Low-carbon hydrogen: sensing the path towards large-scale deployment

6-minute read

In the energy sector, the year 2020 has undoubtedly been that of a change of dimension for low-carbon hydrogen, as illustrated throughout the past six months by the multiplication of hydrogen-centric projects in industry, mobility and energy, but also by the importance of this nascent industry in the recovery plans recently drawn throughout Europe (EU and Member States' levels).

Various energy scenarios developed to model the diffusion of hydrogen in the economy suggest massive growth in the share of the molecule in the satisfaction of final energy demand, from nearly 0 today. According to the Hydrogen Council's January 2020 report, hydrogen could address 8% of primary global energy demand in 2030 and 15% by 2050.

With such massive growth, diffusion of hydrogen uses would be instrumental in the world economy progressing towards climate neutrality in the next three decades.

To achieve this, however, it is for a series of changes that the current hydrogen industry and existing economic structures must prepare. In fact, more than 95% of hydrogen is produced today by methane reforming, a technique using natural gas and, to a lesser extent, coal as raw material. In this form called "grey", hydrogen cannot be considered as a real decarbonization agent insofar as its production is very carbon intensive (world median of 9 kgCO2 emitted per kg of hydrogen produced). It is only in its "blue" (reforming methane with CO2 capture) and "green" (electrolysis of water supplied by low-carbon sources of electricity) forms that the molecule can claim a meaningful role in the decarbonization of the global economy.

In these forms, by replacing fossil fuels which are very largely dominant in existing energy and industrial systems (alone or in addition to other decarbonization agents, in particular low-carbon electricity), hydrogen can actively contribute to the decarbonization of a series of hard-to-abate sectors:

- Industry using the molecule as energy carrier and / or as feedstock (chemicals, steel, glass and cement production, refining);

- Different segments of land, sea and air mobility and

- Heating and electricity supply for buildings and industry.

Better still, produced by the electrolysis of water, hydrogen offers new perspectives to the management of electricity and gas value chains, mainly because it offers an implicit solution of large-scale storage of low-carbon electricity, whether of renewable or nuclear origin (“Power-to-Gas paradigm”). However, to play this role of "systemic" decarbonization agent, low-carbon hydrogen will have to overcome a number of obstacles related to:

- The high cost of producing the molecule in its blue and green forms (production costs 2x to 6x higher than for grey hydrogen);

- The technical and economic problems associated with the transport and distribution (hydrogen refueling stations) of the molecule, which almost triple the cost for the end consumer; and

- The still embryonic nature of hydrogen applications in a number of sectors, in particular in transport where, in certain segments (trucks, ships, aircrafts), FCEVs (fuel cell electric vehicles) have the potential to respond to some current technical limitations of BEVs (battery electric vehicles) that are probably prohibitive. Thus, in mobility, apart from the case of passenger cars which have just entered the commercial deployment phase, other potential applications of hydrogen are at best in the demonstration phase (trains and buses).

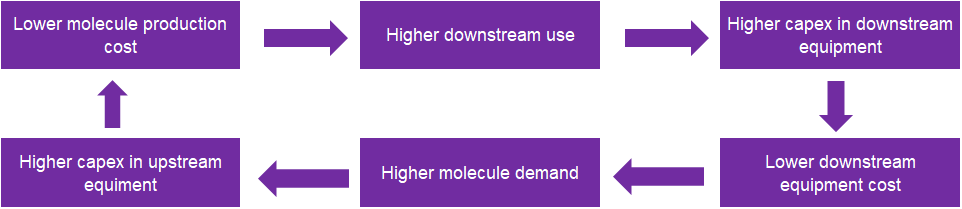

Being still in the structuring phase with very limited uses in volume, the hydrogen value chain mainly faces scale issues. These scale issues account not only for the high costs incurred in the production of green and blue hydrogen, but also for the limited deployment thus far of hydrogen-centric applications of the molecule vis-à-vis established, fossil-fuel centric applications, but also emerging low-carbon ones (as currently seen in the passenger vehicle segment).

Observation of these challenges highlights the need for coordinated action along the value chain, this through two main levers:

- Lowering the molecule cost through massive investments in electrolyser factories. If triggered, this cost reduction dynamic is likely to generate a virtuous circle involving the increase in hydrogen demand and investment in the manufacture of all equipment along the value chain (electrolysers and downstream equipment, in particular in mobility), a prerequisite for the industrialization of the sector and the acceleration of the fall in costs;

- Getting around the logistical and economic problems linked to the transport and distribution of hydrogen by concentrating, through “local hubs”, the production of the molecule and its various downstream uses, starting with mobility and industrial activities where hydrogen is already used as feedstock (ammonia production).

