Financing green hydrogen’s development

5-minute read

In a general context marked by heightened awareness of climate challenges [1], the hydrogen sector has seen a sharp acceleration in its development over the past 12 months. This is perceptible through the multiplication of hydrogen-centric projects at the crossroads of the energy, industrial and mobility sectors, also in the ramp-up of government support to the sector.

In Europe, which is in the midst of an unprecedented health and economic crisis, the last six months have been marked, at both the level of the European Union and the Member States, by the announcement of huge economic stimulus plans featuring ambitious measures to promote hydrogen, focused on:

- The development of hydrogen production capacities, chiefly “green” hydrogen (i.e. produced using water electrolysis powered by electricity from renewable or nuclear energy sources, a nascent process in the same way as “blue” hydrogen [2], being developed in response to the climate externalities associated with the production of “grey” hydrogen which still accounts for more than 95% of hydrogen volumes produced worldwide).

- The development of hydrogen end-uses across the industrial (refining, manufacturing of such products as ammonia and steel) and mobility sectors (buses, trucks and other commercial or utility vehicles).

These recent developments suggest hydrogen in its green form is now perceived as a central solution for the decarbonization of entire swathes of industry and mobility. However, the production of green hydrogen and the various downstream uses of the molecule in industry and mobility are still at early stage and remain plagued by a lack of cost-competitiveness vis-à-vis established, fossil fuel-centric technologies and processes.

By 2030, some $300bn is to be invested in the entire sector, not just to deploy what remains an embryonic value chain, but also to achieve economies of scale to bring down costs right across this chain, from hydrogen’s production to its various end-uses. Only part of the $300bn will be financed by the public sector, with $70bn committed by national governments to date, which underscores the extent of the challenge facing the sector.... and private finance.

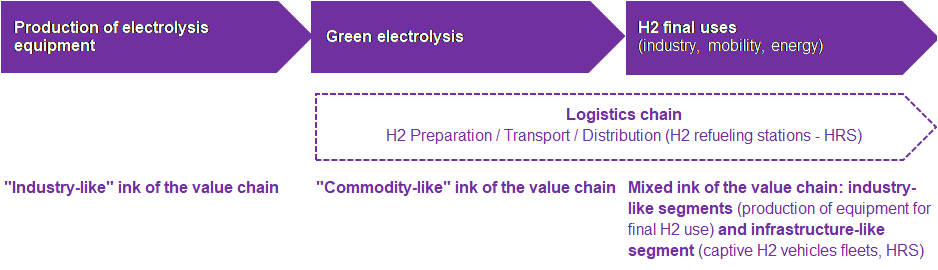

Far from being a homogeneous whole, the hydrogen sector, more particularly green hydrogen, amounts to a vast value chain at the crossroads of three sectors (industry, mobility and energy), bringing together three large business lines (manufacturing of upstream and downstream equipment., green hydrogen production and infrastructures for hydrogen end-uses), each with its own challenges and a specific risk profile.

Graph 1. Green hydrogen value chain: business profile of different segments

Source: Natixis

For potential providers of private capital (debt, equity), the analysis of these segments making up the value chain reveals two major groups of players:

- The players in the industrial businesses of upstream and downstream equipment production operate in an already global market. The equipment they produce not only compete with equipment based on the use of fossil fuels but also with alternative low-carbon technologies / processes (case of battery electric vehicles in the mobility sector). For these players, in particular for the niche players such as French electrolyser and hydrogen refueling stations specialist McPhy and Norwegian peer Nel, the current stage of take-off in the sector is inducing negative cash flow. For this reason, these players are likely to predominantly use the equity market to finance their development, in particular the industrialization of their activity through the development of real assembly lines for the equipment they offer.

- The operators of electrolysers and equipment / assets of the molecule allowing collective uses of the molecule (public buses, household waste collection truck, refueling stations deployed to supply these vehicles) operate in markets for the moment structured around bilateral contractual relations (case of green hydrogen produced for industrial buyers) or the provision of public services (case of the molecule produced to power public buses or waste collection trucks). In both cases, the contractual frameworks underlying the development of electrolysis capacities allow the cost of hydrogen to be passed on to the end user whether he is an industrial off-taker agreeing to pay a premium to decarbonize his activity or the end user of local public services.

These elements highlight the twofold challenge the financial sector confronts at this early stage of green hydrogen sector’s take-off, namely:

- Develop instruments with features adapted to the challenges and risk levels of the assets/entities financed across the value chain

- Replicate wherever possible across this chain the most cost-effective financing mechanisms already massively deployed in other sectors of activity, taking advantage of both nascent business models and public support mechanisms.

