The global race to net-zero: what about hic et nunc decisions?

14-minute read

China’s recently disclosed ambition to become carbon neutral by 2060[1] and to reach its GHG emissions peak before 2030 has been hailed as a potential game-changer[2]. Similar net neutrality announcements are piling up with subsequent risks of “net neutrality washing”. As of November 2020, more than 110 countries had stated their ambition to become carbon neutral between 2040 and 2060. These countries represent in total around half of the world's GDP and global CO2 emissions. They include all the G7 countries and half of the G20 countries (see Figure 1: Countries with carbon or GHG neutrality targets)[3].

Under the international Paris Agreement, several countries have communicated their long-term decarbonization strategies, notably through their Nationally Determined Contributions (“NDCs”) submitted to the United Nations[4]. The Article 4 of the Paris Agreement refers to the concept of “neutrality” defined as the “balance between anthropogenic emissions by sources and removals by sinks of greenhouse gases in the second half of this century”. NDCs are meant to be strengthened regularly as part of a “ratcheting ambition mechanism”.

Nevertheless, all targets and carbon-neutrality announcements do not have the same weight and value. In fact, they vary according to their level of granularity and precision but above all their binding nature and associated implementation means (i.e. whether they are political announcements by heads of State or governments, or bills voted by parliaments). When such targets are enshrined in “hard law” and on the top of the hierarchy of laws, constitutional courts or administrative tribunals can censor infrastructure projects, contracts or budgetary laws in case of infringement.

When supplemented with time-frame national strategies and associated fiscal expenses, the effectiveness of net neutrality targets is stronger. However, such targets often set by mid-century are toothless without intermediary milestones. They vary as well in the perimeter, most of the targets covering only CO2 emissions, with a minority covering all GHG emissions such as methane and HydroFluoroCarbures (HFC). Imported emissions or zero imported deforestation[5] are nascent notions that are starting to be included in climate strategies. Lastly, baselines and end-year targets vary although most countries’ net neutrality targets are set by 2050 in coherence with the Paris Agreement.

However, as a result of our collective incapacity to reverse the trends of absolute emissions that have been increasing since 2015 (2020 being an exception because of the economic recession triggered by the COVID-19 pandemic and lockdown measures), the 2050 deadline to become net neutral is arithmetically already obsolete. Between 2010 and 2019, global fossil CO2 emissions have increased by 0.9% per year[6]. The 2050 target to become net neutral will be reassessed and set earlier, likely around 2040, depending on our carbon budget exhaustion speed. Indeed, as emissions have exceeded the “allowed” global carbon budget for 2015-2020, the deadline to become carbon neutral approaches and the hypothetical carbon budget for 2020-2050 becomes tighter.

