Updated Common Ground Taxonomy, the crowbar of international green capital flows?

6 - minute read

The EU-China Common Ground Taxonomy (CGT) has received plenty of attention from international capital markets and policymakers since its initial release in November 2021. Some Asian market participants have started to label green financial products as CGT-aligned. Seven months after the 1st disclosure of the CGT, the International Platform on Sustainable Finance (IPSF)[1] taxonomy working group issued an updated version on June 3, 2022.

In addition to the updated Instruction Report and Table of Activities, the new deliverables include 1) a Frequently Asked Questions (FAQs) section both in English and in Chinese providing users with an overview of the CGT, and 2) a Summary of consultation responses. Natixis together with its parent company BPCE participated in the consultation process. The CGT is recognized as a remarkable trial in fostering international cooperation in sustainable finance, despite its shortcomings in usability still lingering after this 1st update (to recall more details on the 1st version of CGT, we invite you to read our previous article).

Unique features to enable taxonomies harmonization

The groundbreaking work of the CGT aims at improving the comparability and interoperability of taxonomies around the world, the guiding principles and methodologies designed for CGT stick to this purpose. The unique International Standard Industrial Classification of All Economic Activities (ISIC)[1] sector classification mapping methodology is the first critical step toward comparable taxonomies. The ISIC-based CGT accommodates the discrepancies in the economic development model and industry structure across economies, with flexibility to expand the breadth of taxonomies comparison. With this underpinning ISIC sector-mapping methodology, the CGT creams off merits from the EU and China taxonomies and follows 4 major principles in activities selection and technical screening criteria setting:

- Science-based, which is the undisputable cornerstone for the development of taxonomies.

- Key industries’ priority identification to address climate change mitigation activities, reflecting the common high impact sectors between the EU and China.

- Stringent technical screening criteria prevail in the scenario alignment analysis. However, the stringency in terms of criteria and granularity of activities covered are sometimes mixed up, which needs to be distinguished to enhance the clarity.

- Include activities beyond the ISIC codes but contribute to climate mitigation. Considering the indispensable role of technology innovation in the transition, the CGT singles out two innovative technology activities in the “Other Category”, namely “Underground permanent geological storage of CO2” and “Hydrogen storage”, in addition to the six macro sectors. It leaves room to embed other activities that do not fit easily with ISIC codes in the future.

As technology advancement and development models shift, the taxonomy should not be static but evolving over time. However, few taxonomies include this feature[3]. The CGT factors in the evolving nature of our global economy and is planned to be updated regularly. With the evolving feature, IPSF taxonomy working group plans to include the official taxonomies from other members in the CGT, such as Singapore’s Green and Transition Taxonomy[4] .

The updated Common Ground Taxonomy partially responds to the concerns of the public

This Common Ground Taxonomy is much welcomed as the first effort for “apples to apples" taxonomies comparison and to mitigate taxonomies fragmentation across jurisdictions. The majority of respondents to the public consultation solicited by the IPSF expressed concerns about the usability and expected various types of extensions of the CGT. The below table summarized the common feedback from respondents as well as views from Natixis.

Table 1- Summary of the public consultation of CGT

|

Common feedback from respondents |

Reflection in the updated CGT |

Natixis’ point of views |

|

Question on the practical usability in general |

|

|

|

Additional eligible activities and objectives |

|

|

|

Other taxonomy features |

|

|

Sources: Author based on Consultation Responses to IPSF Common Ground Taxonomy, available here.

Compared to the first version of the CGT, the current version includes 17 new economic activities[5] in manufacturing and construction, as well as an extended appendix. The proposed amendments remain a small step towards a more usable and market acceptable CGT. The changes and improvements are not significant enough and usability concerns from stakeholders remain. The working group might need further work to gradually complete the “to-do list” while taking the evolving nature of taxonomy into account.

