France’s strategy on export financing: a stick and carrot approach with fossil fuels funding phasing out and a supporting factor for EU Taxonomy compliant activities

- 12-minute read -

The French Directorate-General of the Treasury handed a report to the Parliament on a climate strategy for public export financing last October. Through amendments to the 2021 Finance law proposal, the French government thereby commits to (1) a phasing-out trajectory of the public support to fossil energy export projects (see details below and our article this month about Engie halting its talks over US LNG supply contract); (2) tighter public support for export projects related to power generation; and (3) a climate reward mechanism for export project support (through credit-insurances) for activities deemed sustainable based on the EU Taxonomy.

As France pledged to support the development of its export sectors in projects that are compatible to the Paris agreement, Bpifrance Assurance Export, which is the guarantor of export credit-insurances and thus a lender of last resort, will establish a methodology to assess whether a project or activity in its portfolio or pipe is sustainable based on the EU Taxonomy and on ad hoc methodologies for “brown industries” not yet covered like naval and aeronautics construction.

Moreover, following the “Green budget” exercise where the French government mapped the environmental impact of its budgetary and fiscal expenses over the 2021 Finance law proposal (see our article), France becomes the first country to establish a methodology to assess the carbon footprint of its public export balance sheet, an additional step in the mainstreaming of climate considerations into public policies.

Background on the climate strategy on export financing

Public export guarantees are public policy tools used in export finance. They are attributed to companies if they produce the value added of their products in France. These companies are usually of strategic interest for industrial sovereignty: defense, naval construction and aeronautics represent 75% of credit-insurance amounts. In a competitive international environment, these French companies use export supporting mechanisms to win public procurements. To note, Germany intends to implement mechanisms to support German companies exporting renewable energy projects abroad[1].

Most OECD countries today have import-export banks[2]. However, getting public guarantees does not actually give an edge to win public markets, but on the contrary those who do not benefit from them get a direct disadvantage. Subsequently, the access to these tools is itself linked with a company’s capacity to challenge its competitors. It is particularly the case in sectors that are capital intensive and where companies need important financial, industrial and human investments.

- What are public guarantees?

The French State, through Bpifrance Assurance Export, gives guarantees on financial operations in order to support exportations. These guarantees consist in insurance contracts: the State assumes financial risks that lenders are not keen to assume because the loan is too big, the country is risky or due to market reasons. Several mechanisms of this kind exist:

- Export credit-insurance (95% in volume of the current portfolio): covers the financing of the export project in case of a contract ending or against a risk of default.

- Prospecting insurance: covers project expense against its failure risk (operational risk).

- Guarantees covering sureties and pre-financing of the exporter.

- Exchange rate guarantees: cover the exporter against exchange rate changes during contract negotiation or sometimes during contract execution.

- Strategic project guarantees cover projects of French companies deemed strategic for the national economy.

- Insurance-investment: covers Foreign direct investment against political risk.

French new climate strategy proposal over export financing

After the COP 21, France pledged to end its support for export projects in coal power plants and in unconventional hydrocarbon exploration and exploitation activities[3]. As an amendment to the 2021 Finance law proposal, the French government handed a report to the Parliament about a climate strategy over export financing composed of three main proposals:

- The first proposal is to progressively phase-out public support for export projects in fossil energy activities. The French oil- and gas-related industries generate 90% of their revenue abroad and employed 50 000 people in France in 2019. These sectors encompass different segments from upstream to downstream activities. However, the French oil and gas industries have few manufacturing plants in France: among a sample of 18 companies that were beneficiaries of credit-insurances, out of their 2019 revenue, they generated €1.2 bn from goods exports and €6.3 bn from services exports. These sectors represent 4% of Bpifrance Assurance Export’s portfolio with €2.7 bn of loan-insurances. The French government proposes the following timeframe to phase-out from fossil energy export projects and provides estimations of the social impact this trajectory can have on the sector in terms of lost opportunities (translated into lost jobs):

There are two exceptions to this new policy:

i. First, the ban is applicable to exploration and exploitation activities and does not touch upon midstream and downstream segments of the industry like transport & distribution and petrochemistry.

ii. Second, the trajectory will be frequently reassessed to redefine the most adapted end dates in accordance with climate and industrial considerations while guaranteeing that there would be at least four years between the decision about the end of the eligibility and its actual end. This means the 2035 year end for gas projects can still change as well as the end date for conventional oil projects.

This timeframe has been criticized by Friends of the Earth. However, this is still an aggressive strategy because France risks penalizing its oil and gas industry. Its actors will probably win fewer public procurements when these ineligibilities are applied. Only Sweden has decided to go beyond unconventional hydrocarbon exploration and exploitation: the Swedish trade and investment strategy aims at phasing out public support to exploration and extraction of all fossil fuels by 2022 at the latest.