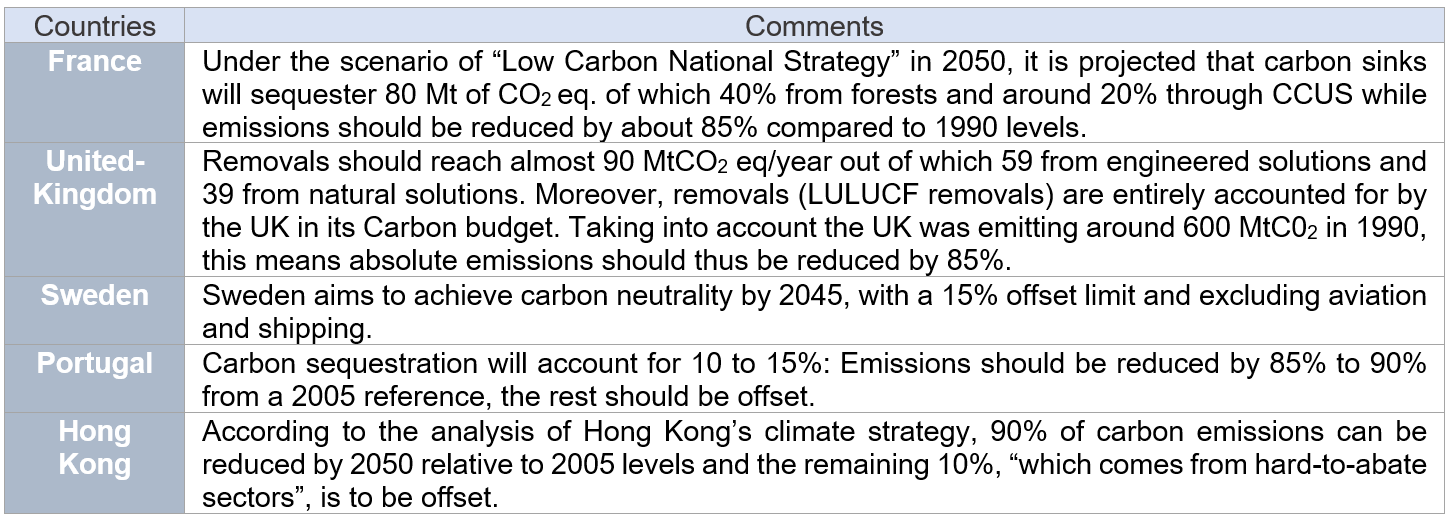

The table below summarizes some of the nations’ targets:

Table 1: National carbon or climate neutrality targets

Sources: National websites, press releases, OurWorldInData (2018)

Figure 1: Countries with carbon or GHG neutrality targets

Source : Natixis GSH

1. The NDCs, the political instrument defining Parties’ ambition

The Nationally Determined Contributions (NDCs) [7] are at the heart of the Paris Agreement. NDCs embody the highest possible efforts by each country to reduce national emissions and adapt to the impacts of climate change. The current round of NDC updates plays a critical role as more demanding targets can create favorable policy context towards climate neutrality. Indeed, an NDC-enhancing mechanism with a ratcheting effect is necessary as the actual level of NDCs (as of September 2020) leads to a 2.6°C scenario if the pledges are met (something uncertain). In theory, NDCs are submitted every five years to the UNFCCC secretariat and all Parties were required to submit the next round of NDCs by the end of 2020.

As of December 2020, 188 parties have submitted their first NDCs, out of which, 126 countries have stated their intention to enhance ambition or action in updated NDCs (including the European Union), representing 44.6% of global emissions. 19 countries (9.5% of the global population, covering 14.2% of the global emissions) submitted a new or updated NDC.

Some of them have submitted an updated NDC that does not increase the climate ambition of the country (for example, Japan and Singapore’s NDCs in March 2020, New Zealand’s NDC in April 2020) [8]. Brazil’s updated NDC targets (Dec 2020) to reduce emissions by 37% and 43% from 2005 levels by 2025 and 2030 respectively are unchanged on paper, but an increase of emissions in the base year used as a reference means that Brazil can continue to increase its emissions and still meet its targets. The emission levels in the base year, 2005, were 2.1 GtCO2e in the first NDC but increased to 2.8 GtCO2e because of methodological changes in the emissions inventory. Russia formally submitted a new NDC in November 2020 that did not strengthen the country’s 2030 target, as it is higher than Russia’s own 2030 emissions projections under current policies [9].

2. The need for intermediary targets and carbon budgets consistent with net neutrality goals

Few countries set intermediary targets of GHG emissions reduction, and when they do so, their reference dates sometimes differ as is the case for Brazil whose reference year is 2005. Chile set itself a carbon budget of 1,100 Mt CO2eq for the period 2020-2030, with a peak in 2025 while China plans on peaking its GHG emissions by 2030.

Countries set their intermediary targets according to their economic development scenarios and gauge their targets’ parameters accordingly (year of reference, emissions peak year). Indeed, setting intermediary targets and their subsequent reference dates can be very much linked with the trend of GHG emissions in a given country, whether it is on an increasing or a decreasing pathway: some countries like France, Germany and most EU countries already “peaked” while Chile and China for instance are yet to peak in terms of GHG emissions. This dynamic in the structural evolution of GHG emissions evolution in a country is itself linked to the stage of development of countries in terms of GDP but also other factors such as demographics.

The carbon neutrality objective is global in nature, it does not involve that all countries would need to reach it within their boundaries at the same date and with the same policies (in that sense, the 2060 year chosen by China reflects that view). The principle of equity and common but differentiated responsibilities and respective capabilities is crucial. It requires to take into account local context, historic and per capita emission that are strongly correlated to economic development.

