CSRD, where are we at?

Last June the European Parliament and Council agreed on a final text [1] for the corporate sustainability reporting directive (CSRD), that will update the 2014 Non-Financial Reporting Directive. With the definition of binding European Sustainability Reporting Standards (ESRS) and the extension of the scope of affected companies (enlarged from about 11 000 to 57 000 reporting entities), and new auditing obligations, the CSRD will put sustainability reporting at the same level as financial reporting. The EFRAG is tasked with the challenge to define a first set of sector-agnostic sustainability standards by mid-November 2022, so as to enable the EU Commission to introduce them in EU regulation by June 2023. This is a first challenging milestone and a crucial stake for companies and investors in a context of international competition to define global ESG disclosure standards and guidelines.

Contents

I - The context : from NFRD to CSRD

1 - Why the CSRD?

2 - What are the main changes brought by the CSRD?

II - How will the new European sustainability Reporting Standards for companies be constructed?

1 - Who will define the new mandatory European Sustainability Reporting Standards (ESRSs)?

2 - What is the content and adoption timeline of the ESRS?

3 - What will the ESRS require from corporates and bring to investors? What the ESRS are, what they are not

I - The context: from NFRD to CSRD

1 - Why the CSRD?

The “Corporate Sustainability Reporting Directive” (CSRD) is not a new directive as such: it is the result of a review of the previous directive of 2014, the “Non-Financial Reporting Directive”, which, in the wake of the 2008 financial crisis, laid down the principle of reporting sustainability information on an annual basis for certain large companies .

As it is a directive and not a regulation, the transparency principles set out in the NFRD remained broad and required transposition into national law by the Member States. The 2014 directive established the principle of sustainability reporting by large companies throughout the EU and the principle of double materiality (companies have to report about how sustainability issues affect their business, but also about their own impact on people and the environment). However, the heterogeneous transposition by Member States, the very general and non-binding nature of the reporting principles and guidelines, and the evolution of the new sustainable finance reporting obligations of Financial Market Participants (taxonomy, SFDR), quickly revealed that the information reported by companies was not sufficient.

The European Commission has pointed out the following problems of quality and exhaustiveness in the information reported:

- Reports often omit information that investors and other stakeholders think is important.

- Reported information can be hard to compare from company to company,

- Users of the information are often unsure whether they can trust it.

- With knock-on effects, in a context where investors, increasingly interested in sustainability issues, require on the one hand a reliable overview of sustainability-related risks to which companies are exposed and their sustainability impact on the environment, and on the other hand information to meet their own transparency obligations under the SFDR (Sustainable Finance Disclosure Regulation).

As a result of its Communication on the European Green Deal, the Commission committed to review the NFRD in 2020 as part of the strategy to strengthen the foundations for sustainable investment. On 21 April 2021, the European Commission adopted a package of measures, which includes a proposal for a Corporate Sustainability Reporting Directive (CSRD).

2 - What are the main changes brought by the CSRD?

Three main changes to be taken into account

– to extend the scope of the reporting requirements to additional companies, including all large companies and listed companies (except listed micro-companies);

– to require assurance of sustainability information;

– to specify in more detail the information that companies should report, and require them to report in line with mandatory EU sustainability reporting standards; these requirements will also enable Financial Market Participants to comply with their own reporting obligations under SFDR.

Table 1- Main changes between NFRD and CSRD

|

|

NFRD |

CSRD |

|

Entry into force |

December 2014 |

20 days after publication in the OJEU (end 2022 probably) |

|

Scope of reporting entities and first reporting year |

Large companies which are “public interest entities” : listed companies, banks and insurance companies, with more than 500 employees (yearly average)

Subsidiary exemption possible [2] |

NFRD scope:

+ Enlarged CSDR scope:

Non-EU companies with branches or subsidiaries in the EU above certain thresholds (more than EUR 150 million turnover in the EU)

Subsidiary exemptions remains but:

|

|

First year of reporting |

First reporting as of 2018 on information relating to the 2017 fiscal year |

|

|

Estimated number of reporting entities by the EU Commission |

About 11 000 |

About 57 000 |

|

Type of reporting |

Large principles on disclosure related to:

|

Information to be reported through standardized disclosure requirements (European Sustainability Reporting Standards) on:

|

|

Implementation guidance |

Guidance documentation:

|

Mandatory European Sustainability Reporting Standards:

|

|

Location of information |

At discretion |

Dedicated section of the management report |

|

Verification of information |

statutory auditors and firms should only check that the non-financial statement or the separate report has been provided |

Audit (assurance) of reported information requirement, starting with limited, later reasonable |

Source: Natixis

II - How will the new European sustainability Reporting Standards for companies be constructed?

