Navigating the sea of proposed climate-related disclosures: A deep dive into the SEC’s, ISSB’s and EFRAG’s proposals

20 - minute read

Executive summary

On March 21st, 2022, the American financial watchdog, the Securities and Exchange Commission (SEC), proposed rule changes that would require registrants [1] to disclose certain climate-related information (including GHG emissions, climate-related risks, impacts and financial metrics). It would apply to both domestic and foreign SEC registrants. This proposal takes place in a context of flourishing climate-related disclosure regulations in the world.

The “Enhancement and Standardization of climate-related disclosures for investors” [2] is a holistic and ambitious proposal that would replace the “SEC’s Commission Guidance Regarding Disclosure Related to Climate Change” (2010). Since then, US climate-related disclosure regulations have remained largely stagnant. If enacted, issuers will be required to disclose clear and detailed information, thereby providing investors with consistent, comparable and decision-useful information. This will allow investors to understand issuers climate strategies’ robustness, along with associated risks and opportunities. Consequently, they would be able to make informed investment decisions and effectively engage with firms on business practices.

The proposed rules constitute a breakthrough in US climate finance regulation and align with the international benchmark of practices in other jurisdictions, this is consistent with the wider call for more appropriate disclosures.

Despite the apparent multiplication and fragmentation of national climate-related disclosure regulations, they all build on international voluntary standards such as the TCFD, and therefore regulatory requirements are converging across countries. This is notably the purpose of the International Sustainability Standards Board (ISSB) which released on March 31st, 2022, its draft standards aiming at contributing to standardization of climate disclosures at global level.

5 - A quantum leap in the US regulation unprecedently prescriptive

1 - Comparing SEC’s proposed rule with foreign climate disclosure and international initiatives

3 - Europe is still at the forefront of climate disclosures and global standardization

Enforcing climate-related disclosures to obtain accurate and insightful information is a means to overcome some of the main hurdles that harm the development of sustainable markets such as data collection, assessment, and monitoring. Indeed, as companies still tend to selectively use and disclose the ESG-related metrics that suit them, investors are forced to fill a void with estimates or external data providers. The climate-related standards under development across the world, including the SEC’s proposed rules, could help providing investors with consistent, comparable and decision-useful information.

PART I – US REGULATION: OVERVIEW OF SEC’S LANDMARK PROPOSAL

After extensive external consultations (2016-2019 ) [3] and internal recommendations [4], on March 21st, 2022, the SEC proposed rule changes that will require registrants [5] to disclose climate-related information including GHG emissions, climate-related risks, impacts and financial metrics. Concretely, the proposed rules would amend the existing Regulation S-K which governs regular disclosure (addition of a new Subpart 1500) and Regulation S-X on financial statements (addition of a new article 14) to require the disclosure of climate-related risks, climate-related financial metrics and GHG emissions. It would impact each of the forms: S-1, F-1, S-4, F-4, S-11, 10, 10-K, 10-Q and 6-K for both domestic registrants and foreign portfolio investors.