Moreover, a five-year time interval between decarbonization targets appears as a prerequisite to track actual progress and assess consistency and credibility of pathways meant to lead to net zero situation. Such short-term interval and regular reviews are necessary to continuously adjust efforts.

On the different proxies and ways to express decarbonization strategies, setting pluriannual carbon budgets rather than reaching a certain amount of annual emissions at a set date is a more stringent and comprehensive tool. Due to the long life cycle of GHG in the atmosphere, the absolute volume of emissions during a set period – often over five years – makes more sense and is a way to set targets that are achievable on even shorter terms and that are closer to the length of a political mandate.

However, even fewer countries set carbon budgets in a such manner. According to the abovementioned Canadian Net-Zero Emission Accountability Act, the Canadian government is to prepare and design carbon budgets starting from 2030. France and the UK [10] already set pluriannual carbon budgets (see figures 3 & 4). Both countries break these carbon budgets down by sector.

Over time, one expects the merger of pluriannual budgtary laws and pluriannual carbon budgets, both being assessed by independent bodies, in terms of consistency and credibility (the sincerity of budgetary forecasts is assessed by constitutional courts, the same reasoning could apply to carbon budgets).

Figure 2. Distribution across sectors in the carbon budgets of France (2015-2033)

Source: French Ministry of Ecological Transition, National Low Carbon Strategy Project (December 2018), available here.

Figure 3. UK Carbon budgets and total annual GHG emissions (2008-2032)

Source: Institute for Government Analysis, BEIS (February 2020), available here.

3. Neutrality targets must be implemented through sectorial measures

In addition to national neutrality targets and the need to break them between sectors and over shorter timeframes, several countries are proposing sub-sector goals or implementation measures, for instance plans to phase out coal. France commits to phase out its coal power generation capacity by the end of 2022. In late 2016, Canada announced that it would remove coal from its energy mix by 2030. Germany has always been a leading European coal producer and a country where coal represented between 40 to 58% of the power generation mix from 1990 to 2016 according to the IEA. Germany had an installed capacity of 48 GW (almost evenly distributed between hard coal and lignite) in 2019 and plans to phase out all its 146 coal-fired power plants by 2038 (more information about Germany’s installed capacity here). Denmark renewed its commitment to phase out coal use by 2030 at the COP23 conference in 2017, after the target was temporarily abandoned by the government in 2015. However, the three main producers and consumers of coal, China, India and the USA, which account for more than 65% of global coal consumption for power generation, have not yet committed to phasing out coal production [11].

