Investors’ actions and appetite for social bonds in response to Covid-19

The sanitary Covid-19 crisis has affected, since its start, all parts of the economy, and financial markets. A response to the Covid-19 crisis is arising from the world of sustainable finance from lenders as well as investors.

On the one hand, coalitions of investors have called for action.

A new investor coalition, led by Domini Impact Investments, the Interfaith Centre for Corporate Responsibility, and the Office of the New York City Comptroller, has been launched: “The Investor Statement on Coronavirus Response”. 195 investors, representing USD 4.7trn have already signed the statement which is a call for investee companies to protect employees, customers and suppliers through the current Covid-19 crisis. This statement, however, does not include specific commitments nor a precise action plan from investors.

The Principles for Responsible Investment (PRI) has issued a guide on “How responsible investors should respond to the Covid-19 Coronavirus crisis” highlighting immediate actions to take between engagement, support, and maintaining a long-term focus in investment decision making.

The International Corporate Governance Network (IGCN) considers Coronavirus as a new systemic risk. ICGN also considers the role of institutional investors and how this crisis links to their own fiduciary duties, investment horizons and stewardship practices. It recommends investors to keep calm and maintain a long-term perspective.

SRI investors are reshaping their sustainability-themed investment strategies in the face of the crisis and of the necessary anticipation of its long-term effects, some of whom specifying response to Covid-19 must be done in alignment with the SDGs.

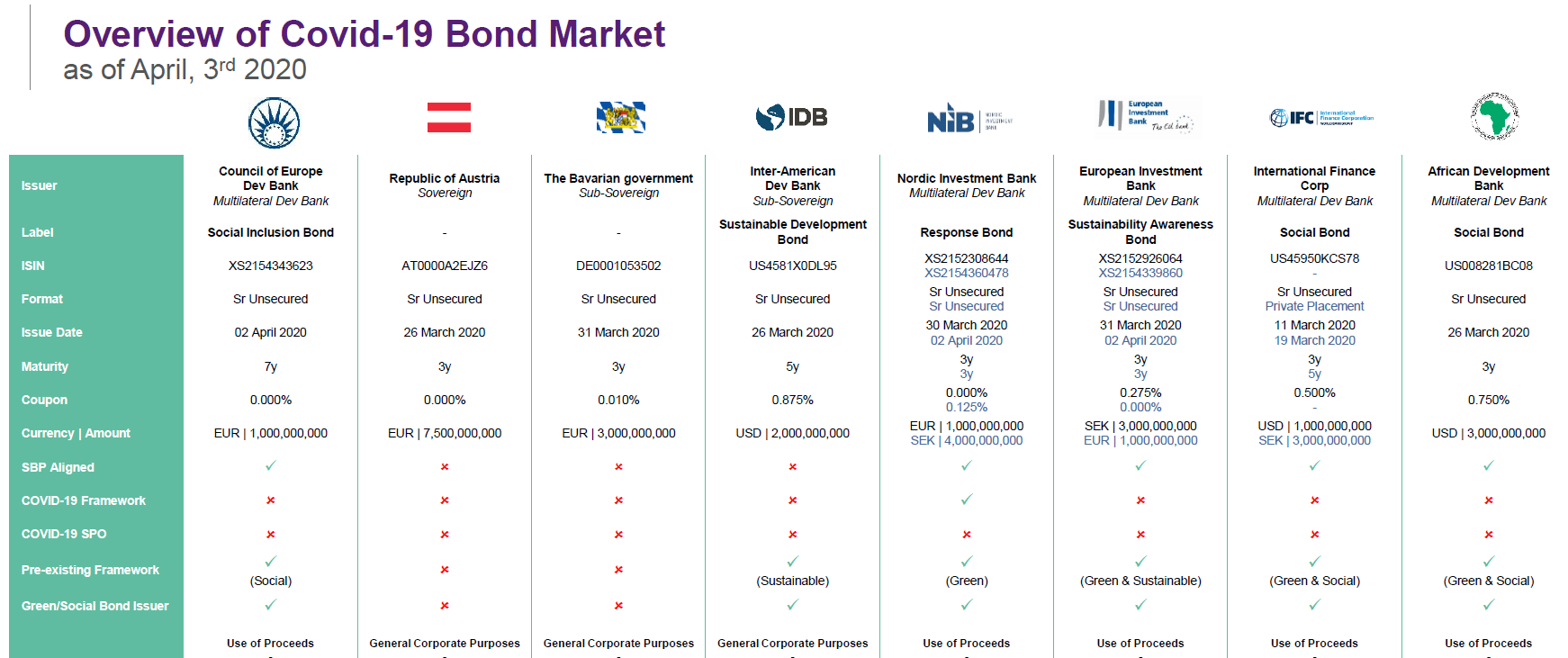

On the other hand, lenders/ borrowers, mostly SSAs, have started issuing Covid-19 related bonds, some of which under the Social Bond format. The International Finance Corporation (IFC), the Bavarian Government, the Republic of Austria, the Inter-American Development Bank (IADB, or IDB), the African Development Bank (AfDB), the Nordic Investment Bank (NIB), the European Investment Bank (EIB), and the Council of Europe Development Bank (CoE, or CEB) are amongst the issuers of such bonds.