1 - A holistic proposal covering a large typology of climate-related information

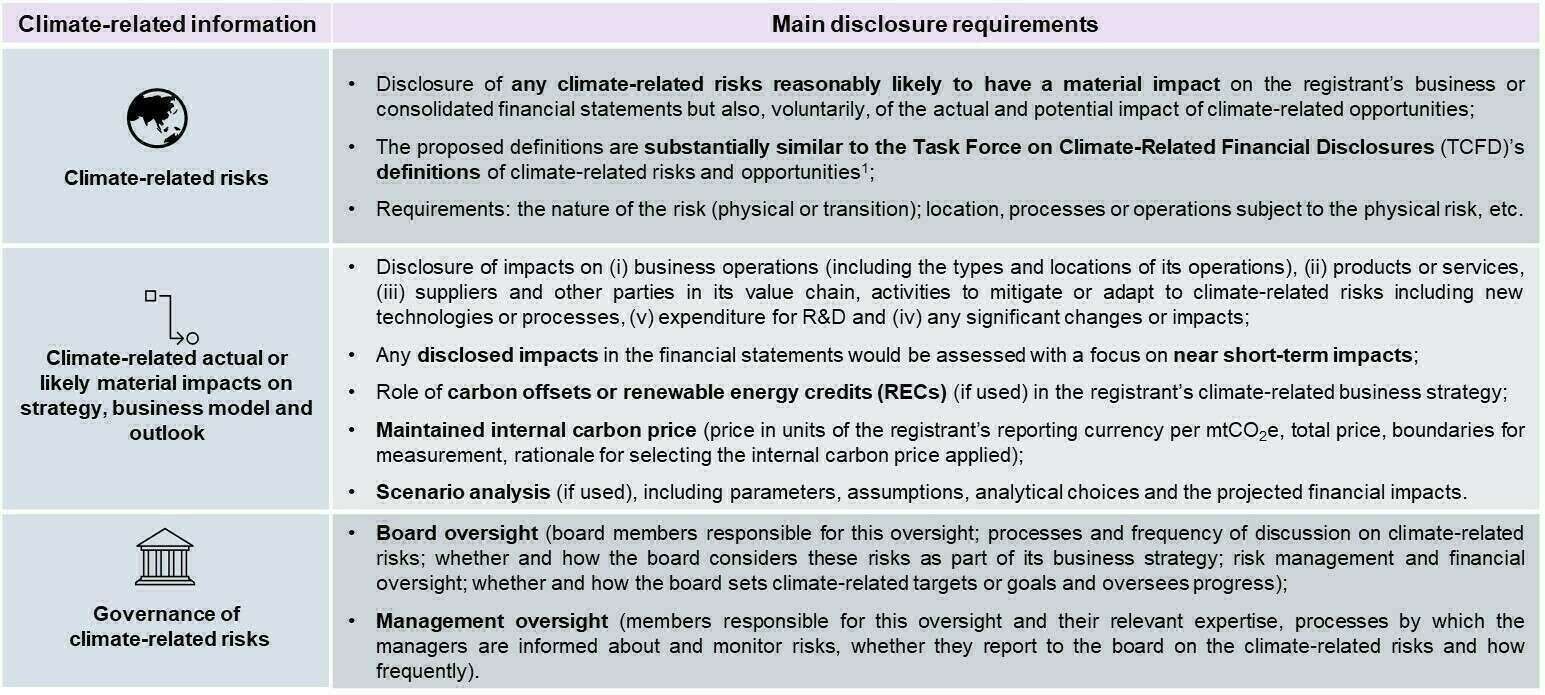

Given its breadth and depth (see the table below), the new proposed rules could be a turning-point for climate-related disclosure in the United States. Among the key proposed disclosures, issuers would be required to publish climate-related risks and their material impacts on business, strategy and outlook, GHG emissions, certain climate-related financial statement metrics, information on climate-related targets and goals, transition plan, if any, as well as on governance practices on climate-related risks and relevant risk management processes.

Figure 1: SEC's proposal requirements to disclose a wide range of climate-related information

Source: Natixis GSH, based on SEC's proposed rule

2 - Disclosure of companies’ GHG emissions as the cornerstone of the proposed rule

Under the current proposal, all companies would have to eventually disclose their GHG emissions even though timelines and scopes depend on companies’ size.

In particular, all registrants would be required to disclose their scope 1 and 2 GHG emissions expressed both by disaggregated constituent GHG and the aggregate in absolute terms (not including offsets), as well as in terms of intensity (per unit of economic value or production). It is a big step forward as 20% of S&P 500 companies still do not disclose scope 1 and scope 2 emissions according to the Principles for Responsible Investment. This degree of disclosure also exceeds what companies currently publish under voluntary standards such as the TCFD. For large companies [6], direct GHG emissions (Scope 1) and indirect emissions (Scope 2) would have to be disclosed from 2024 onward. In parallel, issuers will have to include an attestation report from a third-party for reliability purposes. If enacted in December 2022, limited assurance [7] will be required from 2024-2025 and reasonable assurance will be required each year after. If it is quite unusual for the SEC to require registrants to obtain assurance over disclosure provided outside of the financial statement, it is critical to holding companies accountable and keeping estimates honest. Smaller reporting companies [8] are subject to specific rules. They can start to disclose their GHG emissions from 2026 onward and are exempted from the attestation report requirement.

With regards to value chains’ GHG emissions, companies would have to report Scope 3 emissions if they are deemed “material” based on the US Supreme Court definition [9] or if the company has set a GHG emissions target that includes Scope 3.

Even though the implementation of scope 3 disclosure rules is flexible (delayed compliance date, safe harbor for liability [10] and exemption for smaller companies), they have led to a heated debate. This debate has focused on the disclosure feasibility rather than their utility for decision-making purposes. Yet, one should acknowledge that scope 3 – and especially downstream scope 3 use of product sold – is essential to understand the robustness and the effectiveness of a company’s strategy and transition plan.

3 - Climate-related financial statement metrics disclosures: a pioneering requirement

Under the proposed rules, registrants would also be required to disclose impacts of climate-related events (e.g., extreme weather events and physical risks) as well as transition activities (including transition risks identified by the registrant) on each line item of the consolidated financial statements [11] (in statement of cash flow, inventories, intangible assets, long-term debt or contingent liabilities) unless the aggregate impact is less than one percent of the total line item [12]. Transition activities may include changes linked to new emissions pricing or regulations, upstream costs (such as transportation of raw materials).

