COP 28 UAE Main Takeaways

Collective progress made but still far from 1.5°C

The first global stocktake (a five-year global review of progress against the goals of the Paris Agreement) acknowledges significant collective progress from an expected global temperature increase of 4°C according to some projections prior to the adoption of the Agreement to an increase in the range of 2.1–2.8°C with the full implementation of the latest nationally determined contributions (NDC)

The COP “notes with concern” that implementation of current NDCs would solely reduce emissions on average by 2% by 2030 (compared with 2019 levels) when limiting global warming to 1.5°C (with no or limited overshoot) requires a CO2 emission reduction of 43% by 2030 and 60% by 2035.

That decarbonization pace seems clearly out of reach unless drastic action is taken by the different parties.

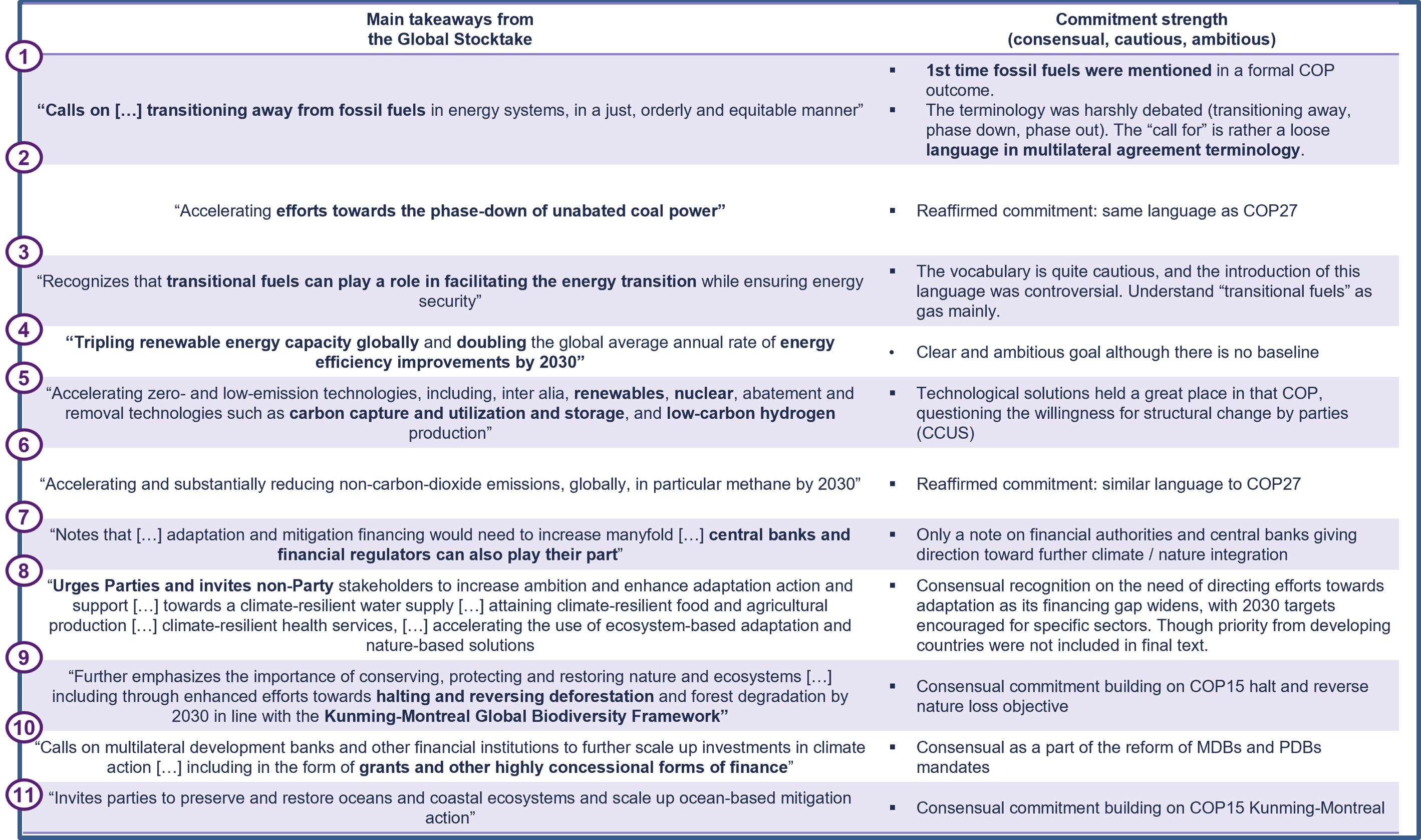

Although historical language has made headlines – transitioning away from fossil fuels, in a just, orderly and equitable manner –, the lack of clear pathway (incl. deadline and intermediary milestones) for fossil fuel phase out diminishes its scope. The text accommodates the use of fossil fuels beyond energy use, and the continued use of gas for power generation as a transition fuel.