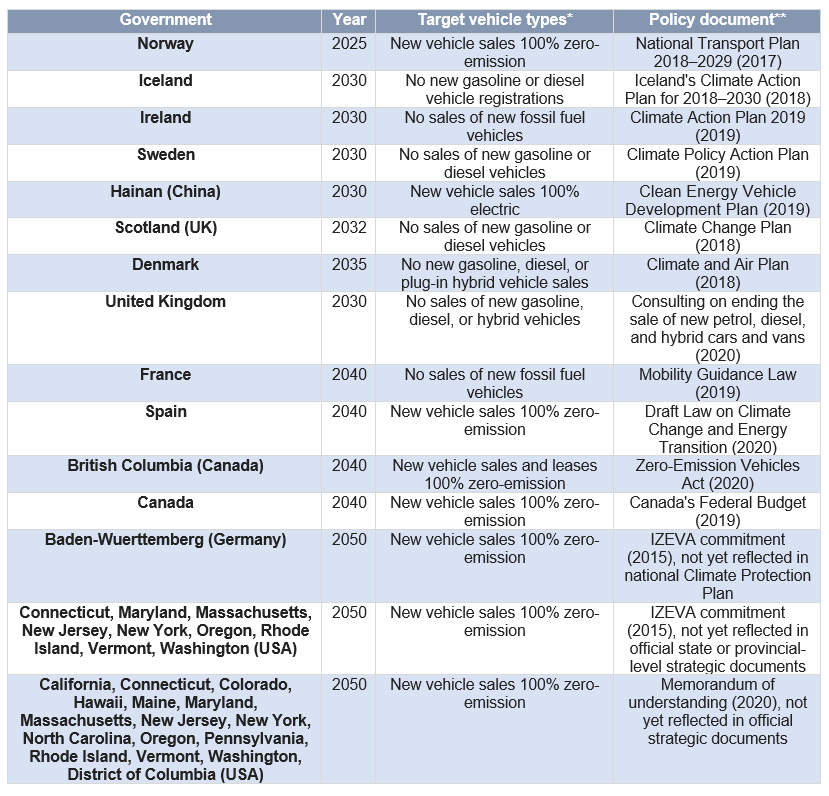

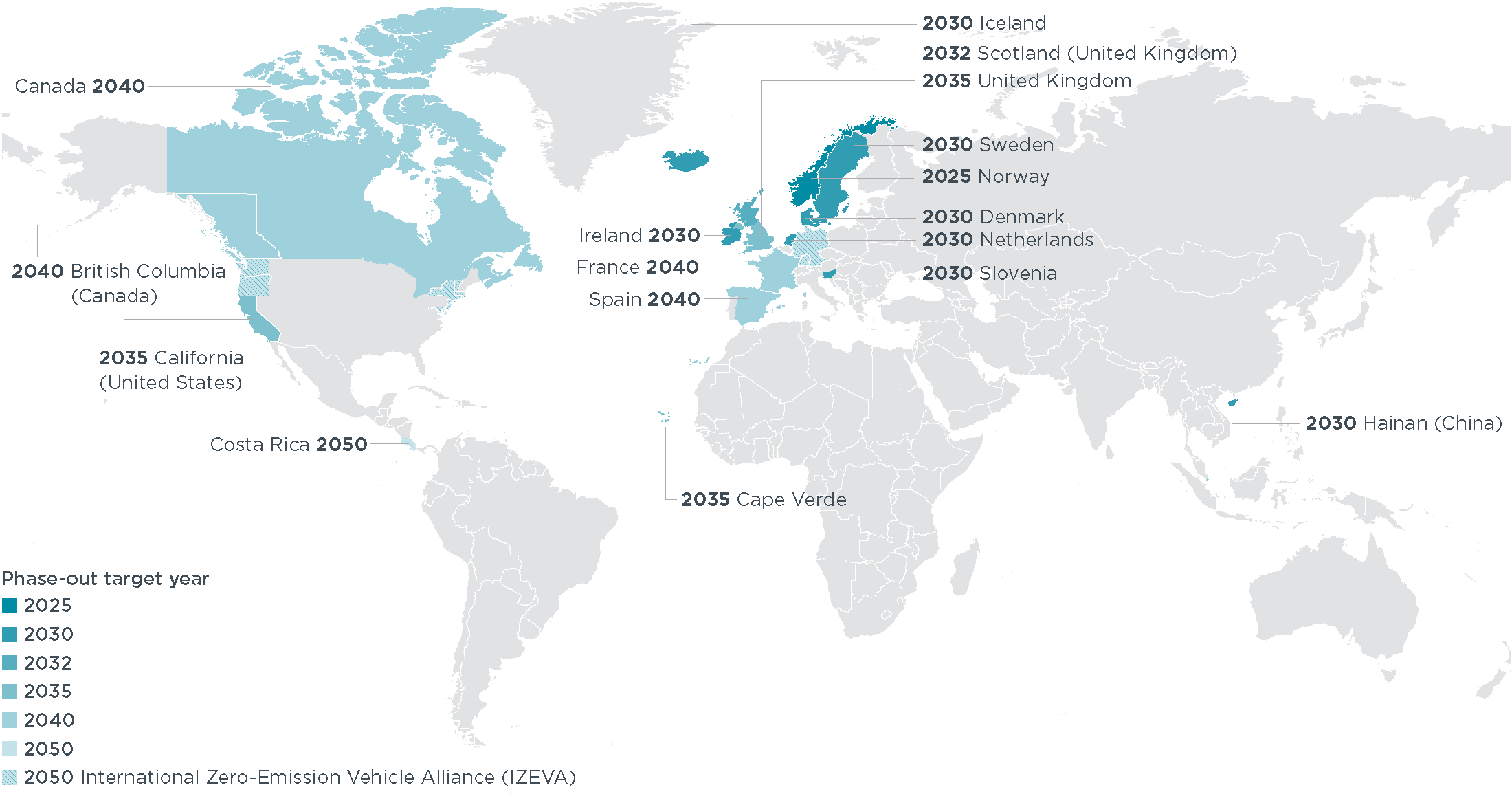

Other common measures to reach neutrality are bans on the sales of new internal combustion engines (ICE), at either the national, provincial, or city level. For instance Canada, Denmark, France, the State of Baden-Wuerttemberg in Germany, the province of Hainan in China, Iceland, Ireland, Norway, Spain, Sweden, the UK, and the 12 U.S. states that have adhered to California's Zero-Emission Vehicle (ZEV) Program have all set concrete targets to phase out sales of new ICEs. The deadlines are set up between 2025 and 2050 for these jurisdictions (see Table 2). Some of the largest vehicle markets such as the United States, China, or Germany have not yet officially announced plans to phase out combustion engines in passenger cars. However, Germany implicitly agreed to phase out combustion engine vehicles by 2050 by becoming a member of the Zero-Emission Vehicle Alliance (IZEVA), which brings jurisdictions to expand the ZEV market and work on ZEV policies and deployment. Meanwhile, China is already quite far ahead in terms of electrifying its bus fleet. Indeed, in 2019, 96% of new bus sales were electric vehicles in China.

Table 2: National, provincial, and state government targets for phasing out sales of new ICE vehicles or setting targets for 100% electric vehicle share of new sales, registrations, or imports up to 2050

Source : The International Council On Clean Transportation (Nov. 2020), available here

*Terminologies used in official policy documents

**Publication date

Source : The International Council On Clean Transportation, available here

4. The devil is in the detail of the targets

Several national targets do not apply to all GHG and only cover carbon dioxide emissions (see table 1). As a reminder, carbon dioxide accounted for around three-quarters (74.4%) of GHG emissions in 2019. Methane contributed 17.3%; nitrous oxide, 6.2%; and other emissions 2.1% (such as HFCs, CFCs, SF6) [12]. Methane and other gases emissions are rising (global methane emissions have risen by nearly 10% over the past two decades [13]) and could jeopardize the achievement of the Paris Agreement goals. In general, sensing the concept of climate neutrality entails addressing a much more complex accounting of life cycle emissions and removals compared to the measurement of gross CO2 emissions. Indeed, if carbon neutrality is achieved at a given date – which is the main goal of most governments as well as the most easily understandable and accessible concept of GHG targets – its meaning and impact on climate is weak: the accumulated emissions and the GHGs that will also be emitted from now until 2050 for instance will have more of an impact on the concentration of CO2 in the atmosphere than the anticipated balance between emitted and compensated emissions starting from 2050.

