Taxo4: insights from the release of criteria for non-climate objectives

On April 5th, 2023, the European Commission (EC) published the long-awaited draft delegated acts (DAs) to the Taxonomy Regulation containing technical screening criteria (TSC) for the four remaining non-climate objectives (Taxo4). The Commission also launched a consultation on amendments to the Taxonomy Climate Delegated Act (mitigation and adaptation), and on the Taxonomy Disclosures Delegated Act. The TSC are built to a very large extent on the recommendations of the Platform on Sustainable Finance, published in August 2021, March and November 2022. In contrast, important activities have been added or removed, some of them steering controversies. The consultation will end on May 3rd, with an expected adoption of the DAs by end of June and an entry into force in January 2024 (with consequences on eligibility disclosure, the alignment disclosure on these 4 new objectives is postponed to 2025).

As a reminder, six environmental objectives are defined in the European Environmental Taxonomy:

- Objective 1 – Climate change mitigation

- Objective 2 – Climate change adaptation

- Objective 3 – Sustainable use and protection of water and marine resources

- Objective 4 – Transition to a circular economy

- Objective 5 – Pollution prevention and control

- Objective 6 – Protection and restoration of biodiversity and ecosystems

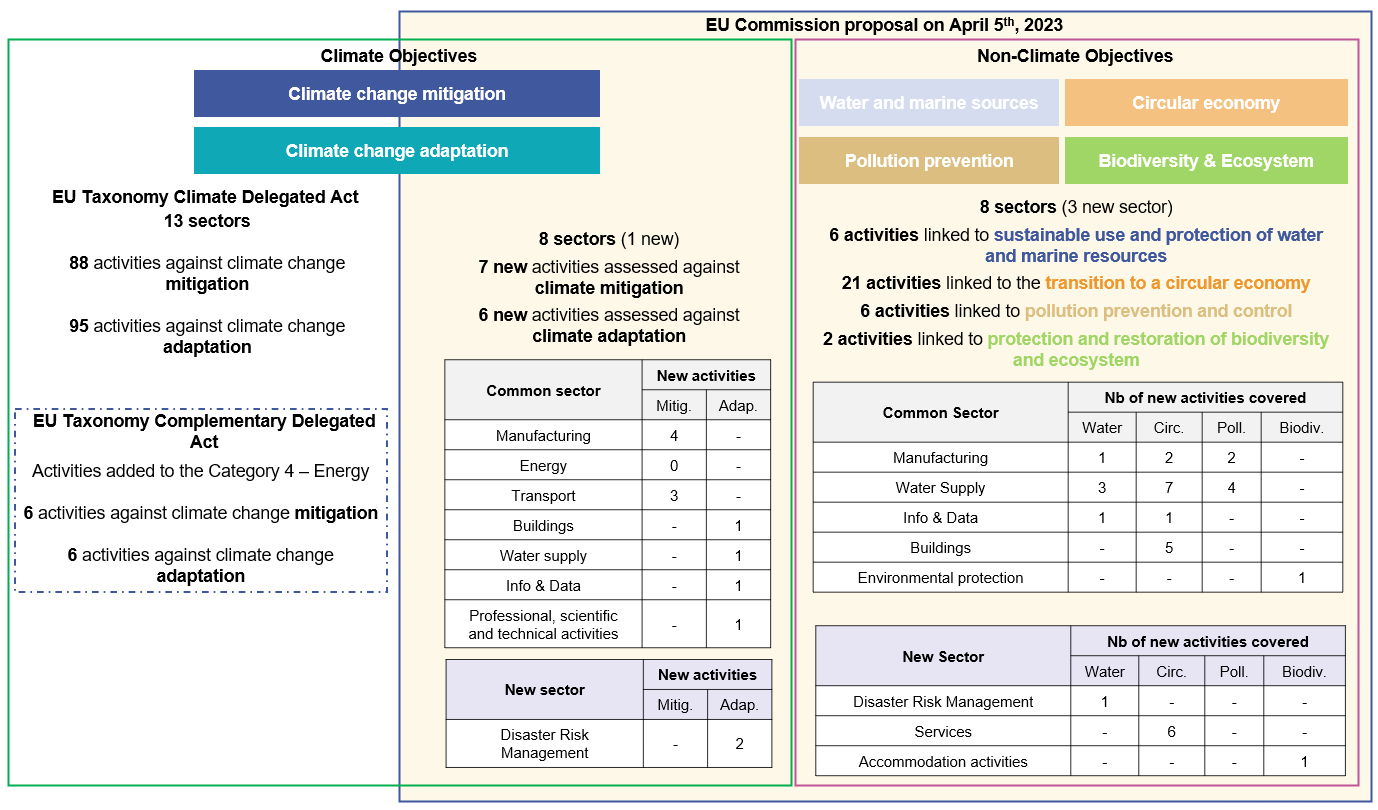

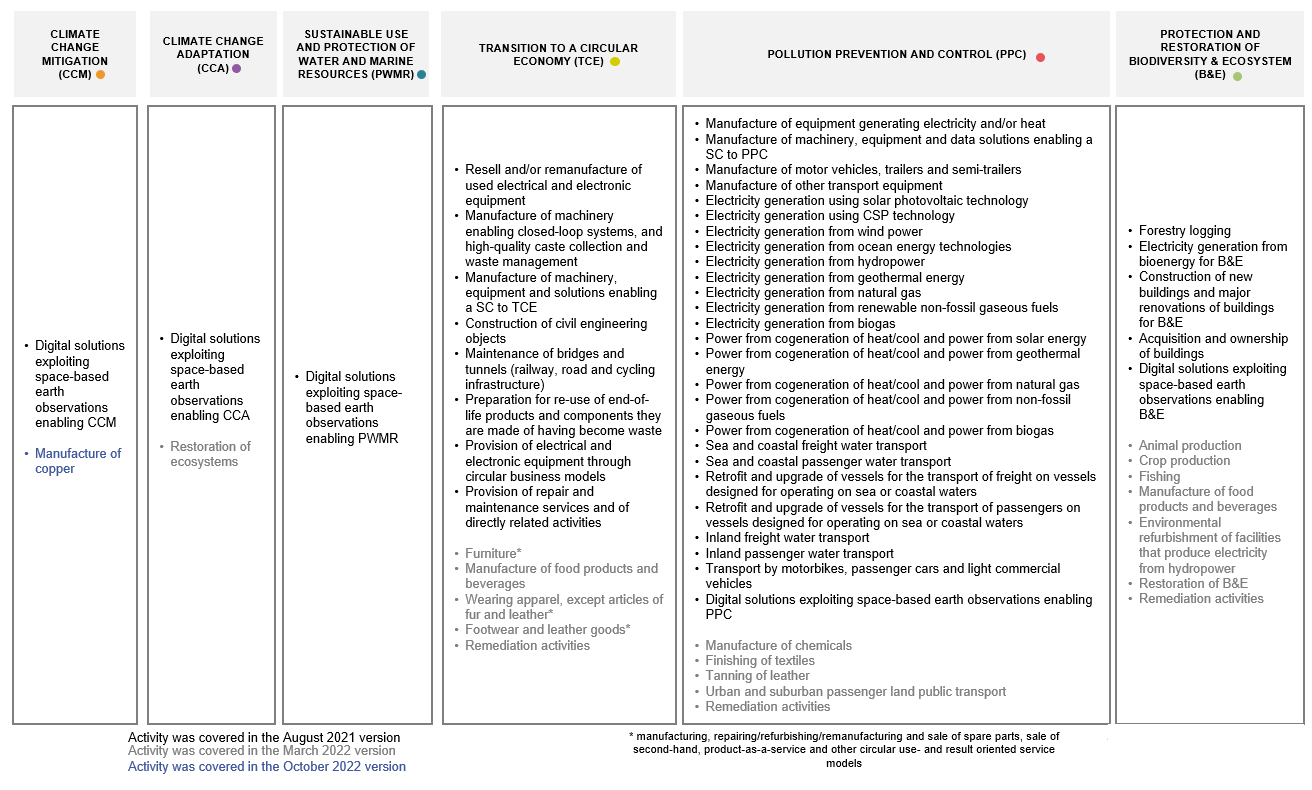

The European Commission (EC) introduced a new batch of 48 assessed economic activities (versus 51 in the publication made by the Platform on Sustainable Finance on March 2022[1]). See the proposal summary below in figure 1.

