Blue finance: beyond climate, highlighting nature objectives

Introduction

2024 brought the blue label further into the spotlight, notably with Europe’s first benchmark corporate blue bond for Saur, and Fidelity’s Blue Transition Bond fund. The interest in blue finance has continued to grow into 2025, extending beyond Europe with Banco do Brasil closing a Blue Repo transaction. These developments bring a comprehensive approach to the financing of broader environmental goals by bridging the gap between climate and nature objectives.

Natixis foresees this thematic to further expand in sustainable finance. The Blue label highlights the importance of water resources, both freshwater and marine, for environmental and social objectives, notably its interrelations with nature and climate adaptation.

Water challenges are increasingly acute, with news on destructive floods in Valencia (Spain) and Rio Grande do Sul (Brazil), or droughts leading to wildfires (California). The blue label allows for a better identification of water-related investments, material to other sustainability and social objectives, such as resource preservation, health protection (drinking, sanitation) or climate change adaptation.

What makes a bond (or other financing) blue? Blue bonds are a subset of Green bonds, as such as blue bond is aligned to the International Capital Market Association (ICMA)’s Green Bond Principles. Blue is a thematic, a label to highlight the domain or area of the financed use of proceeds. What falls under “blue” is not strictly defined, and there are various perspectives in the market: One perspective, followed by the ICMA in its 2023 Practitioner’s guide, is to focus on marine resources and coastal ecosystems. The other is to have a broader interpretation, including freshwater and wastewater management, and the overlap with environmental objectives such as pollution prevention and control, natural resources conservation, biodiversity and climate change mitigation, which is the stance taken by the International Finance Corporation (IFC) in its Guidelines for blue finance.

In practice, as highlighted for instance by Fitch’s 2024 research paper on the topic, freshwater projects receive a larger share of funding compared to marine initiatives. From the investor side, interest in blue bonds has been notable, one example featuring this appetite being Fidelity’s launch of a dedicated blue fund in October 2024, which contribute to both ocean and freshwater objectives. This separation between “marine” and “freshwater” investments is not strictly followed in the market, and Natixis GSH encourages a consolidated approach in coherence with the water cycle, that encompasses multiple interactions. Indeed, the water cycle (also called hydrological cycle), encompasses various stages, and interrelations between freshwater bodies (like rivers, lakes, and wetlands) and marine ecosystems (oceans and seas). Rainwater that falls on land flow into rivers and eventually reach the ocean, making freshwater ecosystems vital to the health of marine environments. Land runoff carries nutrients and organic matter into marine systems, which when in excess, harm these ecosystems. This was the reason why in the Equity Index “Euronext Water and Ocean Europe 40 EWD5” designed by Natixis, the eligibility criteria target companies contributing both to supplying, treating, preserving, optimizing the freshwater resource but also protecting oceans.

Issued in October 2024, Saur's blue bond represents a milestone in the evolution of the blue market. As a leading sustainable water utility, Saur's blue bond will finance expenditures related to water supply and wastewater treatment, financing its core mission of preserving water resources, particularly vulnerable to the challenges of climate change. This transaction extends opportunities for blue finance beyond ocean & marine protection. Natixis acted as Global Coordinator and ESG Coordinator for this transaction, highlighting Saur’s environmental contributions and developing the blue market.

From the perspective of Bénédicte Peyrol, Saur’s Head of Sustainability: “the blue label was a natural choice to reaffirm our leadership role in the water transition, from reducing consumption upstream to valorizing wastewater downstream. It also aligns with our strategy of innovation, as we develop into industrial water solutions and expand nature-based solutions. This blue bond further highlights our commitment to resource preservation and brings more light to the crucial topics of protection of ecosystems and sustainable water management”.

Investor response to Saur's blue bond was positive, with over 100 investors engaged during the two days of marketing. This strong interest allowed the issuer to seize its largest bond size ever (upsizing to €550 million) thanks to qualitative demand (€1.95bn of final investors’ interests) and at very attractive financing conditions (the issuer achieved its strongest spread tightening in the euro market).

As Saida Eggerstedt, Head of Sustainable Credit at Schroder Investment Management, an investor in the bond, highlighted: “The Blue Bond will finance predominantly CAPEX for Water production and supply as well as wastewater collection and treatment, supporting to provide citizens with clean drinking water and efficient, effective wastewater treatment. This fits our impact objectives of a healthy society with access to essential services like clean water and responsible use of resources like water. In longer term, it also helps health and wellness. Blue bonds are rare and while they are technically a branch of green bonds, it needs to be embraced by water-related issuers to meet SDG 6 goals, and hopefully over time also to protect life below water, SDG 14, as all water ends in the sea.”