2. The second proposal of the government is to stop public support for export projects on power producing assets if the following condition: after a life-cycle analysis of the carbon intensity of projected power plant in gCO2/kWh, if this intensity is higher than the average carbon intensity of the electricity mix of the recipient country, then the project is not eligible to public credit-insurers. There are three exceptions to this rule and three cases where plants with a higher carbon intensity are still eligible to credit-insurance:

i. If the plant is necessary to the stability of the power grid of the recipient country and if pilotable low carbon alternatives are not available or too costly, the plant is eligible. A gas thermal plant would thus be eligible in a country that massively invests in intermittent renewable energies.

ii. If the use of low carbon sources is impossible for instance due to a low capacity of a country to develop them (geographical reasons like interconnexion difficulties of renewable plants with the grid).

iii. If the country has a low-carbon transition strategy for its power sector and if the project is still coherent in that strategy, then the project is eligible.

These exceptions seem broad and will let significant room for interpretation.

3. The third proposal of the French government is to implement a climate reward to export projects that are deemed sustainable. We will dig into this proposal and before studying the portfolio of credit-insurances of Bpifrance Assurance Export and its carbon impact, we will analyze different credit export tools.

Support to export projects in France

- Bpifrance Assurance Export’s portfolio composition

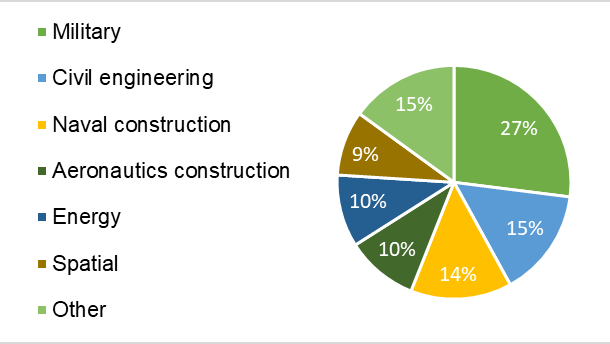

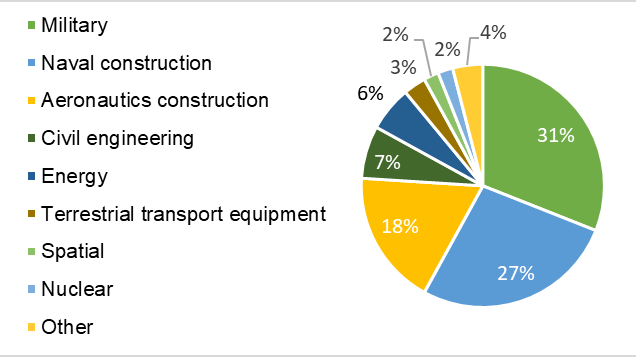

In 2019, Bpi Assurance Export distributed €11.7 bn of export credit-insurance guarantees (against €14.6 bn in 2019) and its portfolio volume (stock of guarantees accorded) was €59.2 bn (against €65.1 bn in 2019). As we can see, these are sectors that are intensive in capital, whereby there is a strong desire for recipient states or agencies in charge of public procurements to receive sound proposals that are backed by lenders of last resort like Bpi Assurance Export.

Renewable energy (RE) financing represents €400 m in the portfolio (less than 1% of it) with mainly solar PV plants and hydropower capacities. In 2019, €200 m worth of new credit-insurance contracts were signed, out of which 90% for PV plants. The volume of RE projects is small because according to the report, goods and services production capacities in this sector are not as developed in France as in other countries like Germany or Spain for instance, and public guarantees do not aim at supporting equity investment in export projects unless the firms have capacities and means in France beforehand.

Table 1. Credit-insurance guarantees attributed by Bpi Assurance Export by sector in 2019 (€11.7 bn)

Table 2. Credit-insurance guarantees in Bpi Assurance Export’s portfolio by sector (stock as of end 2019: €59.2 bn)

Carbon impact of the export guarantee portfolio

Scope - As credit-insurance represents 95% of the stock of loans in its €60 bn portfolio out of the 6 asset classes that Bpifrance manages (mentioned above), the methodology is focused on credit-insurance. Moreover, the carbon impact assessment has been conducted on the civil portfolio (military loans have been excluded), which represents two thirds of the total credit-insurance portfolio.

Methodology - For the first time among credit insurers, Bpifrance Assurance Export conducted a climate analysis of the aforementioned portfolio covering Scope 1, Scope 2 and Scope 3 emissions as well as intensity in tCO2/M€.The carbon impact of “activities” (companies, industrial assets or ad hoc projects) guaranteed and supported has been analyzed both in absolute terms and with intensity metrics (tCO2/M€). First, the carbon intensity of each project is calculated[']. hen, BpiFrance gets a share of this carbon impact according to share of the total equity and debt raised that is guaranteed.