Figure 1 : How the EC Proposal interact with existing Delegated Acts

Source: Authors (Natixis GSH), based on the EC drafts Delegated Act

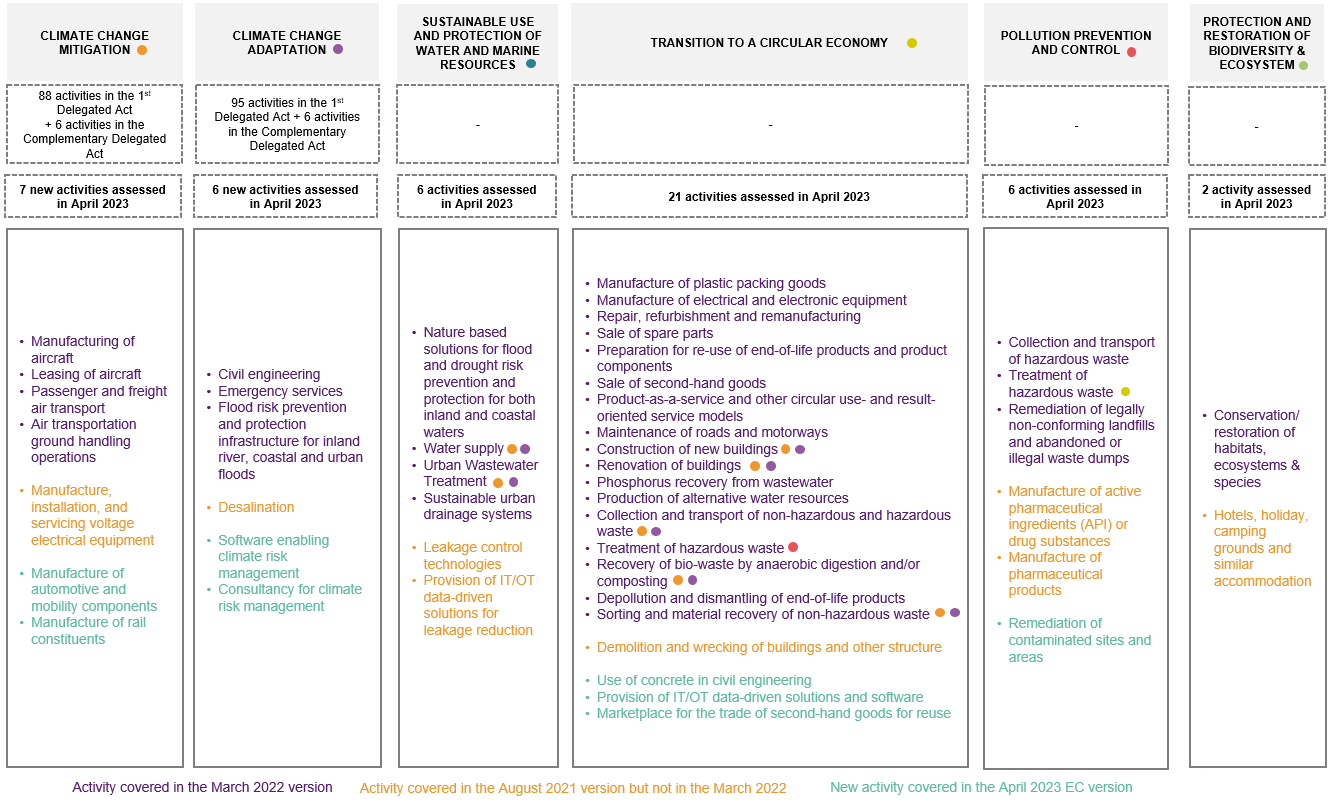

Regarding the environmental objective “protection and restoration of biodiversity”, three important economic activities previously covered by the Platform, namely animal production, crop production and fishing have been left aside. This environmental objective is therefore depopulated with only two economic activities : “hotels, holiday, camping grounds and similar accommodation” and “conservation, including restoration of habitats, ecosystems and species”. The EC also took advantage of this Delegated Acts to develop criteria for 13 new economic activities contributing to the climate mitigation and adaptation objectives. See the summary of the covered activities below in figure 2.

