Green Enabling Projects eligibility framing by ICMA, and a first transaction with Vulcan

Introduction

To date, sustainable finance initiatives focused on climate change mitigation have understandably been focused on greenhouse gas (GHG) emissions reduction. Historically this was a focus on an entity’s Scope 1 and 2 GHG emissions and increasingly the focus has expanded to Scope 3 (value chain emissions). From a global macro perspective this is the key lens given the planetary boundaries for GHG emissions. Though, an individual entity does not finance a pro rata share of the global economy, rather entities tend to specialize, either by geography, industries, and/or size of client, and make active decisions on who and how to deploy their capital. Because of this, a focus solely on scopes 1, 2, and 3 can at best obscure, or at worst restrict, investment in activities that while not low-carbon per se, are critical to unlocking the successful transformation of the global economy to a net-zero world, the “green enabling activities”.

So, while the bulk of the sustainable finance industry has until now focused on funding well established “green” activities or encouraging improved sustainability performance of issuers/borrowers. A number of “green enabling” activities, are not currently considered as green per se, but remain critical to these eligible categories, and have not been expressly framed as eligible for use of proceeds approach.

Therefore, on June 25th, 2024, the International Capital Markets Association (ICMA) published a Green Enabling Projects Guidance (available here).

It recognizes the important role Green Enabling Projects play in catalyzing and scaling the transition to a low-carbon economy. This must be done in line with the goals of the Paris Agreement while recognizing the complexities of value chains and challenges of multiple end-uses.

This document provides definition and guidance for Green Enabling Projects encompassing both the induced and avoided emissions dimensions, as well as the management of related environmental and social (E&S) risks. This new guidance strives to solve a missing piece of sustainable finance; which can be synthetized as following: how can an electric car be an eligible green asset if its core and most critical components are not considered climate change mitigators (namely batteries and its necessary metals)? Eligibility criteria for sustainable financing products must span across entire value chains, including upstream phases.

Natixis CIB initiated and has co-coordinated a dedicated taskforce within ICMA to guide market practices based on existing definitions, promote issuer transparency and protect market integrity. In our “2024 horizons” article, we stressed that avoided emissions were an area of intense methodological innovation with a strong interplay with enabling projects. This new guidance could help enhancing access to (sustainable) finance to firms whose contribution to the transition is not properly acknowledged, and whose absolute emissions will grow as the total volume of their products or services is to rise dramatically to accompany and scale up the transition. The goal is to award and encourage emission avoidance from solution providers, should it be capital goods, equipment, key inputs or feedstock.

