2024 horizons

While it’s still time, the Green & Sustainable Hub (GSH) of Natixis CIB is delighted to present its best wishes for 2024 and share insights on the 5 major trends linking 2023 and 2024 in the sustainable finance ecosystem:

- Geopolitics keeps on driving the transformation and regionalization of the global economy;

- Nature is being further monitored and factored in sustainable finance;

- The newly born world objective to “transition away from fossil fuels in energy systems” could create a subset of methodologies and labels;

- Heightened scrutiny revamped the search for integrity, especially around transition claims and planning;

- The market participants’ initiatives to develop “avoided emissions” methodologies (so-called scope 4 emissions).

We’ll stay on the watch to follow the evolution of these trends into 2024. In the meantime, we wish you a pleasant year and an even better read-through.

Yours,

Natixis CIB Green & Sustainable Hub

Showdowns in international relations will continue to reshape economic affairs and obfuscate sustainability considerations. Geopolitics keep reshuffling value chains and driving regionalization. In response, “homeland economics [1] are deployed to reduce the risks “presented by the vagaries of markets, an unpredictable shock such as a pandemic, or the actions of a geopolitical opponent”.

With more than 60 elections around the world, 2024 will turn to be decisive and not only in the USA where ESG is being politicized. Views and financing policies on the defense sector will likely be altered, including a softening among the ESG broad community, particularly vis-à-vis the situation in Ukraine. In 2024, strategic autonomy and industrial policies (ex: on food, energy, medicines) will increasingly be a popular agenda item. The effects of the energy crisis provoked by Russia’s invasion of Ukraine continue to unfold. For the time being, major famines seem to have been avoided, as well as resources shortages and power outages. Value chains were one of the most compelling concerns in 2023 through supply disruptions, shortages, and subsequent inflation. The ways these constraints have been handled have had major ambivalent sustainability impacts. It created foreseeable carbon lock-ins or future stranded assets (LNG) or extended the lifetime of coal power plants. But it also urged countries to double down on low-carbon energy sources (IRA, NZIA), reconsider nuclear as a relevant technology for the energy transition and develop large (commercial) scale national low-carbon equipment manufacturing capacities (batteries or solar gigafactories, green hydrogen production) closer to where they are consumed. It also pushed governments to grab a hold on critical metals and raw materials necessary for the energy transition [2] and sustainability roadmaps delivery.

A significant number of tangible projects answering to these trends and mechanisms are emerging and both raise great appetite from financial institutions willing to support the dual energy transition and security, but also underlines the need for full life cycle analysis and quantification of environmental and social costs and benefits.

In sum, value chains are being reshuffled, shortened, brought nearby, or twisted towards like-minded partners. Subsequently, traceability across those reshuffled value chains is increasingly mandatory, with new legal due diligence provisions being set (such as the EU upcoming Corporate Sustainability Due Diligence Directive (CSDDD)) and the integration of carbon in trade policies (EU Carbon Border Adjustment Mechanism progressive implementation).

