ISS acquisition by Deutsche Börse in a context of mounting ESG data sourcing quality & sovereignty concerns in Europe

9-minute read

In November 2020, the operator of the Frankfurt stock exchange, Deutsche Börse acquired 80% of the American company, Institutional Shareholder Services group of companies (ISS), a leading governance, ESG data and analytics provider, valued at more than €1.9 billion [1].

The acquisition is expected to close in the first half of 2021 and is now subject to regulatory approvals.

According to Edelman's Institutional Investor Trust Report [2], ISS ESG ranks number 2, out of 10 major ESG rating agencies most used as part of investment decision-making by U.S. investors. In the same ranking, Bloomberg is classified first, followed by Sustainalytics, CDP and S&P (RobecoSAM). ISS serves more than 4,000 customers, including leading institutional investors worldwide. From ESG Fund Rating to ESG index solutions, governance data, climate solution and advisory services, ISS ESG offers a diversified range of solutions for market players.

The deal represents the fourth ownership change of ISS in a decade. Genstar Capital, a Private Equity fund, which is the current owner of ISS, bought the firm for $720 million in 2017 from Vestar Capital Partners. In 2014, Vestar Capital Partners bought the company for $364 million from MSCI, which had owned the company since 2010. Since the acquisition from Vestar Capital Partners, the value of the company had been multiplied by 5 and net sales are since then expected to grow annually by 5% on average until 2023.

The ESG expertise and the data-side range of ISS services is reportedly complementary to Deutsche Börse’s business model, which covers the securities trading chain and data analysis. The deal marks the latest example of a stock-exchange company bulking up its offerings by joining forces with an ESG provider of data and analytics. Indeed, the landscape of ESG data or rating providers have been particularly reshuffled by acquisitions over the last few years (see table 1 below).

Table 1. Recent major mergers and acquisitions on the ESG data provision market since 2018

Source: AMF (2020), provision of non-financial data: mapping of stakeholders, products and services

A growing and increasingly strategic ESG data market

- A growing market in terms of size

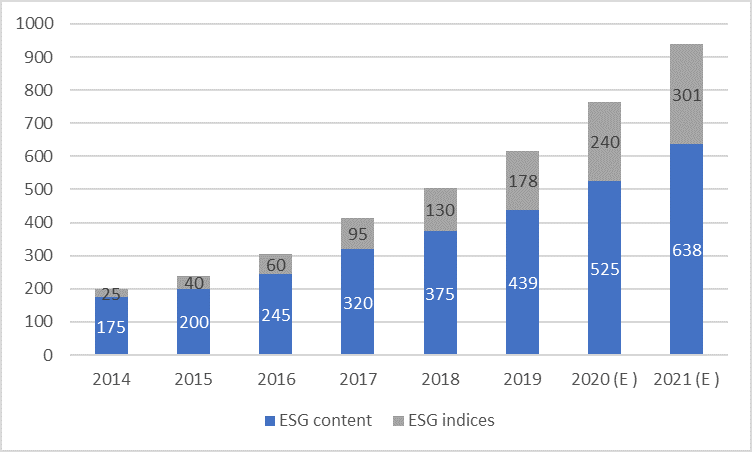

The market of ESG data has increasingly grown since the last decade and could reach a yearly revenue of $1 billion by 2021 according to Opimas’s report “ESG Data Market Not Stopping Its Rise Now” [3]. In 2019, the ESG market data generated $617 million of revenue and is expected to grow annually by 20% in 2020. The growth of the ESG data market has been supported by the regulatory agenda all around the world, notably in Europe. But if originally ESG data was used for compliance or “tick the box” marketing strategies by financial institutions, it also gradually became a key component of investment decisions.

Figure 1. ESG data market size (in $ billion)

Source: Opimas

According to Opimas’ study, 60% of expenses in ESG data are incurred by European actors, mostly investors. In 2015, the amount of assets subject to sustainable investment strategies and/or criteria represented 51% of total European assets under management (AUM) compared to 47.5% in 2011 [4]. In 2016, the asset under management on the European sustainable investment fund market represented €476 billion with 2413 funds compared to €251 billion with 1503 funds in 2010 according to a study conducted by KPMG (2017).