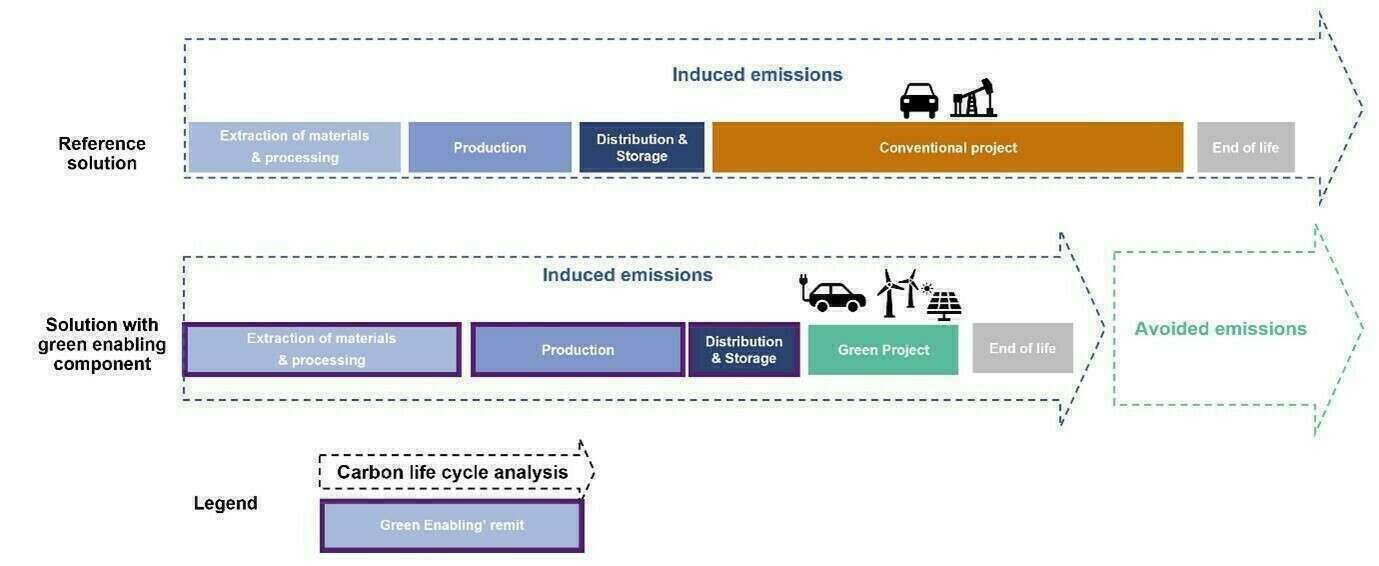

A Green Enabling Project is a necessary component of an enabled Green Project’s value chain, but it is not necessarily a conveyor of a direct positive environmental impact on its own (ex: the lithium mining project, i.e. the Green enabling Project, needed for electric vehicles’ batteries, i.e. the Green Project’s value chain). The enabled Green Project is the one that must deliver a clear environmental benefit, as described in the Green Bond Principles.

A green project’s value chain delivering a clear environmental benefit in avoiding GHG emissions:

Source: Natixis GSH, 2024

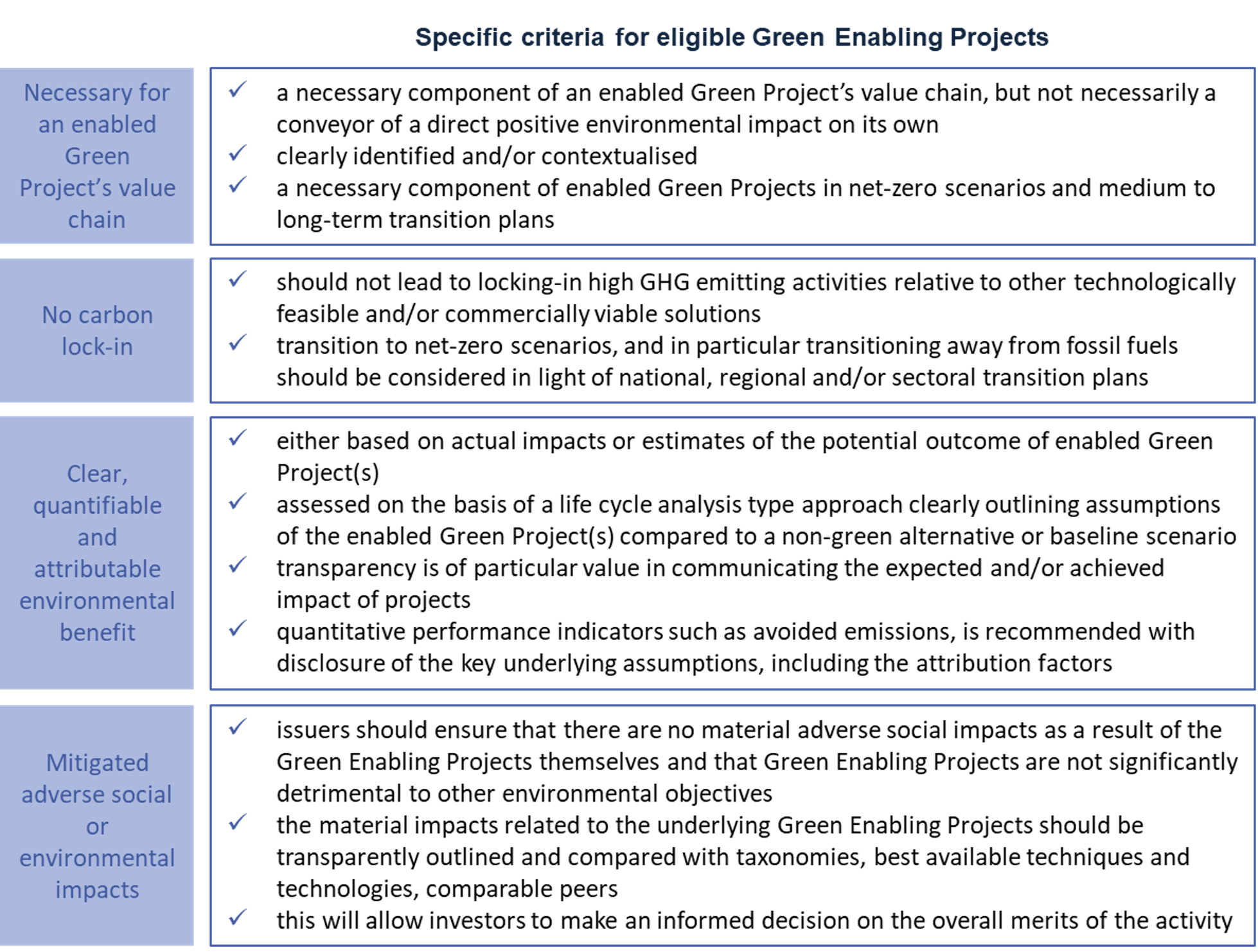

In the guidance document published by ICMA, Green Enabling Projects are subject to all the criteria (to be deemed eligible) described below:

Overview of Taxonomy Objectives and Economic Activities

Source: Green enabling projects guidance, ICMA, 2024.