Since the inception of the EU Taxonomy, Natixis has always been in favor of including as much activities as possible, not discarding an activity because of its “brown” nature. The EU Taxonomy is not a whitelist, what matters is the TSC proposed, their stringency and usability. However the proposal to include new transitional activities involving usage of fossil fuel engines in aviation and shipping will certainly reopen the pandora box. One could remind the debate around the inclusion of certain gas and nuclear activities.

Some criteria may be seen too loose compared to the environmental impact of the activity covered. It is particularly the case for the aviation sector with some CO2 emission level not challenging enough, a replacement ratio difficult to compute and a minimum share of Sustainable Aviation Fuel calculation based on a questionable methodology. The new criteria defined for shipping activities after 2026 favorise LNG-powered container and cruise ship ignoring "methane slips and downstream emissions from LNG, which often make them worse for the climate than the traditional fuels they replace", remind the NGO Transport & Environment. For T&E, "Millions of euros could therefore be channeled towards some of Europe’s biggest polluters like Airbus, Ryanair and MSC".

The only 2 activities proposed for biodiversity may also raise concern with the inclusion of short-term tourism accomodation and the non-exclusion of offset in conservation activities ("The conservation activity does NOT ONLY serve the purpose of offsetting the impact of another economic activity").

Figure 2 : Overview of activities covered in the European Commission proposal

Source: Authors (Natixis GSH), based on the EC drafts Delegated Act

The Climate Delegated Act is also amended for some of the activities already covered.

18 amended activities relate to the mitigation objective and 15 relate to the adaptation objective. The most significant information is the creation of criteria from 2026 onward for water transport activities for the mitigation objectives while most of the amendments related to the adaptation objective are some typo corrections of the current DA. Other modifications have additionally been made on the Do No Significant Harm (DNSH) section.

These modifications are not transformative, except some DNSH criteria. This shows the necessity to grant a long enough grandfathering clause (see our article on the EU Green Bond Standard[2]).

