Integrating sustainability criteria into central banks’ asset purchasing programs – the Swedish Central Bank as a first mover

3-minute read

The Swedish Central will reportedly purchase more green bonds in its asset purchasing programs. At the end of last year, Sweden’s Central Bank (the “Riksbank”) announced its intent to increase its assets purchasing programs and to include green considerations in it. Amid the downturn of the Swedish economy - GDP drop by almost 3.5% in 2020 (available here) - the Riksbank decided to implement additional easing monetary policies for year 2021 on 25 November 2020. The Swedish Central Bank will raise the volume of its asset purchases program by SEK 200 billion (around €1.9 billion) up to a total of SEK 700 billion until end of 2021 (around €6.9 billion). To our knowledge, this is the first time a Central Bank will explicitly target green and sustainable assets.

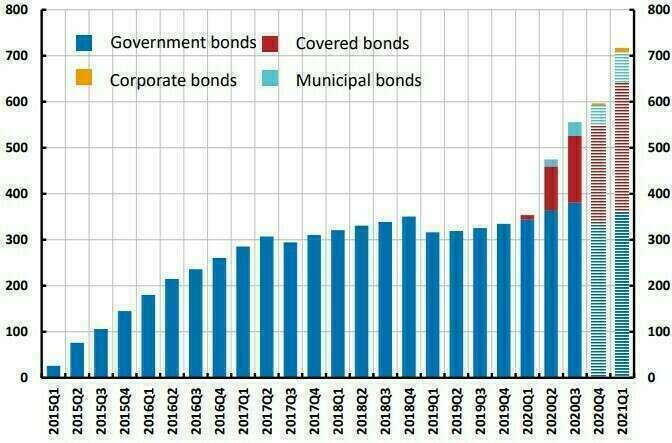

The purchase program will target treasury bills, sovereign and municipal Green Bonds as well as corporate bonds whose issuers comply with “international standards and norms for sustainability” (see details later). Note that Government bonds account for the bulk of the Central Bank’s holdings (representing more than 65% of the Riksbank’s total bond holdings as of Q3 2020, see figure 1) since purchase of covered bonds and municipal bonds only started in Q1-20 and Q2-20, respectively. The expected purchase volumes of corporate bonds (where sustainability criteria will be taken into consideration) will account only for a small fraction.

Figure 1. The Riksbank’s bond holdings (in SEK billion)

Source: The Riksbank, Monetary Policy Report – presentation, November 2020 – availalable here.

To explain its decision, the Riksbank published an article on the impacts of climate change on the Bank (available here). It offers an overview of physical, transition and irreversible climate thresholds effects risks, as well as their impact on monetary policy. In an annex document (available here) details are given on the Quantitative Easing (QE) program. The Bank explains that it runs a monetary policy of achieving a 2% inflation rate while minimizing risks for the financing system’s stability and for its own balance sheet when choosing the adequate tools it uses. The Swedish Central Bank recognizes some of these risks are linked to sustainability “on the basis of the assumption that it is more risky to buy bonds issued by companies that are in breach of universal norm-based principles”, referring to both reputational and climate transition risks. Earlier in November 2019, the Swedish Central Bank had already sold off bonds issued by Australian states of Queensland and Western Australia and by the Canadian province of Alberta (available here) from its foreign exchange reserves because their carbon emissions were considered too high. As a result of this newly disclosed analysis, it states that, the following assets will be purchased between 1 January and 31 March 2021:

1. Swedish nominal and real government bonds and Swedish sovereign Green Bonds to a total nominal amount of SEK 13.5 billion.

2. Bonds issued by Swedish municipalities and regions and by Kommuninvest i Sverige AB (Swedish Local Government Funding Agency) to a nominal amount of SEK 23.5 billion, which may also include purchases of green municipal bonds.

3. From January 2021, only corporate bonds issued by companies deemed to comply with international standards and norms for sustainability shall be purchased on the basis of the UN Global Compact (around SEK 10 billion), a voluntary initiative based on CEO commitments to implement universal sustainability principles (see further details below). Green corporate bonds will be included.