1 - Who will define the new mandatory European Sustainability Reporting Standards (ESRSs)?

The role of EFRAG: defining the draft ESRS

The European Financial Reporting Advisory Group (EFRAG) [5] has been mandated by the EU Commission for developing these draft standards.

The role of the Commission: translating them into EU law

The Commission, on the basis of the EFRAG proposal, will draft its own proposal in the form of a delegated act. Before adopting any standards, the Commission will consult the Member States Expert Group on Sustainable Finance and seek the opinion of the European Supervisory Authorities (ESAs) [6], and other topical specialized organisations [7]. These consultations will help to ensure a broad consensus on the content of the standards, and coherence with relevant EU legislation and policies.

2 - What is the content and adoption timeline of the ESRS?

2022-2023 - Set 1: the sector-agnostic ESRS

On 29 April 2022, EFRAG published 14 ESRS Executive Drafts for public consultation and consulted until August 2022 on them. On the basis of the results of the public consultation, EFRAG is adapting its proposal and should deliver by mid-November 2022 its recommendation on “sector-agnostic” standards, so that the content of Set 1 can be adopted by the EC by 30 June 2023.

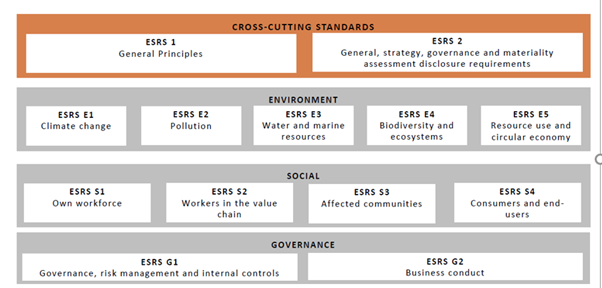

Table 2- The ESRS executive draft architecture

Source: EFRAG

Cross-cutting standards - ESRS 1 and 2

The cross-cutting standards (ESRS 1 and 2) address general disclosures requirements on matters that are crucial to the relationship between sustainability issues and the company. ESRS 1 describes precisely the principles to be followed in order to provide adequate disclosure (how to disclose a policy, a target, a performance measurement for instance). ESRS 2 contains disclosure requirements on company’s strategy and business model, its governance and organization, and its materiality assessment. Following the concept of double materiality, companies have to identify their material sustainability-related impacts as well as risks and opportunities.

Topical standards – E, S and G

The topical standards cover a specific sustainability E, S or G topic or subtopic (see the chart below). They set disclosure requirements related to sustainability impacts, risks and opportunities (IROs), regardless of the sectors they operate in. Such disclosure requirements are complementary to those prescribed in the cross-cutting standards and require information on:

• the policies, targets, actions and action plans, resources (PTAPRs) adopted by the entity on a given sustainability topic or subtopic,

• corresponding performance measurement metrics.

Each ESRS provides also additional details in annex with application guidance elements.

