EBA’s newly released transition plan guidelines

Introduction

Amid ongoing uncertainty surrounding the simplification of EU ESG regulations – including transition plan disclosure and implementation in CSRD and CSDDD – the European Banking Authority (EBA) released its final “Guidelines on the Management of Environmental, Social and Governance (ESG) Risks” on the 8th of January 2025.

Under CRD VI, banks must draw up transition plans to address and manage ESG risks. The EBA Guidelines provides implementation orientations and precises the related scope of information that the ECB will request from EU banks. The ECB indeed enforces rules set by the EBA and has been given powers to assess banks’ transition plans and ESG risks. The information will not be made publicly available unless banks choose to do so.

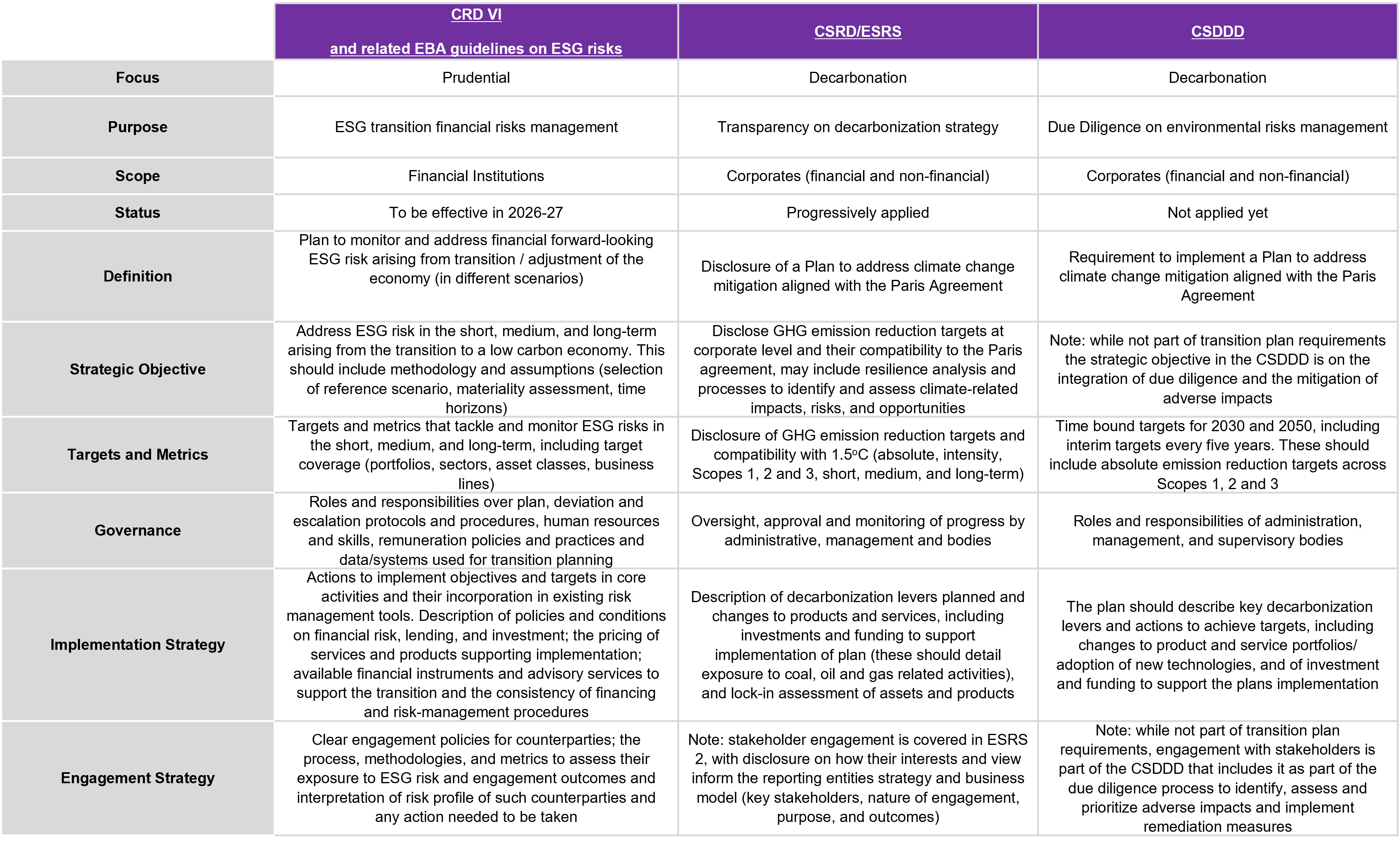

As a prudential transition plan, the CRD / EBA transition plan differs from the decarbonization transition plans integrated into CSRD and CSDDD (for a comparison, see table n°1 infra). Rather than disclosing information on or requiring alignment to climate objectives and dedicated transition pathways, the EBA Guidelines details how financial institutions should articulate their preparedness to respond and mitigate material ESG risks that could affect them. These guidelines request so whether those risks materialize in a context of a “smooth and orderly transition” or a disordered or more chaotic one.

The CRD / EBA prudential transition plan does not require financial institutions to exit or divest from carbon-intensive sectors, its focus relates to ESG risks management at financial institution level to preserve financial stability.

However, the EBA emphasizes that financial institutions’ prudential plans should be “coherent and consistent” with transition plans requirements under other pieces of EU legislation, such as the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD) approach, and all relevant aspects of internal management (business strategy, risk management, due diligence and sustainability reporting). Notably, CSRD and CSDDD include requirements for the disclosure and adoption, respectively, of plans to ensure the compatibility of business models of undertakings with the limiting of global warming to 1.5°C and the objective of the EU to achieve climate neutrality by 2050. The EBA guidelines emphasizes that institutions will need to develop a single, comprehensive strategic planning process that covers all regulatory requirements stemming from applicable existing regulatory frameworks.

