EUGBS: hurrah a political agreement… but no legislative transcription details yet

After months of political dead-end[1], market participants were relieved by the political agreement concluded between the Council and the Parliament on the European Green Bond Standard (EUGBS)[2]. Since end February, the Swedish Presidency has been trying to convert the oral agreement into technical and legal provisions. For the time being, we only have an oral provisional agreement, with a laconic press release deprived of key information necessary to fully assess foreseeable impacts. Hopefully, a text should be released by the 30th of June 2023.

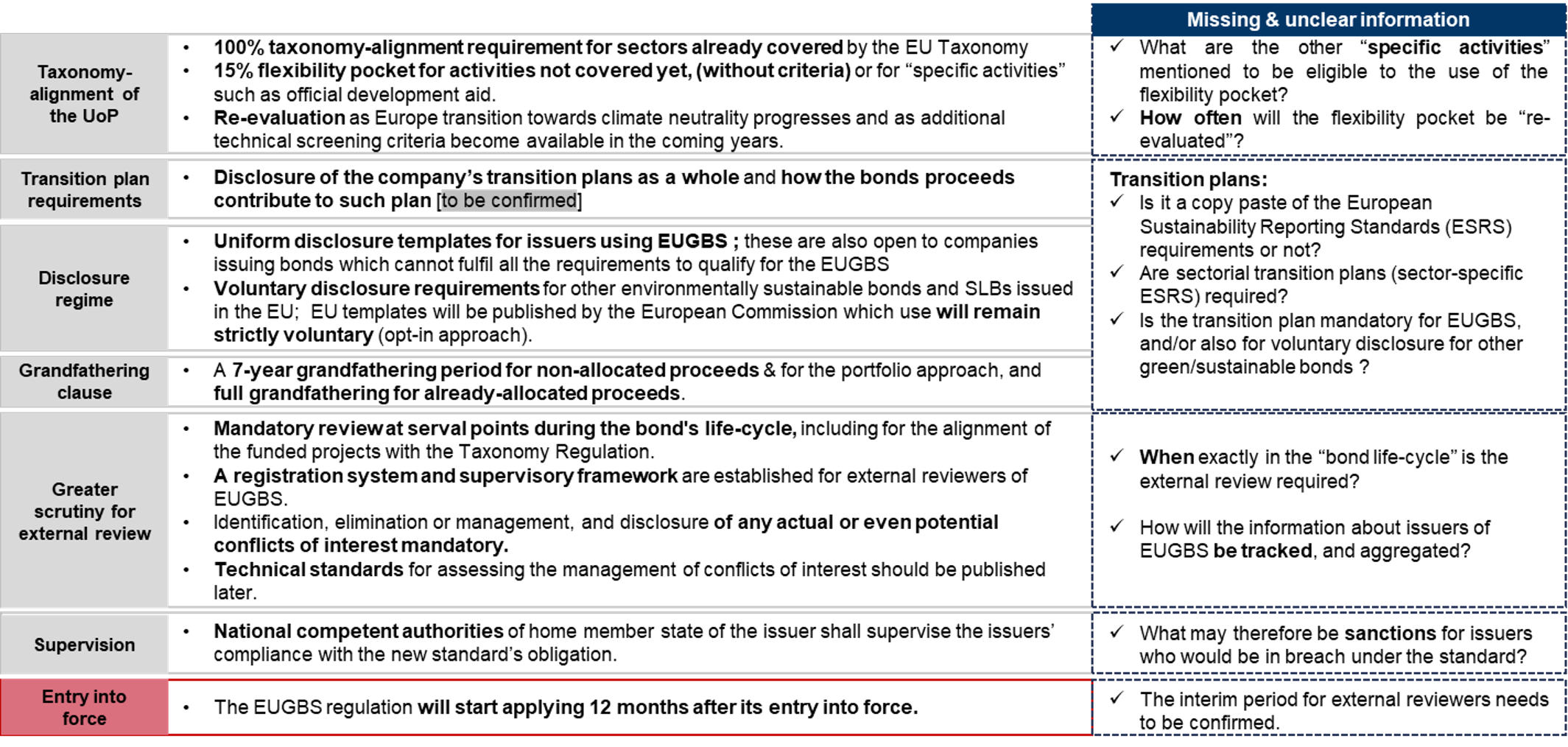

Figure 1 - What do we know of the EUGBS provisional agreement?