-

A matter of national and regional sovereignty

The predominant spending on ESG data in Europe is particularly due to an increasing number of investment regulations. For instance, in France, the Article 173 of the law on energy transition and green growth, defines the reporting obligations of institutional investors regarding their consideration of ESG criteria, has been in force since January, 2016, and has in part inspired the EU Sustainable Finance Action Plan .

North America accounts for one-third of the market and Asia accounts only for a small portion of expenses on ESG data acquirement. Asset managers are the largest consumers of ESG data, accounting for 59% of purchases.

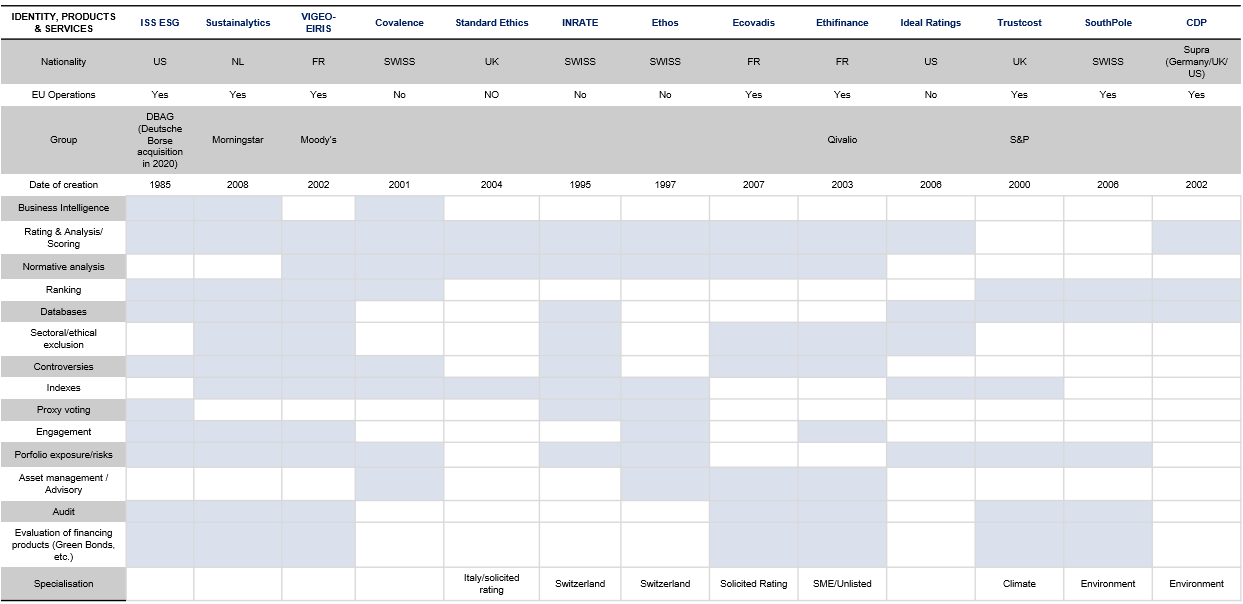

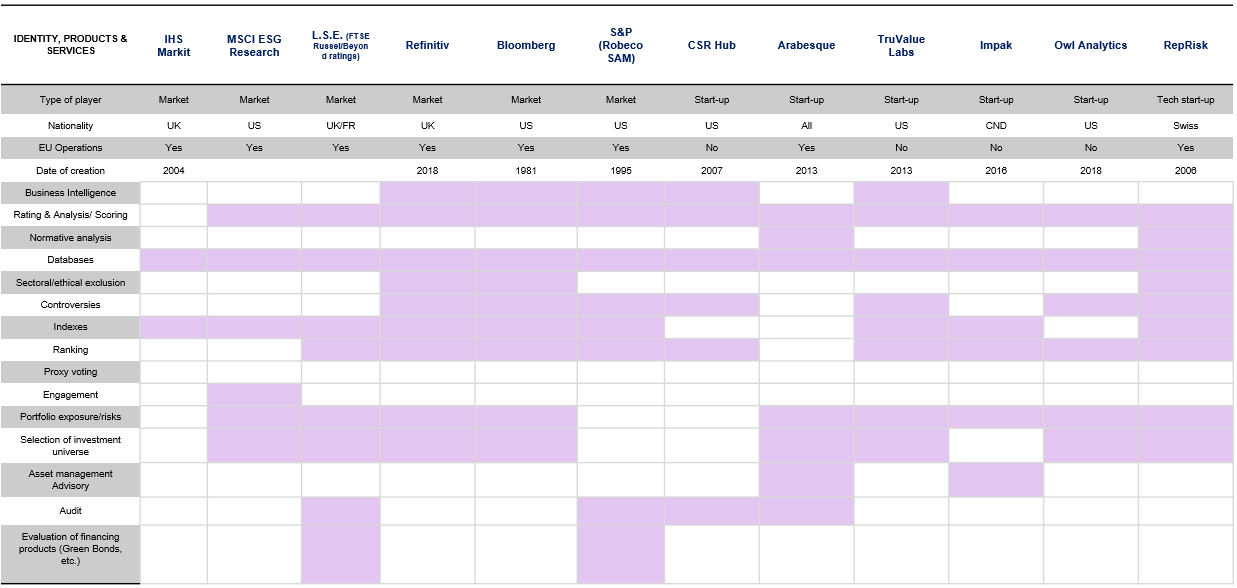

Today, ESG data is mostly used in Europe, however the vast majority of ESG data players have their head office outside of Europe. A recent report by the French Market Authority (AMF) mapping stakeholders, products and services, shows that among a sample of the 25 main companies[5] in the ESG market, 80% have their head offices outside the European Union. However more than half of these 20 players have a presence in European Union in the form of subsidiaries, branches or offices.

-

The evolution of ESG providers services and profiles

Four categories of ESG providers could be identified:

- Generalist data providers (e.g., Bloomberg or Refinitiv), index producers (MSCI) as well as stock exchanges (London Stock Exchange and Deutsche Börse)

- ESG-focused data vendors (e.g., ISS-ESG, Sustainalytics, Carbon4 Finance, CDP)

- Credit rating agencies (e.g., Moody’s and S&P) and exchanges (such as LSE, JSE, etc.). Moody’s and S&P have recently acquired ESG data providers (Trucost for S&P, Four Twenty Seven for Moody's) and ESG ratings firms (RobecoSAM's ESG rating subsidiary for S&P, Vigeo-Eiris for Moody's).