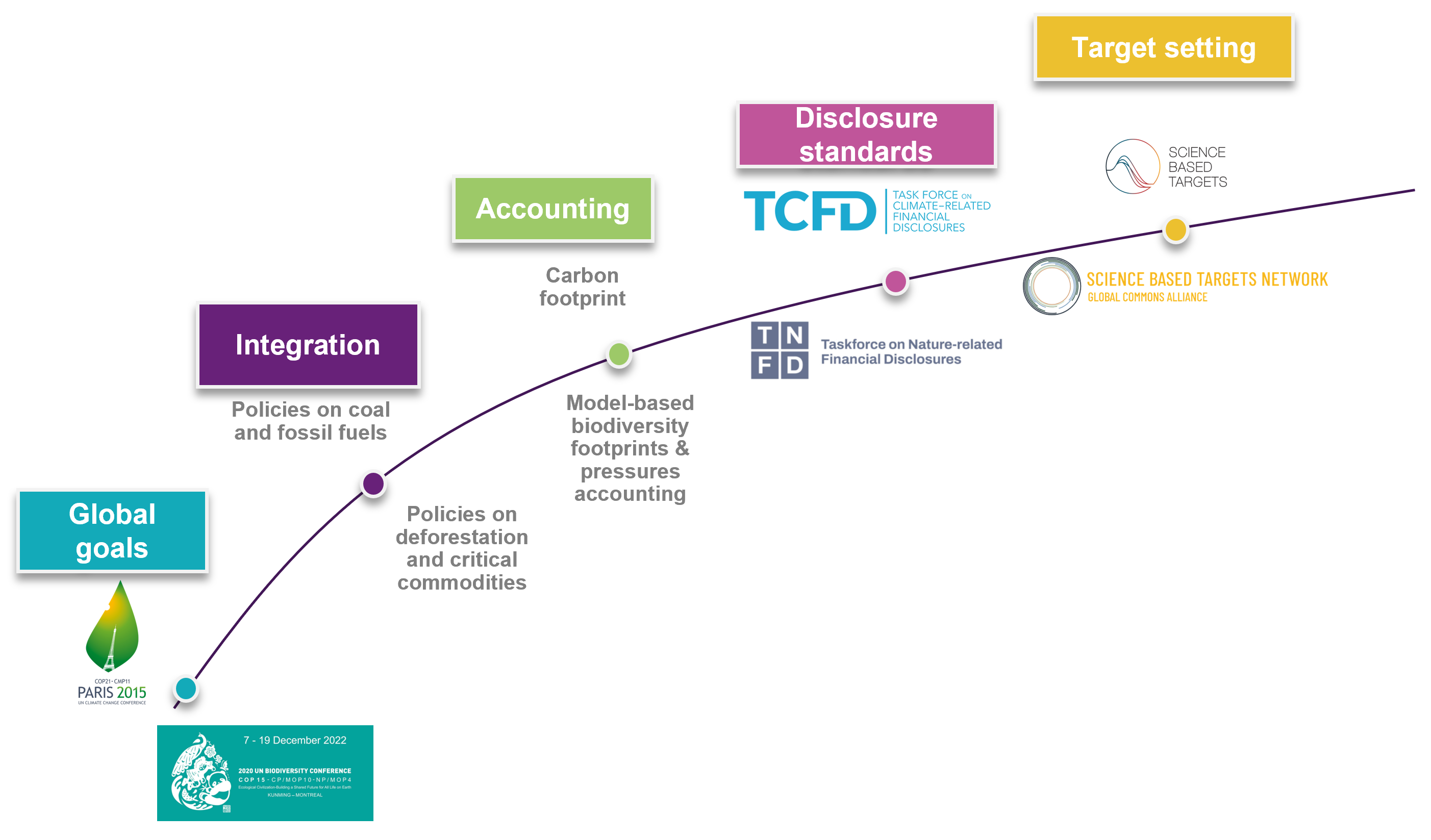

Nature, also called biodiversity, was at the core of the sustainable finance ecosystem discussions in 2023 with COP15 Kunming-Montreal paving the way for a proper integration of the thematic in the economic realm. As the equivalent of the Paris agreement for biodiversity, the momentum provoked by COP15 is mirroring the climate one, only faster. There is a multiplication of standards, regulations and approaches (TNFD, SBTN, ESRS, Taxo 4, NGFS, ECB):

The biodiversity momentum mirroring climate efforts

The year to come will prove instrumental on the thematic uptake by stakeholders, whether it would be for regulators (CSRD, and Taxonomy implementation), corporates with nature-related disclosure or financial institutions’ nature-related stress tests building on NGFS and ECB work. 2024 will certainly witness the real uptake of cross-environmental life cycle analyses and biodiversity footprinting (PBAF). This rise should be perceived among corporates engagements along the year, and financial institutions’ upgraded risks assessments and policies, diving into pressures, dependencies and impacts on nature.

A differentiation between sectors and geographies is urgently expected on that front. A set of agrifood companies are called to demonstrate their engagement in the fight against deforestation as the EU is implementing its law on deforestation-free products and further engage on a reduced exposure to primary ecosystems (Ramsar sites, Key biodiversity areas or other biodiversity rich areas).

COP28 (see our dedicated article here) marked the beginning of a new era including in the financial sector as to how these institutions will finance and accompany the “transition away from fossil fuels”. The matter has been tackled by a growing number of banks with new engagements on fossil fuels including Gas. Banks are urged by civil society to stop financing any new oil fields for which final investment decisions would have been made after December 2021. Beyond asset financing, one key challenge lies in the treatment of firms partially and diminishingly operating in the fossil fuel sectors (divestment, engagement, conditionality), and how lenders and investors handle non-pure players which have begun a diversification.

The “transition away from fossil fuel in energy systems” in “a just, orderly, and equitable manner” raises the question of the appearance of a focus in sustainable finance dedicated to phase outs or phase downs, as well as the related investment and expenditure needs to accompany working capital and workforce shift or support. Sustainable finance might complete its green focus with greater attention on shrinking, decommissioning or repurposing brown activities or making them greener. It calls for a strong inclusion of social factors, employment considerations, true and contextualized transition planning assessments paying heightened attention to the notion of carbon lock in.