Source: Authors (Natixis CIB GSH)

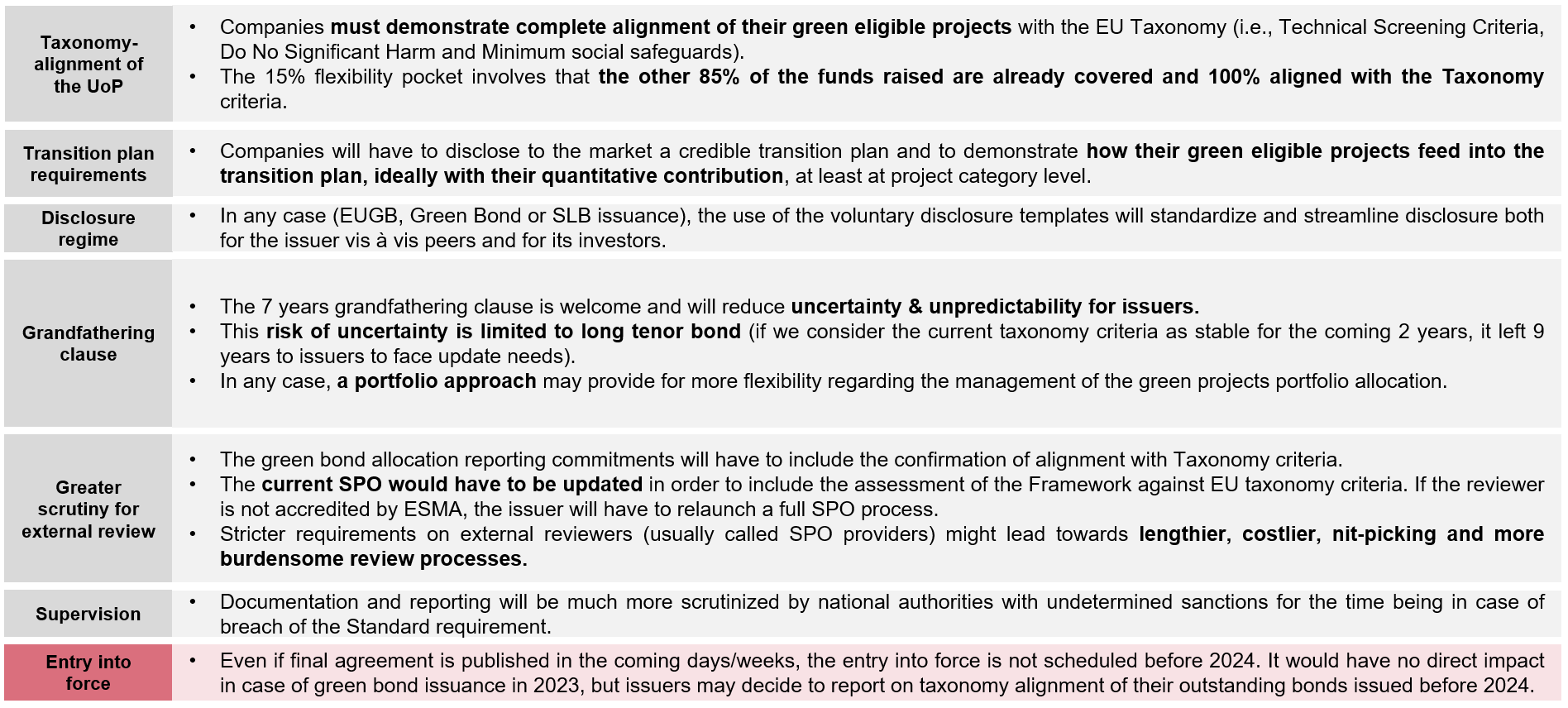

Figure 2 - General implications for issuers: not a revolution, but one expects changes in market practices and pre and post issuance processes

Source: Authors (Natixis CIB GSH)

With the aim of establishing a “gold” standard to fight against greenwashing, the establishment of disclosure templates for EUGBS issuances will help harmonizing and streamlining the information made available by issuers. Importantly, these templates will also be accessible to companies issuing bonds which cannot or do not want to fulfil all the requirements to qualify for the EUGBS (so called “opt-in” templates). The voluntary nature of the EUGBS relieved the International Capital Market Association (ICMA), which published an updated note[3] on the EUBGS in April.

As a reminder, the EUGBS is open to all EU and non-EU issuers, including corporates, sovereigns, financial institutions, and issuers of covered bonds, project bonds and asset-backed securities.

