Extended Taxonomy: in betweenness and elitism softening

The Platform’s March 2022 recommendations on extending the Taxonomy are timely and meaningful, but unlikely to be politically endorsed. Nonetheless, market participants must not wait for unpredictable legislative outcomes to consider or even test the suggested concepts.

The current Taxonomy scheme is too static and binary and incidentally too “elitist”. If enacted, the Platform’s proposals would allow more inclusiveness, while preventing transition washing.

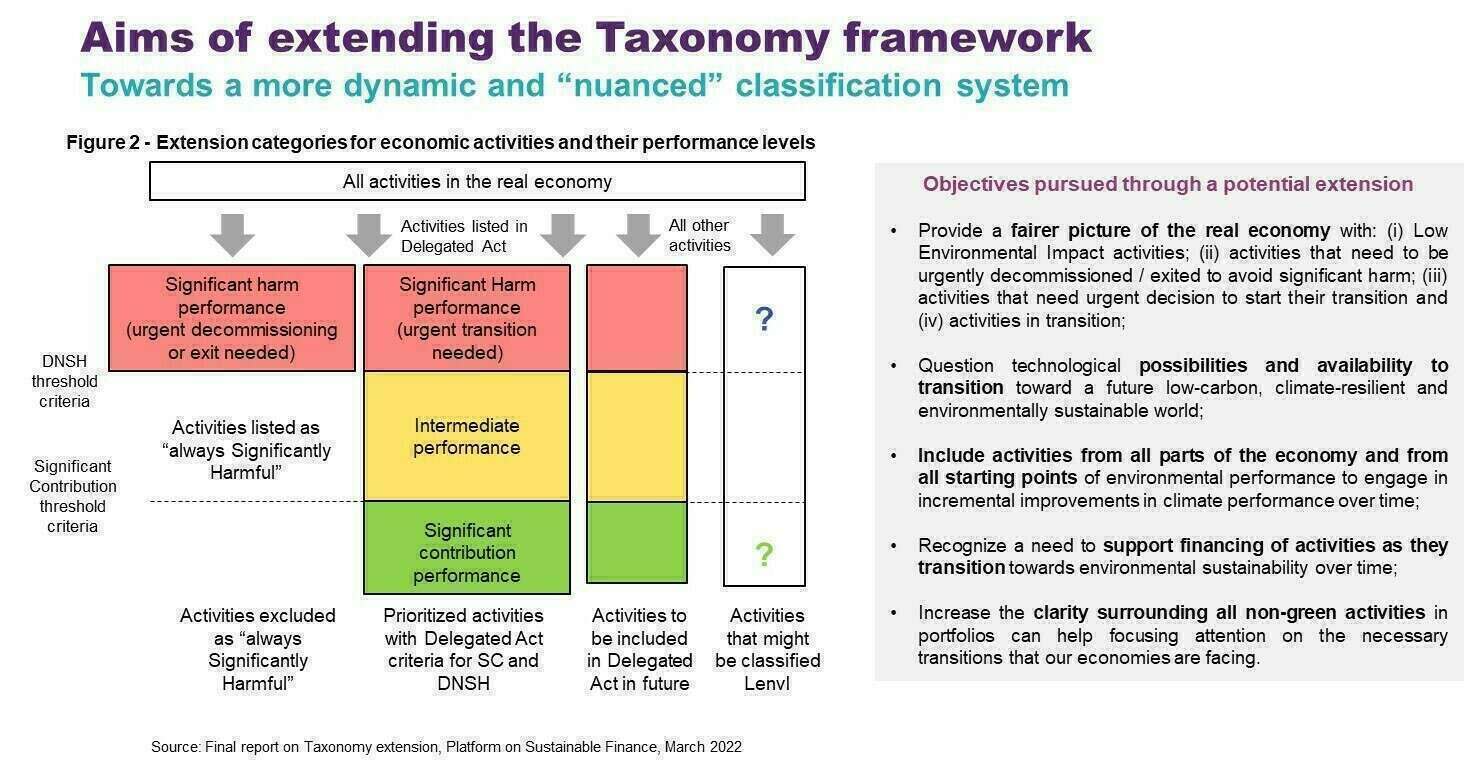

The group of Experts proposes to explicitly introduce additional performance levels, in particular “amber” for Intermediary Performance (IP) and “red” for Significantly Harmful (SH) performance. Among the latter, the “always significantly harmful” activities would include “urgent exit” and pave the way to decommissioning finance, which we advocate.

Currently, several performance levels exist but only by default: Do No Significant Harm (DNSH), Significant Contribution (SC) and what implicitly stands in between. The Platform suggests formalizing a multi-level system, including “Low Environmental Impact activities” (ex: accounting services to SMEs or childcare). But the co-legislators never had in mind to set various performance levels, including Significant Harm. The three implicit levels interpretation is far stretched or even contra legem (A). Moreover, the three existing and implicit performance levels were not set to work in a dynamic space (B).