- Asset managers with ESG research subsidiaries (e.g., Arabesque, RobecoSAM's ESG rating subsidiary, etc.).

Figure 3. Overview of ESG data provider new entrants

Source: AMF (2020), provision of non-financial data: mapping of stakeholders, products and services

Source: AMF (2020), provision of non-financial data: mapping of stakeholders, products and services

AI sets the stage to new ESG data niches

The emergence of new technologies such as big data and artificial intelligence has allowed the development of new entrants like technology start-ups, in the ESG market. For example, Trendeo, a data provider focused on employment and investment in France, has accumulated nearly 60,000 data points affecting employment and investment since 2009. This data is collected through search engines using keywords related to employment. Trendeo offers a semi-automatic collection, based on both numerical tools (keyword, tagging, algorithm) and manual analyst verification. The data is updated daily, classified by type of operation, sector (SIRET, NAF 2008 sector), geographical area (GPS coordinates, address, employment area, department, region), country of origin, size of investor (VSE, SME, ETI, large company). Other companies like CSRHub that rely on data from other providers and aggregate ratings should stimulate the ESG data market in terms of transparency and accessibility.[6]

Initially, the players in the ESG market were raw data providers on environmental, social and governance issues. Today their role has been expanded as they offer diversified products and services such as:

- Portfolio Analysis

- Construction of financial indexes

- ESG strategy definition support

- Evaluation and certification of financing products such as green bonds, social bonds or sustainability-linked bonds

The ESG data sector is therefore in full expansion, whether in terms of market depth, types of products and services offered, geographic scope or players.