The guidelines provide an outline for the core content that should be included in transition plans (see in appendix infra). Reading the headlines may evoke a sense of déjà vu as it builds on the foundational elements of transition plans set forth initially by the Taskforce of Climate-Related Disclosures (TCFD) and more recent voluntary and regulatory frameworks that reference transition and physical risk as part of transition planning.

The guidelines outline how institutions must develop internal processes and ESG risks management frameworks. They will apply to European financial institutions from 11January 2026 and to small and non-complex institutions on 11 January 2027. Institutions are required to follow the guidelines, under the supervision of the ECB: the CRD and CRR regime evolutions validated in 2024 empower supervisory authorities to incorporate ESG risks in their supervisory review and evaluation processes, as well as in authorities’ stress testing.

For the entities directly supervised by the ECB, the administrative penalties for non-compliance are directly defined by EU Regulations[1]. If the ECB estimates that a bank is not meeting its prudential requirements, if may impose several actions ranging from compelling the bank to hold more own funds to request the bank to present a plan to restore compliance, or to impose administrative fines. If a clear breach of a requirement has occurred, the ECB may impose administrative fines. These may be “up to twice the amount of the profits gained or losses avoided because of the breach (where those can be determined), or up to 10 percent of the total annual turnover” of the bank in the preceding business year, or other financial penalties in relevant Union law (article 18(1) of Council Regulation 1024/2013).

The variety of requirements across regulatory frameworks can be intimidating, but detailed comparison shows common elements and reinforces the need for consistency as set forward by the EBA. It will require updates to reflect upcoming regulatory development under the Omnibus as it references specific CSRD elements in its transition plan toolkit. The EBA is preparing complementary guidelines for ESG Scenario Analysis, currently in public consultation (ends on 16 April 2025).

Table 1. Transition Plan Requirements in EU Regulatory Frameworks

Source: Natixis GSH based on EBA's report