & Sustainable Hub, Natixis (2020), Transition tightrope report (forthcoming)

However, the industry faced the ambiguous problem of the rebound effect. Even if the sector’s fuel efficiency has improved by 70% over the past two decades, the world annual traffic doubled between 2003 and 2018 from 4 trillion Revenue Passenger Kilometer (RPKs) to 8 trillion RPKs explaining the global aviation’s emissions increase of 0.15 Gt CO2 between 2005 and 2016.

Global emissions reduction based on Nationally determined contributions under COP 21 vs Aviation Carbon emissions based on industry target

Source: Air Transport Action Group

While Etihad Airways and other market players in the aviation sector must achieve carbon neutrality they will have to do so while facing a growing demand for air traffic. Before the Covid-19 pandemic, the International Air Transport Association (IATA) predicted continuing strong growth in global air traffic, with passenger journeys set to double from 4.5 billion in 2019 to an estimated 9 billion by the late 2030s.

Projected Air Traffic Growth according to the International Air Transport Association

Source: Air Transport Action Group

According to IATA, the COVID19 pandemic will result in a demand contraction of 66% (expressed in RPK) in 2020 relative to 2019 levels. However, even though updated statistics are likely to challenge this statement, demand levels are expected to return to pre-crisis levels by 2024, delaying the transition challenge for the aviation sector . The speed of the recovery of the aviation sector will to a large extent depend on the effectiveness and availability of Covid-19 vaccines, future lockdowns and movement restrictions and on the speed of economic recovery in main aviation regions, as well as the future of business related travels with the current development of visio-conferences. As of now (late 2020), IATA forecasts return of air traffic to 2019 levels around 2024, while most estimates given by commercial airlines fall between 2023 and 2025 range.

A demand side approach is necessary to reduce absolute carbon emission

Faced with the rebound effect and the lack of alternatives to air travel, a demand side approach therefore seems necessary.

In fact, some companies are already exercising this lever in one form or another. In June 2019, Dutch airlines (a subsidiary of the AirFrance-KLM Group) launched its “Fly Responsibly” campaign encouraging people to avoid unnecessary flights and rather use alternatives as trains when they can. Another bold move came from the Hungarian low-cost airline Wizz Air, calling on the industry to place a “… ban on business class travel for any flight under five hours”. Similarly, Norwegian has decided not to offer business class, claiming that this makes it one of the most climate efficient airlines in the world.

Political regulations can also reduce the demand for air travel. In France, the Citizens' Climate Convention, bringing together 150 citizens with the objective of making proposals to reduce greenhouse gas emissions by 40% by 2030, proposed in 2020 to phase out air traffic on domestic flights by 2025, on routes where there is a satisfactory low-carbon alternative in price and time (on a journey of less than four hours). French president Emmanuel Macron said he was in favour of a less ambitious measure concerning journeys of less than two and a half hours.

The European Union through its so-called EU taxonomy is currently working to identify potential green activities in the aviation sector. For now, in the draft of the delegated acts published by the European commission this month[9], only “low-carbon infrastructure activities” are provided with technical screening criteria. The draft defines low-carbon airport infrastructure as construction and operation of infrastructure that is required for zero tailpipe CO2 operation of aircraft or the airport’s own operations, as well as for provision of fixed electrical ground power and preconditioned air to stationary aircraft.

Two screening criteria have been selected for the contribution of the activity to climate change mitigation:

1. The activity complies with one or more of the following criteria:

- (a) the infrastructure is dedicated to the operation of aircraft with zero tailpipe CO2 emissions: electricity charging and hydrogen refueling;

- (b) the infrastructure is dedicated to the provision of fixed electrical ground power and preconditioned air to stationary aircrafts;

- (c) the infrastructure is dedicated to the zero direct emissions performance of the airport’s own operations: electric charging points, electricity grid connection upgrades, hydrogen refueling stations.

2. The infrastructure is not dedicated to the transport of fossil fuels

As previously said, as of now, few technological alternatives exist in terms of low-carbon airplane. Research & development will need funding to be developed and financial market could play a key role to support this effort.

[1] Revenue Tonne Kilometers is the revenue load in tonnes multiplied by the distance flown

[2] Etihad Airways (January 2020), Towards sustainable aviation, available here

[3] The 2 Degrees (Shift-Improve) scenario, based on the IEA’s 2 Degrees scenario, is consistent with the overall aim of the Paris Agreement to hold “the increase in the global average temperature to well below 2°C above pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5°C above pre-industrial levels”, albeit at the low end of the range of ambition. This scenario assumes that emissions reductions associated with air transport are achieved by a mixture of measures, including improved fuel efficiency, increased use of low-carbon alternative fuels, and a shift in air passenger activity to more energy-efficient modes of travel, such as high-speed rail. The assumption regarding a shift in air passenger activity to other modes of transport is contentious, however.

[4] VE (2020), SPO Etihad airways, available here

[5] Reuters (2018) Islamic finance sees mixed growth, buoyed by capital market

[6] M. Cames, J. Graichen, A. Siemons, V. Cook (2015) Emission reduction targets for international aviation and shipping, available here

[7] Remark: Data is based on official conversion factors used in UK reporting. These factors may vary slightly depending on the country, and assumed occupancy of public transport such as buses and trains.

Source: UK Department for Business, Energy & Industrial Strategy. Greenhouse gas reporting: conversion factors 2019, available here or here

[8] A320neo family The Airbus A320neo family (neo for new engine option) is a development of the A320 family of narrow-body jet-airliners produced by Airbus. Launched on 1 December 2010, it made its first flight on 25 September 2014 and it was introduced by Lufthansa on 25 January 2016. It is declared to be 15% to 20% more fuel efficient than the A320ceo family. A key contributor to the NEO’s performance is Sharklets – which were pioneered on the A320ceo (current engine option). These 2.4-metre-tall wingtip devices are standard on NEO aircraft, and result in up to four per cent reduced fuel burn over longer sectors, corresponding to an annual reduction in CO2 emissions of around 900 tones per aircraft.

[9] EC (2020), Delegated Acts of EU Taxonomy, available here