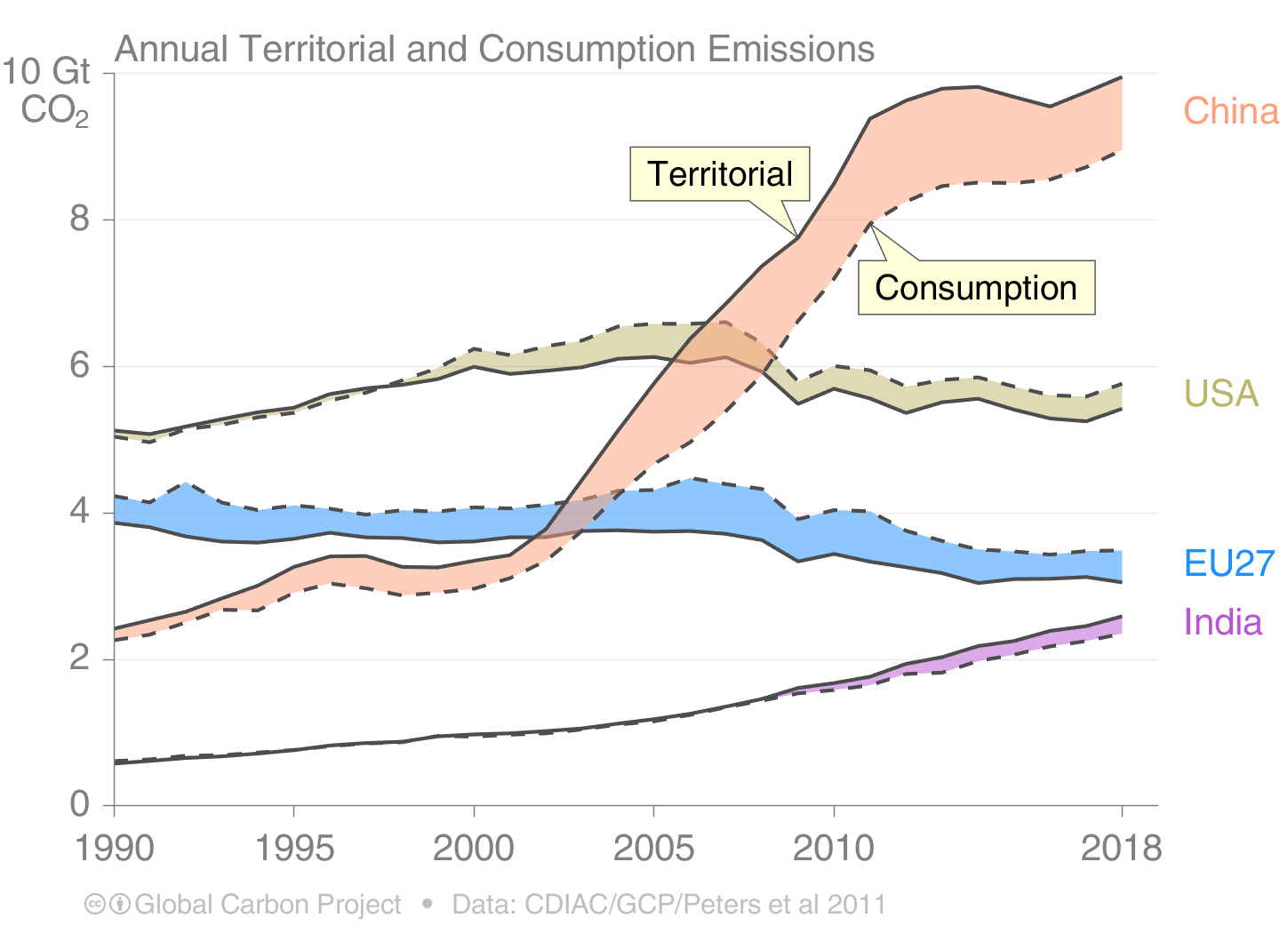

Another major variable when setting targets is the perimeter of emissions covered. Nations can either set a net-zero objective in terms of domestic emissions “territorial emissions” or look for a net-zero “carbon footprint” (by subtracting CO2 export-related emissions to the domestic ones, and adding import-related emissions), or “climate footprint” (including all export and import-related GHG emissions). Furthermore, international aviation is very often not accounted for in these objectives. Although imported emissions or zero imported deforestation are increasingly included in the debate, most of the targets’ perimeters are expressed in terms of domestic emissions.

Figure 5: Consumption-based emissions

Annual territorial & Consumption emissions

Source: Global Carbon Project (December 2020), available here.

Countries should not turn a blind eye to their responsibility for carbon emissions through import activities. Ideally, targets should allocate fossil CO2 emissions to consumption to better reflect the efforts and action needed for each country to reach the global balance. As shown in figure 5, the USA and EU27 countries are net importers of embedded emissions, China and India are net exporters.

Even domestic emissions targets lack details and harmonization among countries. Several NDCs do not cover emissions from highly polluting sectors. UK’s NDCs exclude emissions from international aviation and shipping from their perimeter. Some NDCs include Land Use, Land-Use Change, and Forestry (LULUCF) emissions and removals (New Zealand, Vietnam), whereas others do not clearly target the contribution of LULUCF (Brazil, for example).