However, the Swedish Central Bank does not provide target purchase levels of green bonds among these three asset types. Meanwhile, the Swedish Central Bank will measure and report the carbon footprint of its corporate bond portfolio which will, according to the Bank, incentivize companies to measure and report their GHG emissions by themselves. Risk on the financial system is the rationale for central banks looking to reduce the exposure of their portfolios to carbon-intensive assets.

In its Sustainability Strategy published on 16 December 2020 (available here), the Swedish Central Bank states “the bond is also required to have been issued by a company that complies with international standards and norms for sustainability” without clarifying its internal process to evaluate such compliance. While this announcement by the Swedish Central Bank will in fine contribute to the mainstreaming of sustainable finance, one awaits for more details concerning mainly the specific criteria that will be looked for in the bond’s and its issuer’s characteristics, as well as the sources of data.

Insights and implications on green and sustainable QE

Central banks (notably the Bank of England and the Dutch Central Bank) increasingly pay attention to the potential consequences of their asset purchasing programs on climate change. They are urged by various stakeholders to take into account sustainability criteria in various ways. There is no single approach. Christine Lagarde, President of the European Central Bank, stated in July that “every avenue [tool] should be explored by central banks to combat climate change” (8 July interview available here). It could be assets weighting adjustment (to purchase more so-called green assets or to reduce exposure to brown assets) or strict exclusions (halting to purchase some assets).

Thereafter, there are different ways to set eligibility criteria: compliance with standards is an option. However, the EU Taxonomy technical screening criteria are not yet finalized and the pool of compliant bonds, using the EU Green Bond Standard, would be too small for monetary policy purposes considering scale constraint. Exclusion — based on the brown share of activities — is another avenue, but there is no commonly agreed threshold or brown taxonomy yet (only lists with companies exposed to solid fossil-fuels are used by market participants). ESG notation and ratings could technically also be used, but it would require central banks to pick one or several private providers, something that is politically sensitive as it would be considered as an endorsement (see our article about ESG rating agencies this month).

If market neutrality tenet is to be accommodated, it requires adjustments (“distortions to correct market failure”) based on reliable, audited, verifiable ESG & Sustainability data that is consensual, something largely absent today. Self-declared conformity to standards, poor quality and questionable independent external verification cannot serve as bedrock for central banks’ green policies.

Taking all this into consideration, one can have doubts about the Swedish Central Bank’s decision to rely on UN Global Compact as a criteria and wonders what data point it will use, if any, to realize a negative screening. The UN Global Compact is largely used but lacks a proper certification scheme. It is broad and universal but very loose, and can be considered rather as a minimum safeguard (excluding major breaches). Some ESG rating agencies like ISS ESG negatively screen companies on the basis of their adherence to international norms on human rights, labor standards, environmental protection and anti-corruption set out in the UN Global Compact and OECD Guidelines.” (available here). Sustainalytics also integrates the compliance with the 10 Principles of the UN Global Compact (available here). Finally, some indexes like the MSCI ESG Controversies Index allow institutionals to screen companies in breach of international norms like the UNGC (available here).This purchasing rule is not very demanding because on top of seven anti-corruption human rights and labour related principles, the three environmental principles of the Global Compact are rather aspirational principles advocating for environmental consideration with no threshold or criteria

At least, if not explicitly supporting or targeting sustainable finance assets because of the interpretation of their current mandates, central banks can at least refrain from stifling market innovation by accompanying the rise of new products. An illustration of such support can be seen for instance in the European Central Bank’s (ECB) decision last September on the acceptance of bonds with coupon structures linked to certain sustainability performance targets (SPTs) as eligible collateral for Eurosystem credit operations and for outright purchases in Eurosystem monetary policy operations (see our article “European Central Bank accepts sustainability-linked bonds as collateral”). The ECB announced it will accept corporate sustainability-linked bonds (Green Bonds are already accepted) as collateral for banks refinancing operations (when coupons are linked with a performance target referring to one or more of the environmental objectives of the EU Taxonomy or to climate change or environmental degradation related SDG) starting from 1 January 2021 (available here). The eurozone national central banks are likely to rely on second party opinion providers to know whether the bonds are compliant with ICMA SLB Principles (read our previous article “Sustainability-Linked Bond Principles : a set of guidelines to help this new product thrive in integrity” or the recently released FAQ on sustainability-linked bonds).