Figure 2: The three categories under which the disclosure unravels

|

Type of metrics |

Requirements |

|

Financial impact metrics |

Positive and negative impacts associated with the same climate-related events and transition activities |

|

Financial expenditure metrics |

Separately aggregate amounts of expenditure expensed and capitalized costs incurred during the fiscal years |

|

Financial assumptions |

Qualitative description of how climate-related events and transition activities impact the estimates and assumptions used to prepare the financial statements |

Source: Natixis GSH, based on SEC's proposed rule

In addition, registrants would have to disclose the associated contextual information, including a description of significant inputs and assumptions used to calculate the specified metrics.

4 - Heated debates and threats of litigation put the implementation timeline under pressure

The SEC proposed an implementation timeline aiming at a partial enforcement of the rule from 2023 onward. The SEC adapted its requirements to the size of the companies and the degree of difficulty to fulfil the requirements. Overall, the larger the entity, the earlier the disclosures will be required to begin.

Figure 3: Phase-in Timeline of SEC’s Proposed Disclosure Requirements

Source: Natixis GSH, based on SEC's proposed rule

On May 9th, 2022, the public comment period was extended until June 17th, 2022, by the SEC [13]. Given the scope and complexity of the proposed rules, comments are expected to be extensive, and litigation threats are likely if the proposed rules are adopted. Significant comments and potential challenges to the proposal could therefore delay adoption of final rules and its timeline. In particular, the Scope 3 GHG emissions disclosure has been the most contested. The required disclosures are seen as being overly broad and burdensome by issuers who argue that this relies on imprecise estimates.

Since the SEC is not a legislative body, it was also accused of overstepping its authority by tackling a “social and economic policy” agenda. According to commentators, it is still likely that any final rule will receive a sufficient vote to be adopted later in 2022.

5 - A quantum leap in the US regulation unprecedently prescriptive

The proposed rules are much more prescriptive in nature than the previous principles-based regulation. It will require companies to integrate and cascade it in their controls, audit and oversight bodies. This would shed light on climate risks and impacts in an unprecedented manner to allow investors with the appropriate level of information to make informed-decisions and effectively engage with firms on business practices.

This SEC’s proposed rule constitutes a breakthrough in US climate finance regulation and brings it closer to European counterparts [14]. Interestingly, the SEC proposal could also kickstart the emergence of a wider ESG regulatory strategy in the US and serve the broader environmental agenda of the Biden Administration (see our Report on the last US election and the great divide on climate policy).

Furthermore, on May 25th, 2022, the SEC has released its ESG disclosure proposal to establish disclosure requirements for funds and investment advisers that markets themselves as having an ESG focus[15]. This proposal aims at tackling the challenges raised by the growing investor interest in ESG investments with “hundreds of funds and potentially trillions of dollars under management”[16] in the US sustainable investment universe. The proposal would particularly require funds to:

- Provide investors with information in the prospectus about what ESG factors are considered along with the strategy they use for funds saying they consider ESG factors;

- Disclose details about the criteria and data they use to achieve their investment goals and more specific information about their strategies; and

- Disclose relevant metrics for particular types of ESG-focused funds[17]: report the greenhouse gas emission metrics of their portfolios for ESG-focused funds that consider environmental factors, related metrics and the annual progress of impact funds toward their ESG goals, etc.

The comment period for this proposal remains opened until July 24th, 2022.

PART II - INTERNATIONAL BENCHMARK: TCFD STANDARDS AT THE HEART OF THE ONGOING CONVERGENCE OF SOARING CLIMATE DISCLOSURES

Just like the SEC, Regulators across the world are set to continue aligning with the Task Force on Climate-related Financial Disclosures (TCFD) standards. At a global scale, the adoption of national-level disclosure requirements for firms has accelerated in 2022. The apparent multiplication and fragmentation of national regulations may however not necessarily result in an additional burden for global issuers, as in practice, it is building on the same international voluntary standards.

1 - Comparing SEC’s proposed rule with foreign climate disclosure and international initiatives

As more countries are reinforcing or implementing climate-related disclosure requirements, climate-related disclosures are developing at high speed at the world level (see Figure below and Appendix for more information).

