Blackrock Report to the EU Commission on the integration of ESG factors into prudential frameworks

5-minute read

In August 2021, the European Commission, released a report[1] based on a study carried out by BlackRock Financial Markets Advisory on the integration of ESG objectives into EU banking prudential framework, banks’ business strategies and investment policies.

The report

The 273-page final study published by the European Commission was conducted as a stock take, collecting views from more than 150 stakeholders, including banks, supervisors, civil society organizations, etc., to reflect a full spectrum of opinions. The study’s objectives are to identify modalities of:

- integrating ESG risks into EU banks’ risk management processes;

- integrating ESG risks into EU prudential supervision;

- integrating ESG objectives into EU banks' business strategies and investment policies.

Although it does not provide detailed examples of best or worst practices, nor technical tools that could be directly actionable, the report provides a clear overview of current practices and challenges: despite most banks state that they have integrated ESG in their lending and investment activities at least partially, there is a need to further develop approaches to actively steer the portfolio towards ESG goals.

Integration of ESG risks within banks’ risk management

The study emphasized the need for standardized ESG definitions, data and targets while also stating the importance of granularity in definition and understanding of each of the E, S and G pillars. To ensure full alignment with the Paris Agreement goals and advance ESG risk integration, training and education are regarded as important tools, especially at the board level.

While most banks claim to they plan to fully integrate ESG risks, it is currently at an early stage and there is a lack of available and high quality ESG related data, guidelines, and integration tools. Banks’ measurement of their exposure to ESG risks is very limited. They conduct targeted pilot exercises but do not embed ESG risks into business-as-usual practices. Significant developments both at management and infrastructure level are required. Framework must be enhanced and standardized for better ESG risk integration and ESG related disclosure and reporting. Further development of quantitative approaches within banks’ risk management frameworks is required.

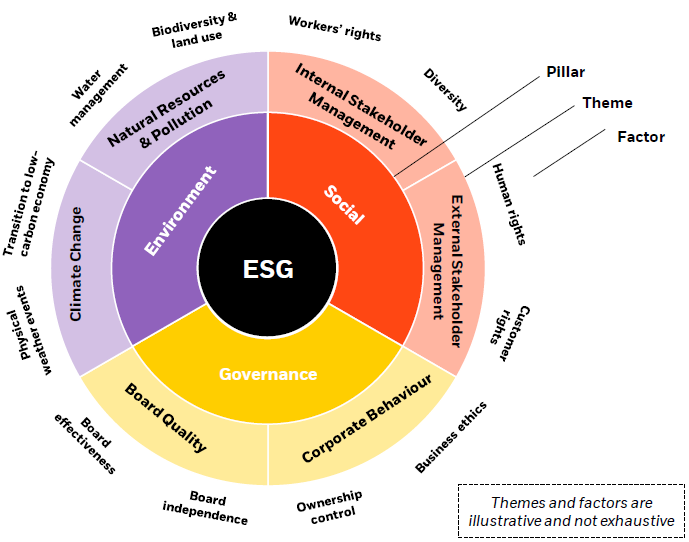

The below figure provides a visualisation of the terminological framework applied for the purposes of the study, including ESG pillars, themes, and underlying factors.

Figure 1 - Terminological framework including illustrative ESG themes and factors

Source: BlackRock Development of Tools and Mechanisms for the Integration of ESG Factors into the EU Banking Prudential Framework and into Banks' Business Strategies and Investment Policies

Integration of ESG risks within prudential supervision

The report is also critical of the supervisory authority stating there is no common ESG definition among supervisors. Many of them indicated their intention to observe the work of the European Banking Authority (EBA) and follow issued guidance in this respect. There are different levels of advancement among supervisors in relation to the assessment of ESG risks. Most supervisors have not yet defined quantitative indicators for the measurement of ESG risks and only few of them -for example, the European Central Bank (ECB) (focusing on climate and environmental related risks specifically), Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin), and Österreichische Finanzmarktaufsichtsbehörde (Austrian FMA)- have developed dedicated and publicly communicated ESG prudential strategies.

Meanwhile awaiting the outcome of the EBA mandates related to Pillar 1 and Pillar 3 of the Basel Accord, many supervisors do not currently consider Pillar 1 - capital requirements - tools as the best suited to address ESG risks, stating that robust quantitative evidence for a risk differential e.g. for green and brown assets is yet to be established. On the other hand, several civil society organisations rather see capital requirements as an effective tool. Arguing that it would play a role in incentivising banks to redirect capital towards more sustainable sectors and investments.

