World Bank’s new SLB Platform for Sovereigns

Ahead of COP 27 starting on November 6th, 2022, the Sustainability-linked Sovereign Debt Hub (SSDH) was launched last September by several Development Finance Institutions (DFIs), including the World Bank, the European Bank for Reconstruction and Development (EBRD), the Asian Infrastructure Investment Bank (AIIB), as well as the International Capital Market Association (ICMA) and the Climate Bonds Initiative (CBI). The stated ambition is to “reshape sovereign debt market to deliver sustainability dividend”.

While total outstanding sovereign debt reached around USD 67 trillion[1] in 2022, that “cooperative space” intends to enhance sustainability risk management and support sustainable development perspectives through sovereign debt market.

Sovereign bonds market accounts for 45% of the USD 150 trillion global debt market[2]. However, while there is a growing interest for use-of-proceeds instruments (e.g., USD 108 billion green bonds were issued by sovereigns in 2021 against USD 26 billion in 2020)[3], sovereign bonds with covenants linked to sustainability performance targets remains in its infancy. There are solely two issuances. Chile was the first sovereign to issue sustainability-linked bond (SLB) in March 2022[4], followed by Uruguay in October[5] (see our article on the green, social, sustainable and sustainability-linked bond market here).

The hurdles or reluctancies expressed by sovereign debt management officers (DMOs) or officials lie in:

- The fear of target failure and the subsequent political backlash,

- Passing objectives and constraints on next governments and parliaments,

- The targets being themselves at risk of political reversal after elections,

- The moral hazard around the asymmetrical dominant mechanism (coupon step up although Uruguay issued with a symmetrical adjustment mechanism),

- Taxpayers, investors and “sustainability” interest misalignment,

- The risks of debt spiral with decarbonization failure, transition risks materialization and fiscal situation deterioration,

- The exogenous factors disturbing performance achievement and targets modeling.

However, remedies are possible: performance intervals, choice of KPIs with “constitutional” and transpartisan endorsement, innovative and balanced mechanism (step up and down, efforts strengthening), the existence of short-term and intermediary targets, technical assistance around trajectories setting and understanding. On all those aspects, the Platform can be helpful.

The Hub’s goal is therefore to provide sovereign issuers with tools and technical guidance to boost the development of sustainability-linked sovereign bonds. It will be established in the first instance for a limited four-year period.

Housed by NatureFinance, formerly known as the Finance for Biodiversity Initiative, the Hub is reportedly "intended to provide the three-fold public good of:

- “enhancing sovereign debt markets’ sensitivity to emerging [sustainability] risks;

- delivering a lower cost of capital to sovereign debtors that invest in ways that deliver sustainable development outcomes, and particularly on nature and climate-linked adaptation and resilience – the wording appears a bit peculiar, and;

- advancing innovations that make sovereign debt markets more suited to a world of external shocks.”

The cooperative space is designed to support new debt issuances over the longer-term, as well as addressing new debt issuance linked to debt refinancing. Established as a partnership-governed independent unit, the Hub will be assisted by an Advisory Board consisting of, among others, representatives of the founding DFIs[6]. Finally, a “small core team” will oversee effective execution and coordination between the partners. The Hub expects to become fully operational by November 2022, for COP27 hold in Charm el-Cheikh, Egypt.

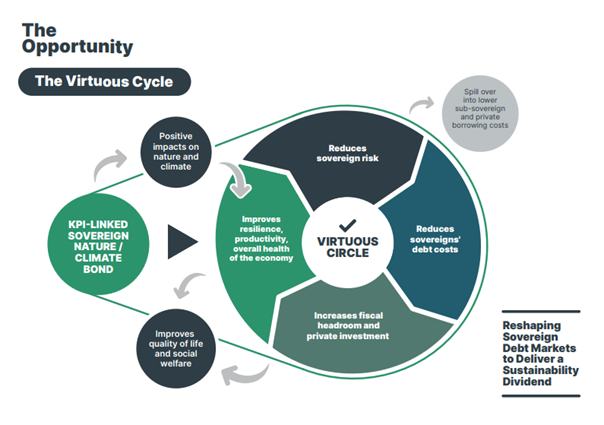

The Hub has based its approach on a “virtuous circle” (see diagram below) created through structural reforms, sustainable policies’ implementation, and financing with KPI-linked sovereign nature bond or climate bond. To such end, one expects that the Hub will identify hurdles in the issuance of SLB by sovereigns and will propose remedies per type of profiles – even though the audience is to be clarified.

Figure: the “virtuous circle” designed by the Sustainability-linked Sovereign Debt Hub

Source: The Sustainability Sovereign Debt Hub

The Hub’s ambition to encourage sovereigns to integrate their dependence on natural capital and biodiversity by designing a reliable work in the field of nature KPI-linked constitutes an opportunity to enhance countries’ risk management and increase resilience against sustainable risks. It is also predictable that opportunities for investors will arise from the initiative. According to World Bank professionals, sovereign SLBs may be an efficient and effective way of combining debt financing with ESG risk mitigation tools.

At this stage however, solely nature and climate-focused issues are mentioned. It is not specified if the Hub intends to include social and governance perspectives within the scope of guidance. It would be helpful to enlarge it to essential services access (social SDGs) because climate change mitigation is often less material for intermediate to low-income countries (considering the historic, current and GHG emissions per capita) and less under control as it is influenced by many exogenous factors (conversely to social issues such as school enrolment rate).

Interactions with other initiatives will be key, such as the Sustainability-linked bond Principles - ICMA being one of the advisory board members.

The success will be mainly assessed through the work’s contribution to:

- increasing the volume, quality, and impact of sustainability-linked sovereign debt issuance. However, targets are not set yet due to the Hub’s complex role, though it hopes to help reaching at least USD 7.5 billion of sustainability-linked sovereign debt new issuance and refinancing spread globally over the four-year period. This would reportedly ask for an estimated “pipeline of concessionary financing and credit enhancement that might amount of upwards of USD 500 million”.

- the market building (development of innovations, standards, norms). We do not know yet if the Hub intends to support the creation of Sustainability-linked sovereign bonds dedicated Standards. In the meantime, ICMA released its KPI registry in June 2022 for SLB structuring purposes (see our article “ICMA’s newly released KPI registry to discipline SLB issuances” available here) which is keen to constitute guidelines for corporates as well as for sovereigns.

- stimulate the investment to support the Sustainable Development Goals.

Note that a workshop dedicated to sustainable finance in emerging markets will be organized during our Green Summit taking place on November 29th. An open stage dedicated to SLB will also touch upon the very limited presence of sovereigns on this market segment for the moment (you can see the program of the summit and register here to the workshop).

[1] According to Bloomberg’s data.

[2] According to Bloomberg’s data.

[3] According to Bloomberg’s data.

[4] Chile issued USD 2 billion 20-year SLB.

[5] Uruguay issued USD 1 billion 12-year SLB.

[6] The World Bank, the European Bank for Reconstruction and Development (EBRD), the Asian Infrastructure Investment Bank, the Asian Development Bank (ADB), the International Capital Market Association (ICMA) and the Climate Bonds Initiative (CBI).