Figure 4: Benchmark against leading financial countries on climate-related disclosures

Source: Natixis GSH, based on SEC's proposed rule

Many countries have scheduled mandatory Task Force for Climate-Related Financial Disclosure (TCFD) reporting totally or partially, or are planning to do it (e.g., UK - see our 2020 article on UK’s mandatory TCFD climate disclosure, Brazil, Germany, France, Canada, South Africa, Switzerland, Japan, Hong Kong, Singapore, China etc.). Contrary to certain other OECD countries (e.g., UK, New Zealand), the SEC does not specifically mandate TCFD reporting.

|

BOX N°1: THE TASK FORCE FOR CLIMATE-RELATED FINANCIAL DISCLOSURE (TCFD) AND INTERRELATIONS WITH NATIONAL JURISDICTIONS As a reminder, the TCFD is an initiative created in 2015 by the G20 to develop recommendations on climate risks disclosures. It constitutes an advisory body of the Financial Stability Board (FSB). Interestingly, the SEC’s proposal, just like many of the recent national climate disclosures (such as the UK’s and New Zealand’s ones), draws upon the TCFD’s recommendations and the Greenhouse Gas (GHG) Protocol which are widely used voluntary standards. 388 TCFD supporters out of 3,000 corporate, financial and government ones are domiciled in the US. And TCFD supporters are growing rapidly, with a record level of adoption in 2021 (1,117 new supporters). As compared to the global trend, the SEC initiative was therefore anticipated and is particularly welcome. Compared to foreign regulations, it is characterized by:

The significance of the proposal in what is still the deepest and most important capital market in the world, cannot be overstated. One way or another, these requirements will likely “trickle down” into any jurisdiction, as they apply to foreign entities. |

2 - 2022 opens a momentum in terms of climate-related reporting requirements with ISSB's & EFRAG's standards also under consultation

With the launch of the International Sustainability Standards Board’s (ISSB) and the European Financial Reporting Advisory Group’s (EFRAG) consultations on newly proposed international standards, 2022 is set to be a decisive milestone in the development of climate-related disclosure standards across the world.

To promote a “building block approach” and contribute to standardization initiatives at global level, the International Financial Reporting Standards (IFRS) Foundation announced the creation of a new International Sustainability Standards Board (ISSB) at the 2021 UN COP 26 in Glasgow. Those standards are also heavily inspired from the TCFD recommendations. Two standards were proposed on March 31st, 2022: one focuses on the general sustainability-related disclosure requirements [18] while the other relates to climate-related disclosure requirements [19]. ISSB is currently seeking feedback on the proposals over a consultation period closing on July 29th, 2022.

Figure 5: ISSB’s timeline

Source: Natixis GSH, based on ISSB’s draft standards and website

The initiative represents a major step forward in establishing consistent, comparable global reporting. Fostering international convergence is an ambition shared with the SEC. This may benefit global issuers by reducing the need to work on too many disclosure templates at the same time if they were to be shared by countries. ISSB intends to further enhance compatibility between its exposure drafts and the ongoing shift on sustainability disclosure standards across jurisdictions. On April 27th, 2022, ISSB launched the creation of a working group with national and international representatives such as EFRAG, the European Commission, the US, UK, Japan and China for dialogue purposes. Some investors have however voiced concerns with the US involvement in this working group as they fear that its traditionally contentious-oriented approach may water down the ISSB’s initiative. This would not sway the EU’s work anyway but could lead to a stubborn regulatory asymmetry between Europe and the US.

In parallel, the European Financial Reporting Advisory Group (EFRAG) is developing draft European Sustainability Reporting Standards (ESRS) while leveraging TCFD recommendations for the European Commission. They will be used as part of the Corporate Sustainability Reporting Disclosure (CSRD). On April 29th, 2022, a first version of its Draft ESRS Exposure Drafts (EDs) [20] was published. The public consultation period runs until August 8th, 2022.

Figure 6: EFRAG & CSRD's key timeline steps

Source: Natixis GSH, based on EFRAG’s draft standards and CSRD’s proposal

The proposals build distinctively on the “double materiality” principle, which requires to assess both the ESG impacts on the company, and the company's impact on the environment and society. The release of draft European corporate sustainability reporting standards has been hailed as a much-needed strengthening of EU disclosure requirements. As companies may not be moving fast enough to align with the Paris Agreement objectives and sometimes to achieve their own commitments and targets, these new disclosure standards will be key to engage with them.