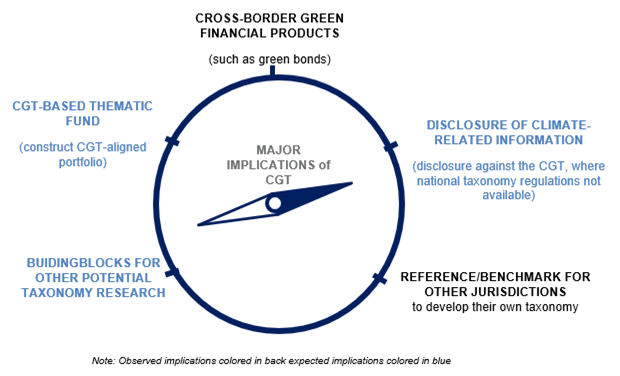

Greater influence and implications in Asian economies than in other regions

The CGT is well received by market participants especially in China, notwithstanding the slight limitations of CGT itself. Chinese FIG issuers have started labelling their green bond issuances as “CGT aligned”. China Construction Bank took the lead in issuing the first ever offshore Common Ground Taxonomy aligned floating green note in December 2021. More recently, in June 2022, Bank of China Frankfurt Branch issued the first 3-year 500m USD green bond based on the Common Ground Taxonomy Updated Version. Natixis acted as the joint bookrunner for these two inaugural transactions. Despite the challenging market environment, the CGT-aligned issuances are attractive to investors[6]. Although we have not observed any CGT-aligned green panda bond issuances from European market participants so far, the up-to-the-minute China Green Bond Principles[7] allowing overseas issuers based on the CGT would set the stage for green panda bonds. With the enforcement of SFDR Article 8 and Article 9, investors need to report the taxonomy alignment figures. As such, a CGT-based financial product would eliminate the concerns regarding misalignment and soften the complexity of gap analysis. Another envisaged implication of CGT appears in disclosure. Chinese listed enterprises and financial institutions may consider voluntarily reference to the CGT as the basis for sustainable business activities disclosure. Other jurisdictions without established taxonomies may also disclose against the CGT in the future – making it a reference in the market.

Primary users of the CGT also include sovereigns such as national governments or regional bodies looking for toolkits or guidance to develop their own taxonomy. The Sri Lanka Green Finance Taxonomy[8] is an example. It follows the IPSF and UN-DESA’s high-level recommendations and the activity description benchmarks at CGT, making its taxonomy internationally comparable and interoperable from the outset. Countries can design their taxonomies in line with the best international practices while integrating local context. Another example would be Hong Kong. The Green and Sustainable Finance Cross-Agency Steering Group, co-chaired by the Hong Kong Monetary Authority and the SFC, has announced its plan to align with the CGT with industry practitioners, experts and stakeholders last December. The position of Hong Kong as the international financial center and gateway for green capital flows between Mainland China and the rest of the world confirm it will be deeply influenced by the CGT. Hong Kong Green Finance Association (HKGFA) released the 1st phase research report[9] last month, discussing the market reaction, fundamental principles, and hurdles to adopt the CGT. The challenges are partly derived from CGT’s outstanding blemishes, pronounced ones include usability, especially on data availability, and missing features such as DNSH. However, the CGT is a living document, with continued work from IPSF taxonomy working group, the respective development of taxonomies across jurisdictions and standardized disclosure requirements with quantitative measurement capacity building, the challenges will not always be here.

Graph 1: Major implications of CGT

Source: Natixis GSH

The updated version of Common Ground Taxonomy does not contain yet instrumental breakthroughs, nonetheless, the work has roughly met the intended objectives at this stage. In the past few months, we have observed valuable discussions on more harmonized taxonomy, CGT labelled financial products and CGT-based taxonomy development, yet its observed implications are mostly restricted in Asia. To lever more substantial green capital flows in Asia and the rest of the world, the envisioned future work has to be completed. A joint effort will be needed from the entire sustainable finance ecosystems, the IPSF working group itself cannot solely achieve them. While the process will be strenuous, having already issuers using the CGT as a reference provides it with a good momentum and hope for its future development.

[1] IPSF is a multilateral forum that aims to enable exchange of practices and increase international cooperation on sustainable finance related matters. Members of the IPSF include EU, China, Singapore, Japan, and India etc., representing 55% of global GHG emissions and 55% of global GDP.

[2] Since the United Nations issued the initial draft in 1948, more than 100 countries around the world have developed their own industry classification standards based on ISIC, including the EU and China. It enables the jurisdictions to classify green economic activities by using the same language.

[3] The EU Taxonomy contains the evolving nature in design, the underlying technical screening criteria outlined in Delegated Acts are subject to review and modification.

[4] Singapore Green Finance Industry Taskforce (GFIT) published the second public consultation paper for the taxonomy in May 2022. Available here.

[5] The CGT Activities’ Table expands from 55 activities to 72 activities at present.

[6] Subscription of over 6.0x covered for BOC Updated CGT-aligned issuance

[7] China Green Bond Standards Committee chaired by the NAFMII released the China Green Bond Principles on 29th July. It will be serving as a voluntary principle and aims to promote the standardization of China’s green bond market. It is noticeable that the new principles require the proceeds must 100% allocate to green projects, regardless of the types of the green bond. Available here.

[8] Sri Lanka Green Finance Taxonomy, May 2022, available here

[9] CGT Research Series Phase 1: Principles for advancing the adoption of the Common Ground Taxonomy in Hong Kong SAR and the Greater Bay Area, HKGFA, June 2022. Available here.