Figure 1: scale challenges in the nascent low-carbon hydrogen industry

Source: Natixis

Somewhat theoretical, these elements should not obscure the diversity of situations across the globe and the specialization that could take place in the production and use of low-carbon hydrogen. In certain regions (Australia, North Africa, Latin America, Saudi Arabia, etc.) characterized by a high potential for renewable energy production (in particular wind and solar PV), the production of green hydrogen has a good chance of eventually reaching cost-parity with grey hydrogen. In others (North America, Northern Europe), the production of blue hydrogen has significant potential due to the large presence of raw material (natural gas), sites suitable for CO2 storage and a diversified industrial sector, allowing a wide distribution of the uses of hydrogen. Finally, other zones not benefiting from these advantages but having substantial industrial production bases (Western Europe, Japan, South Korea) are likely to seek specialization in the manufacture of upstream (electrolysers) and downstream equipment (FCEVs).

On the way to achieving potential cost parity with grey hydrogen and then with natural gas, blue and green hydrogens present specific trajectories, the former relying on industrialization / large-scale deployment of CCS, the latter on industrialization of electrolysis and further cost abatement in wind / solar PV. Although the conditions for the success of these two technologies remain largely dependent on local conditions, in view of the recent cost deflation affecting electrolysers (-40% on alkaline water electrolysers since 2014) and even more renewable energies (levels <$25/MWh for solar PV in certain areas), it is reasonable to anticipate greater cost reductions in the production of green hydrogen than in that of blue hydrogen.

From a strictly temporal point of view, even if the recovery plans announced in Europe could somehow affect the sequencing of investments planned by industrial players before the Pandemic, sector development will likely be done in various stages:

- By 2030, as indicated above, the priority is to massively lower the costs of electrolysis alongside gradual diffusion of downstream uses of hydrogen, particularly in land mobility and industry where the molecule is already used as feedstock for the production of chemicals, in order to develop demand and stimulate R&D efforts in other, less-advanced applications.

- Once this stage is completed, perhaps between 2030 and 2040, there will be a phase of gradual deployment of networks dedicated to the transport of hydrogen in pure form, so as to support the dissemination of uses, in particular in industry and mobility, and foster interconnection between the various local hydrogen hubs having emerged by then;

- Then, probably not before from 2040, a last phase of development of the sector would see the large-scale deployment of the molecule in its low-carbon form for specialized uses in industry (production of methanol, for example), in parallel with the trivialization of its use in land mobility and its possible development in air and sea transport.

Figure 2: potential timeline for low-carbon hydrogen diffusion

Source: Natixis

These elements form the basis of a scenario in which rising demand for hydrogen, upscaling of electrolysis and downstream uses would fuel a virtuous circle making it possible to reach in 2050, in some areas, levels of production costs for green hydrogen lower than those currently for grey hydrogen (>$1/kg vs. a range of $2.3-$4.6/kg currently).

However, even assuming such a drop in production costs for the molecule in its green form, it is likely that the spread of its uses in a number of industrial activities currently based on fossil fuels will depend on the implementation of carbon pricing systems, a system that exists on a large scale only at the level of the European Union, in the form of a CO2 emissions cap-and-trade system. The profusion of project launches in blue and green hydrogen reveals the dynamism of a certain number of industrial and energy players and their belief in the potential for the entire sector ultimately achieving commercial viability. The analysis of these projects and, more generally, the apprehension of the investment needs by 2030 to generate the scale effects necessary to lower costs (some $280bn) reveals the importance of public support in this process.

In addition to direct aid for pilot projects in the sector, governments will have to provide the regulatory visibility required for risk-taking on the part of industrial players, but also provide relevant price signals (role of carbon prices, in particular in hard-to-abate sectors) to encourage investments in low-carbon technologies being diffused. The deployment of assets along the value chain will most likely require the establishment of innovative financing schemes replicating the “infrastructure model” involving a large sample of actors (equipment suppliers, users, public authorities, commercial banks and development banks) and covering the widest possible range of upstream and downstream equipment.

In this emerging ecosystem, sustainable finance will have a critical, twofold role to play: mobilize the collective savings available to finance the development of the sector and ensure transparency in the use of private capital and build confidence in the investor base. The development of low-carbon hydrogen production presents a certain number of issues and potential risks, for the moment theoretical in view of the state of development of the sector: extent of water resources required for large-scale deployment of electrolysis and potential damage to biodiversity as far as green hydrogen is concerned as well as safety of carbon transport and final storage, as far as blue hydrogen is concerned.

These risks and issues must be understood by the various stakeholders (private companies, governments, NGOs, local communities) and integrated into the structuring of financing products / solutions for the sector. Integrating these issues and risks and, in doing so, promoting best practices in the emerging industry constitute a major challenge for sustainable finance in its support of the world economy’s decarbonization.

TO GO FURTHER