ESG Analysis of the Banking sector: From G to E?

Evaluation by investors of Environmental, Social and Governance (ESG) practices before investing or financing a company has become mainstream. The banking sector is no exception to this trend. Companies are paying increasing attention to stakeholders’ ESG scoring, and there is a distinct lack of uniformity. In order to understand investor perspectives, Natixis has conducted a series of meetings with ESG specialists from asset managers on what matters most for them when assessing a bank on its ESG practices.

Mid-March, we held the 3rd edition of our annual FIG (Financial Institutions Group) Sustainable conference where investors and bank issuers met together and addressed the current relevant topics of the sector. These meetings were focused on the bond markets, but the main elements mentioned can also be broadly applied to equity markets.

G matters the most

Analysing ESG practices of any company is now a pre-requisite before investing in either debt or equity; most asset managers form their own views based on in-house and sector specific scoring models. The implementation of SFDR further increases the need to take ESG factors into account in all investment processes and strategies.

During our discussion, investors confirmed that when they evaluate the ESG practices of a bank, the Governance pillar is given the most weight in their scoring model because of its proven financial materiality. It is also the case for most ESG rating agencies.

While all 3 ESG pillars are all taken into consideration, they are weighted differently depending on each investor’s ESG rating methodology and the grid applicable to each sector/ and sub sector. Typically, governance metrics represent about half of a bank’s overall ESG score.

Governance analysis mostly includes the consideration of two sub-pillars:

- Business Ethics: historically the banking sector has been implicated in various market-relevant governance failings (e.g., mis-selling, tax evasion under cover of banking secrecy, sanctions breaches, market manipulation & rogue trading...). Business ethics controversies are now well integrated in investors’ scoring, notably thanks to quantitative models and the assessment of controversies level of severity which are proposed by rating agencies (e.g., Sustainalytics with a 1 to 5 scale) and further qualitative assessment also conducted directly by many asset managers.

- Board Structure and Remuneration: including topics such as Executive and Supervisory Boards composition (e.g., independency and diversity of expertise, gender, and ethnicity), and particularly on ESG integration in compensation packages (alignment of incentives with management of ethics and business sustainability risks, but increasingly also transparency, relevancy, and ambition of Environmental and Social targets).

These questions are systematically addressed as part of investors overall stewardship activities and engagement practices, but also on roadshows, including credit updates.

Of note, we observe growing investor interest in gender diversity supported by new regulations and collaborative engagement. For example, the French 30% Club Investor Group was established in November 2020, when six asset management companies – representing nearly 3 trillion Euro in assets under management – came together to promote better gender diversity within the SBF 120’s executive management teams. Those companies were led by AXA Investment Managers and included Amundi, La Banque Postale Asset Management, Sycomore Asset Management, and two firms affiliated with Natixis Investment Managers, Mirova and Ostrum Asset Management.

What expectations on banks contribution to Climate action?

Climate action emergency and challenges, increased pressure from civil society, greenwashing accusations when financial institutions continue to actively finance "brown" sectors and growing disclosure requirements on ESG risks, are now on the top of “green-driven” investors’ agendas for financial institutions.

Historically environmental (as well as social) issues used to be considered less material for banks to compare with other sectors (e.g., Utilities, Industrials, Energy...). Direct CO2 emissions (scopes 1 & 2) are low for banks, coming mainly from building and employee travel footprints and scope 3 emissions are difficult to collect accurately. Other environmental challenges (such as pollution, water use, impact on biodiversity...) are historically seen as less relevant for the sector.

However, given banks’ role as major funders of the economy, they can arguably be held indirectly responsible for a large proportion of total CO2 emissions from a scope 3 perspective. As such, expectations of civil society, including NGOs, are increasing and the financial sector is seen as a powerful lever for climate action.

As of today, many investors address bank’s scope 3 emissions by considering lenders sectorial policies, and their exposure to “brown” and “green” sectors, via careful review of loan book, and capital markets activities (see our January 2022 article “Insightful benchmark of climate and fossil fuels practices of French financial institutions and corporates by the AMF and the ACPR”, available here).

From now on, it should be noted that Financial Stability Board – Task Force on Climate-related Financial Disclosures (TCFD) and Net Zero Banking Alliance (NZBA) are pushing the banking sector to make more commitments on Climate Action.

In Europe, banks are now subject to increasing ESG Pillar 3 disclosure requirements to report information about climate risks in four main categories starting in 2023:

- How banks integrate ESG considerations into governance, business, strategy, and risk management.

- Exposure to carbon-related assets and assets subject to climate change-related risks, including transition and physical risks.

- Support for counterparties through the low-carbon transition and in climate adaptation.

- Key performance indicators on sustainable finance activity based on the EU Taxonomy.