In this respect, the recent example provided by the deployment of renewable energies offers a good illustration of the role as a trigger played by private finance (through asset-based lending) in shaping an industry that was technologically immature at the onset, but in receipt of public support aid in various forms.

For green hydrogen, it is largely the public authorities that will provide the levers for private finance’s increasing involvement in the sector’s coming of age: development at the initiative of local authorities of territorial hubs concentrating hydrogen end-uses in mobility and industry, start made introducing feed-in-premia to electrolysers, direct and indirect support mechanisms to stimulate demand for green hydrogen in the industrial and mobility sectors. In the EU, the expected strengthening of the Emissions Trading Scheme (ETS) for industrial sectors already covered (refining, production of steel and chemicals, etc.) and its expansion to other sectors (road transportation) may ultimately act a key lever to bridge the cost gap between green hydrogen centric equipment and processes, on the one hand, and their fossil fuel centric competitors, on the other hand.

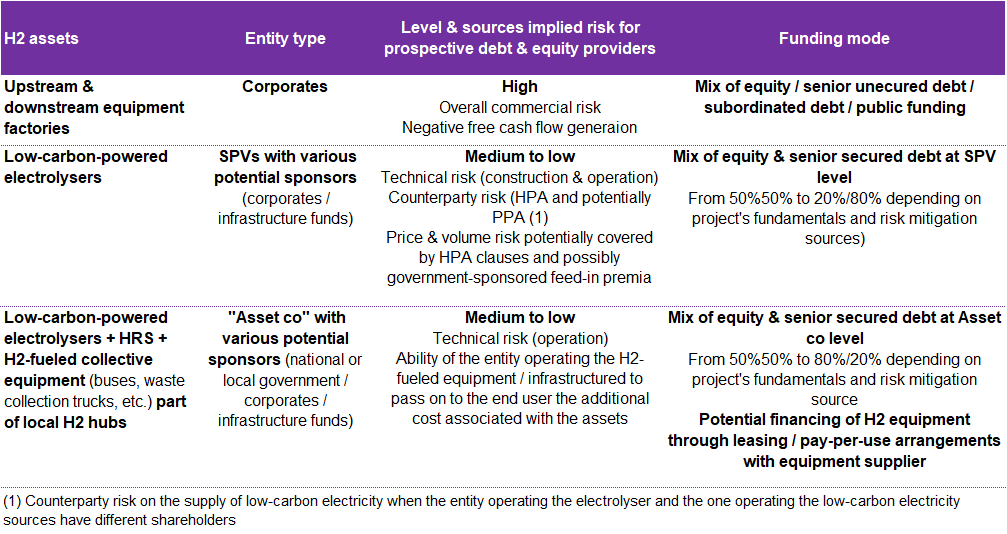

Still nascent, these mechanisms could, in time and under certain conditions, support the deployment within the hydrogen sector of financing based on the credit quality of the very assets being financed: secured senior debt instruments for green electrolysis and hydrogen-centric ecosystems, spurred by public initiatives (territorial hubs and national, even international infrastructures, including airports), lease/pay-per-use financing for hydrogen-powered equipment provided by the suppliers, ultimately by commercial banks. Along with the mobilization of equity markets by specialized equipment manufacturers and of senior unsecured debt by early projects sponsors, one could see the systematization of senior secured financing whenever possible for green electrolysis and hydrogen-centric equipment for public services.

Table 1. Typology of possible financing schemes along the green hydrogen value chain