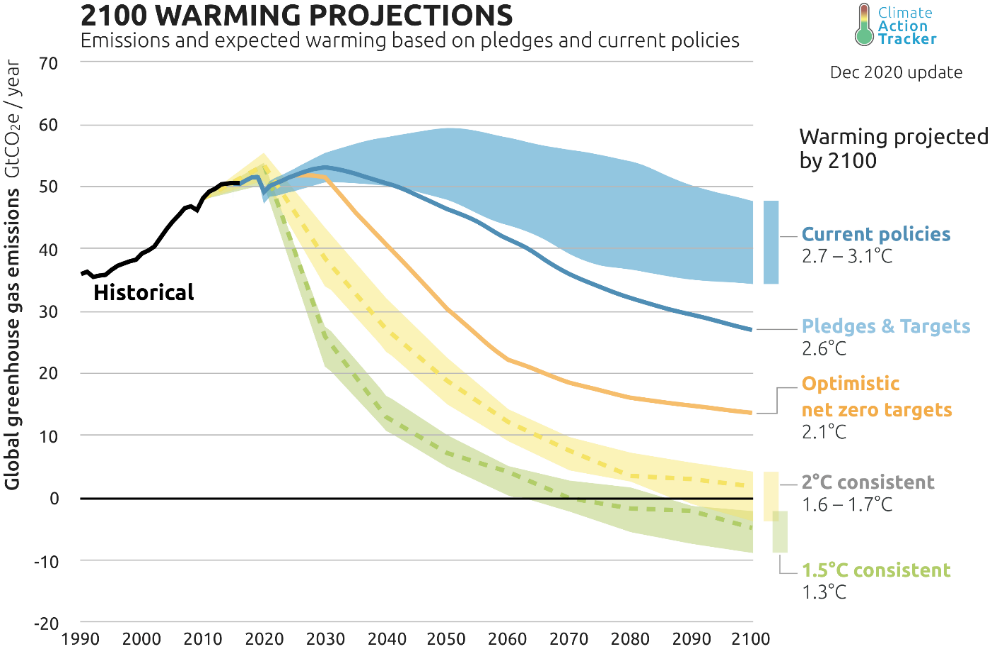

In addition, current policies in place worldwide are projected to reduce baseline emissions and result in a temperature increase of about 2.9°C above pre-industrial levels. The unconditional pledges and targets governments have made, including NDCs and some long-term targets as of September 2020, would limit warming to about 2.6°C above pre-industrial levels if attained [14].

Figure 6: 2100 warming projections

(emissions and expected warming based on pledges & current policies)

Source: Climate Action Tracker (December 2020)

5. The risks of excessively betting on negative emissions and technological progress

Reaching net zero anthropogenic emissions results from the reduction of raw anthropogenic GHG emissions and an increase of removals, either by reinforcing the role of natural sinks, or by creating artificial ones, through carbon capture and storage (CCS) and bioenergy with carbon capture and storage (BECCS) technologies. However, net-zero plans relying heavily on future or ongoing development carbon removal technologies are risky bets. If the removal technologies anticipated fail to reach the maturity performance expected, then compensating for the cumulative emissions might be even more challenging. Moreover, removal technologies might trigger a rebound effect that would ultimately lead to negative impacts.

Most of countries’ NDCs explicitly refer to the contribution of removals from LULUCF but do not project the contribution of other removal technologies though they are more or less explicitly mentioned as means. A few countries (see table 3) explicitly refer to negative emissions and consider them necessary to offset agricultural emissions and other hard-to-abate sectors.

Table 3: Projected negative emissions needed to achieve carbon neutrality by 2050

Technological progress and energy efficiency improvements have almost always been reallocated to boost or create additional demand, what is called “rebound effect”. Recent research[15] confirmed that since 1960, the demand for transport (expressed in kilometers per person per day) has been increasing at the same rate as the average speed of travel. The primary objective of an increase in the average speed of transport was not to travel faster on trips of the same length, but to increase the distance of our trips, especially daily trips, while spending the same amount of time. Emissions grew at the same rate as kilometers traveled. Technological progress did not lead to the reduction of emissions from vehicles of the same performances, but rather to the increase of mass and power – to increase comfort – while keeping consumption levels similar. To align economic sectors with the goal of carbon neutrality, it is therefore necessary to combine breakthrough technology progress with sobriety (i.e. reduction in the weight of new vehicles and speed in the case of the car-industry), otherwise technological progress leads to contradictory effects for the environment.

Conclusion

While 2050 net zero targets are commendable, for the sake of credibility governments must adopt more ambitious and clear-cut 2025 and 2030 targets. Every year, efforts tend to be delayed. Carbon neutrality targets must be settled timely according to global carbon budget exhaustion pace. Moreover, some major economies are still missing from the picture (Russia and India for instance, concerning the U.S. see our recent study about the climate agenda of US President-elect Joe Biden). Around 50% of global CO2 emissions are not yet covered by a net-zero commitment.