Furthermore, on a voluntary basis the Net Zero Banking Alliance initiative, launched in April 2021, represents today over 40% of global banking assets (129 banks form 41 countries for US$74trn total Assets)[1] which are committed to aligning their lending and investment portfolios with net-zero emission by 2050. Members commit to set intermediate decarbonization targets in their priority (most impactful) sectors. These targets must be achieved by 2030 at the latest and members report annually on their progress towards achieving these targets. An 18-month deadline is given from joining the Alliance to formulate and declare initial targets. As of November 2022, 90% of member banks (60 banks, over half of the Alliance) which were due to submit a target did, and over 90% of responding members report having a sectoral policy on coal and/or oil and gas financing, and have set an emissions reduction target in one, or both of those sectors. Additional targets in the nine climate-intensive sectors identified will need to follow (Real Estate, Steel, Auto, etc.).

Going forward, not being part of this alliance or not being able to respect these commitments might be negatively assessed by investors within their environmental pillar analysis framework.

In practice when investors are meeting banks, what are they talking about?

On the 22nd and 23rd of March we organized the 3rd edition of our FIG Sustainable conference. It was a unique opportunity for investors and banks to debate current sustainable topics.

During those two days, we organized 2 panels on key topics:

- The 1st panel, titled: “The end of the beginning – financial institutions taking the next steps in sustainability”, highlighted the key challenges of financial institutions on the data front: availability, accuracy, standardization, and harmonization. Panellists also discussed the relevance of existing climate change scenarios and climate risk stress tests, and the need - still under debate - to incorporate ESG/ Climate risks in prudential regulation (see our November 2022 article “Climate worst performers under strain from ECB's Green QE, collateral and parliamentary proposals for capital rules changes”, available here). A consensus has emerged, European Banking Authority (EBA) Pillar 3 disclosures (see our March 2022 article “New pillar 3 ESG risks requirements to offer a partial snapshot of banks’ transition”, available here) on ESG risks and the brand-new Corporate Sustainability Reporting Directive (CSRD), which came into force in January this year, should facilitate investors' access to the information they need to assess banks' risks arising from climate change and other sustainability issues. The panellists also highlighted the benefits of more clarity on definitions of social financing, like the existing green taxonomy.

- The second panel titled: “Beyond sustainable bonds sustainable financing strategy and products” featured a mix of banks and investors and discussed what directions they might take when looking into the future for sustainable debt issuances and investments. As the sustainable bond market matures, the question of aligning treasury strategies with overarching sustainability objectives has become key to enable financial institutions to deliver on the transition agenda. At the same time, investors are facing greater scrutiny on ESG labelling and are increasingly focused on impact and additionality.

All panellists agreed that sustainable bond penetration rates will keep growing, notably in Europe. As of today, most sustainable bonds issued by banks are green “use of proceeds” instruments. Investors expect format diversification in terms of sustainability themes (from green to social) and capital instruments (Tier 2 and AT1).

On the social side of things, it is worth noting that some “pure” social bond funds have been launched over the past two years, but the market segment is still a niche due to the lack of market depth beyond public sector issuers and the difficulties to assess real impact. As an example, the use of a beneficiary survey to assess impact is seen as a very good practice.

In term of potential future product development banks are looking at, if not already proposing, sustainability commercial paper, sustainability deposit solutions, sustainability repo, sustainability discounted loans, as well as more sustainability-themed indices, and green/social bond equity-linked products have been most frequently mentioned. From an investor point of view, product development will be linked to evolving SFDR requirements and the capabilities to increase the percentage of sustainable investment and/or taxonomy alignment commitment in funds’ portfolios.

In addition to these two panels, the event featured more than 90 investor-bank meetings, during which investors, including ESG analysts, credit analysts and portfolio managers, had the opportunity to directly ask their questions on the sustainability topics that matter for them currently.