ESG data providers and users are still facing growing challengers

Traditional ESG data providers have attempted to strengthen their offer and have increased their coverage over recent years but they are still struggling to solve key ESG data challenges. In the consultation on Renewed Sustainable Finance Strategy, the majority (57% of 408 respondents) rated as “poor” both the comparability, quality, and reliability of ESG data from providers currently available in the market, as well as the quality and relevance of ESG research material [7].

A non-exhaustive list of ESG data challenges could be identified [8]:

- Lack of forward-looking data for scenario analysis

- No robust link with the UN Sustainable Development Goals

- Insufficiency of granular data to measure impacts at a local level

- Low trust in the quality of company-reported information with inconsistent methodologies and disclosures

- Difficulty in linking ESG performance with financial performance

- Inconsistent data across asset classes

- Low correlation between ESG data providers due to inconsistent methodologies and data sources

Let’s delve further into a few important challenges.

One of the major challenges is the lack of certain data. For example, in the fight against climate change, data linked to scope 3 emissions is still difficult to account for in certain sectors and there is a lack of standards to estimate them. Indeed, to assess climate alignment of assets or market players, financial actors need ESG data covering a high degree of granularity with a standardized and practical use. The challenge is to find the right balance between usability and granularity.

The issue for market participants is not only the lack of information, but also the quality of the information published. To identify the “good” explanatory data, market players need to know the definition of the indicators used, the scope concerned and the stability of the publications of the same data over several years, but above all to have standardized data to compare them within a group “peer”.

However, comparisons are still delicate and risky, and work on homogenization is still underway.

Regulations and taxonomies to standardize the use of ESG criteria

All around the world, regulations and taxonomies are underway to standardize ESG criteria and improve the quality of raw ESG data. In Europe, the European Commission published in November, the long-awaited Draft Delegated Act under the Taxonomy Regulation (see our article). This legal text specifies the technical screening criteria under which specific economic activities qualify as contributing substantially to climate change mitigation and adaptation. In line with the Taxonomy, to strengthen the foundations for sustainable investment, the European Commission committed to review the non-financial reporting directive (NRFD)[9] in the first semester of 2021. The NFRD can be decisive provided it is set to require extensive use of Taxonomy and spur large-scale appropriation. As a reminder, the main issue with the NFRD right now is that it only covers large public-interest companies with more than 500 employees. SMEs have no similar requirements imposed on them and therefore ESG data is still not systematically available. At an international level, the Task Force on Climate-related Financial Disclosures (TCFD) final report, published on June 2017, specifying the elements of climate reporting expected incorporates reference documents, focusing on 4 pillars: governance, strategy, risk management and metric & targets will also create more transparency in the financial market. Indeed, last November, the UK announced that it will make mandatory economy-wide disclosures in line with the Task Force on Climate-related Disclosures (TCFD) by 2025 (see our article “The UK about to impose mandatory TCFD climate disclosure and to issue a sovereign Green Bond”).

This month, with a view to improving the transparency of non-financial data, the French Financial Market Authority (AMF) and its Dutch counterpart, the Autoriteit Financiële Markten (AFM), propose a framework for data and extra-financial service providers which could be one of the key measures of the European Commission’s renewed strategy on sustainable finance.

The AMF and the AFM propose the establishment of a European regulation, which would entrust to the ESMA the supervision of the actors operating on a professional and commercial basis within the European Union. This regulation would introduce transparency requirements, in particular about methodologies and potential conflicts of interest. It would include organizational and operational requirements to ensure the robustness of data collection and processing. This framework is envisaged as a first step and should be reassessed regularly to take into account future market developments.[10]

How is ISS positioned in European taxonomy-related services or sustainable finance?

