Asset Owners sharpen the implementation of their Net-Zero Carbon investment strategies

5-minute read

With the publication of its “Draft 2025 Target Setting Protocol”, the Net Zero Asset Owners Alliance (NZAOA) provides a useful tool in the journey to fulfill its members’ commitment to transition their portfolios to net-zero emissions by 2050.

Launched in early 2019, the NZAOA gathers 33 asset owners (representing ~USD 5trn in assets), which include Allianz, Swiss Re, CalPERS, Scor or Axa. More than a year after its creation, the alliance announced in October 2020 that its members had collectively agreed to set quantitative portfolio decarbonization targets for the next five years with the aim of having transparent and unique targets setting processes.

Published for public consultation, the 2025 Target Setting Protocol sets out the Alliance’s approach towards this target setting and reporting exercise for the period 2020-2025. It details an approach in four parts, that should be viewed in conjunction with one another:

- Portfolio targets: members should set carbon reduction targets both on Scope 1 and 2 emissions for their underlying holdings and on Scope 3 of underlying holdings for ‘priority sectors’ (Oil and Gas, Utilities, Steel, Aviation, Shipping and heavy and light duty road transport). Based on an assessment of the Intergovernmental Panel on Climate Change (IPCC) 5°C scenario, the NZAOA has estimated that targets for carbon emission reductions should range between -16% and -29% for the period 2020–2025. The protocol covers 3 asset classes: corporate equity, corporate debt and real estate portfolios.

- Sectors targets: definition of an average carbon reduction pathway for key high emitting sectors (e.g. Energy, Transport, Steel)

- Engagement targets: Alliance members are encouraged to perform engagement activities that contribute to achieving net-zero commitments (individually or through the Alliance or other collective initiatives). The protocol identifies engagement key performance indicators (KPI) that the Alliance members can select from to elaborate on these engagement activities that can take different forms, including for example corporate engagement with a company, notably in the framework of the CA100+[1] initiative or the publication of position papers on an issue or sector, etc. The emphasis given to engagement justifies the intention of the NZAOA to partner with the Climate Action 100+.

- Financing transition targets: to increase investments in climate solutions. The protocol states that targets may concern the share of revenue from green activities, the invested value in climate solutions investments or the associated avoided emissions.

With this protocol, emphasis is especially put on engagement with the high-emitting industries and investment into climate solutions. What is worth remarking, however, is the absence of any mention of the EU mandated Technical Expert Group’s (TEG) who proposed climate benchmarks i.e. the EU Paris-aligned benchmark (PAB) and EU Climate transition benchmark (CBT) (see our publication), which could be additional interesting tools to support the NZAOA’s commitment. The main objectives of these new climate benchmarks were to provide investors with comparability, alignment tools, transparency and to disincentivize greenwashing. Reasons for this absence could be many - the euro-centric nature of these benchmarks, and the lack of maturity of the market, most funds being tied to passive investments in ETF, etc.

NZAOA’s announcement intervenes just a few months after the Paris Aligned Investment Initiative (PAII)[2] and the Climate Action 100+ unveiled new frameworks to help members of their own coalition in aligning their portfolios to net zero carbon goals (see our September article). Beyond collective engagement, a growing number of institutional investors are making explicit mentions to alignment with temperature trajectories. Some are even going further than the NZAOA by initiating independent works to analyse the degree of alignment, or non-alignment, of their portfolios with low-carbon trajectories and by setting temperature-related targets.

At this stage, the NZAOA states in its protocol that it is too early to set temperature-related targets, since temperature alignment methodologies are still evolving with no global recognized standard. This is the reason why it currently favors portfolio emissions reduction targets and has launched in April 2020 a call for convergence on the temperature alignment methodologies. (see our April 2020 article).