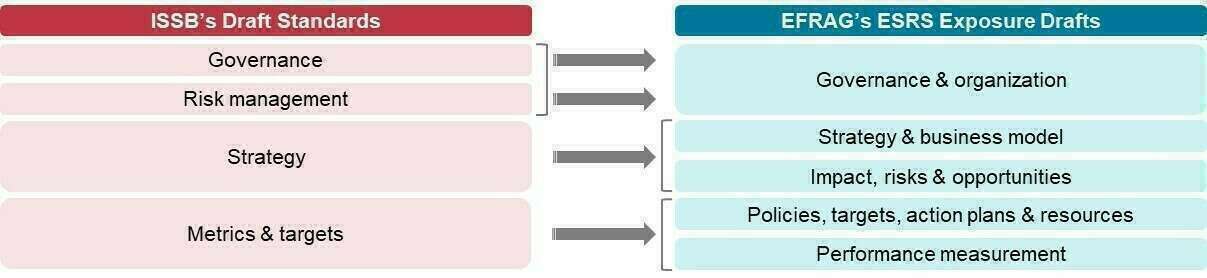

BOX N°2: COMPARISON OF THE TWO DRAFTS STANDARDS RECENTLY RELEASED BY ISSB AND EFRAG

EFRAG’s classification of sectors is based on the NACE codes (14 groups and 40 sectors) whereas ISSB’s classification of sectors refers to Sustainability Accounting Standards Board (SASB) industry-based standard (11 sectors and 77 industries).

Even though their respective structures slightly differ, the content of ISSB’s and EFRAG’s standards is similar. The main categories of these two standards are matching:

Figure 7: Comparative analysis of ISSB's and EFRAG's standards

Source: Natixis GSH, based on ISSB’s and EFRAG’s standards

However, EFRAG’s ESRS generally propose more comprehensive and detailed disclosure requirements, especially with four more specific disclosures compared to the ISSB’s proposal:

- Energy consumption & mix (total and detailed energy consumptions in MWh);

- Energy intensity (information in MWh/Monetary unit);

- GHG removals (in mtCO2e);

- Avoided GHG emissions from products and services (in mtCO2e).

Note that EFRAG is expected to submit the final first set of proposals to the European Commission in November 2022. Both EFRAG and ISSB announced their intention to release final versions by December 2022.

3 - Europe is still at the forefront of climate disclosures and global standardization

At the European level, two main disclosure regulations have entered into force or are about to: the Corporate Sustainability Reporting Disclosure (CSRD) and the Sustainable Finance Disclosure Regulation (SFDR).

Drawing on the principle of “double materiality”, the CSRD will replace the Non-Financial Reporting Directive (NFRD) and significantly expand its coverage. It requires corporates to disclose information on the way they operate and manage social and environmental challenges.

This regulation will apply to all EU large public-interest companies - whether they are listed or not, and without the previous 500-employee threshold - as well as to potentially listed SMEs, except for listed micro-enterprises. This regulation will capture about 50,000 companies. The EU feature of companies is a major difference compared to the SEC’s proposal which should apply to both domestic and foreign SEC registrants. Nonetheless, the CSRD, notably its scope and its extra-territoriality, is currently under discussion in the EU Parliament and the Council. The trilogue period is in progress but an agreement between the co-legislators by the end of June 2022 appears unlikely. A third-party assurance of the reported data will also be mandatory which is similar to the third-party attestation proposed by the SEC.

The CSRD proposal mandates that companies need to report according to new EU sustainability reporting standards developed by EFRAG. The reported sustainability information will be both included in the management report and digitally tagged by companies. The first set of reporting standards under the CSRD will enter into provisional application in January 2023 and only in January 2026 for SMEs. This implementation timeline differentiated according to the scope of companies is consistent with SEC’s approach.

The SFDR creates a framework for investors to disclose how they integrate and manage sustainability factors. This regulation applies to all financial market participants and financial advisers operating within the EU. The scope is therefore both domestic and foreign, just like SEC’s proposal. However, the major difference between both regulation is the SFDR is focusing on investors and not companies. The principle of “double materiality” is once again at the core of this Regulation, notably with the Principal Adverse Impacts (PAI). SFDR’s reading scheme is close to SEC’s proposal. Market participants must disclose the impact of material ESG risks on an insurer’s portfolio performance. Several themes are also included in the mandatory Environmental PAI, especially GHG emissions and energy performance.

Disclosure requirements required by the SFDR can be bundled into three separate categories:

|

Categories of disclosure requirements |

Examples of disclosure requirements |

|

Pre-contractual disclosures |

Description of sustainable risks and results of assessments regarding the Article 8 and Article 9 products. |

|

Disclosures on manager’s website |

Notably information on the inclusion of sustainability criteria in investment policies and in particular the classification of products under Articles 6, 8 and 9 of SFDR. |

|

Additional disclosures in periodic report |

Especially qualitative and quantitative indicators demonstrating the product meets the Article 8 or Article 9 requirements. |

Finally, the SFDR applies to product distribution through so called “articles 6, 8 and 9” categories of financial products. The Regulation has already entered into force on March 10th, 2021, for portfolio management companies. Periodic reporting requirements for sustainable investment products entered into application in January 2022. On April 6th, 2022, the European Commission adopted the final Regulatory Technical Standards (RTS) supplementing the Sustainable Finance Disclosure Regulation (SFDR) and its annexes. These RTS specify the mandatory website, pre-contractual and periodic reporting templates for financial market participants and in-scope financial products. They will apply from January 1st, 2023.