Up to now, the bulk of the green finance industry has focused on funding well-established “green” activities that have a direct environmental benefit. Those green activities/solutions are assets and entities that directly remove or reduce real-economy GHG emissions. Examples may include a renewable energy asset.

However, to comprehensively address the climate emergency, the sustainable finance market should allocate capital to the entire value chain of a low-carbon / sustainable economy, rather than solely focusing on the end green activity/solution. Indeed, a number of enabling activities that are necessary for the development of green projects must be scaled up and financed to ensure we reach a net-zero economy in time. For example, according to Wood Mackenzie, battery grade lithium demand is forecasted to grow nearly 43 times by 2050 compared to 2020 demand levels and projects announced/funded today only cover a growth of 13 times. Nonetheless, none of the net zero frameworks adopted by financial institutions are including the enabling components[1]. When measuring a financial institution’s carbon footprint or setting decarbonization targets (such as NZBA for banks) we are neither accounting nor valuing the potential impact of being involved in critical raw materials for green activities.

Yet, if you do create that spotlight on this enabling activity, it needs to be framed and objectivized as some of these “green enabling” projects come with ESG challenges (including climate and biodiversity loss) and may have multiple end-uses with variable environmental benefits.

The market guidance does not aim at building another taxonomy defining eligible or ineligible activities. It aims to help issuers objectivize clear enabling environmental benefits through detailed principles and criteria to further enhance transparency.

This market guidance can be used for both bond or loans. Immediate application examples spring to mind in the mining and metals sectors project finance.

Financial actors like to engage in projects where we know 100% of the offtake, but this is not always possible, and so this is when the guidance can come into play.

The guidance has been designed for projects in sectors where the clarity/transparency of the value chain needs to be further developed. This includes, but is not limited to:

- Mining and metals (mapped for example to the clean transportation Green Project category when used in electric vehicles)

- Building and construction supplies and equipment (mapped for example to the pollution prevention and control Green Project category when used to limit air emissions)

- Chemicals and specialty chemicals (mapped for example to the green buildings Green Project category when used for the manufacturing of building insulation materials)

- ICT and telecommunication networks (mapped for example to the energy efficiency Green Project category when used for smart grids)

- Manufacturing of industrial parts and components (mapped for example to the renewable energy Green Project category when used for the development of electricity grids)

Natixis CIB has recently been appointed by Vulcan Energy as its ESG Coordinator, with the aim to secure the first ever green financing aligned with ICMA’s green enabling market guidance (link here)

Vulcan Energy is a fully integrated renewable energy and lithium chemicals company, with access to the largest lithium resource in Europe, Germany’s Upper Rhine Valley. Its ZERO CARBON LITHIUMTM Project aims to produce both renewable geothermal energy and lithium hydroxide monohydrate (LHM) for Battery Electric Vehicles (BEV), from the same deep brine.

Vulcan Energy aims to produce 24,000 tonnes of LHM per annum that could equip 500,000 EVs. The company has binding lithium offtake agreements with some of the largest cathode, battery, and automakers in the world, including Stellantis, Renault, Umicore, LG Energy Solution and Volkswagen. The Project is expected to have a substantial positive environmental impact as the company intends to use zero fossil fuels in its LHM production process.

The Project could have been structured in a pure and simple alignment format with the GBP under the categories:

- Renewable energy production

- Energy efficiency and pollution reduction considering the substantial gains in carbon and water footprint from lithium processes.

However, the contribution of its lithium production to CO2 avoidance in the EV value chain would have been completely overlooked. It is therefore an ideal green enabling candidate as it meets all the criteria for best in class in minimising impacts and avoiding emissions.

A new chapter in sustainable finance is being written with this market guidance. It pushes the green finance market to go one step further by addressing the notion of both necessary supply and end-uses i.e, the criticality of a technology for a certain value chain while looking at induced and avoided impacts, extending the scope of possibilities for new market participants.

[1] Scaling Transition Finance and Real-economy Decarbonization, GFANZ, 2023, available here