100% Taxonomy-alignment of all EUGBS proceeds is required, provided the activities concerned are already covered by Delegated Acts[4]. Note that the European Commission just released its draft proposal for the 4 remaining environmental objectives, enlarging the pool of eligible assets/projects and potential amounts of aligned proceeds (see our analysis here on “Taxo4”).

The “flexibility pocket” for proceeds alignment with the Taxonomy set at 15% (i.e., what is allowed not to be taxonomy-aligned) must not be misunderstood: it is only applicable to the few activities not yet eligible in the Taxonomy (e.g., agriculture sectors, including industrial livestock farming), and to “specific activities” for which the list remains unknown, except for public development aid. It means that the other 85% of the funds raised are covered and 100% aligned with the Taxonomy criteria. As a reminder, alignment to the EU Taxonomy requires cumulatively complying with the Technical Screening Criteria (TSC) for one objective, the minimum social safeguards[5], and to do no harm to the remaining environmental objectives (DNSH).

The possibility to use the flexibility pocket will decrease over time as a growing number of activities will become eligible, but we ignore the rhythm of its “re-evaluation”. The seven-year grandfathering period for non-allocated proceeds (and the portfolio approach) following criteria update is the time allowed to issuers to adapt, which should give them comfort and guarantee a minimum of legal security.

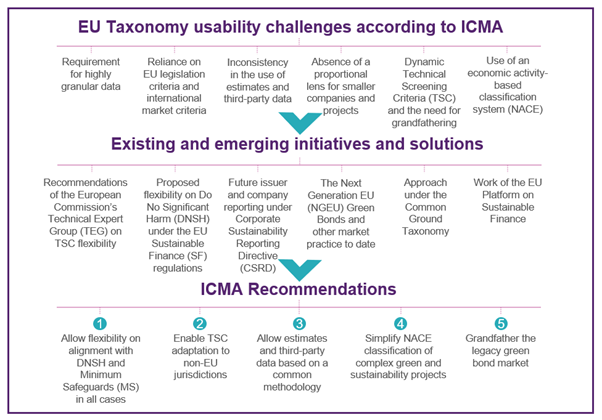

Taxonomy usability challenges however remain, and the ICMA has rightly underlined their nature and potential ways to address them (see the table below).

Figure 3 – ICMA’s view on the EUGBS’ underlying challenges

Source: ICMA

The EUGBS does not add further binarity to the Taxonomy

We foresee a few candidates for full alignment in the short run (most likely single-activity issuer with “easy to achieve” technical screening criteria, and clear environmental and social procedures to evidence DNSH). Encouraging issuers to disclose below 100% (or 85% when considering the flexibility) alignment ratio of their green bonds proceeds is welcome. It will probably bring a welcome transparency, granularity and nuance when assessing the environmental performance of use-of-proceeds. Alignment scoring spanning over a large scale will be made available to market participants. Doing so prevents from adding further restriction or binarity to the existing binarity of the Taxonomy (an activity is either aligned or not aligned). We thus expect to avoid the situation where a bond would have been either 100% aligned or not aligned at all. Based on bilateral discussions, we can mention that investors have appetite for bonds with the highest possible alignment ratios while not being fully EUGBS as long as it feeds their GARs. ICMA’s expectation is that the EUGBS will be initially tested by EU SSAs, due mainly to their policy support and involvement with the label. Renewable energy projects in the EU, such as solar and wind power, by European power and energy companies and utilities, will also very likely be financed with EUGBS.

We anticipate there will be a coexistence of templates with green bond frameworks as they exist today. Frameworks express intents and commitments, but in our view their influence will diminish. Should we try to categorize how market subsegments will coexist following the adoption of the EUGBS, one can imagine three categories of green bonds:

- the top in class European Green Bond with full taxonomy alignment

- the middle category of bonds being transparent about their taxonomy alignment

- And the business-as-usual category with a bit of Taxonomy shopping

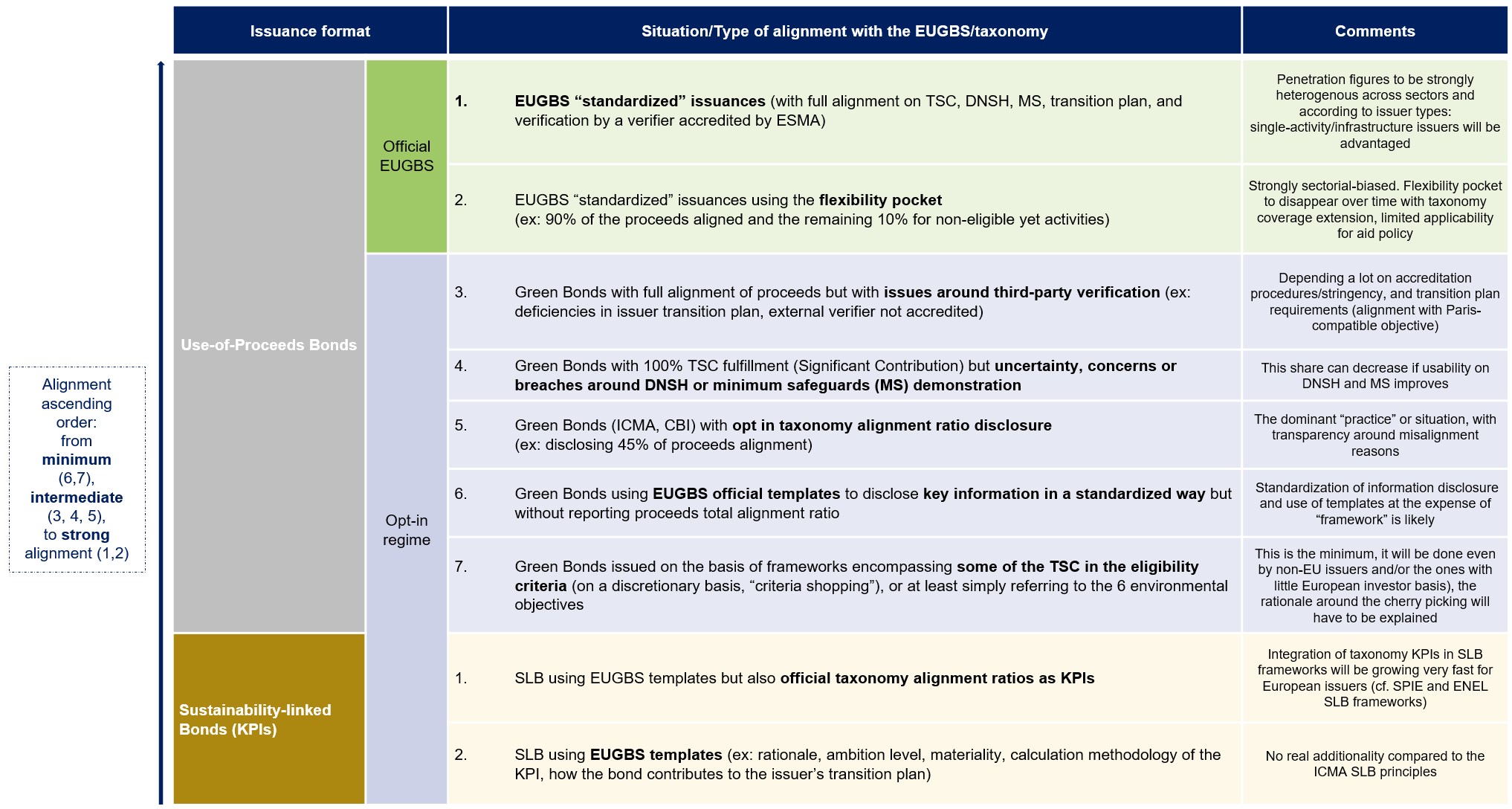

We have identified the various possibilities or situations open by the EUGBS regulation, and tried to assess their potential market shares (see the figure 4 below).

Figure 4 - The EUGBS regulation breaks with the EU green Taxonomy binarity

Source: Authors (Natixis CIB GSH)

There were fierce debates about the requirements imposed on issuers of "other environmentally sustainable bonds and sustainability-linked bonds" (i.e. abiding by ICMA principles), willing to use the EU templates. The opt-in option has been picked, meaning that any companies opting in to these requirements will also be required to state the minimum proportion of bond proceeds to be used on activities that are environmentally sustainable under the EU Taxonomy. The opt-out and simple guidelines options less demanding have been discarded. It seems, at this stage, that there will only be voluntary disclosure requirements: this is welcome, wiser than mandatory requirements, we however ignore how value-additive and precise will the European Commission’s EU templates be. What leaked on the voluntary disclosure template is not convincing, as it does not bring anything additional to the ICMA sustainability-linked bonds principles (SLBP) (for instance, the rationale, level of ambition, materiality, and calculation methodology of the key performance indicators, or how the bond is intended to contribute to the transition plan of the issuer, a description of the bond structure, including the coupon adjustment mechanism).