Results - On a portfolio of €40 bn of credit-insurance under guarantee, there are 3 Million TCO2 of Scope 1 + 2 emissions and 50 million TCO2 of Scope 3 emissions. Naval construction and cruises represent 39% of the total carbon impact of the portfolio, civil aviation 25%, oil and petrochemical installations 5% and thermic plants 3%.

This carbon impact assessment does not constitute a tool in itself to define public policies yet. Moreover, being the lender of last resort here does not allow to monitor this portfolio's carbon trajectory. Thus, to reduce the carbon intensity of this portfolio, the solution is either to abandon highly emitting sectors or to increase the share of less emitting sectors (or both).

A climate reward for sustainable export projects

- The need for a climate incentivizing mechanism

The French government, through Bruno Le Maire, Minister of Economy and Finance, has announced that a climate support mechanism (reward) will be put in place during the Climate Finance Day.

As export mechanisms are first conceived as public policy tools to back industry, their effect can be used to support green or sustainable projects or their companies. The main obstacle is that these tools are used for mature technologies and assets that are produced in France like it is the case of ship manufacturing in the Saint-Nazaire harbour. All “green” sectors or technologies are not at this maturity stage. These tools should thus be accompanied by other supporting mechanisms like the “Investment for the Future Program” (so-called PIA program), European funds or more favorable regulation overall (it seems competition is emerging between Spain, Germany and France on industrial hydrogen producing capacities, notably on the electrolysis segment).

The French Treasury thus proposes to introduce a climate reward mechanism. This reward could be based on a lump-sum model and calculated on the basis of technological cost abatement needed to make the projects profitable; or a reward could be attributed to projects that are deemed to have positive contribution to climate mitigation. That way, the reward could be applied to both renewable energy projects and to projects in highly emitting sectors when they allow to reduce the carbon impact of the industry compared to peers and/or counterfactuals.

- Limits of such a mechanism

Export credit-insurance and export credits are tools that are regulated by European competition law. The regulation aims at avoiding that public support gives way to projects selected on the sole basis of attractive bidding pricing rather than on criterii linked with the actual bid (after technical characteristics and economic cost-benefit analysis) and its adequation with the needs.

Public support to export projects is also regulated by an OECD Arrangement on Officially Support Credit Exports which is the “framework for the orderly use of officially supported export credits” whose aim is to foster a “level playing field” and “competition among exporters”[5]. There is thus a contradiction between environmental performance and objectives, and competition considerations.

- Possible options

In order to respect competition sub-requirements, public support to a sector can only be limited but it can be applied leveraging on three parameters:

- A stronger support during “pre-financing” stages of projects’ approval

During preliminary steps with industrials, the upstream phase often defines environmental objectives before the actual call for tenders. During this phase, foreign clients first study and then write the call for tenders with their needs and their decision criterii and this is the only phase where the prospect can decide if it looks for low-carbon technologies or more sustainable companies. By financing this study phase or actual impact assessment studies, Bpifrance Assurance Export could influence choices of the prospect and incentivize the inclusion of environmental criterii before the actual project enters into the financing phase (see the six public guarantee tools that the agency possesses above).

- Wider and more available resources for sustainable projects

By proposing more direct loans or concessionary loans with favourable conditions as well as with lower structuration fees for small cap project financing, it is possible to support the export of green projects. Along with export credit public guarantees provided by Bpifrance Assurance Credit, the State can sometimes propose direct financing tools for infrastructure projects or services[6]. These direct financing tools are:

i. Direct loans from the Treasury: export finance infrastructure or service projects with quite competitive terms compared to market conditions

ii. Direct loans from the Treasury for Public Development Aid projects conducted by French companies: these loans have very advantageous tariffs

iii. Reimbursable advances or actual donations to finance feasibility studies before project starts.

- A financial reward for export projects

Among export credit agencies, both private and public credit-insurers receive risk premiums according to the guarantees and the share of risk they bear. These premiums are calculated according to country risk profiles, political risk and commercial risk. In the case of sustainable projects, public credit agencies could thus apply a lower risk premium as a reward, and this, not to reflect lower financial risk, but to favor environmental performance. Such a climate reward is already conceived, and thus conceivable for other sectors, as more flexible terms and conditions are allowed for renewable energy, climate mitigation and water projects in the OECD Arrangement on Officially Support Credit Exports.

How can sustainable export projects be defined?