In 2023, Asia gave birth to multiple coal managed phase out mechanisms. These mechanisms’ adaptation to other economic activities incompatible with the Paris agreement or the Kunming-Montreal targets - oil & gas, cattle farming, plastics, pesticides - is foreseeable. Managed phased out will be one of our key themes of investigation in 2024.

The intense debate on fossil fuels phase-out percolated into products or labels’ update decisions as the tip of the iceberg regarding standardization and regulation of sustainability claims. 2024 will mark the accentuation of the regulatory trend to define more guidelines, minimum and golden standards as to the characteristics of products entitled to use any green / ESG or sustainability-related term.

The trend is shaping financial regulators intervention in the EU (SFDR potential review, ESMA guidelines on funds names), in the UK (SDR recently released regulation) and in the US (funds names regulation)

In France the SRI label recently excluded investments in companies developing new oil & gas projects. Additionally, a transition plan aligned with the Paris agreement will be required for companies in the sector to be investable. The design, key features and adequacy assessment of transition plans are a topic heavily investigated by market participants, and not thought far enough by policy-makers who however refer to it as a key requirement in many regulations (e.g., EU CSRD, UK SDR, SEC Climate Investor Disclosure, Monetary Authority of Singapore, Hong Kong Stock Exchange, among others). Incidentally, one also expects collective efforts continuation, in terms of skills, data intelligence, regarding the assessment of targets’ ambition. Forward-looking analytics capabilities has become a key differentiator, with growing importance of scenario analysis, not only on climate change but also on nature (reflected by the sophisticated work from NGFS/IMF, etc.).

Those verification, updating and forecasting needs extensively apply to EU taxonomy alignment demonstration. Methodological, legal and marketing framing of alignment claims will absorb market participants and financial watchdogs in 2024. Guidance is looked for on claims, verification, or performance or target updates. The need is two-fold, strengthening the reliability and opposability of taxonomy ratios, data and claims, but also accommodating usability obstacles resulting from the very design of taxonomy criteria.

After fierce criticism against Sustainability-linked bonds (SLBs) in 2022 for the lack of ambitious targets or insufficient use of scope 3 emissions, market pressures and guidance, notably through ICMA’s KPI registry update, lead to practices enhancement, though room for improvement remains. Moreover, the rising number of ‘sleeping SLL” is calling for a certain vigilance, a topic which is identified by the LMA ESG Committee.

Enabling financiers to better spot opportunities through sustainability solutions providers will be key in 2024. So-called avoided and facilitated emissions are areas of intense methodological innovation. Avoided emissions would fall under “scope 4 emissions” to give the deserved climate credit to decarbonization solution providers. Facilitated or underwritten emissions (cf. PCAF new methodology) are GHG emissions that are supported by the issuance of capital market instruments. Methodological work on “advised” emissions, in a context where advisory/consultancy on sustainability is growing in importance, is also explored.

A focus on enabling activities and how to account for the emissions they allow to avoid has recently peaked the attention of a group of financial institutions, incl. Natixis/Mirova to create a common methodology and develop a database of avoided emissions factors and associated company-level avoided emissions on a large firm univers[3]. Such refined carbon accounting would enhance access to sustainable finance to firms whose contribution to the transition is not properly acknowledged, and whose absolute emissions will grow as the total volume of their products or services is to rise dramatically to scale up the transition.

The goal is to award and encourage emission avoidance from solution providers, should it be capital goods, equipment, key inputs or feedstock[4]. Indeed, how come an electric car be an eligible green asset if its core and most critical components are not considered climate change mitigators (namely batteries and its necessary components)? Sustainable finance needs to give due credit to the metals and mining industry, while incentivizing to reduce its non-neglectable negative externalities (water consumption and pollution for instance) and contribute to enhanced transparency. The notion of “enabling activities” and more importantly the assessment of the enabling potential of a technology/activity though deserves further definition and methodological work. This is what the ICMA dedicated taskforce, co-chaired by Natixis CIB, is intending to start with.

Natixis’ Green & Sustainable Hub will keep on investigating these topics further in dedicated papers and accompany the sustainable finance ecosystem through these structural changes.

[1] The Economist (October 7th, 2023), Are free markets history? The rise of homeland economics.

[2] Recent moves of China tightening its grip on the critical minerals sector will impact the price of a vast majority of green technologies needed to achieve the transition.

[3] See “Mirova and Robeco announce I Care and Quantis to develop a global standard for calculating emissions avoided by low-carbon solutions”, available here.

[4] The enabling dimension of industries must be further incorporated into EU’s regulations and market guidance. One regrets that scope 4 was removed from the ESRS of the CSRD (optional DR E1-14 – avoided GHG emissions from products and services). Avoided emissions play a key role, see “Mirova & Robeco lead initiative to develop global database of avoided emissions factors and associated company-level avoided emissions”, available here.