Furthermore, most public tools are “enablers of the transition” – subsidies to low-carbon technologies, carbon taxes or green criteria for public procurement just to mention examples – in the last resort, meaning that decarbonization must be implemented by private and individual actors. The private sector has an equally important role to play in creating carbon neutrality trajectories. Even though an increasing number of companies have set targets to reduce their carbon footprints (companies with a combined revenue of over $11.4 trillion are now pursuing net zero emissions by the end of the century[16]), challenges when defining the perimeter are even greater than for governments.

The sum of neutrality targets at corporate level relying disproportionally on negative emissions cannot lead to neutrality at the planet level (natural sinks will be scarce). The core notions and methodological twists revolve around the perimeter, trajectories and timing, as well as the reliability of emission data (across supply chains often spanning over regions and countries). Transboundary flows like international aviation or emissions accounted in imports and exports make the calculations harder.

The core issue when setting climate neutrality targets is the blurred limits of the emissions perimeter covered and the timing mismatch and complexity of carbon sinking mechanisms.

Moreover, the “net neutrality situation” is poised to be only a milestone in our endeavor to curb climate change. Starting from 2050, our economies must become carbon net absorbers (meaning that a large number of companies, households or countries will have to sink more carbon dioxide than they emit). As of today, this “net negative emission situation” seems unrealistic considering our current inability to reduce absolute emissions except in the context of lasting economic recession.

TO GO FURTHER

[1] Net zero emissions is a situation where anthropogenic emissions of greenhouse gases to the atmosphere are balanced by anthropogenic removals over a specified period whereby the concentration of greenhouse gases over that period remains stable. This means that for an x amount of greenhouse gases emitted and added to the atmosphere due to human activities, an equivalent x amount is extracted and stored in carbon sinks through anthropic activities. For further details, see here.

[2] Since then, China has announced its objectives to lower its carbon dioxide emissions per unit of GBP by over 65% from 2005 level (versus 60-65% in its first NDC), increase the share of non-fossil fuels in primary energy consumption to around 25%, increase the forest stock volume by 6 billion cubic meters from the 2005 level, and bring its total installed capacity of wind and solar power to over 1.2 billion kilowatts.

[3] Source: “Net-Zero Emissions Must Be Met by 2050 or COVID-19 Impact on Global Economies Will Pale Beside Climate Crisis, Secretary-General Tells Finance Summit” – United Nations (Nov. 2020), available here.

[4] The full resources on communication of long-term strategies are available on the United Nations Climate Change website, available here. Norway, Finland, South Africa, Singapore, Slovakia, the EU, Costa Rica, Portugal, Japan, Fiji, Republic of the Marshall Islands, Ukraine, the UK, Czechia, France, Benin, the US, Mexico, Germany and Canada have submitted their strategies.

[5] In November 2018, France has implemented a national strategy for the fight against imported deforestation, “Stratégie Nationale de Lutte contre la déforestation importée – 2018-2030”, available here. It aims at putting an end to the importation of unsustainable forest or agricultural products contributing to deforestation by 2030.

[6] Global Carbon Project (Dec 2020)

[7] All the NDCs submitted can be found here.

[8] Source: Climate Action Tracker (Dec. 2020), available here.

[9] Source: Climate Action Tracker (Nov. 2020), available here.

[10] The UK Climate Change Act 2008 requires the government to set five-yearly carbon budgets, running until 2032. The budgets are fixed in advance and set five-year caps on the total GHG emissions allowed to ensure the UK meets its emissions reductions commitments. The UK is on track to meet its third carbon budget (the current one, covering 2018–22) but does not seem to be on track to meet its fourth (2023–27) and fifth (2028–32).

[11] IEA, Global energy review, Coal in 2020, available here.

[12] Source: OurWorldInData, Climate Watch, the World Resources Institute (2020), available here.

[13] Source: Ed Dlugokencky, NOAA/GML, available here.

[14] Source: Climate Action Tracker (Dec. 2020), available here.

[15] Bigo, Aurélien (2020), « Les transports face au défi de la transition énergétique. Explorations entre passé et avenir, technologie et sobriété, accélération et ralentissement », PhD in Economics, Institut Polytechnique, available here.

[16] Source: NewClimate Institute (Sept. 2020).