The second largest bank in Latin America by total assets, Banco do Brasil, has closed its first Blue financing in March 2025 with Natixis CIB as counterparty and Blue Coordinator. The Blue Repo was a USD 95 million 2-year transaction which will finance Banco do Brasil’s eligible water and sanitation portfolio. As one of the largest financial institutions in Brazil – covering 92,9% of municipalities – the Bank plays an important role in enabling sustainable development at the local level, which includes enhancing water supply and improving sanitation coverage. The transaction will support Brazilian states and municipalities in financing water capture, distribution and treatment projects, and the expansion of basic sanitation.

Francisco Lassalvia, Chief Wholesale Officer, highlighted Banco’s do Brasil commitment to sustainable finance and innovation by stating "the transaction reinforces Banco do Brasil's pioneering role in structuring treasury operations focused on sustainable finance, consolidating our leadership position in this segment. Once again, we have the support of a major international partner, such as Natixis CIB, in this transaction, […] which demonstrates our commitment to innovation and sustainability in the global financial market.”

For José Ricardo Sasseron, Vice President of Government and Corporate Sustainability “This transaction is a milestone and was only possible precisely because of Banco do Brasil's leading role in operations with the public sector in supporting public policies. We are excited about the success of the 'Blue Repo' transaction and believe that it will have a significant impact on promoting new water and sanitation projects”

The Blue Repo highlights the use of different financing instruments in sustainable finance, in this case, providing helpful optimization and liquidity in the broader context of sustainable funding programs.

Tracking blue debt remains somewhat complex due to the diversity of labels (blue, water, etc.), at the discretion of the issuer, and heterogenous market guidance. Data from Bloomberg underscores the growth in blue bond issuance over the past few years. In 2023, the market achieved a total of $4.79 billion from 16 blue bonds, largely propelled by a $1 billion issuance from the Export-Import Bank of Korea in November. The momentum has continued into 2024, which has already seen over $3.2 billion raised through 22 blue bond issuances. Although the total amount issued in 2024 is lower than in 2023, the increase in the number of bonds demonstrates the development of this format among issuers.

Current blue bond issuers (as tracked by Bloomberg) are mainly SSA (Sovereign, Supranational and Agency) and corporate issuers, with a few financial institutions also present in this segment. Geographically, most of the blue bond activity is concentrated in the Asia-Pacific region, with some issuances in South America. In hjyubn, featuring a few examples such as the €100 million blue bond issued by Ørsted in 2023 to finance offshore biodiversity, and Saur’s recent issuance (see above).

The rising interest in blue transactions aligns with a broader trend in sustainable finance, where themes related to nature, particularly biodiversity, are gaining prominence. Water issuers overlap not only with biodiversity but also climate adaptation, as water supply and wastewater treatment investments are directly impacted by droughts, heavier rainfall patterns as well as increased frequency of extreme weather events.

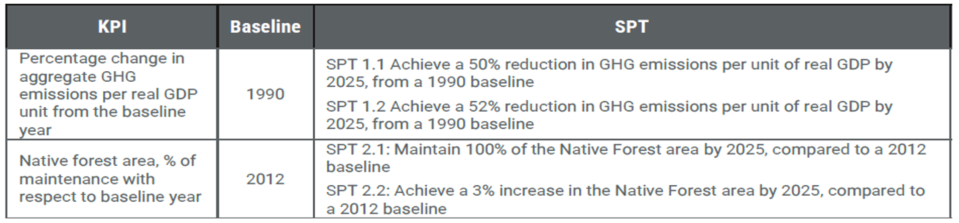

Figure 10: selected KPI and SPT within Uruguay's SLB Framework

Source: Natixis GSH based on Uruguay’s SLB Framework.

Webinars

Tuesday 19th September

5.00 p.m. - 6.00 p.m.(CEST)

11.00 a.m. - 12 p.m. (EST)

Presented by:

Robert White, Managing Director, Head of GSH, Americas - Natixis CIB

Leisa Cardoso De Souza, Green & Sustainable Finance Expert, GSH, EMEA - Natixis CIB

Vishwas Vidyaranya, Co-Founder, Ambire Global / Consultant Climate Bonds Initiative

Tuesday 26th September

3:00pm - 4:00 pm (UTC+08:00)

9:00am - 10:00 am (UTC+01:00)

Presented by:

Olivier Menard, Head of Green & Sustainable Hub, APAC, Natixis CIB

Leisa Cardoso De Souza, Green & Sustainable Finance Expert, Green and Sustainable Hub, EMEA, Natixis CIB

Manshu Deng, Deputy Head of China Programme, Climate Bonds Initiative

To register, send an e-mail at:

CIB-Communications@natixis.com

To register, send an e-mail at:

communication-asia@natixis.com

[1] Read more about the greening of the corporate portfolio and the collateral framework in the letter of Christine Lagarde, “Further steps to incorporate climate change into ECB’s monetary policy operations”, July 4th 2022, available here.