Nonetheless, clear objectives were set with concrete implications for clients and sectoral orientations:

- Tripling renewable energy by 2030;

- Doubling the global average annual rate of energy efficiency improvements by 2030;

- Accelerating efforts towards the phase-down of unabated coal power;

- Accelerating zero- and low-emission technologies (renewables, nuclear, hydrogen, CCUS), nuclear being mentioned for the first time;

- Establishment of a loss and damage fund. Although a considerable win after decades of demand by the global south, only $700mm pledged by wealthy nations falls far short of the estimated annual cost of damage (est. between $100bn-$580bn)

Agreements were found on the sidelines of the COP (non-exhaustive):

13 countries designed a global climate finance framework as part of the “UAE leaders declaration on a global climate finance framework” in which they reaffirm the willingness to deliver high-integrity carbon markets, recognizes the role of sustainability-linked bonds, debt-for-climate swaps and other incentivizing instruments in delivering more ambitious action at country level among other mechanisms such as concessional finance, public-private partnerships, hybrid capital. Moreover, one of the declaration’s priorities is “building better, bigger and more effective MDBs”, highlighting a growing area of concern in the international arena and the final stocktake agreement at COP28 calling for MDB reform to scale up investments in climate action.

The UAE have launched a $30bn catalytic climate vehicle, ALTERRA - which will become the world's largest private investment vehicle for climate change action and will aim to mobilize $250bn globally by 2030 - mainly focused on EM and developing economies.

The announcement of the net zero nuclear industry pledge regrouping 20 countries including France set the objective to triple nuclear energy capacity from 2020 to 2050.

Declaration on sustainable agriculture, resilient food systems, and climate action signed by 159 countries to work collectively towards more resilient and productive sustainable agricultural systems

A COP that did not look like any other before on some aspects:

- It is the first COP where the finance sector is front and center: the COP of Finance ministers more than Climate change ministers

- Highly focused on transition finance with a true quest for a differentiated transition finance definition according to developed vs emerging markets realities, while necessary bearing the risks of loosing perspective. Just transition presented as a safeguard for sustainable development and the necessary buy-in for rapid climate action with strong role for capital markets to finance the just transition.

- Rise of the resilience on the agenda of all parties with quite a number of adaptation-oriented investments.

- Incredible, and unexpected momentum on Carbon markets considered by many as a substantial part of the solution, but also highlighting all of its shortcomings to address and global standards to strengthen.

- A strong voice given to the oil & gas players and their transition avenues with quite some focus of the Presidency on methane abatement technologies and financing schemes.

- Blended finance at the forefront (e.g. Green Climate Fund record funding level reached, Green Coalition for the Amazon) and the need to capitalize multilaterals differently to decouple their impact.

- Trade policy / Export credit guaranties (see Net Zero Export Credit Agencies Alliance) as a key trigger for transition

- Low carbon Steel & Green Hydrogen had also incredible momentum in the discussions / commitments & initiatives

Summary of the main outcomes

Positive outcomes at COP, but substantial action needed

- To achieve the stocktake objectives countries will need to increase the ambition of their NDCs. These are due in 2025, with contributions up to 2035. The stocktake once again makes a clear call for countries to reflect the highest ambition possible (considering “common but differentiated responsibilities and respective capabilities”). Countries are expected to begin working on their NDCs during this year and a series of global and regional workshops will be held to support them in this process.

- COP28 launched the Road Map to Mission 1.5°C to keep the Paris goal of limiting global temperature alive. The Road map aims to strengthen international cooperation and the ambition of the NDCs to be submitted in 2025.

Unsettled topics to be tackled up to Baku (non-exhaustive)

- Loss and Damage Fund: while the fund was operationalized, with a USD792m contribution from developed nations, there are still pending institutional arrangements on how resources will be disbursed. The World Bank to initially host the fund.

- Global Goal on Adaptation: the global stocktake recognizes time-bound targets for specific sectors but further work is needed to set a clear roadmap to address the adaptation finance gap.

- New Collective Quantitative Goal: new climate finance goal that replaces the 2009 $100bn annual commitment from developed countries. Discussions in Dubai focused on the process of setting a new goal, rather than the timeline, sources and structure leaving those elements to the next negotiations. Three technical expert dialogues will be held throughout the year to address the NCQG elements in preparation to COP 29, in Azerbaijan, on the 11-24 November 2024.

- Carbon Markets: no decisions were made on the rules for carbon markets, which should be addressed at COP29. Countries are yet to agree on the process of authorizing emission transfers, reviewing confidential information and correcting inconsistency in country reports, the scope and definition of “cooperative approaches” (carbon trading to meet their NDCs), and eligible activities to be included under article 6.

A roadmap for action

- The first Global Stocktake provides a blueprint on what action is needed to limit global warming to 1.5°C: move away from fossil fuel, triple renewable energy, double energy efficiency improvements, accelerate zero and low-emission technologies, deliver climate-resilient water supply and agrifood production, restore and protect nature, among others. There are opportunities to transform these pledges into real-economy outcomes, with an important role for private sector to drive change.