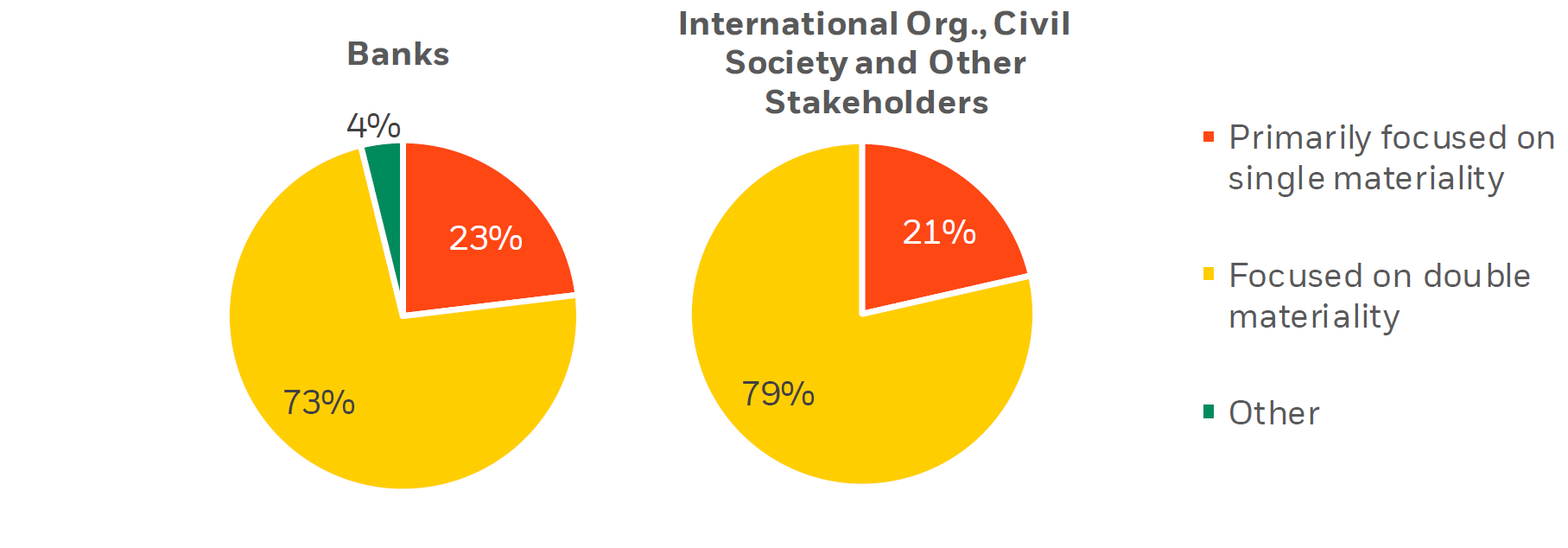

The document also recommends paying greater attention to the topic of ‘Double Materiality’[2], although it acknowledges that the consideration of sustainable materiality remains controversial among the supervisors and policy setters. Indeed, some consider prudential supervisory mandate should not go beyond financial materiality, i.e. considering how ESG risks and opportunities may impact banks’ balance sheet. The concept of sustainable materiality, which is promoted by common standards such as GRI[3] (Global Reporting Initiative), allows the banks to look beyond the potential impact of ESG risks on their balance sheet, and accordingly assess the impact of their activities on the external environment.

Not taking a clear position, BlackRock recommends promoting more standards allowing to better capture sustainable materiality, then opening the way to its inclusion into the prudential mandate.

Results from the study however show that most banks which have past the early stage of ESG integration already recognize double materiality as a better approach to define ESG risks. (Figure 1)

Figure 2 - ESG Definition by Materiality Approach

Source: BlackRock FMA analysis

Integration of ESG in banks’ business strategies and investment policies

Findings in the report showed an urgent need to gear up the process of defining and implementing ESG strategies into EU bank’s investment and business priorities, as it found that only a “few” banks had an explicit and well-defined ESG strategy in place. “While banks continue to evolve their offering of ESG-related products and services, such as sustainable bonds and green project finance, many ESG-related offerings are still under development or offered only by a small group of banks.” Many actors consider such products as growth opportunities[4].

However, the need for common standards in term of ESG labelling remains high. Various participants across stakeholder groups suggested an expansion of the EU Taxonomy to define brown or grey activities and cover considerations on the social dimension. The introduction of brown criteria into the taxonomy could enable a more standardised approach to exclusion policies, support the assessment of underlying risks of exposures by banks as well as by supervisors – which could allow consistency in supervision through common definitions - and improve disclosure of business activities in line with the taxonomy.

A common issue reported by banks is the difficulty to report while extending the integration of ESG factors into their lending and investment activity. Such ESG-related commitments are often formulated at a high level and lack adequate monitoring and targets. Most of the time banks are able to report only on specific products or certain sectors while it is highly technical and almost impossible to measure the entire portfolio exposure. The need to develop new approaches to actively steer the portfolio toward ESG goal is clearly identified. On this field, the report does not provide detailed tools or best practices that could be implemented. At Natixis, the Green Weighting Factor, launched in 2019, clearly answers to this challenge, at least on the Environmental pilar. Designed as a strategic tool to drive risk assessment as well as commercial perspectives of the bank, it has been deployed on the whole balance sheet of the bank and served as the bedrock of its freshly published 2024 climate strategy and 2050 net zero carbon target.

Challenges

Data challenges and a lack of common standards continue to be the most prevalent challenges faced by banks and supervisors alike.

In light of the widening scope of Sustainable Finance and considering the vital role of ESG risk integration into investment and financing processes, banks should now pay more attention to developing and strengthening their own ESG data aggregation and risk assessment methodologies, as reliance on third party data providers can only be treated as complementary to one’s own data and methodology, given the different approaches implied and the lack of transparency among the rating and data providing agencies.

The keys takeaways from the study can be summarized as recommendations which will nourish next steps of the EU commission’s Sustainable Finance Action Plan, increasing its scope on banks’ regulation and incentivization tools, the pace of implementation of which needs to be constantly accelerated.

[1] Final study: available here

[2] Most banks plan to assess ESG risks through both financial materiality and the material impacts of their activities on environmental and social issues

[3] Global Reporting Initiative (2020). GRI contribution to the EU public consultation regarding the proposal by the European Commission for regulation. Available here.

[4] The areas where respondents see most emerging business opportunities for ESG offerings are green loans, sustainability-linked bonds, transition bonds, electric car loans, and green mortgages across business segments.