[2] Read more about the last ECB monetary decisions in the associated Press Release, June 9th, 2022, available here.

[3] Note that CSPP holdings are published here with aggregate data, such as total holdings, a breakdown of primary and secondary market purchases, and a breakdown by rating, country and sector.

[4] See Eurostat “Flash estimate - July 2022 Euro area annual inflation up to 8.9%”, July 29st 2022, available here.

[5] Prior to the COVID-19 crisis, the ECB used to purchase government bonds in proportion to the capital each Member State contributes. However, its €750bn Pandemic Emergency Purchase Program (PEPP) is more flexible, allowing for instance, the purchase of more Italian and Spanish Bonds to prevent the widening of spreads. Issuer-limit that forbids the ECB from holding more than a third of any member’s sovereign debt has also been lifted.

[6] See in the “Decarbonizing is easy: beyond market neutrality in the ECB’s corporate QE” paper published by The New Economics Foundation, UK universities, Greenpeace in October 2020 here.

[7] As enshrined in the Article 3 of the Treaty on European Union.

[8] “Climate change and the transition to a greener economy affect our primary objective of maintaining price stability due to their impact on our economy and on the risk profile and value of the assets on the Eurosystem balance sheet” notes the ECB in Annex “ECB Climate Agenda 2022”, available here.

[9] The latest full list of eligible assets is made available by the ECB here.

[10] See “Occasional Paper Series: the Eurosystem collateral framework explained” published in May 2017 by the ECB here.

[11] As the Central Bank has a zero-default probability in domestic market operations, collateral providers are willing to accept severe haircuts to obtain credit. The higher the haircut (against valuation uncertainty before counterparty default or against value changes after counterparty default), the better the central bank is protected.

[12] As a reminder, the CSRD applies to large-public interest companies with more than 500 employees. This covers approximately 11 700 large companies and groups across the EU including listed companies, banks, insurance companies, other companies designated by national authorities as public-interest entities. More information on corporate sustainability reporting is available here.

[13] More information on the Eurosystem credit assessment framework is published by the ECB here.

[14] In addition to debt instruments issued by corporates, marketable assets include ECB debt certificates, central government debt instruments debt instruments issued by central banks, local and regional government debt instruments, supranational debt instruments, covered bank bonds, credit institutions debt instruments, and asset-backed securities according to ECB website.

[15] See in the ECB Press Release,“ECB takes further steps to incorporate climate change into its monetary policy operations”, July 4th 2022, available here.

[16] According to the preliminary figures on Asset purchase programmes, as of June 2022, available here.

[17] See in ECB Blog, “A catalyst for greening the financial system”, July 8th 2022, available here.

[18] According to the preliminary figures on Asset purchase programmes, as of June 2022, available here.

[19] “PSPP purchases are guided by the ECB’s capital key on a stock basis over the life of the programme. In order to implement the allocation, the Eurosystem gears its monthly purchases to align a jurisdiction’s share in the PSPP stock over the medium term as closely as possible with the respective share of the ECB’s capital key.” Read more about the Public sector purchase programme (PSPP) in the ECB Q&A here.

[20] Read more about capital subscription here.

[21] Note that PSPP stands for “Public Sector Purchase Programme”, CPBB3 stands for “Third Covered Bond Purchase Programme”, CSPP stands for “Corporate Sector Purchase programme and ABSPP stands for “Asset-backed Securities Purchase Programme”.

[22] See in the Financial Times, “ECB set for greener ‘tilt’ in €386bn corporate bond portfolio”, July 4th,2022, published here.

[23] Read more in the Annex to the minutes, “The Riksbank’s purchases of bonds during the second half of 2022”, June 29th 2022, published here.

[24] Read more about the Bank of England and the greening of its corporate portfolio on its website, “Greening our Corporate Bond Purchase Scheme (CBPS)” available here.

[25] See Speech by François Villeroy de Galhau, Governor of the Banque de France, “The role of central banks in the greening of the economy”, February 11th 2021, available here.

[26] The study “Decarbonizing is easy: beyond market neutrality in the ECB’s corporate QE” published by the New Economics Foundation, a UK thinktank, Greenpeace and UK universities in October 2022 is available here.

[27] The study “An environmental mandate, now what” published by university of London, University of Greenwich and the University of the West of England in January 2022 is available here.

[28] Read more about Carbon4 providing climate-related data to the Eurosystem on its website. Press release, “Carbon4 Finance selected by the Eurosystem to supply climate-change related investment data”, March 10th 2022, available here.

[29] Read more about the study “Sustainable investing and climate transition risk: a portfolio rebalancing approach” published by Giacomo Bressan, Irene Monasterolo and Stefano on June 20th 2022 here.