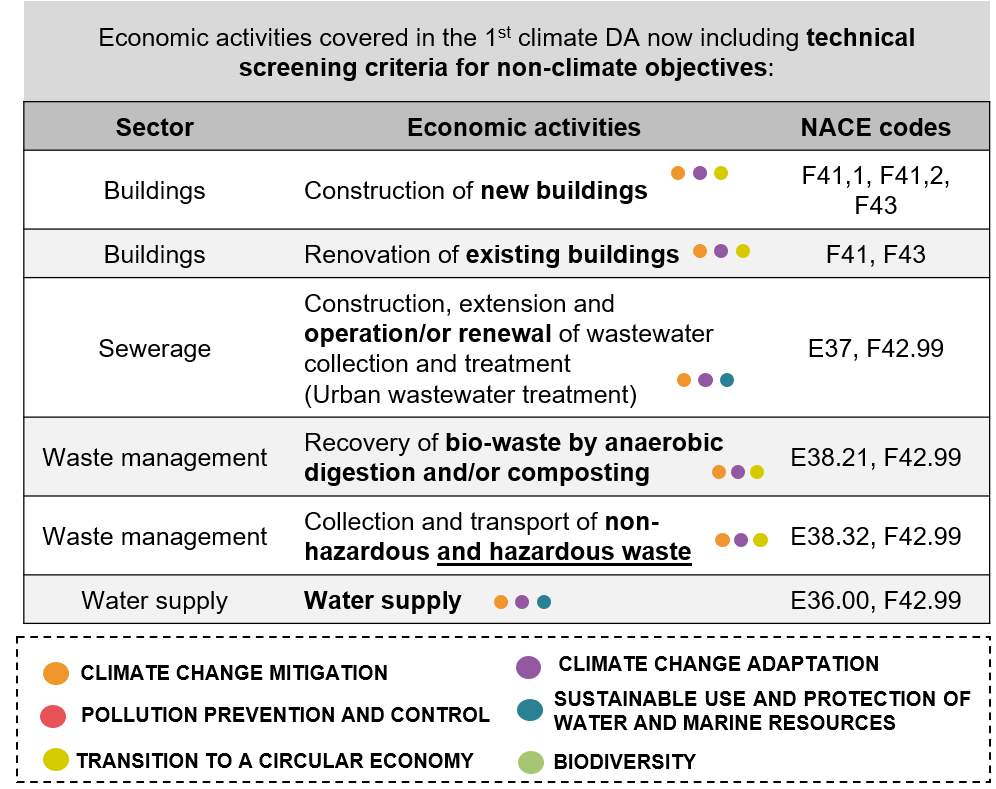

Some economic activities are covered by multiple objectives and criteria.

Besides being covered for the climate objectives in the first CDAs, 5 economic activities are assessed against transition to a circular economy objective and 2 activities against the protection of water and marine resources. More information on those activities is shown on the figure below. There is no guidance on how issuers should prioritize one objective versus another for a single activity provided with criteria for at least two of the environmental objectives. The objective for which alignment is easier might be chosen, but with DNSH requirements to respect.

Figure 3: Economic activities with technical screening criteria provided for more than 2 environmental objectives

Source: Authors (Natixis GSH)

Natixis welcomes the assessment of activities present in the Climate Delegated Acts[3] against these new objectives with 8 economic activities that have now TSC beyond climate. Nevertheless, the high technicity level of some TSC and the hurdles existing when articulating some activities already covered in the Climate Delegated Acts (DA) displays consistency gaps. For instance, differences in activities’ scope and perimeter between both documents, such as variations in economic activities’ name and associated NACE codes, bring confusions and difficulties for companies to report. We strongly recommend harmonizing the economic activity description.