Such opt-in regime may create incentives for ICMA UoP sustainability bonds’ issuers to disclose taxonomy-alignement share. Disclosure of granular information will notably be valued and upgraded as investors have to meet increasing number of extra-reporting requirements. We therefore anticipate that as the investors progressively express interest in such issuers’ disclosure, the EUGBS would progressively be used in different manners. Natixis agrees with the rapporteur Paul tang when he said he hopes that “investors will push for at least the middle category, and that issuers will use the opt-in templates to get ready for using the European Green Bond label as soon as they have sufficient project available[6]”.

Following that trend, we can easily imagine the issuance of an increasing number of sustainability-linked bonds (SLB) with taxonomy-alignement indicators disclosed (see ou article on ENEL, but one can also mention SPIE). This will be the case especially for European corporates, as Taxonomy related KPIs will be the most systematically reported, but also standardized, comparable and audited KPIs on the market. Furthermore, those KPIs create a unique interdependence relation between issuers and investors, on top of allowing to merge different green activities under a single metric. We believe such Taxonomy KPIs will go hand-in-hand with scope 1 to 3 emissions KPIs.

Transition plan: yes, or no?

Lots of the commentary buzz is “reinventing the wheel”: there is nothing new on the “existence” of an entity’s transition plan. We ignore whether the EUGBS will bring or request something additional compared to what will be required as per the Corporate Sustainability Reporting Directive (CSRD)[7]. This lack of additionality on “the transition plans of the company as a whole” holds true except for issuers not subject to CSRD, but those are limited.

What is supplementary is the need to evidence the consistency between bonds proceeds and an overall issuer’s footprint and transition plan. Indeed, the main novelty lies in the explanations of how bond proceeds are expected to contribute to the issuer’s taxonomy-aligned turnover, capital expenditure and operating expenditure. Quantifying such contribution would be interesting but also difficult. For Paul Tang, the question should not just be: are the proceeds of this green bond spent correctly? But: does this green bond help the company’s Paris-aligned transition[8]?

For both the European green bond documentation and the opt-in templates, the rapporteur wants issuers to link their bonds to those transition plans. However, regarding the information we got from the press releases, we still are not certain that this transition plan rule will apply to both the “standardization regime” and the “opt-in regime”. A possibility would be that this requirement would solely apply to the opt-in transparency regime.

External reviewers become higly accountable

Finally, the main and long known feature of the Standard is the greater responsibility and scrutiny on external reviewers: those will be accredited by ESMA as part of registration system and supervisory framework in order to verify EUGBS pre and post-issuance documents. The key aspect lies in the post-allocation verification (“European green bond allocation report”) aimed at checking whether the Technical Screening Standards and Do no significant harm criteria are fulfilled. Additionally, allocation disclosure will require to specifically identify the share of proceeds allocated to gas and nuclear energy activities aligned with the taxonomy criteria.

Stricter requirements on external reviewers (usually called Second Party Opinion (SPO) providers) might lead towards lengthier, costlier, nit-picking and more burdensome review processes, with activity growth for auditors and third-party verifiers.

The frequency, timeframe, and precise nature of external reviews across EUGBS bonds lifetime require further clarifications. What also remains unclear is how information will be tracked, and aggregated, about issuers of EUGBS (prior issuance labeling and after issuance confirmation or refutation). Finally, it seems that one verifier only should be handling all the different reviews for an issuance candidate to the EUGBS designation (i.e., pre and post-issuance documents).

Reminding the provisional nature of this political agreement, a strategic space is left for techical arbitrages. Scrutiny of the final text is therefore key as future regulatory details could become even more decisive in shaping the EUGBS cumbersome effect and impacts on market practices. As the final regulation should be issued by the 30 June 2023, the Swedish Presidency is confronted with an ambitious task. We are eager to discover the text of the agreed Regulation and examine thoroughly its details, and the Delegated Acts which will follow to enable its full implementation.

[2] The final trilogue took place on 28 February 2023. See the EU Parliament press release.

[3] ICMA, Updated note, 5 April 2023.

[4] The Climate delegated act and the Nuclear and Gas Delegated Act.

[5] See the report of the Platform on sustainable finance on Minimum Safeguards.

[6] Paul Tang, Trust, Transparency and Transition: the European Green Bonds Regulation, 17 April 2023.

[8] Ibid.