Source: Natixis

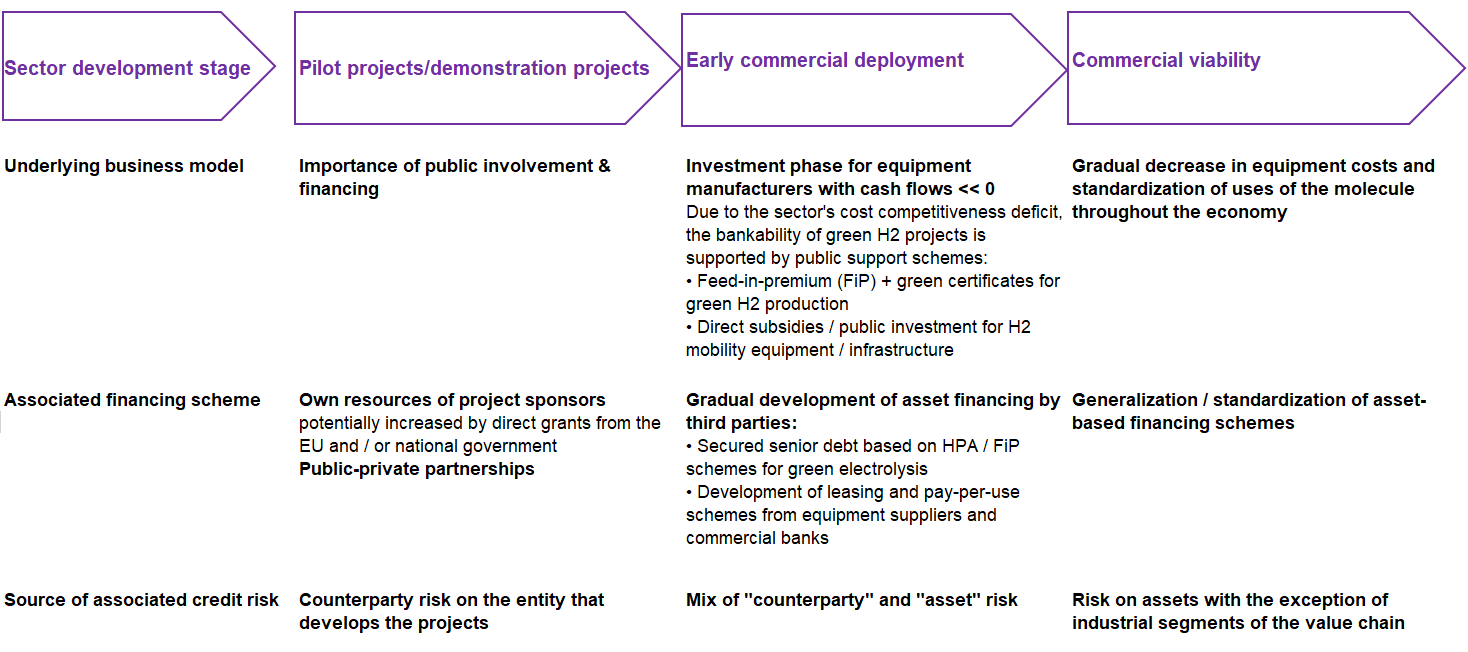

All in all, this gradual mobilization of private finance can be expected to both spur and follow the sector’s maturing, with two crucial watersheds:

- Transition from pilot projects to a commercial scale deployment of equipment. It is precisely this phase that has been ushered in by the ramping-up of public support, with the intervention of public authorities taking on a more “systemic” form: development of territorial hubs, start of direct support to low-carbon electrolysis on the part of governments, concurrently with the implementation of mechanisms to support demand for green hydrogen in the most challenging sectors to decarbonize (i.e. industry, mobility).

- Gradual attainment of commercial viability across the different segments of the value chain through a multiplication of projects, a steady increase in demand, the industrialization of the equipment production platforms and, ultimately, the generation of economies of scale to bring down costs throughout the green hydrogen sector.

From the standpoint of private capital providers, the coming of age of the green hydrogen value chain will offer possibilities for an increasingly greater involvement:

- At the onset, directly, in the form of equity financing needed by specialist equipment manufacturers for their development, or indirectly, in the form of unsecured senior debt issued by the sponsors of the first projects and by full-line equipment manufacturers with ambitions in the sector.

- Then gradually, in the form of asset-based financing: secured senior debt for green hydrogen electrolysis and the ecosystems built around hydrogen, supported by public initiatives (territorial hubs, national, even international infrastructures, including airports), lease/pay-per-use financing for hydrogen powered equipment provided by the suppliers, ultimately by commercial banks.

- In time, once the standardization of asset-based financing has been completed, in the form of a possible securitization by the banks of the various credit instruments to institutional investors (insurers, fund managers). Already observed in the renewable energies sector, this evolution will accelerate the development of the green hydrogen sector by lightening the balance sheet of the banks, allowing them to fund new projects/assets.

Table 2. Green hydrogen sector: the path to the sector’s maturity and financing mechanisms

Source: Natixis

[1] Three recent political developments illustrate the growing awareness of the challenges presented by climate change at the level of OPEC+ countries: the decision of the United States to rejoin the Paris Agreement following Joe Biden’s election (January 2021); the announcement by China that it aims to achieve carbon neutrality by 2060 (September 2020); the European Union’s decision to revise upwards its intermediate target, which is now to reduce greenhouse gas emissions not by 40% but by 55% below their 1990 level by 2030 (December 2020).

[2] As for grey hydrogen, the production of blue hydrogen relies on steam methane reforming (SMR) using coal or natural gas as a feedstock, which is highly carbon intensive. In the case of blue hydrogen, scope 1 emissions associated with SMR are mitigated through the use of carbon capture and sequestration processes (CCS).