***

(A) Defining the red space, i.e., shades of Significant Harm from “urgent exit” to “urgent transition”, is of utmost relevance, especially for beyond exclusion or divestment uses. Decommissioning or urgent transition financing are desirable, provided attention is paid to labor issues (cf. on fair transition, 2021).

Regrettably, the Platform’s report falls short of “breakthrough” examples defining technologically “doomed” activities, limiting itself to obvious activities such as thermal coal mining and peat extraction.

Regarding the method, to define Significantly Harmful activities which must urgently transition, the Platform proposes to “reuse” the DNSH criteria. Thresholds indeed already exist for various heavy-industrial activities (e.g., manufacture of cement or aluminum). Nonetheless, Experts acknowledge the limitations in doing so, and the extra work that would be required, for inapplicable and qualitative DNSH, or the ones built on the sole respect of environmental or social laws. Furthermore, we believe explicit nuances are necessary within the “red space”. One must treat differently activities that must be decommissioned (i), the ones that urgently need to transition (ii) and the ones “simply” failing on the DNSH criteria (iii).

***

(B) The Platform groundbreakingly proposes to acknowledge changes from a performance level to another (e.g., red-to-amber transition) and track dynamics. Such performance shifts must be “constant” argue the Experts, for instance requiring to continuously staying out of Significant Harm performance level (red zone). Meanwhile, the boundaries of this red zone are meant to be tightening over time, what is being called “falling curves”.

Framing red-to-amber transitions is probably what could contribute the most to carbon cuts. To properly factor and encourage “enhancing movements”, the Platform partially breaks with pure activity-level canvas of assessment. We applaud this entity-level conceptual move, however confessing it inescapably increases complexity.

We recently noticed that the Complementary Delegated Act on gas power generation already deviated from the activity-level tenet with subsequent complications and shortcomings (cf. “Taxonomy criteria’s Achilles heel unearthed by the War in Ukraine”, March 2022).

For years, we have been advocating transition finance frameworks applicable at entity-level and anchored in green/brown shades and holistic criteria (“Why we need a shaded taxonomy from green to brown and in between”, 2019 and “Transition Tightrope Series”, 2021).

However, whether such performance up-notching must be backward and/or forward-looking is largely eluded by the Platform, as well as verification safeguards. The linchpin on which too many regulatory provisions are currently built is the notion of “transition plan”. This concept remains too vague as the CSRD simply refers to “business model and strategy compatibility with the objective to achieve climate neutrality by 2050 at the latest” (cf. EU-Green Bond Standard, 2022).

In contrast, awarding performance up-notching only ex post would limit sustainable finance instruments to refinancing, with a backward-looking bias and little additionality. So, when must the color of a transition plan be attributed? Should this plan be completed, underway or simply announced ? We suggest a trade-off requiring an already launched transition plan assorted with preliminary achievements (i), granular near-term milestones (ii) and a reasonable completion period (iii).

The need for accountability is made more daunting by the Taxonomy extension avenues laid down by the Platform. It once again raises the question of third-parties’ roles and responsibility. The pitfalls of forward-looking criteria can be summarized in one oxymoron: “intents enforcement”. Policy makers and financial watchdogs must handle the discrepancies between intended transition plans and what ultimately comes to fruition. Any transition plan cannot be taken for granted based only on intent. Meanwhile, products design should not incentivize issuers to set low-hanging targets by fear of failure and stigmatization. Then the question left unanswered is who takes responsibility for gaps, on what basis, and with what product and labelling consequences.

***

The timeline for Taxonomy extension is blurred, due to Taxonomy-related bottlenecks (tough adoption of complementary DA on gas and nuclear, adoption of technical criteria for the four non-environmental objectives, unlikely extension to social objectives). Regulatory fatigue is noticeable among market participants, despite real implementation and appropriation progress (see the takeaways of a panel we recently organized at Environmental Finance Conference, Apr. 2022).

We doubt the European Commission has the guts to launch the several years legislative fight to formalize red/significant harm performance levels (which can be perceived as an “exit signal” and will be fiercely opposed by economic and political lobbies). This is probably why the Platform advocates a rapid phasing in (“as rapid as possible”), and a voluntary reporting (based on the first legally in-force climate Delegated Act criteria). In the meantime, Experts insist the necessary work to identify activities for which no technological possibility of improving their environmental performance must be initiated as soon as possible.

We believe the complexity of the extension proposals should not be overstated provided the different color /performance levels are set alongside the same unit and metric. The entry costs of mapping out activities against technical screening criteria can be lowered once and for all within companies and financiers.

The present study is therefore there to help launching the “trial period” and spur the voluntary uses encouraged by the Platform. There must be a continuum between industry-led standards/initiatives and hard-law requirements. Regulatory growth does not disregard market innovation. It simply requires exploring new domains where experimentation is needed prior to legislators or supervisors’ intervention.

Natixis CIB Green & Sustainable Hub Team