To define projects and assets that are sustainable among export projects, Bpifrance Assurance Export could attribute the climate reward on the base of the sustainable nature of the product or activity as defined in the EU Taxonomy. Indeed, the EU Taxonomy distinguishes between low-carbon activities, transitioning activities and enabling activities, and the goal is to apply a reward to projects and assets that have a substantial contribution to climate mitigation.

However, some sectors that are important to French exportations have not been yet reviewed (i.e. provided with technical screening criteria) in the Taxonomy. It is the case for Nuclear (because of the do-no-harm principle) and Aeronautics. Naval construction (34% of the portfolio) is not treated in its entirety as only freighted is provided with criteria[7]. Indeed, in the draft of the Taxonomy delegated acts, aircrafts are not included and only low-carbon air transport infrastructure (airports) is covered.

According to the French Treasury, the Taxonomy is a particularly well-adapted methodology for financial institutions like credit insurers, but its limit is that it signals alignment with European climate objectives, making it less applicable to extra-European projects. Thus, there is no methodology to date that defines sustainable activities that are (1) recognized internationally, (2) easily usable by Bpifrance Assurance Export, banks and industrials, and (3) covering the aforementioned export sectors for French industrials. The Taxonomy covers the first two criterii, but not the last one yet.

All in all, it is proposed to assess projects on the basis of the European Taxonomy on sustainable activities, excluding at first the naval and aeronautics sectors before an ad hoc methodology is applied for a transitory purpose[8].

This example demonstrates the extent to which the EU Taxonomy can become instrumental across various policies and also France’s willingness to remain at the forefront of climate action and financial innovation.

[1] The “German Energy Export Initiative” is carried out by the Germany Energy Agency (“dena”) which is commissioned by the Federal Ministry for Economic Affairs and Energy to implement its measures - more information about the role of dena here and about foreign trade supporting measures for renewable energy companies here.

[2] Import-export banks - Chinese EXIM banks are for instance particularly active in Africa for instance where Chinese companies are in charge of many infrastructure projects, notably a railway connection rehabilitated and jointly operated by Ethiopian and Chinese companies from Addis Abeba to Djibouti – more information available here.

[3] UK followed and stopped its support for coal projects in January 2020 – more information available here.[4] For downstream Scope 3 emissions which represent 65% of total absolute emissions of the portfolio, CO2 emissions’ factors have been identified and then applied to projects. Scope 1+2 emissions have been identified using annual CDP reports. Upstream Scope 3 emissions have been estimated with sectorial statistical emissions data.Thus, a specific impact assessment analysis is conducted for projects or assets with strong value (especially for ad hoc projects), for others, a statistic approach is used: a CDP-based approach is used for companies or assets that are “known”.

[4] For downstream Scope 3 emissions which represent 65% of total absolute emissions of the portfolio, CO2 emissions’ factors have been identified and then applied to projects. Scope 1+2 emissions have been identified using annual CDP reports. Upstream Scope 3 emissions have been estimated with sectorial statistical emissions data.Thus, a specific impact assessment analysis is conducted for projects or assets with strong value (especially for ad hoc projects), for others, a statistic approach is used: a CDP-based approach is used for companies or assets that are “known”.

[5] More information about the Arrangement available here.

[6] These need governmental approval and are negotiated with the contracting State to negotiate reimbursement. A committee composed of the Budget, the Treasury, the Ecology Ministry, the Foreign Affairs Ministry, the French Development Agency (AFD) and any other technical ministry selects the projects.

[7] For sea and coastal freight water transport vessels not dedicated to transporting fossil fuels, those that could be deemed sustainable assets (i) have zero direct (tailpipe) CO2 emissions; (ii) until 31 December 2025, are hybrid vessels that use at least 50% of zero direct (tailpipe) CO2 emission fuel mass or plug-in power for their normal operation; (iii) until 31 December 2025, and only where it can be proved that the vessels are used exclusively for provision of coastal services designed to enable modal shift of freight currently transported by land to sea. Cruising is thus not covered.

[8] For naval construction’s methodology, the report reminds that the International Maritime Organization (IMO) aims at reducing the total volume of the maritime sector’s GHG yearly emissions by at least 50% in 2050 compared to a 2008 baseline, which requires around 85% less CO2 emissions per ship. A mid-term objective is to cut carbon intensity of the fleet of ships by at least 40% between 2023 and 2030 compared to 2008 (Source: IMO, IMO GHG Reduction Strategy, 2018 – available here). The Poseidon Principles emerged from occidental banks financing maritime transport with a pledge to measure one a year global emissions of the ships in portfolio. Bpi Assurance Export will thus see if these ships are compatible with the trajectories defined by the IMO and to compare its own portfolio’s performances with peers.