Recently, ISS assessed the taxonomy alignment of 75 listed companies in three major European indexes (EURO STOXX, DAX30 and CAC40).[11] The alignment was measured in terms of revenue share derived from economic activities which contribute to climate mitigation or adaptation and are compliant with Taxonomy thresholds and criteria. The ISS report highlights that the overall alignment levels with the EU taxonomy is still low, indicating the need to further green the economy. Across 75 analyzed companies, on average, only 2% of their revenues were found to be fully taxonomy aligned[12]. There is a disparity between the taxonomy and companies’ reporting regarding the granularity of information needed under the taxonomy requirements. This disparity leaves a place for approximation for investors and companies. ISS also confirms that current obstacles, such as data availability, need to be resolved thanks to new reporting requirements under the Non-Financial Disclosure Regulation for example.

This assessment published by ISS was commissioned by the German Federal Ministry for the Environment in the context of Germany’s Presidency of the EU Council in 2020. ISS is also currently developing a Taxonomy Solution to help investors quantify the share of investments which are taxonomy aligned, in order to comply with upcoming disclosure obligations.

This contribution of ISS on the EU taxonomy implementation and operability opens a broader discussion of the ownership of ESG databases. Should it be public or private? Should EU push for local players in this field?

Indeed, ESG data is at the heart of sustainable finance mainstreaming. Among the responses to the public consultation on Renewed Sustainable Finance Strategy published by the European Commission in November 2020, a substantial majority of stakeholders (53% of 355 respondents) agreed that EU policy actions are necessary to maximize digital tools for integrating sustainability into the financial sector. Among the main proposals to ensure accessible and reliable data, respondents mentioned the need to develop a centralized ESG data portal, set-up of an open-source EU wide ESG database, free of charge.

For Alexandre Holroyd, deputy of the French National Assembly, author of the report "Choosing a green finance at the service of the Paris Agreement", presented to Bruno Le Maire, the French Minister of Economy and Finance, this is a question of European sovereignty.

“The takeover of a large majority of European non-financial rating players by international groups is worrisome,” Alexandre Holroyd writes in his report. “The capacity to collect, standardize and analyze this data is crucial and poses an important question of competitiveness and sovereignty.”

For once, the takeover of ISS by Deutsche Boerse comes as a positive response to Holroyd’s concerns: with ISS, the German financial service provider relocates a major ESG data player (Oekom Research which became ISS ESG Research in 2018) in its homeland.

[1] In 2020, ISS is expected to generate net revenue of more than $280 million (IFRS pro forma) and to have an adjusted EBITDA margin of approximately 35%. Net sales are predicted to grow organically by more than 5% per year on average until 2023. Deutsche Börse is waiting for an additional operating profit (EBITDA) of €15 million per year by 2023 for ISS.

[2] Edelman Trust Barometer Special Report : Institutional Investors, available here

[3] Opimas (2020), ESG Data market not stopping its rise now, available here

[4] EC Europa (2018), commission staff working document impact assessment, available here

[5] List of companies in the sample: Arabesque; BLOOMBERG; CDP ;Covalence; CSR Hub; Ecovadis Ethifinance/SpreadResearch; Ethos; Ideal Rating; IHS Markit; Impak; INRATE/zRating; LSEG (FTSE Russel/Beyond ratings); ISS ESG; MSCI ESG Research; Owl Analytics; Refinitiv ; RepRisk; S&P(RobecoSAM); SouthPole; Standard Ethics Ltd; SUSTAINALYTICS; Trucost; TruValue Labs; VIGEO-EIRIS

[6] Trendeo, website, available here

[7] European Commission (2020), Renewed Sustainable Finance Strategy in the EU recovery context,

The Commission received 648 questionnaires. Most of the respondents were business associations (23%, 146 answers), EU citizen (22%, 140 answers) followed by financial companies (14%, 90 answers).

[8] BNP Paribas (2019), fintechs and the ESG data challenge

[9] The non-financial reporting directive (NFRD) – lays down the rules on disclosure of non-financial and diversity information by large companies. EU rules on non-financial reporting only apply to large public-interest companies with more than 500 employees. This covers approximately 6,000 large companies and groups across the EU. More information available here

[10] AMF (2020), Position Paper: Call for a European Regulation for the provision of ESG data, ratings, and related services, available here

[11] ISS (2020) Measuring the taxonomy alignment of European large caps, available here

[12] Taxonomy relevant + substantial contribution + do no significant harm + minimum social safeguards (fully aligned)