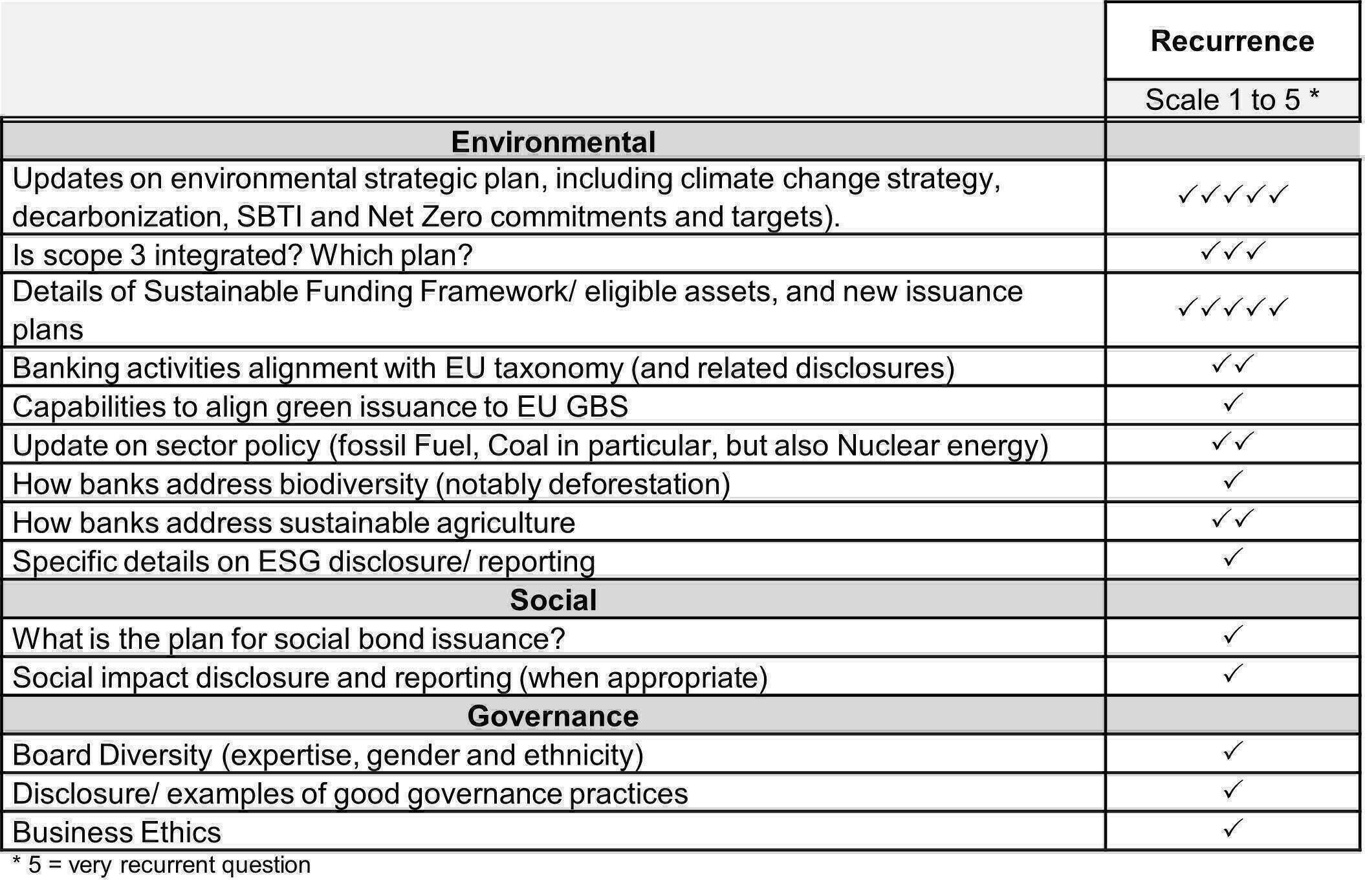

The table below attempts to summarize the different topics in the discussions:

Source: Natixis CIB GSH (April 2023), based on investors-banks meetings

Environmental topics were definitively at the heart of the discussions. Many questions were raised concerning the banks’ current environmental strategic plans: how banks meet their current commitment to decarbonization, net zero, and if any what are their future targets in the pipeline? What are the methodologies used by them to assess their carbon footprint, their clients’ sustainable performance… The inclusion or not of scope 3 GHG emissions has been raised several times as well as the percentage of banks' activities aligned to the taxonomy (see the Green Asset Ratio under EBA Pillar 3 disclosures on ESG risks).

Most of investors were also interested in an update of the existing green (or social if exists) framework to assess the overall Corporate Social Responsibility (CSR) strategies of companies (are material sectors covered?) as well as by the capability and intention of the bank to issue new green/social format and the percentage of green financing assets (including incentive for clients to progress in low carbon transition).

Last, beyond historic sector polices on controversial sectors (such as coal or oil & gas) investors are now expected banks stance on Biodiversity.

Conclusion

Beyond the well-understood risks of poor corporate governance, investors are increasingly focused on the environmental and social impacts of banks activities and recognize the role banks will play in energy and ecological transition.

In addition to understanding sectorial policies and banks’ exposure to brown and green sectors, investors are starting to integrate new data sets to assess the environmental profile of the banks in which they invest. Supporting this is a push for greater transparency on the consideration of ESG criteria in their investment strategies, particularly in the context of compliance with SFDR.

Banks' stance on other sustainable issues as human capital and natural capital will also be under greater investor scrutiny going forward. In Europe, taxonomies on sustainable use and protection of water and marine resources, transition to a circular economy, waste prevention and recycling, pollution prevention and control, and protection of health ecosystems, will help investors frame their approaches (see our dedicated article on Taxo 4 here).

Like other asset owners, banks and investment managers are now coming to understand stakeholders’ new expectations, and the risks that climate change pose to their business models. In Europe, regulatory action has hastened and formalized this process, but market pressure is also starting to show in disclosure, policies and actions. In the future, it will be necessary to measure the financial performance of economic players in the transition, starting with the financial sector, banks, and investors.