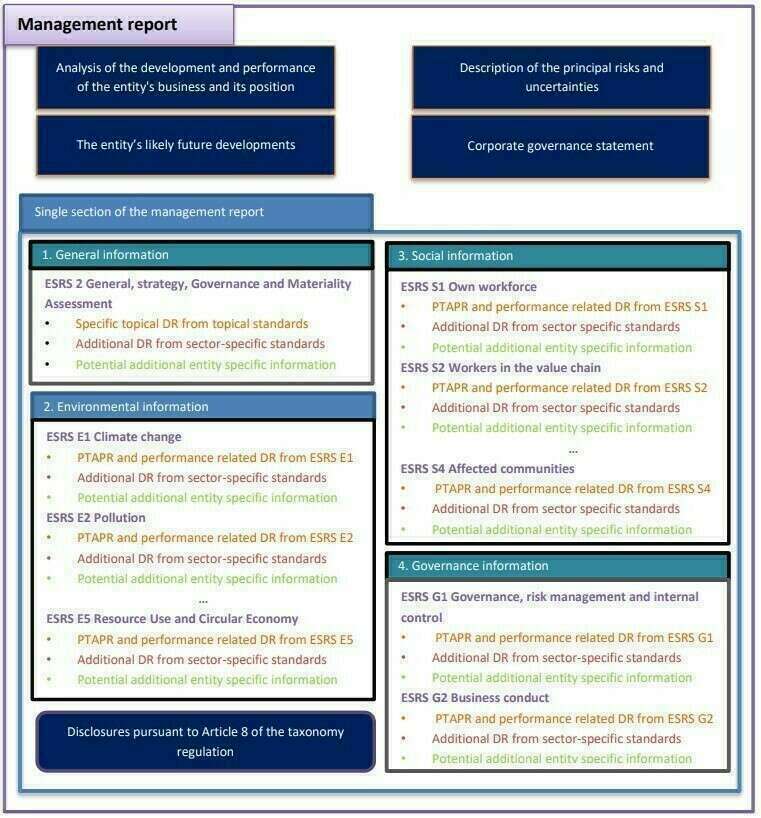

Presentation of the sustainability statement:

The latest version of the CSRD text has chosen to promote a presentation in the form of a single separately identifiable section of the management report.

Table 3 - Example of sustainability reporting organisation within the company management report

Source: EFRAG draft ESRS1

DR = Disclosure Requirement; PTAPR = Policy Target Action Plan and Resources.

2023-2024: Set 2 - additional standards

Following the issuance of the final text of the CSRD, the following content of Set 2 is anticipated to be adopted by the European Commission by 30 June 2024, with EFRAG consulting and delivering its recommendations by November 2023:

a) First set of sector-specific standards:

A first list of sectors has been confirmed for the adoption of sector-specific standards by June 2024:

- Agriculture, - Farming and Fishing

- oal Mining & Mining

- Energy and Utilities

- Food and Beverages

- Motor Vehicles

- Oil and Gas Mid to Downstream & Oil and Gas Upstream

- Road Transport

- Textiles, Accessories, Jewelry and Footwear

Additional sets of sector specific standards will be defined by November 2024 and November 2025 – the exact list of sectors for these timelines remains to be confirmed.

b) Standard for non-EU companies

c) Standard for listed SMEs

d) Voluntary guidance for non-listed SMEs

What will the ESRS require from corporates and bring to investors? What the ESRS are, what they are not

- Sustainability reporting put at the same level as financial reporting

This is the objective of the EU, to provide sustainability reporting that is relevant, comparable, reliable, containing forward-looking and restrospective information, with the same level of standardization as financial reporting. The challenge is great though since all sustainability issues are not at the same level of maturity in terms of understanding, measurement or not under the same level of control of the company across the value chain. In most cases, sustainability issues also require a great deal of qualitative information to provide appropriate understanding to the users. The disclosure requirements have been drafted consequently but still pose some challenges for preparers and auditors in terms of gathering all the necessary information and ensuring its quality.

- A disclosure requirement aimed at enabling Financial Market Participants to comply with their own obligations and instore a dialogue on sustainability between investors and issuers

The CSRD, redefining corporates’ sustainability reporting obligations, arrives paradoxically after the definition of new disclosure regulations for the financial sector (Taxonomy Regulation and SFDR). CSRD is therefore aimed at requiring appropriate information to companies, so as to enable Financial Market Participants to meet their own obligations (such as reporting of SFDR Principle Adverse Indicators) but also more broadly to set a basis for dialogue on issuers’ policies, targets, action plans, resources and performance on all sustainability-related aspects.

- An obligation to disclose, not a duty to perform

The very granular level of the disclosure requirements in the executive drafts, with several hundreds of data points, has also created some confusion for some preparers as to the very nature of the ESRS.Even though the disclosure requirement may prove an incentive to endorse some specific sustainability-related practices, they remain merely disclosure requirement. Not having endorsed any specific policy or target, if material to the company’s activities, should only be reported but a company would never be sanctioned for not having implemented any element mentioned in the ESRSs.