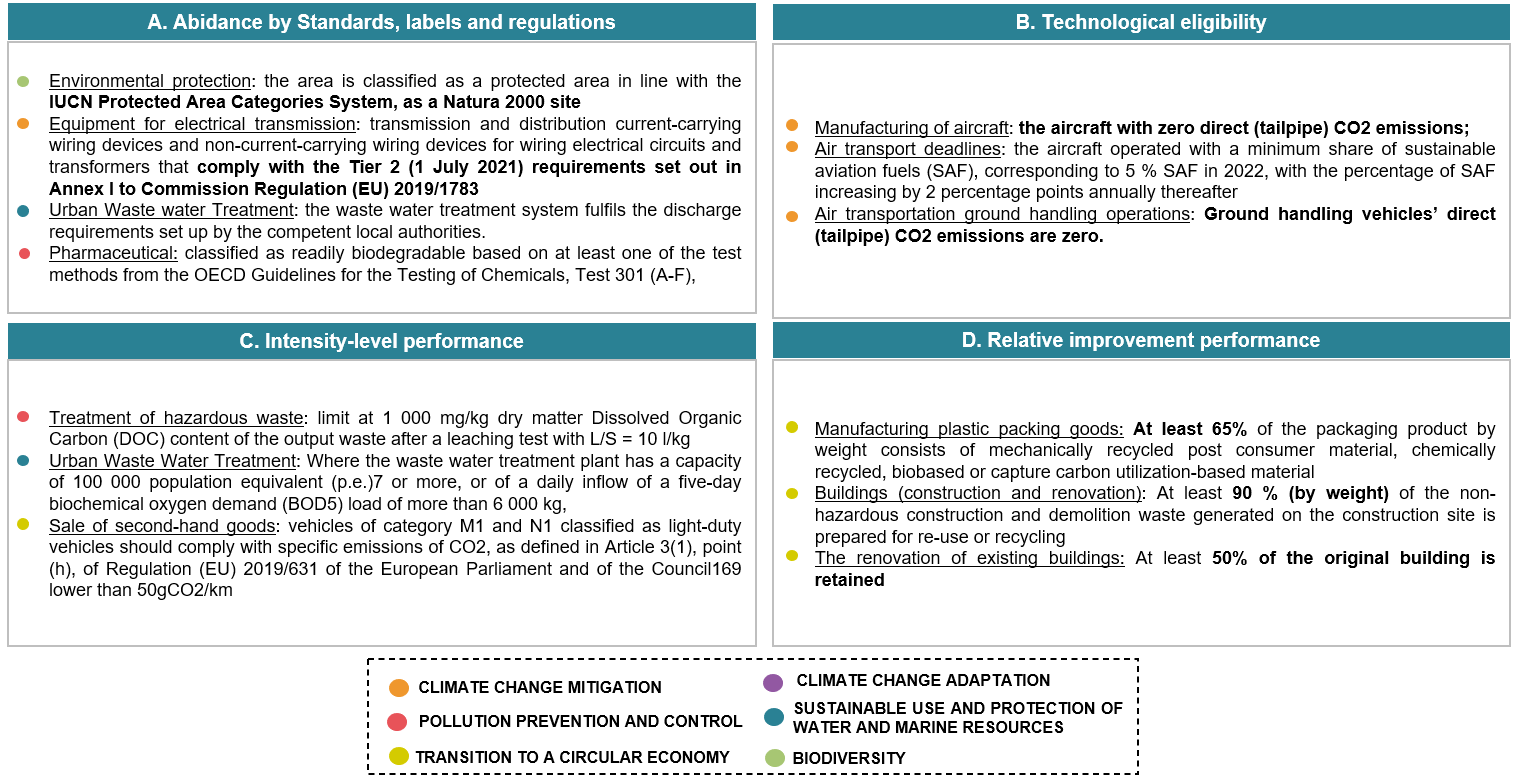

Overall, considering substantial contribution, one can identify four types of alignment criteria based on the various metrics: abidance by Standards, labels and regulations; technology eligibility; intensity-level performance; and relative improvement performance requirements. Such diversity in framing substantial contribution, especially for labels and regulations, challenges the monitoring of transition plans and alignment ratio assessment.

We listed some examples and the objective the activity is responding to respectively, on the figure below.

Figure 4: Examples of different type of alignment criteria based on different metrics found in the Draft DAs

Source: Authors (Natixis GSH)

Additional economic activities based on the Platform’s previous recommendations should be expected quickly. One can foresee progress on biodiversity with activities such as forestry, animal & crop production and fishing. In parallel, other activities and TSCs enabling the green transition would be most welcome even if challenging to assess. One can think of land-based mining and quarrying, other than lignite or crude oil/petroleum.

Figure 5 : Overview of activities not covered in the European Commission proposal but previously explored by the Platform

Source: Authors (Natixis GSH)

The EC introduced amendments to the Taxonomy Disclosures Delegated Act.

What can be underlined is the proposal for financial companies to publish information on their exposure to non-NFRD companies[4] and on the proportion of derivatives in their total assets when calculating their Green Asset Ratio. The amendment is welcome, though we suggest that the EC also requires financial companies to disclose their exposures to central governments, central banks and supranational issuers. We believe that this additional disclosure would help provide more clarity on the structure of banks’ balance sheet (which may vary greatly depending on the business model).

Next steps

The European Commission Draft Delegated Act was open to public consultation until the 3rd of May while the final delegated acts are expected to be adopted on 30 June 2023 to be fully in force by the 1st of January 2024.

[1]See our dedicated article: Taxonomy criteria for non-climate objectives: a welcomed hard work with some inconsistencies, May 2022

[3] The first Climate Delegated Acts dedicated to climate mitigation and adaptation entered into force on January 1st, 2022.

[4] The Non-Financial Reporting Directive. It will be progressively replaced by the Corporate Sustainability Directive, published in December 2022.