APPENDIX

In 2022, many countries across the world have implemented national climate-related disclosures rules or have them under development. Most of these national regulations are largely inspired by the TCFD recommendations. Two countries stand out of this global trend: China, which has not considered interoperability to build its disclosure requirements, and Australia whose national legislation only covers GHG emissions.

Figure 8: International benchmark of climate-related disclosure requirements

|

Country |

Interoperability with SEC requirements and international standards |

Description |

|

French “Loi Energie Climat”’s article 29 deepens and strengthens SFDR rules |

The implementation decree of article 29 is designed in articulation with European law (SFDR), applies the TCFD recommendations and will take into account the future TNFD proposals. |

Adopted on November 9th, 2019, the “Loi Energie Climat” allows the French Government to step up its climate and energy policies to reach carbon neutrality by 2050. Its article 29 transposed the Sustainable Finance Disclosure Regulation (SFDR) but it set more stringent extra-financial disclosure requirements at French level. What to disclose? The article confirms the preexisting non-financial reporting by requiring to disclose the policies and resources devoted to the energy transition, indicative targets on alignment with the Paris Agreement objectives, similarly to the EFRAG’s draft requirements, as well as to publish environmental objectives by 2030 in volume of GHG emissions or in implicit temperature increase. Furthermore, in complement to SFDR, the article 29 also requires to disclose the risks associated to climate change and the risks management, strategy, governance and impact measurement, similarly to the SEC’s proposal. This article also required to disclose the risks related to the decrease in biodiversity. Concerning the biodiversity requirements, the future Task Force on Nature related Financial Disclosure (TNFD, see our 2020 article Towards a TNFD) will provide breakthroughs in reporting, risk identification and upstream measurement for asset portfolios. A common definition of biodiversity is waited. The TNFD will adopt a final nature-related risk management and disclosure framework by 2023. Entities concerned Compared to the previous rules, the scope of covered actors is extended and the portfolio management and investment activities of banks, credit institutions and investment firms as well as real estate funds are now subject to the new system. Timeline of implementation The entry into force is sequential. The Article 29 Implementation decree was published in the French Official Journal on May 27th, 2021 and began to partially apply for the 2022 reporting for a first part of the requirements. A second part of the article 29’s rules will come into force as of the 2023 reporting. |

|

United Kingdom: new rules entered into force in April 2022 |

United Kingdom and Canada’s climate-related disclosures requirements are also largely based on TCFD recommendations

|

UK recently enshrined in law mandatory Task Force on Climate-related Financial Disclosures (TCFD) aligned requirements for Britain's largest companies and financial institutions. Fast-forward to October 2021, the UK government introduced two disclosure requirements:

What to disclose? New legislation requires firms to disclose climate-related financial information. UK companies will be provided with a uniform way to assess how a changing climate may impact their business model and strategy, and ensure they are well placed to harness opportunities from the UK’s transition to net zero. The rule induces a requirement for qualitative scenario analysis. Entities concerned Several types of entities are concerned by these new UK rules:

Timeline of implementation They came into force on April 6th, 2022. Investors and enterprises in other geographies are watching keenly, as they assess the success with which the new demands are met. If the TCFD’s recommendations are quite generic, the UK is, until now, the only country to have put an estimation in place to make the different participants aware of what costs are incurred in terms of being compliant. With regards to this, the UK is paving the way for other countries, such as Singapore and Hong Kong, even though their plans are not as specific as the UK rules. |

|

Canada: climate disclosure requirements under project |

On October 18th, 2021, the Canadian Securities Administrators (CSA) published a CSA Notice and Request for Comment on climate-related disclosure requirements (NI 51-107). What to disclose? Issuers will have to disclose several categories of information largely consistent with the TCFD recommendations:

Entities concerned All reporting issuers are concerned, with the exception of investment funds, issuers of asset-backed securities, designated foreign issuers, SEC foreign issuers, certain exchangeable security issuers and certain credit support issuers. Timeline of implementation These rules are not expected to come into force before December 31th, 2022, followed by a one-year phase-in period for non-venture issuers and a three-year phase-in period for venture issuers. |

|

|

New Zealand’s laws on climate risks and opportunities

|

New Zealand recently passed law on climate change disclosures based on the TCFD recommendations.

|

On October 21st, 2021, New Zealand passed laws requiring banks, insurers and investment managers to report the impacts of climate change on their business. These disclosures are subject to the publication of climate standards from New Zealand’s independent accounting standard setter, the External Reporting Board (XRB). Those standards will also be based on the Task Force on Climate-related Financial Disclosures (TCFD) recommendations. What to disclose? The new laws require financial firms to explain how they manage short-, medium- and long-term climate-related risks and opportunities present to their business. Those unable to disclose would have to explain their reasons. Entities concerned About 200 of the largest financial firms in New Zealand will have to make disclosures, including:

Timeline of implementation Several foreign firms that meet the NZ$1 billion threshold - including Australia's four largest banks - will also come under the legislation. The disclosures requirements will become mandatory for financial years beginning in 2023. |

|

Australia’s mandatory reporting of GHG emissions

|

Australia’s legislation is only focused on GHG emissions and doesn’t consider general climate-related risks. |

General disclosure of climate-related risks is not mandatory in Australia. However, the 2007 National Greenhouse and Energy Reporting Act (NGER Act) establishes the legislative Framework for the NGER Scheme which is a national framework for annual reporting greenhouse emissions and energy information. What to disclose? Companies in Australia must disclose their greenhouse gas emissions (Scope 1 & Scope 2), their greenhouse gas projects as well as energy consumption and production (including initial extraction, own-use of energy, and the transformation of energy within and between facilities). The NGER legislation requires the total amount of each commodity to be reported, including each transformation of energy from one fuel or commodity into another. Entities concerned Two type of thresholds determine which companies have an obligation under the NGER Act:

Timeline of implementation The NGER legislation is entered into force in 2008. Since then, several amendments have been made since. New proposed ones are currently under consultation [23]. |

|

Hong Kong’s climate disclosure standard |

The SFC and HKEX are closely following the prototype developed by IFRS Foundation and aligning with the framework of the TCFD to design their new climate standard. |

The Securities and Futures Commission (SFC) and Hong Kong Exchange (HKEX) are working together to develop a climate disclosure standard. The prototype was published on November 3rd, 2021. What to disclose? Largely in line with TCFD, the prototype requires to disclose the following information, on an annual basis, by assessing four aspects:

Entities concerned Both financial institutions and listed companies will be concerned by this new standard. Timeline of implementation These climate-related disclosures will be mandatory across relevant sectors no later than 2025. |

|

Singapore Exchange’s Roadmap |

Climate-related disclosures proposed in the SGX’s roadmap are based on recommendations of TCFD. |

On December 15, 2021, Singapore Exchange (SGX) today unveiled its roadmap for all issuers to provide climate-related disclosures. What to disclose? Issuers must especially conduct an internal review of their sustainability reporting processes and all directors must undergo a ‘one-time training’ on sustainability. Entities concerned All issuers are concerned by these future requirements. Timeline of implementation They must provide climate reporting on a "comply or explain" basis in their sustainability reports from the financial year starting 2022. Climate reporting will be made mandatory according to two different dates:

|

|

New China’s requirements |

For its disclosure rules, China has not considered disclosure standards developed by international organizations such as the TCFD. |

In July 2021, the China Securities Regulatory Commission issued amendments requiring listed companies to disclose environmental administrative penalties and encouraging carbon emissions disclosures. On December 11th, 2021, the China’s Ministry of Ecology and Environment (MEE) has issued new disclosure Rules that will require domestic entities to disclose a range of environmental information on an annual basis. What to disclose? Covered entities must disclose information on environmental topics including: environmental management; pollutant generation; carbon emissions; and contingency planning for environmental emergencies. They must also disclose climate change, ecological and environmental protection information related to investment and financing transactions. Entities concerned The rules apply to domestic listed companies and bond issuers that were subject to certain environmental penalties in the previous year and other entities identified by the MEE, including those that discharge high levels of pollutants. Timeline of implementation The climate disclosure rules have been effective since February 8th, 2022. |

Source: Natixis GSH, based on a review of national regulations and declarations

To go further:

- Natixis GSH, “USA – 2020 Presidential election. The great divide: opposing US climate policy”, October 2020, available here.

- Natixis GSH, “Towards a Task Force for Nature-related Financial Disclosures and investors’ appetite for science-based targets on natural capital”, October 27th, 2020, available here.

- Natixis GSH, “The UK about to impose mandatory TCFD climate disclosure and to issue a sovereign Green Bond”, November 30th, 2020, available here.

- Securities and Exchange Commission, “The Enhancement and Standardization of Climate-Related Disclosures for Investors”, proposed rule, March 21st, 2022, available here.

- EFRAG, “Draft European Sustainability Reporting Standards”, Exposure Drafts, April 29th, 2022, available here.

- IFRS, “IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information”, Exposure Draft, March 2022, available here.

- IFRS, “IFRS S2 Climate-related Disclosures”, Exposure Draft, March 2022, available here.

[1] It applies to a registrant with Exchange Act reporting obligations pursuant to Exchange Act Section 13 (a) or Section 15 (d) and companies filing a Securities Act or Exchange Act registration statement.