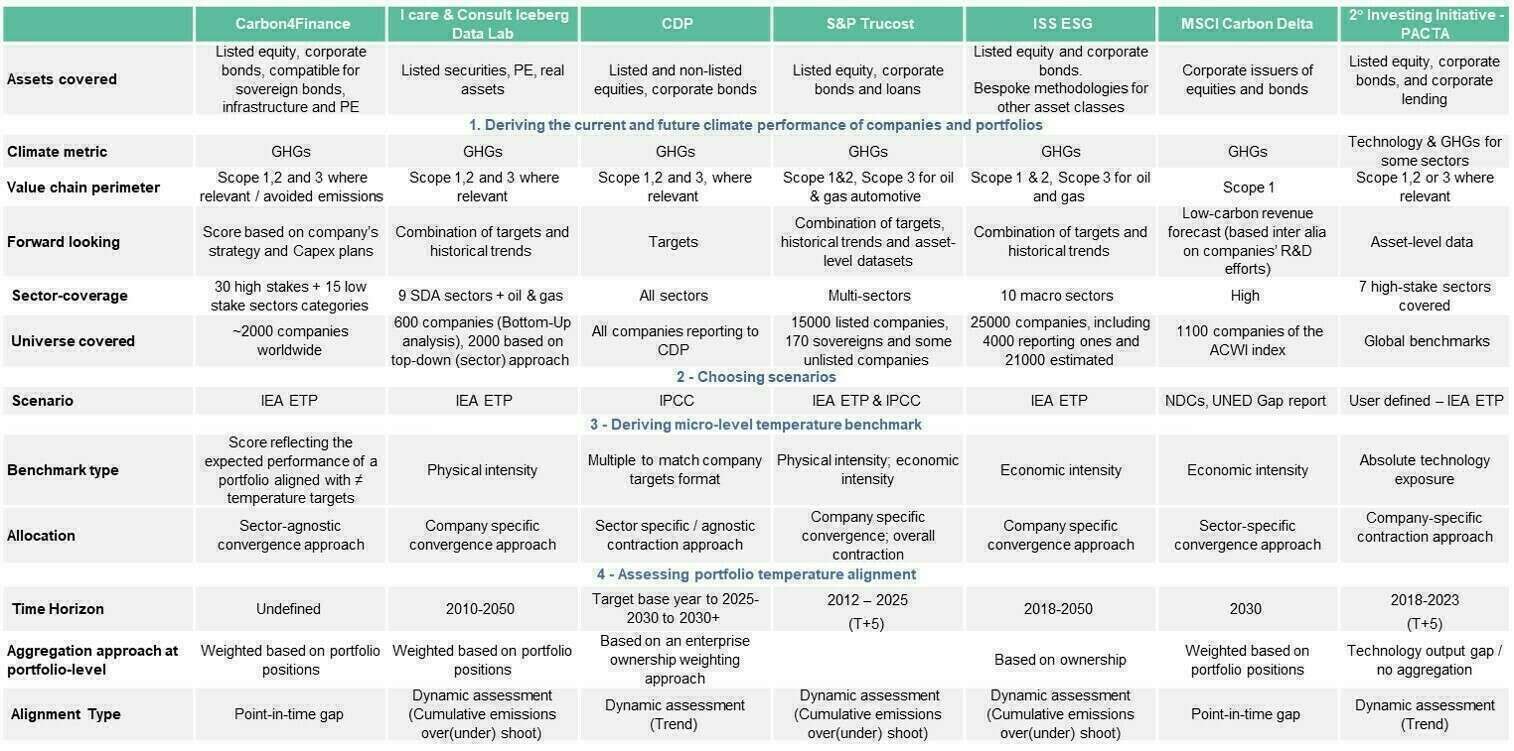

Finding its way between the different temperature alignment methodologies represents indeed the first challenge for investors that want to understand the compatibility of an investment portfolio with a trajectory limiting a temperature rise under a specific level. The publication of ‘The Alignment Cookbook: A technical review of methodologies assessing a portfolio’s alignment with low-carbon trajectories or temperature goal’ by Louis Bachelier Institute in July 2020 provides a valuable review of these different portfolio temperature alignment methodologies and helps to better navigate between them. In this report, the think tank describes four broad steps as a general ‘recipe’ that all portfolio temperature alignment assessments follow, with each step offering different options that an investor must understand to select the methodology that best fits its needs.

STEP 1: Measuring the climate performance of portfolio companies

The aim here is to choose the most relevant metrics to capture the portfolio’s companies’ climate performance. Variables to be considered include:

- Metric: GHG (relative emission evolution; carbon intensity; carbon budget in absolute); Technology mix.

- Value-chain perimeter: Scope 1; Scope 1 & 2; Scope 1, 2 & 3; “Relevant Scope”.

- Forward-looking data: extrapolation based on track record, targets, or asset-level / capex / plant shut down databases

- Type of measurement: Technology breakdown (share of green technology); Carbon intensity (output/monetary); Absolute emissions (tCO2e), induced / avoided emissions.

STEP 2: Selecting scenario(s) from which trajectories are derived

The aim here is to choose a “scenario” which determines a specific carbon budget and shapes pathways against which a portfolio’s alignment would be measured. Variables to be considered include:

- Scenarios: What (conceptual/ practical considerations)?; how many (one/ several) ?

- Adoption of third-party derived pathways: Additional sectors; restatements; geographical breakdowns.

Note that while in theory the choice of the scenario depends on conceptual considerations, users are usually limited by practical considerations, in particular sectoral granularity.

STEP 3: Converting macro-decarbonization pathways to micro-actors ‘benchmarks

The aim here is to distribute the chosen trajectory amongst micro actors for individual target-setting and temperature benchmarks. Variables to be considered include:

- Expression of the benchmark: absolute GHG emissions, energy efficiency, carbon or energy intensity metrics.

- Allocation of the benchmark: additional sectors; restatements; geographical breakdowns.

- Repartition of the carbon reduction burden (homogeneous – contraction method / based on homogeneous target – convergence method)

STEP 4: Comparing portfolio climate performance with the benchmark to assess the portfolio temperature alignment

The aim here is to finally assess the (mis)alignment of a portfolio using the benchmarks chosen in Step 3. Variables to be considered include:

- Measurement of spread v/s speed: Static/ dynamic, trend/ gap/ cumulated gap.

- Expression of results: Binary, score, percentage, temperature.

- Adjustments: Sectoral constraints, sector weights, bounding.

- Appropriation and aggregation: ownership or portfolio weights.

The methodological choices made on these four steps can give rise to numerous permutations that explain the variations between the existing methodologies. Based on Louis Bachelier’s report and on our own analysis, we reviewed 7 methodologies available to investors, whose main differences are described in the table below. These 7 methodologies are particularly suited for listed equities and corporate bonds. Yet, methodologies covering other asset classes exist, such as the Beyond Ratings methodology for sovereign portfolios.

If to date the lack of consistency between these temperature alignment methods has prevented some investors to use them, there is a growing acknowledgement of the large potential they offer to support the increasing number of financial institutions that have since the Paris Agreement made commitments to align their portfolio with temperature trajectories, most often a 2°c scenario.

Table 1 – analysis of various methodologies available to investors

[1] Launched in December 2017, the Climate Action 100+ gathers investors (collectively managing ~ 47 trillion dollars in assets), that have committed to engage with the world’s largest corporate greenhouse gas emitters to improve their climate performance -available here.

[2] Launched in May 2019, the PAII is a working group of more than 70 investors (managing 16 trillion dollars in assets) led by the Institutional Investors Group on Climate Change (IIGCC), that looks at how investors can align their portfolios to the goals of the Paris Agreement.