- IFC explained that proceeds from a previous USD1bn bond issuance will benefit under-served communities across the developing world, including in countries affected by the coronavirus; and proceeds from its SEK 3bn bond are intended to support companies hit by the coronavirus crisis.

- IADB’s global sustainable development bond will concentrate support into four main areas: the immediate public health response, safety nets for vulnerable populations, economic productivity and employment, and fiscal policies for the improvement of economic impacts.

- AfDB’s “Fight Covid-19” social bond issuance, which can be considered as a landmark transaction as it is the largest USD denominated social bond transaction to date in capital markets (USD3bn), under its Social Bond program, will be used to provide support and financing to countries and businesses fighting against Covid-19.

- NIB “Response Bond”, the first social bond issued by NIB, under a dedicated framework with no Second Party Opinion (SPO) and limited reporting commitments, will be used to: Lend to public sector for healthcare services, social security expenditures; Lend to financial sector to provide funding for SMEs negatively affected by the pandemic; and Lend to real economy sector for financing of companies in the medical equipment and healthcare sector, and in the infrastructure sector.

- EIB’s sustainability awareness bond proceeds will be allocated to EIB’s lending activities contributing to sustainability objectives, among them lending to health projects substantially contributing to universal access to affordable health services.

- CoE’s social inclusion bond proceeds will be allocated to eligible social loans according to its social inclusion bond framework, which includes support to SMEs for the creation and preservation of viable jobs. Eligible projects have been extended to additional areas of financing related to the health sector such as the acquisition, under emergency procedures, of medical equipment and consumable material; the rehabilitation and transformation of spaces and medical units; and the mobilization of additional expertise.

Overall, these bonds were very welcome by the market as shown by the over-subscription of the order books (x3 to x7), and the presence of SRI investors demonstrate these bonds are falling under their impact investment strategies/ targets.

However, investors should pay attention to the structure of Covid-19 bonds if they are considering delivering a true impact. Indeed, bonds called “Pandemic bonds”, issued in 2017 by the World Bank, for an approximative amount of $425m, are under criticism.

The idea behind the bonds was to place some of the risk for low-income countries of a pandemic onto the financial markets, rather than their own governments' budgets. However, today they are accused of having structural flaws that prevent them from supporting poor countries hit hard by infectious diseases.

These bonds deliver interest payments to investors until certain trigger conditions are reached, at which point the money is not repaid in full and funds are used instead to help tackle the crisis.

Back in time, investors were able to buy two different tranches of the bonds.

- Tranche A of the bonds, which raised $225m, was designed mainly for flu outbreaks but also covers coronavirus. It offers investors annual interest of Libor plus 6.9 per cent and requires more than 2,500 deaths in developing countries as a result of a pandemic.

- Riskier Tranche B ($95m), which was designed to cover coronavirus and Ebola, pays Libor plus 11.5 per cent until a total of 250 deaths in the origin country, plus at least 20 of them in a secondary country, and that 12 weeks have passed since the original outbreak.

Although the so-called pandemic bonds look set to result in a payout to developing countries, critics have said the conditions are too stringent and that investors have already made money on them due to the regular coupon payments they have received on the back of the initial purchase.

Many critics have also pointed to the fact that the severe attack of Ebola that hit the Democratic Republic of Congo in 2018 did not meet the conditions to trigger payment of the pandemic bonds even though almost 500 people died and that it was one of the largest outbreaks ever recorded.

Since the scheme was initiated almost three years ago, the conditions for payout to countries afflicted by pandemics have not yet been met, but the new COVID-19 coronavirus outbreak looks like it will do so. As a result, it has prompted many of the investors who bought up the bonds to sell them off, as it looks likely that the conditions for the bonds not to be paid back will be met this time.

At last, we should consider even if some developing nations do end up receiving pandemic bond money, it will be a relatively trivial sum when compared with some estimates of the economic damage a sustained coronavirus pandemic would do to developed and developing economies alike.

As the crisis brings back social considerations at the forefront of ESG we are witnessing a huge increase in social bonds whilst green bonds are slightly slowing down.

- Green bonds issuances have made the biggest share of the sustainable fixed income market since 2007, growing by 50% in 2019. However, since the start of 2020, they have declined by 37,7% compared to the same period last year (from $51.4bn to $32bn), according to Environmental Finance.

- Social bonds issuances, on their end, have drastically increased this year, especially in March 2020, as an instrument of funding to respond to the Covid-19 crisis. ICMA published a Q&A on the recourse to Social Bonds to finance emergency response measures and said that the principles are “immediately applicable” to social and sustainability bonds being issued to address the Coronavirus outbreak. On a year to date basis, they have increased by 170,9% according to data from Bloomberg.

Social issues are back in the game.