[2] Securities and Exchange Commission, Proposed rule: The Enhancement and Standardization of Climate-Related Disclosures for Investors, March 21st, 2022, available here (Fact sheet available here).

[3] From 2016 to 2019, SEC Investor Advisory Committee conducted discussions to find out more from market participants on the perceived need from investors to have material and comparable information. In May 2020, it published its recommendations.

[4] In 2020, the SEC Asset Management Advisory Committee’s ESG subcommittee drafted recommendations on the SEC adopting standards for ESG risks disclosures.

[5] It applies to a registrant with Exchange Act reporting obligations pursuant to Exchange Act Section 13 (a) or Section 15 (d) and companies filing a Securities Act or Exchange Act registration statement.

[6] 17 CFR 240.12b-2: “Large accelerated filer” as an issuer after it first meets the following conditions as of the end of its fiscal year: (i) the issuer had an aggregate worldwide market value of the voting and non-voting common equity held by its non-affiliates of $700 million or more, as of the last business day of the issuer's most recently completed second fiscal quarter; (ii) the issuer has been subject to the requirements of Section 13(a) or 15(d) of the Exchange Act for a period of at least twelve calendar months; (iii) the issuer has filed at least one annual report pursuant to Section 13(a) or 15(d) of the Exchange Act; and (iv) the issuer is not eligible to use the requirements for SRCs under the SRC revenue test).

[7] As required by the EU’s Corporate Sustainability Reporting Directive proposal (with an option to move towards reasonable assurance in the future).

[8] The Commission’s rules define a smaller reporting company to mean an issuer that is not an investment company, an asset-backed issuer, or a majority-owned subsidiary of a parent that is not a smaller reporting company and that: (1) had a public float of less than $250 million; or (2) had annual revenues of less than $100 million and either: (i) no public float; or (ii) a public float of less than $700 million. See 17 CFR 229.10(f)(1), 230.405, and 17 CFR 240.12b-2.

[9] Definition of the US Supreme Court:

a. “If there is a substantial likelihood that a reasonable investor would consider them important when making an investment or voting decision”; or

b. If it "has market significance”; or

c. If it “would be viewed by a reasonable investor as having altered the total mix of information made available to holders of securities”.

[10] A safe harbor is defined as follows by Cornell Law School: “a provision granting protection from liability or penalty if certain conditions are met. A safe harbor provision may be included in statutes or regulations to give peace of mind to good-faith actors who might otherwise violate the law on technicalities beyond their reasonable control.”

[11] As part of the financial statements, the proposed financial metrics would be audited by an independent public accounting firm in accordance with existing Commission rules and PCAOB auditing standards.

[12] Excepting such line item reporting when the aggregate impact of the events is less than one percent, the proposed rule would reduce overall costs for firms associated with disclosures for instances where the impact is likely to be quite small, while providing assurance to investors that more significant impacts are reflected in line item reporting.

[13] The first public comment period for the release was originally scheduled to close on May 20th, 2022.

[14] Especially concerning the publication of climate targets (in particular regarding the alignment with the Accord de Paris), the methodology used to estimate the targets, the monitoring of climate and biodiversity risks, the assessment of potential impacts, the transition policies and the percentage of assets exposed to risks.

[15] US Securities and Exchange Commission, “Enhanced Disclosures by Certain Investment Advisers and Investment Companies About ESG Investment Practices”, May 25th, 2022, available here.

[16] According to the statement of Chair Gary Gensler.

[17] According to the proposal, an “ESG-Focused Fund” means “a fund that focuses on one or more ESG factors by using them as a significant or main consideration (1) in selecting investments or (2) in its engagement strategy with the companies in which it invests”. Examples: funds that track an ESG-focused index or that apply a screen to include or exclude investments in particular industries based on ESG factors.

[18] IFRS, “IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information”, Exposure Draft, March 2022, available here.*

[19] IFRS, “IFRS S2 Climate-related Disclosures”, Exposure Draft, March 2022, available here.

[20] EFRAG, “Draft European Sustainability Reporting Standards”, Exposure Drafts, April 29th, 2022, available here.

[21] UK companies that have to produce a non-financial information statement:

a. UK companies that have more than 500 employees and have either transferable securities admitted to trading on a UK regulated market; or

b. Banking companies or insurance companies (Relevant Public Interest Entities (PIEs)).

[22] Making Scope 1 GHG emissions mandatory for all reporting issuers is one option.

[23] The consultation period will close on April 29th, 2022, and these proposed amendments will apply from 2022-2023 reporting year. In particular, they would update the methodology to calculate Scope 2 emissions and create a new biomethane fuel type.