Examples of issues at stake - Many significant questions emerged following the public consultation on the draft ESRS.

- Among them, Rebuttable presumption and the definition of materiality

In the initial version of the ESRSs, the concept of “rebuttable presumption” has emerged so as to enable a reporting company to “rebut” a disclosure requirement when it is not deemed material for the company. This principle is debated as potentially controversial, both in terms of the content (would it be an easy exit door for companies and would this lead to contentious interpretations of sustainable materiality) and on the “burden of the proof” to justify or not when a company would decide not to report. This issue is very much linked to the question of who should decide that a sustainability topic is material (the regulator, the company, both?), of the granularity of the reporting (the burden to report or rebut and justify is higher when the disclosure requirements are extensive), and what should remain sector-agnostic or become sector-specific.

- Granularity and extensiveness vs comprehensiveness

The extensiveness and the high level of granularity of the disclosure requirements, the number of data points in the ESRS have raised some concerns among preparers. EFRAG is faced with the challenge to both keep the level of ambition enshrined in the CSRD, to meet users’ expectations and to limit the number of disclosure requirements (about 200 initially) and data points (more than 1000) to a more reasonable number. The latest version of the CSRD text, adopted in June 2022 and that sets the overall framework, has also limited the scope of the disclosure requirements in some cases. For instance, governance disclosures should only be linked to the governance of sustainability and issues such as tax evasion have been excluded from the scope – more for political reasons among Member States than for limiting the burden of reporting on companies.

- Complementarity or equivalence with other international standards

While the global race to establish sustainability standards has seen a growing consolidation of initiatives, the EU and EFRAG approach remains the most advanced, on the anglo-saxon side, the International Sustainability Standards Board (ISSB) aims to bring together all private stakeholders implementing an ESG reporting framework. This board, an offshoot of the IFRS Foundation, continues its work on climate-related disclosures, and on ESG disclosure on the basis of a single financial materiality perspective so as to serve only investors. While the EU approach is regulatory and based on standards, the ISSB approach will only provide soft guidelines and recommendations, although the two approaches are quite similar and convergent in terms of granularity for climate-related disclosures. The EU standards remain more comprehensive, and CSRD has required EFRAG to provide standards that take into account international developments. The definition of an equivalence system between ISSB reporting and CSRD reporting (to make any CSRD automatically compliant with ISSB) would limit the reporting burden of international companies but remains uncertain at this stage.

- Defining the value chain

The definition and extensiveness of the value chain, which has to be taken into account when assessing companies impacts, risks and opportunities, is a point of debate, with an additional specific need to take into account the specificity of the financial sector and the challenges and relevance questions hinging around the integration of financed assets into the consolidation of some indicators.

[1] The Council and European Parliament have reached a political agreement on the corporate sustainability reporting directive (CSRD) on June 21st, 2022, which was subsequently approved by Coreper. The final text was published on June 30th, 2022.

[2] Subsidiary companies are exempt to share the non-financial information if they are included in the annual report regarding the consolidated annual accounts of their parent companies (i.e., the companies that control the management and operation of the subsidiary companies)

[3] Definition of categories of undertakings and groups: article 3, Directive 2013/34/EU: micro-enterprises: balance sheet EUR 350 0000, net turnover EUR 700 kEUR, 10 employees yearly average);

[4] Definition of categories of undertakings and groups: article 3, Directive 2013/34/EU: SMEs: balance sheet EUR 4M to 20 M, net turnover EUR 8M to EUR 40M, employees 50 to 250

[5] EFRAG is a private association established in 2001 created with the encouragement of the Commission to serve the public interest. Majority financed by the EU, EFRAG relies on a public-private partnership model and its role has been to advise the Commission on the adoption of international financial reporting standards into EU law. This role has now been extended to sustainability reporting standards

[6] The European Securities and Markets Authority (ESMA), the European Banking Authority (EBA), the European Insurance and Occupational Pensions Authority (EIOPA)

[7] The European Securities and Markets Authority (ESMA), the European Banking Authority (EBA), the European Insurance and Occupational Pensions Authority (EIOPA)